ROIC - Shop Till Ya Drop

Summary

- Americans love to shop.

- Buying stuff is a part of this country's DNA.

- In this article, we'll explore four of our favorite retail REITs.

Let's face it, Americans love to shop.

I know that better than anyone.

I have four girls and they love shopping.

I was a shopping center developer for over two decades, so I know the business model "from the ground up."

I live less than a mile away from Target ( TGT ), so I'm addicted.

And I'm a shareholder in Target, Lowe's ( LOW ), Tractor Supply ( TSCO ), Advance Auto Parts ( AAP ), and The Franchise Group ( FRG ).

I was also a franchisee for Papa John's Pizza ( PZZA ) and The Athlete's Foot.

Does that make me an expert?

No.

Not at all.

But I do like collecting rent checks as opposed to paying them. And even with the growth of e-commerce, I still go grocery shopping - I forgot to tell you that I'm a customer and shareholder in Ingles Markets, Incorporated ( IMKTA ).

Why do I like retail real estate investment trusts, or REITs?

First of all, due to their large footprint, there is a supply constraint for high quality retail outlets in metropolitan areas.

Secondly, shopping centers that are anchored by essential stores (such as a grocery store) are not likely to go away anytime soon. It's just so much more efficient to be able to pick up things at your convenience and run multiple errands at once.

The four REITs that are listed in this article are leaders in the industry and have very strong portfolios. Also, they have a solid financial position, and their dividend is very well covered.

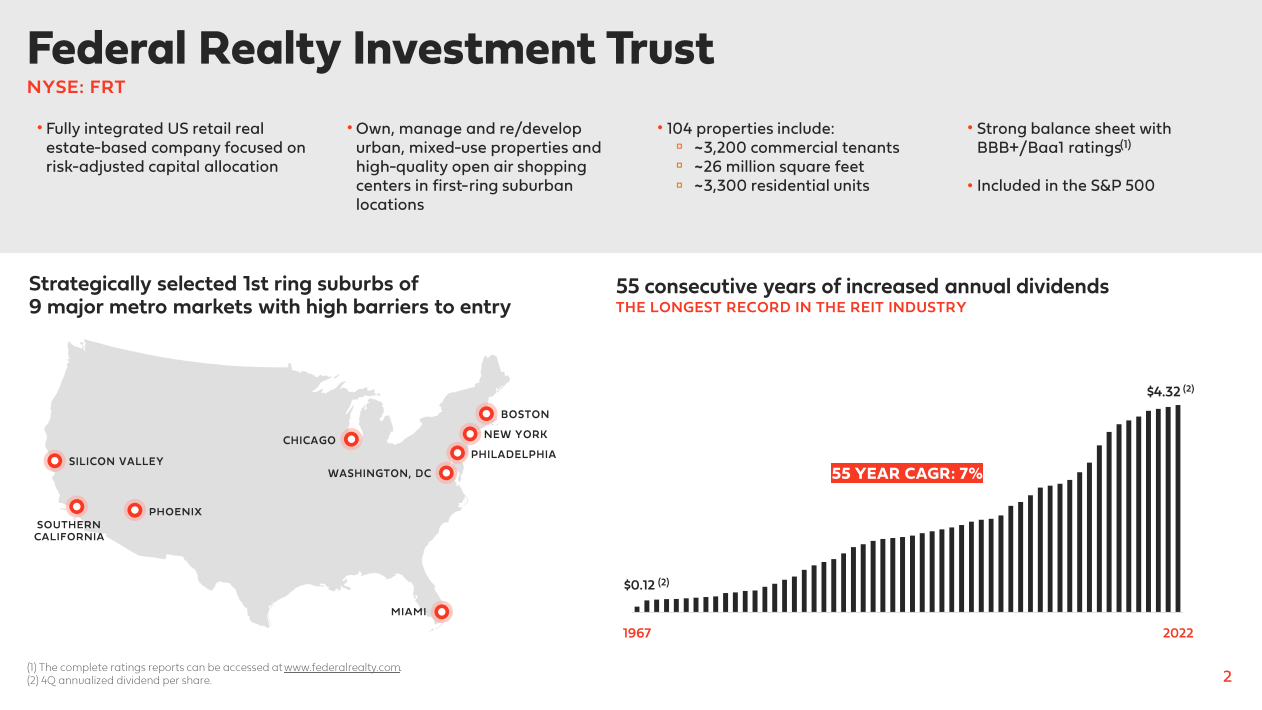

Federal Realty Investment Trust ( FRT )

Federal Realty Investment Trust is a REIT that primarily focuses on owning, managing, acquiring, and redeveloping a portfolio of high quality, retail-focused properties.

They own properties that will provide increasing cash flow over time, generate higher internal growth, and offer the potential for capital appreciation. Their portfolio is strategically placed in 9 major metro markets in the U.S., and these markets have a high barrier to entry that help limit competition.

{kind=link}

Federal Realty also has a pretty impressive record of dividend payment. They have increased their annual dividend payment for 55 consecutive years, which is the longest stretch in the REIT industry. Given their funds from operations, or FFO, interest coverage ratio is at 3.77x and FFO payout ratio is at 67.46%, I believe Federal Realty's dividend payment is safe at this point.

Federal Realty also has a strong balance sheet . Their annualized net debt to EBITDA is about 6x, and fixed charge coverage ratio is about 4x. Also, they have plenty of liquidity (over $1 B) to support their growth and weather a potential financial hardship from a recession.

The REIT has an investor grade credit rating from S&P and Moody's.

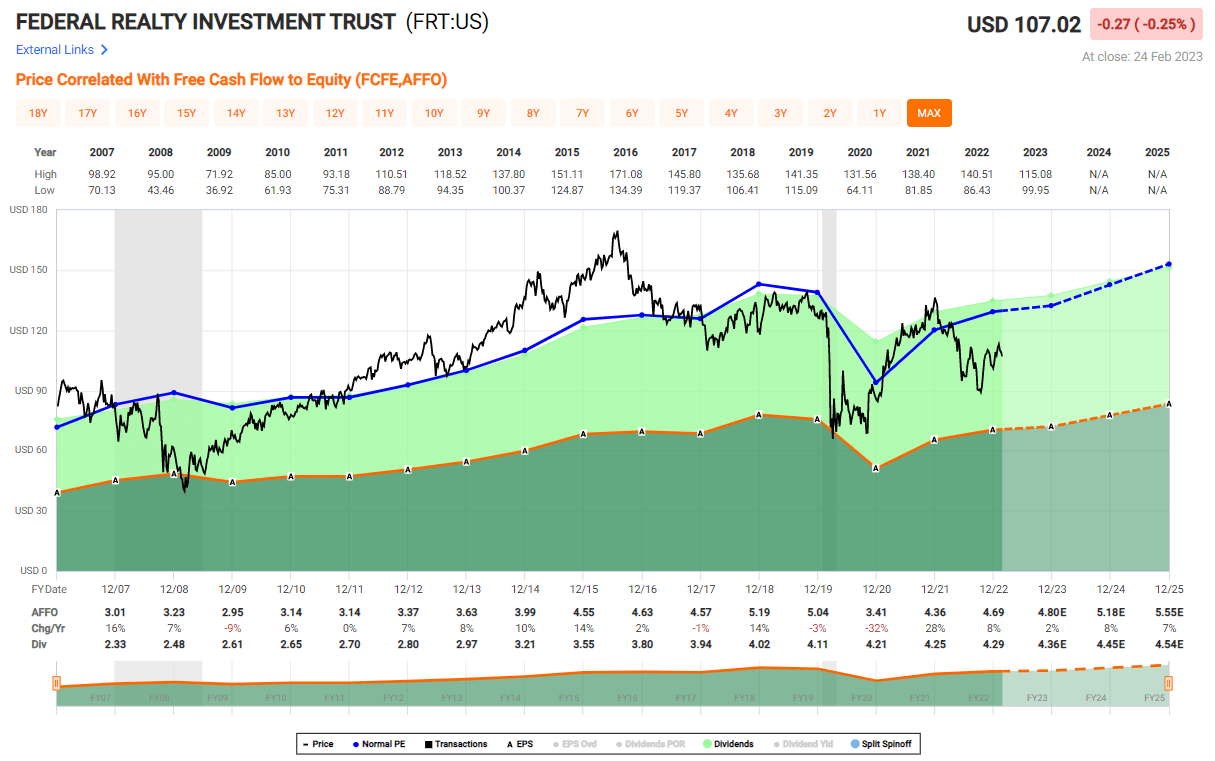

Looking at their valuation metrics, they are currently undervalued compared to their historical average. The P/AFFO of 28.23x and P/FFO of 16.62x are about 12% lower than their 5-year average. I expect their valuation to return to their norm in the future.

{kind=link}

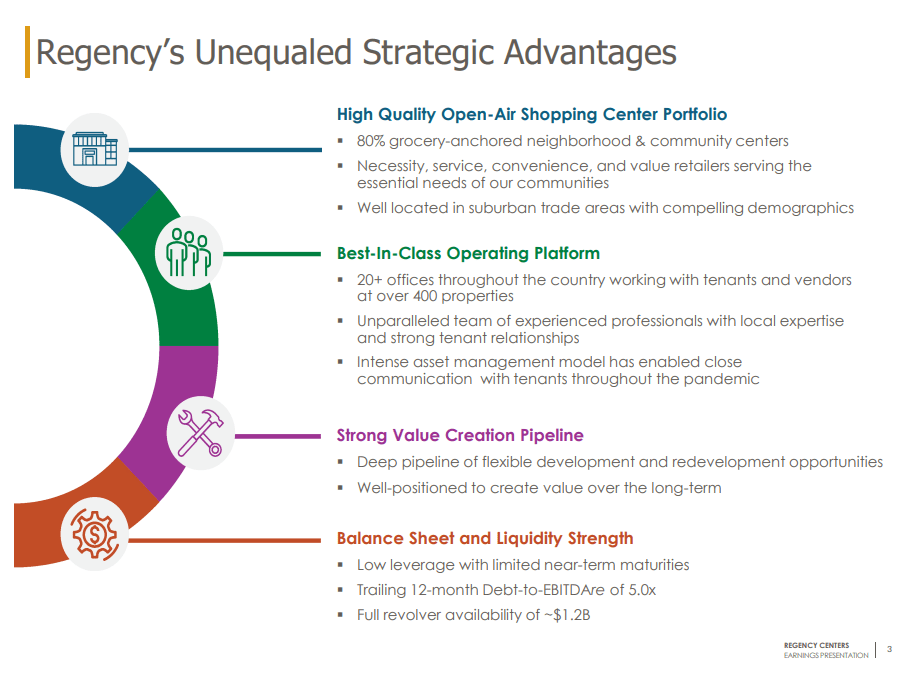

Regency Centers Corporation ( REG )

Regency Centers Corporation is a preeminent national owner, operator, and developer of shopping centers located in suburban trade areas with desirable demographics.

They have over 400 centers in their portfolio with over 50 M square feet. 80% of their portfolio is anchored by grocery stores and community centers, and their portfolio has a deep pipeline of development and redevelopment opportunities.

{kind=link}

Regency has a very strong balance sheet . Looking at their debt maturity profile, the debt is very well spread out until 2049. The weighted average interest rate is at 3.9%, and the weighted average year to maturity is at 8.3 years. Also, they have full revolver availability of $1.2B and an investment grade credit rating from credit agencies.

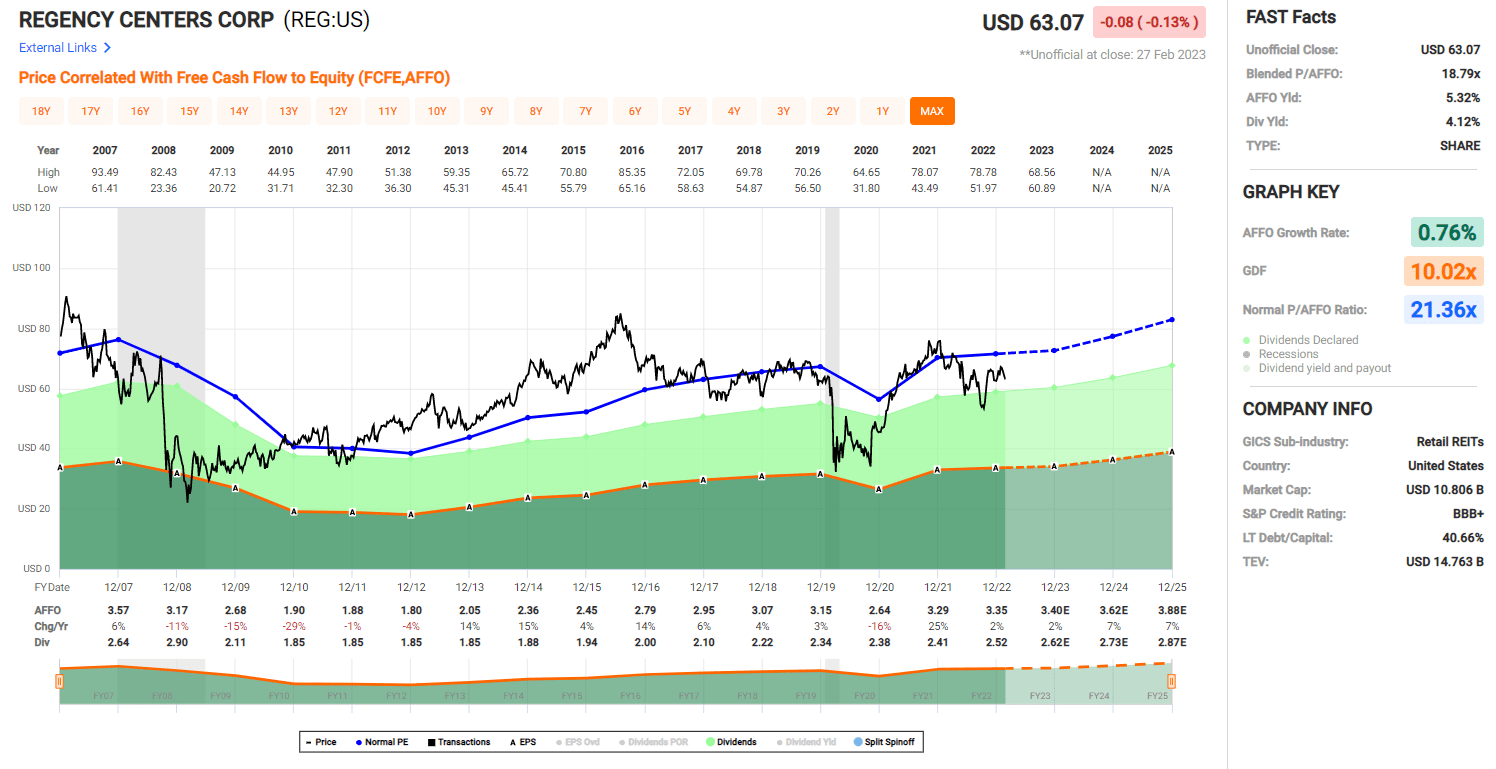

Looking at their valuation metrics, Regency is slightly undervalued at this point. Their P/AFFO of 20.54x and 15.57x are about 8% lower than their 5-year average. I fully expect them to recover to their average value in the near future.

Also , their dividend payment is safe at this point . Their cash dividend payout ratio is at 65.30%, and AFFO payout ratio is at 76.72%.

{kind=link}

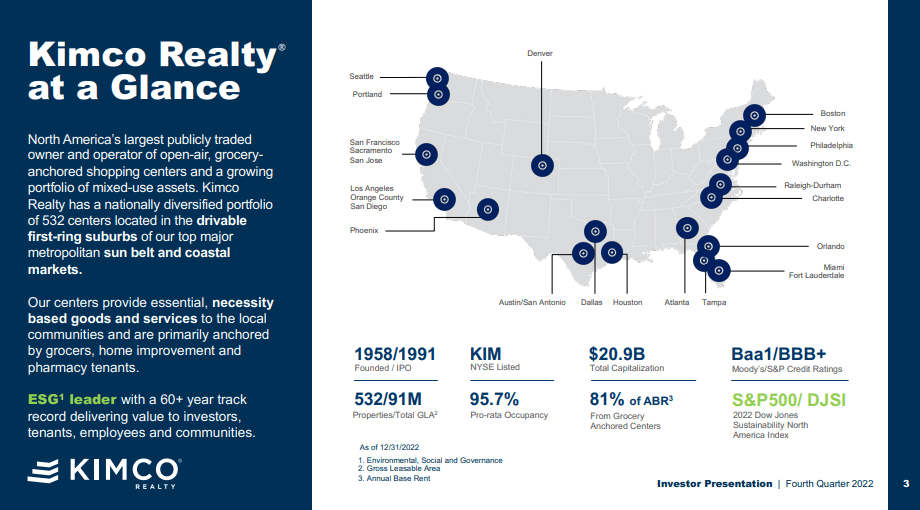

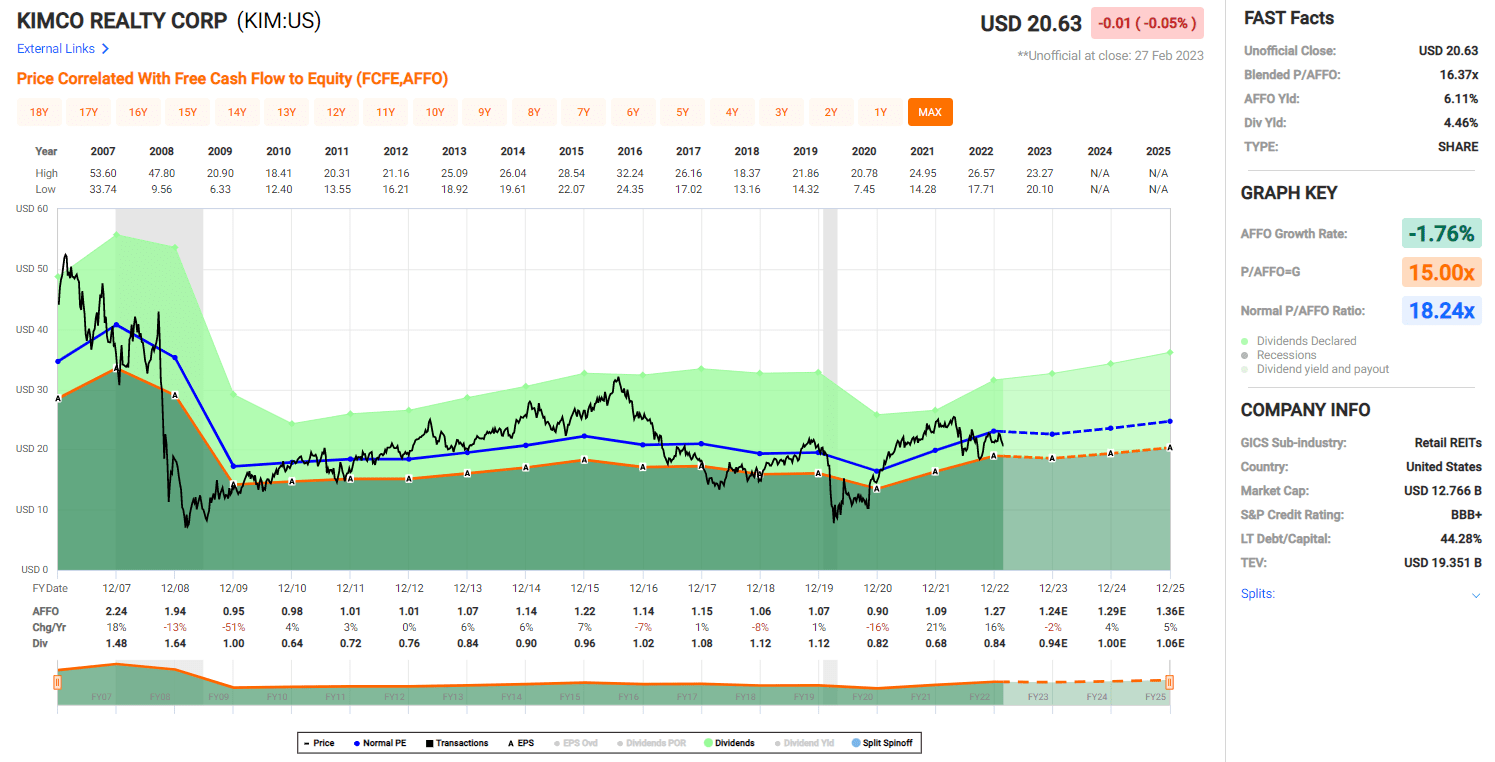

Kimco Realty Corporation ( KIM )

Kimco is North America's largest publicly traded owner and operator of open-air, grocery-anchored shopping centers, and a growing portfolio of mixed-use assets. Their mission is to create destinations for everyday living that inspires a sense of community and delivers value to their shareholders.

Kimco has over 500 properties, with a presence in most of the major U.S. metropolitan areas. In total, their properties span over 90 M square feet. Kimco has a very diversified tenant base, and their top tenants include ROSS, Amazon/Whole Food, and PetSmart.

{kind=link}

Kimco has a very strong balance sheet and financial capacity to support their growth. Their net debt to EBITDA is 6.4x, and fixed charge coverage is 4.1x. They have over $2.1 B of financial capacity.

The credit rating from S&P is at BBB+, and the rating from Moody's at Baa1. Their debt maturity profile is very well managed, and it's well spread over the next couple of decades.

Kimco is fairly valued at this point. Their P/AFFO ratio and P/AFFO ratio is within 5% of their 5-year average. Their dividend is very well covered and appears safe at this point. The cash dividend payout ratio is at 63.26%, and AFFO payout ratio is at 76.45%.

{kind=link}

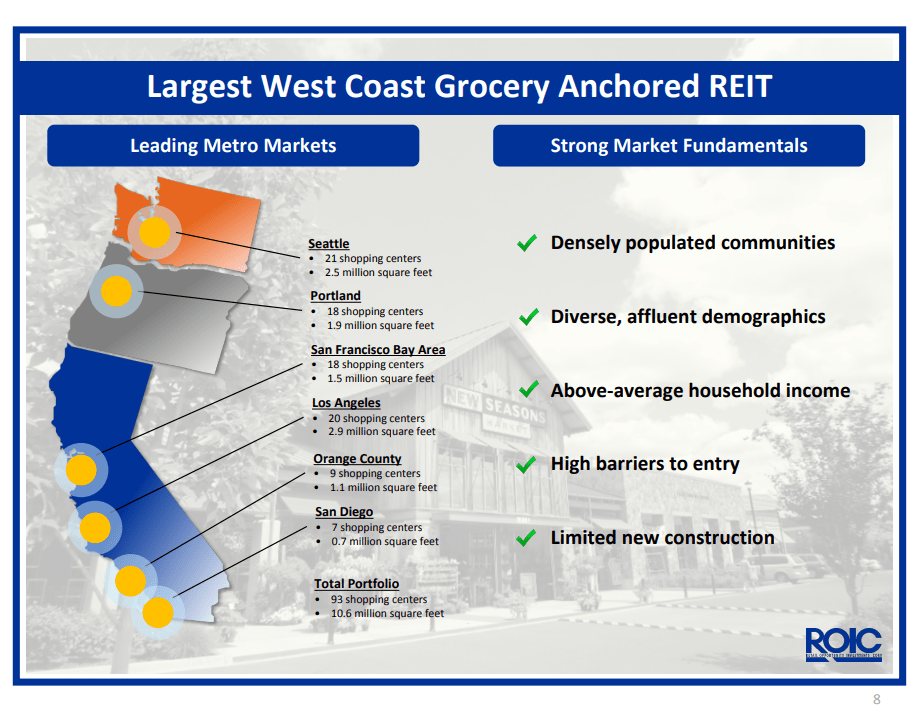

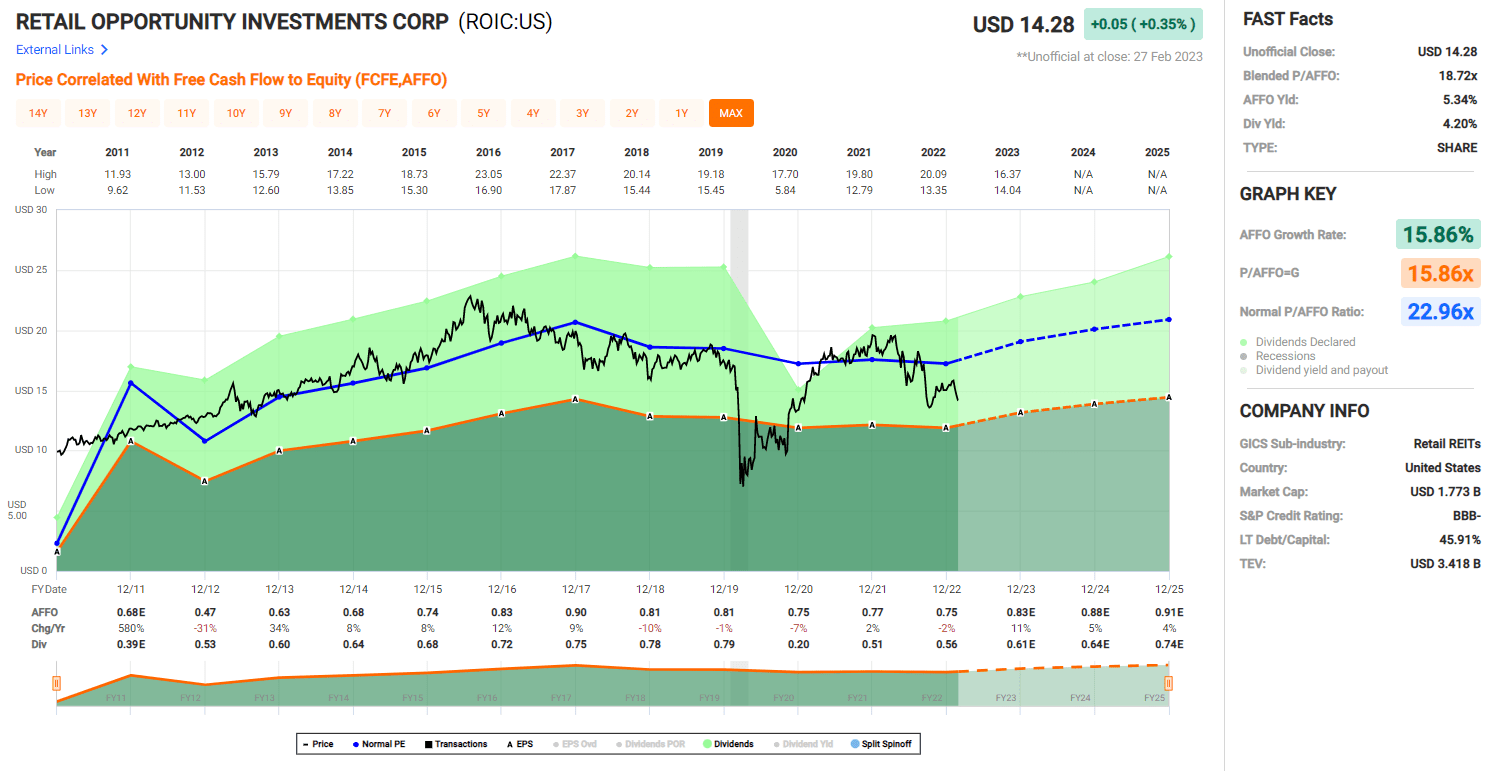

Retail Opportunity Investments Corp. ( ROIC )

Retail Opportunity Investments Corp is a REIT that seeks out shopping centers located in metropolitan areas with supply constraints. The company derives revenues primarily from rents and reimbursement payments from tenants under long term leases at the company's properties.

Their portfolio mostly consists of retailers that provide necessity-based, non-discretionary goods and services, catering to the basic and daily needs. Top tenants of Retail Opportunity include Albertsons, Kroger, Rite Aid, and Trader Joe's.

{kind=link}

Retail Opportunity has a very strong financial position. Looking at their debt maturity schedule, it is very well laddered over the next several years. Also, most of their debt is unencumbered. The interest coverage ratio is at 3.2x, and net principal debt/annualized EBITDA is at 6.6x.

Looking at their valuation, they are currently undervalued. Their P/AFFO of 18.31x and P/FFO of 13.22x are about 17% lower than their 5-year average. Also, iREIT Equity Rating Tracker shows a 21% margin of safety for Retail Opportunity.

Regarding the dividend, their dividend payment appears safe and well-covered at this point. Their cash dividend payout ratio is at 61.46% and FAD payout ratio is at 64.63%.

{kind=link}

Risks…

As many of us know, e-commerce is getting bigger and bigger, and brick and mortal stores are being threatened. Many items that people used to get from grocery stores or convenience stores are now being delivered directly to their doors.

Improvements in logistics and technology are also making it easier to deliver items, such as refrigerated items, that used to be considered hard-to-deliver. Therefore, a shopping center has to constantly come up with new solutions to protect themselves against e-commerce.

The inflation figure appeared to be trending down for couple of months and gave some energy to the stock market at the beginning of the year.

However, now inflation is showing some signs that it will stay little longer at the elevated level. The most recent inflation number was higher than the estimate, and it has increased market concerns that the Federal Reserve will maintain their hawkish stance for longer. If inflation stays high, and the Fed stays hawkish, this will hold the stock market down for a while.

Also, elevated rates reduce pricing power which will likely weigh on interest expense and leading to continued interest expense / refinancing headwinds.

In Summary…

Retail REITs have many intriguing features.

They are very close to our lives, and in fact many of their stores are essential to our lives. Since a retail complex takes up a large amount of real estate, there's strong geographical constraints, which limits supply in the metro areas.

This helps to preserve the value of a shopping center/mall and typically keeps values headed higher. Most shopping center REITs posted strong Q4-22 earnings results, supported by robust leasing and occupancy gains.

At iREIT we're maintaining a tactical strategy within the retail sector, insisting on owning the highest quality names, with an attractive margin of safety. The four REITs in this article have prime real estate and strong portfolios. They have very strong balance sheets and are in the financial position to weather a potential recession.

PS: Get ready for our March Madness REIT Bracketology series.

For further details see:

Shop Till Ya Drop