CURV - Shoe Carnival: Its Run Isn't Over Yet

Summary

- Shoe Carnival has done really well as of late from a share price perspective, with investors experiencing significant upside.

- This is due to how cheap shares have been and has come in spite of a weakening of the firm's fundamental condition.

- Shares are still cheap and likely offer some nice upside, but the easy money has already been made.

More often than not, good investments take a while to pay off. Fortunately, however, there are some scenarios where returns come faster than expected. A great example of this can be seen by looking at recent performance achieved by Shoe Carnival ( SCVL ), a business that's dedicated to the sale of footwear through both traditional retail outlets and online channels. Despite a weakening in financial condition as of late, the firm is still performing reasonably well, all things considered. In addition to that, shares look quite affordable, indicating that further upside could very well be on the table. But because of changing market conditions, I do think that the company deserves a modest downgrade from the ‘strong buy’ I had it at previously to a ‘buy’ today.

Mixed performance comes into focus

Back in early September of 2022, I wrote an article that took a very bullish stance on Shoe Carnival. In that article, I talked about how the company had experienced a rather mixed operating history. Even though it was mixed, the performance over the past few years had been quite positive. Of course, all good things must come to an end, and that became abundantly clear when the business reported some weakness during its 2022 fiscal year. But given how cheap the stock was, I could not help but to rate it a ‘strong buy’ to reflect my view that shares should outperform the broader market to a significant degree for the foreseeable future. Since the publication of that article, the company has truly delivered. While the S&P 500 is up only 3.8%, shares of Shoe Carnival have seen upside of 22.8%.

{kind=link}

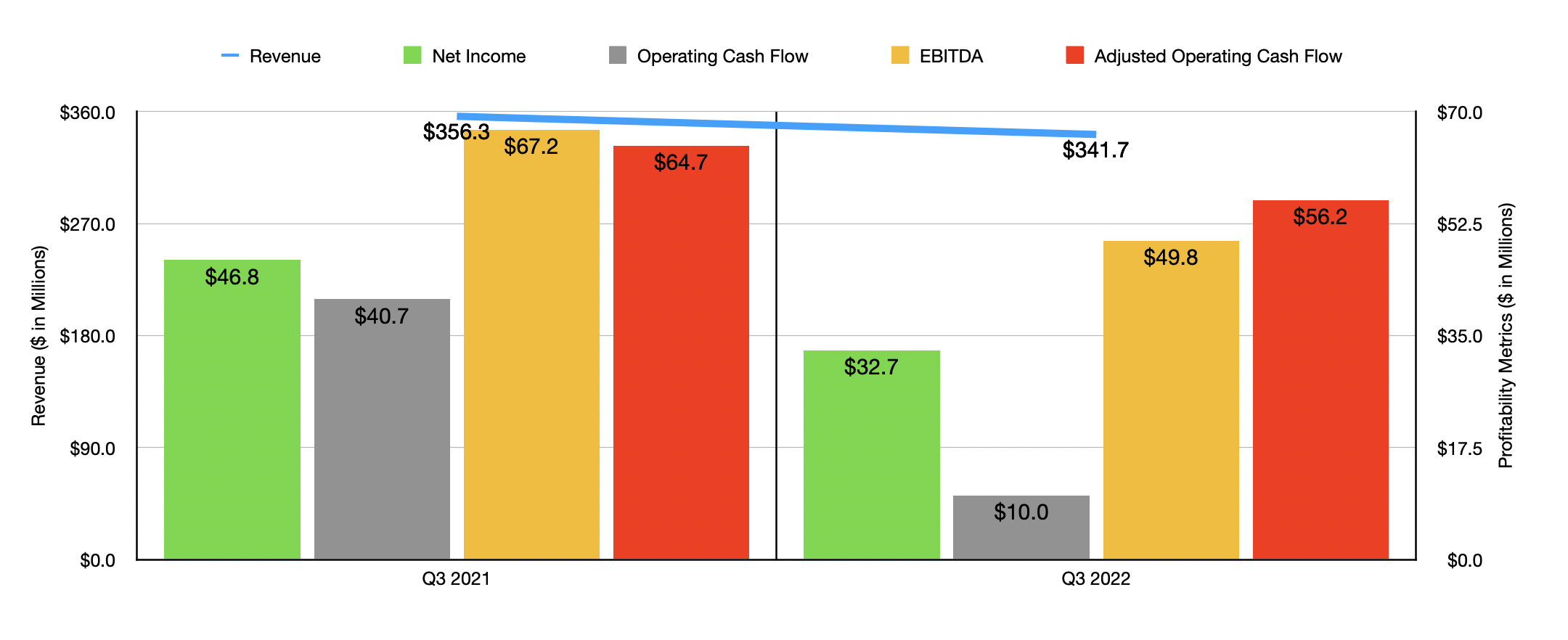

Interestingly, the share price performance achieved by Shoe Carnival has come about despite mixed and generally declining results. Consider how the company performed during the third quarter of its 2022 fiscal year. Sales for that time came in at $341.7 million. That's 4.1% lower than the $356.3 million reported the same time one year earlier. This decline came about despite the fact that the business saw the number of stores it had in operation grow from 377 to 395. The pain for the business was driven instead by a drop in comparable store sales. The real victim was a plunge in comparable store sales totaling 9.9%. Although bad, it is better than what the company reported for its first and second quarters, with declines totaling 10.6% and 13.8%, respectively. This decline seems to be related to a gradual return to normalcy following the COVID-19 pandemic.

This drop in revenue brought with it a decline in profitability as well. Net income for the business, for instance, managed to drop from $46.8 million to $32.4 million. However, there were other factors in this decline as well. The company's gross profit margin, for instance, shrank from 40.4% to 38.3%. This decline, management said, was due primarily to buying, distribution, and occupancy costs rising, as well as merchandise margins declining, with most of these changes attributable to higher inflation across the board. In addition to this, selling, general, and administrative costs, rose from 22.9% of sales to 25.5%. This rise, management asserted, was largely the result of its Shoe Station operations, as well as increased depreciation expense resulting from investments in property and equipment aimed at modernizing the company's stores. Other profitability metrics followed the same trajectory. Operating cash flow, for instance, plunged from $40.7 million to $10 million. If we adjust for changes in working capital, the metric would have fallen more modestly from $64.7 million to $56.2 million. And finally, EBITDA for the business dipped from $67.2 million to $49.8 million.

{kind=link}

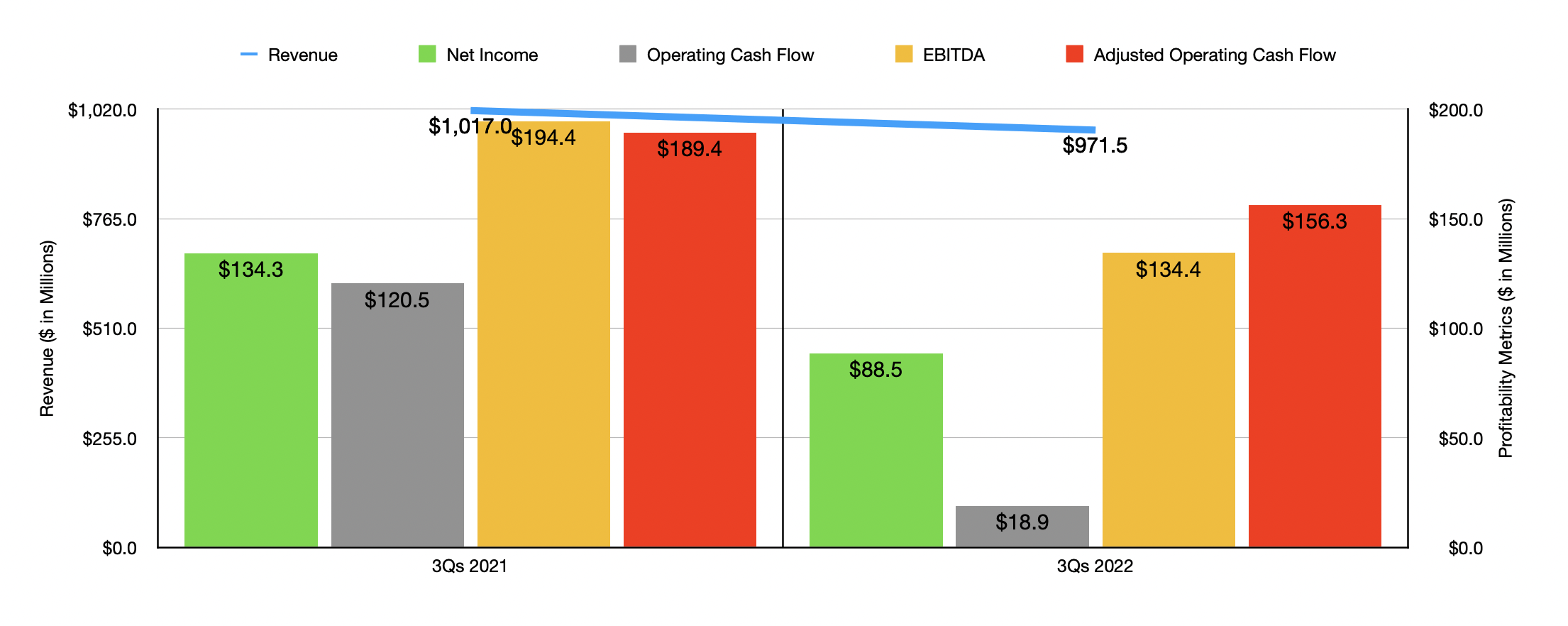

The results experienced during the third quarter of the year aided in pushing results for the first nine months of the year relative to the same nine months one year earlier, down. Revenue of $1.02 billion dropped to $971.5 million. Net income dropped from $134.3 million to $88.5 million. The decline in operating cash flow was even greater, with the metric plunging from $120.5 million to $18.9 million. But on an adjusted basis, the metric fell from $189.4 million to $156.3 million. And finally, we have EBITDA. It ultimately dropped from $194.4 million to $134.4 million. Despite these troubles, Shoe Carnival was happy to continue rewarding shareholders directly. The data revealed by management shows a combination of dividends and share buybacks amounting to over $40 million throughout the year. That brings total returns to investors over the past decade to $275 million. Even though the company has been allocating a lot of cash toward rewarding shareholders directly, this doesn't mean that they aren't focused on growth. In their third quarter earnings release, they said that they would open three additional locations by the end of 2022, taking their store count to 398. Their ultimate goal is to surpass the 500-store count in the next three to five years.

For 2022 in its entirety, management said that revenue should end up coming in at between $1.27 billion and $1.30 billion. Although this would represent a decrease compared to what the firm generated in 2021, it would still be between 23% and 25% higher than what the company generated back in 2019 before the pandemic. Adjusted earnings per share should be between $3.95 and $4.10. That should translate to net income, at the midpoint, of $111.5 million. No guidance was given when it came to other profitability metrics. But if we assume that the data reported for the first nine months of the year is indicative of what the picture will look like for the final quarter, then we should anticipate adjusted operating cash flow of $190.7 million and EBITDA of $160.4 million.

{kind=link}

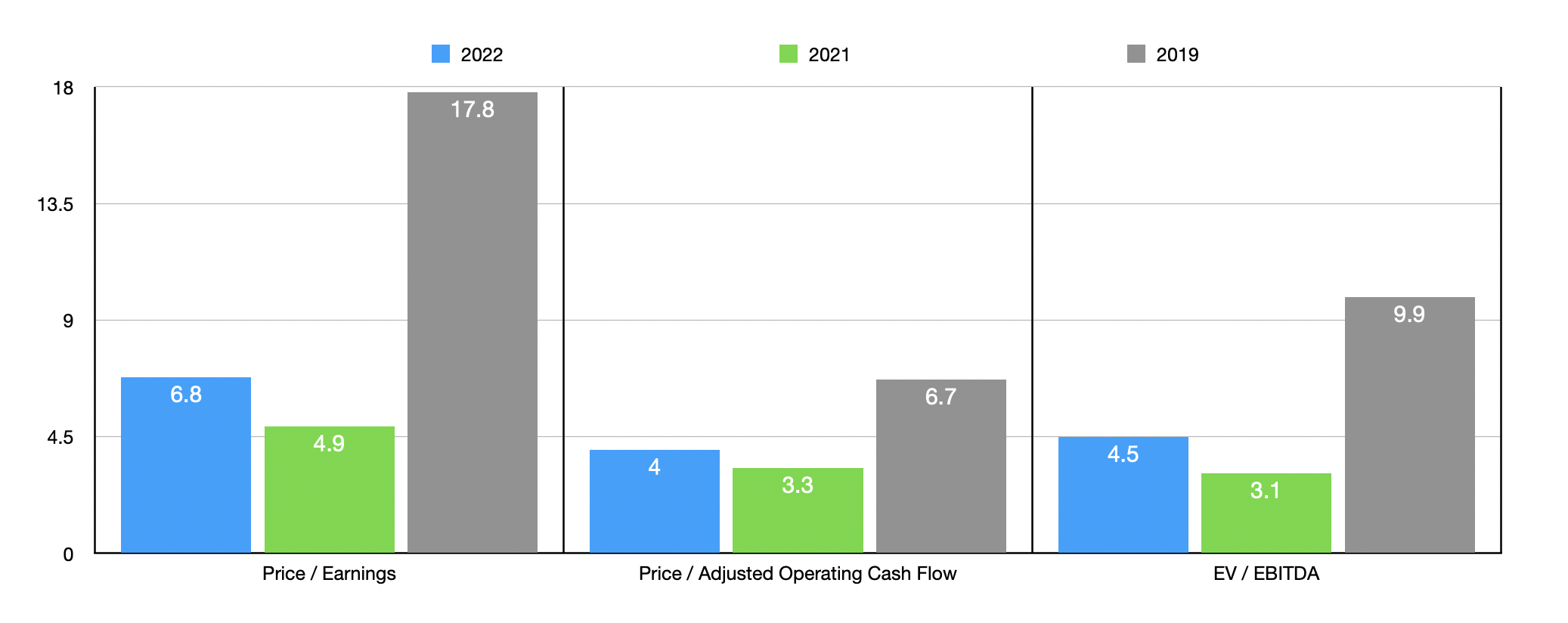

Based on these data points, Shoe Carnival is trading at a price-to-earnings multiple of 6.8. The price to adjusted operating cash flow multiples should be 4, while the EV to EBITDA multiple should come in at 4.5. As you can see from the chart above, this is a bit loftier than the multiples using data from 2021. But shares are still meaningfully cheaper than if we were to revert back to levels seen in 2019. Even a return to those levels, however, would likely result in some upside potential for investors. As part of my analysis, I also compared Shoe Carnival to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 5.7 to a high of 70. Only one of the five companies was cheaper than our target. Using the price to operating cash flow approach, the range was between 6.7 and 19.1. In this case, our prospect was the cheapest of the group. And finally, using the EV to EBITDA approach, we get a range of between 2.9 and 6.5. Three of the five companies in this case were cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Shoe Carnival |

| 6.8 |

| 4.0 |

| 4.5 |

| Torrid Holdings ( CURV ) |

| 10.2 |

| 6.7 |

| 3.3 |

| The Children's Place ( PLCE ) |

| 7.2 |

| 12.8 |

| 5.0 |

| Chico's FAS ( CHS ) |

| 5.7 |

| 11.0 |

| 2.9 |

| Abercrombie & Fitch ( ANF ) |

| 70.0 |

| N/A |

| 6.5 |

| Zumiez ( ZUMZ ) |

| 11.5 |

| 19.1 |

| 4.0 |

Takeaway

Based on all the data provided, I can only say that I am very pleased with the upside experience by Shoe Carnival since I last wrote about it. Even though I rated the company a ‘strong buy’, I had no idea that shares would move up that much that quickly. Shareholders certainly deserved the upside. The stock is still cheap today, but weakness does continue. Given how much upside shareholders have experienced, however, and given the weakness issues involved, I would make the case that a better rating at this time would be a ‘buy’, indicative of a company that should outperform the broader market without generating returns that are vastly superior to it.

For further details see:

Shoe Carnival: Its Run Isn't Over Yet