ZUMZ - Shoe Carnival: A Painful Step

2023-11-22 21:42:22 ET

Summary

- Shoe Carnival has experienced weak performance in 2023, with revenue falling 6.4% and net income decreasing from $32.7 million to $21.9 million.

- The company saw growth in Shoe Station revenue and online sales, but overall comparable store sales fell 7.4%.

- Despite the recent weakness, Shoe Carnival remains a stable prospect with no debt and a surplus of cash and cash equivalents, making it a good buy.

Generally speaking, I am not a fan of the retail space. But the footwear retail space does intrigue me. One company within this industry that has historically done fairly well for itself is Shoe Carnival ( SCVL ). In fact, back in February of this year, I wrote an article discussing just how well the company had done. From November of last year through the time that the article was published, the stock was up 22.8% at a time when the S&P 500 was up only 3.8%. Even though shares of the business were attractively priced after that move higher, I ended up downgrading the stock from a ‘strong buy’ to a ‘buy’. But since then, things have not gone exactly as planned. Weak performance on both the top and bottom lines has pushed the stock down, with shares tumbling 14.5% while the S&P 500 has jumped 12%. Had fundamental performance continued to come in strong, this would have led me to upgrade the stock once again. But in light of the recent weakness from a revenue, profit, and cash flow perspective, I do still believe that a ‘buy’ rating is appropriate right now.

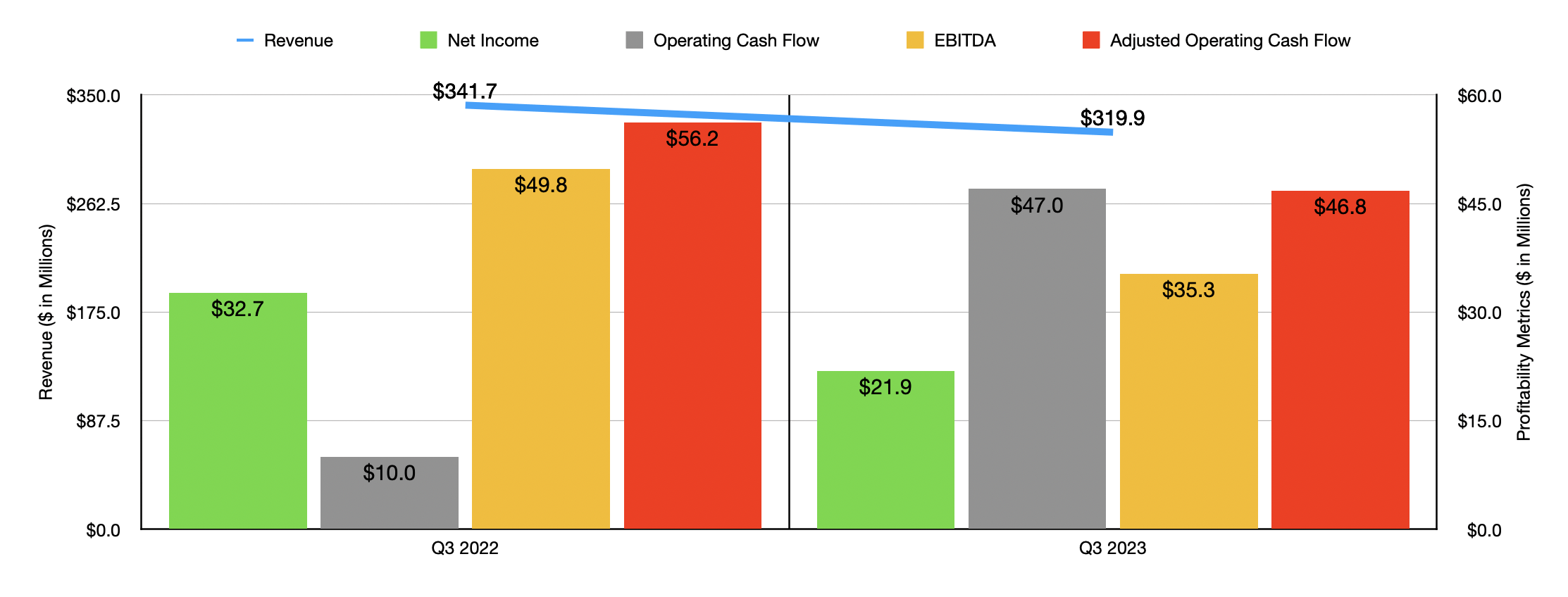

A step in the wrong direction

As I mentioned already, 2023 has not been a particularly pleasant year for Shoe Carnival. The latest example of this can be seen by looking at the third quarter earnings data that management just released on November 16th. Overall revenue came in at $319.9 million. That's 6.4% lower than the $341.7 million the company reported the same time last year. According to management, this weakness was really driven by ‘unseasonably hot weather’ in September and October that led to soft seasonal and non-athletic fall sales at the company's stores.

{kind=link}

This is not to say that everything was awful. Shoe Station revenue, for instance, grew at a low-double digit rate compared to the same time last year and the children's category of shoes grew at a low-single digit rate because of the back-to-school season. In fact, because of the strength of the back-to-school season, the children's category of products experienced the second-highest sales in the history of the company. Online sales came in particularly strong, jumping 10% year-over-year. But none of this stopped overall comparable store sales from falling 7.4%, with much of that weakness occurring after Labor Day.

With revenue falling, profits followed suit. Net income was cut from $32.7 million to $21.9 million. Other profitability metrics experienced the same trajectory. The one exception to this was operating cash flow. According to management, this skyrocketed from $10 million to $47 million. If we adjust for changes in working capital, however, we would see a decrease in operating cash flow from $56.2 million to $46.8 million. Over the same window of time, EBITDA for the enterprise dropped from $49.8 million to $35.3 million.

{kind=link}

It's important to keep in mind that the third quarter was not the only time in which the company experienced weakness. As you can see in the chart above, sales for the first nine months of 2023 as a whole were significantly weaker than the same nine months one year earlier. Year-over-year, the company experienced a 7.8% plunge in revenue. Naturally, profits and cash flows moved in the same direction. Net income fell from $88.5 million to $57.8 million. And although operating cash flow increased, both adjusted operating cash flow and EBITDA took a hit year over year.

For the year in its entirety, management is expecting revenue of between $1.16 billion and $1.18 billion. Comparable store sales are expected to be down by between 8.5% and 9.5%. Though the company should benefit by the addition of around six new stores. On the bottom line, management is forecasting net profits of between $72 million and $75 million. And operating cash flow should come in at between $105 million and $115 million. Based on my own estimates, this should translate to an EBITDA of somewhere around $119.5 million.

{kind=link}

Using these estimates, I was able to value the company as shown in the chart above. Because of the worsening financial picture, the business should go from a price to adjusted operating cash flow multiple of 3.2 using data from last year to a multiple of 5.9 this year. Meanwhile, the EV to EBITDA multiples should increase from 3.4 to 4.8. I then, in the table below, compared the company to five similar firms. On a price to operating cash flow basis, I found that Shoe Carnival ended up being the cheapest of the group. Using the EV to EBITDA approach, meanwhile, two of the five enterprises ended up being cheaper than it.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Shoe Carnival |

| 5.9 |

| 4.8 |

| Torrid Holdings ( CURV ) |

| 9.4 |

| 4.5 |

| The Children's Place ( PLCE ) |

| 29.8 |

| 13.7 |

| Chico's FAS ( CHS ) |

| 7.2 |

| 4.5 |

| Abercrombie & Fitch ( ANF ) |

| 8.2 |

| 8.7 |

| Zumiez ( ZUMZ ) |

| 32.4 |

| 14.4 |

What we have so far here is a business that is facing some near-term pressure. Yes, the stock is trading on the cheap, both on an absolute basis and relative to similar enterprises. But none of this means anything if the firm is not capable of withstanding continued pain in the market should that pain come to bear down on it. The good news is that Shoe Carnival does seem to be well-positioned on this front. As of the end of the third quarter of this year, the company had no debt on its books. It also enjoyed cash and cash equivalents of $71.1 million. Even with these difficult times, the company should generate significant extra cash flow. But even if that were to turn negative for a short window of time, this extra cash and the absence of debt gives management plenty of flexibility to do what they must in order to preserve the enterprise for the long haul.

Takeaway

At this point in time, Shoe Carnival might not be the best prospect on the market. The recent weakening in sales, profits, and cash flows are all a big negative for shareholders. But the stock has already fallen rather significantly and shares look cheap on both an absolute basis and relative to similar firms. The absence of debt and the surplus of cash and cash equivalents make the company a very stable prospect from a solvency and liquidity perspective. Add all of this together, and I do still believe that a ‘buy’ rating makes sense at this time.

For further details see:

Shoe Carnival: A Painful Step