GEO - Short CoreCivic Against GEO: Both An Alpha Source And A Natural Hedge

2023-04-11 09:25:46 ET

Summary

- Two weeks ago I reiterated my long thesis on GEO.

- Given my bearish outlook for the broader market, I'd like to pair the long GEO trade with a short in CXW to hedge out the industry and market exposure.

- The level of EBITDA and business quality don't justify GEO's lower valuation multiples.

- On a standalone basis, CXW offers less upside than GEO.

- I think a long GEO and short CXW trade is a better risk/reward compared to an outright long in GEO at this point.

Situation Overview

Two weeks ago I reiterated my long thesis on The GEO Group ( GEO ). The central point is that while there are some near-term concerns, GEO's valuation has derated to a better risk/reward at ~$8/share. The guidance was conservative which is well setup for a guidance beat should the ICE population start to normalize. More importantly, taking a longer-term view, the deleveraging path of GEO will accrue value to the equity assuming the enterprise value stays relatively stable.

Over the course of the past two weeks, I've started to think more about the broader market and as the result of macroeconomics analysis and a review of my individual holdings, I've started to lay in a portfolio hedge to lower the overall market beta of my portfolio, as well as individual hedge to form pair trades. For my long GEO exposure, the most obvious candidate is to short CoreCivic ( CXW ) as a "lazy hedge". However, as I dug deeper I realized that even on a standalone basis CXW provides less upside than GEO and the current valuation discrepancy is not warranted. Therefore, I'm recommending a long/short trade for the next 6-9 months.

Valuation Comparison

Comparing the valuation multiples of CXW and GEO, it is clear that CXW is significantly more expensive than GEO. Based on the midpoint of their respective EBITDA guidance, CXW is trading at a multiple of 7.6x while GEO is trading at 5.7x, resulting in a valuation discrepancy of approximately 2.0x turns. To calculate the levered free cash flow, I used a uniform 28% tax rate, assumed D&A expenses of approximately $130 million, and took into account maintenance capex provided by both companies. As per my calculations, CXW is generating $217.9 million of unlevered cash flow and $130 million of levered cash flow, with the difference being roughly $85 million of interest expense. On the other hand, GEO generates a much higher unlevered free cash flow due to its higher EBITDA base, which is approximately $220 million higher. However, the interest expense for GEO in FY2023 is nearly $200 million, resulting in a significant difference between its unlevered and levered free cash flow. Overall, both on an unlevered and levered basis, GEO is trading at a cheaper valuation than CXW.

Author

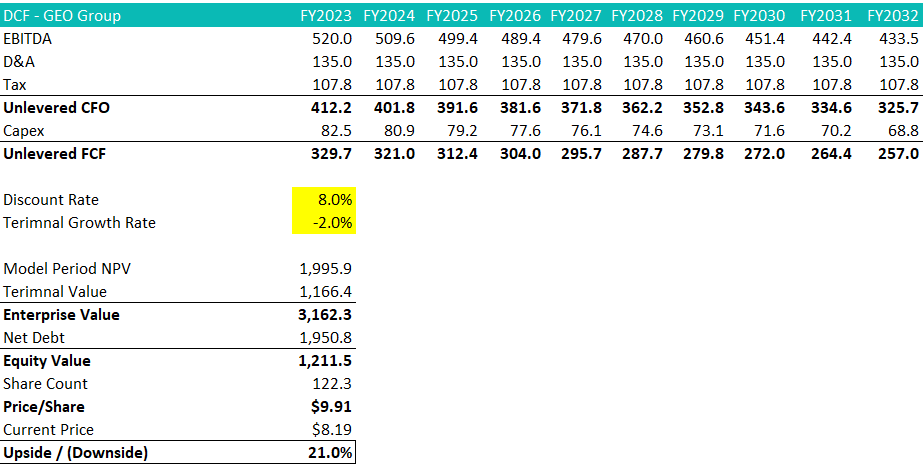

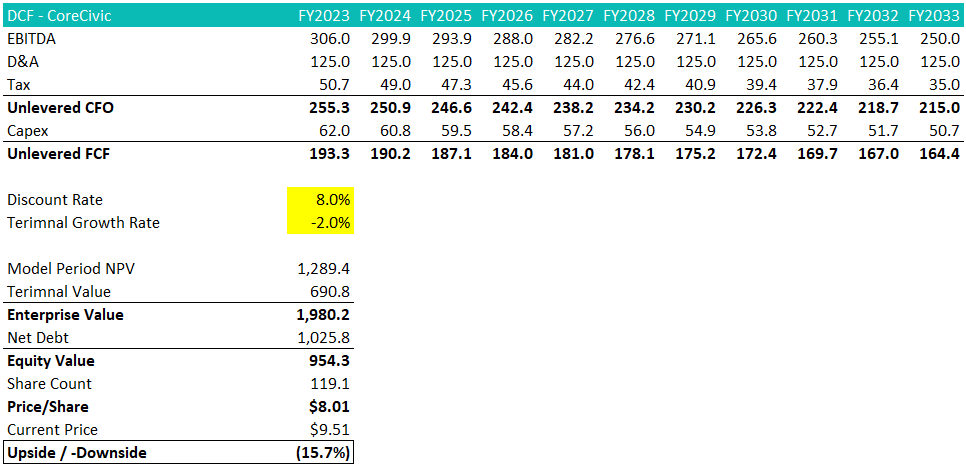

After applying a DCF framework to both GEO and CXW, I have found that GEO offers a greater potential upside under the same set of assumptions. Specifically, I assumed that EBITDA would decline by 2% annually in perpetuity, with maintenance capex requirements following this trend. I then discounted this declining free cash flow stream by 8%. Given that both companies are exposed to similar industry risks, I believe that using a consistent set of assumptions for a quick DCF analysis is appropriate. According to this framework, GEO is currently undervalued by 21.0%, while CXW is overvalued by 15.7%.

{kind=link}

Author

{kind=link}

Author

Business Quality Comparison

The next important consideration is whether the valuation gap between GEO and CXW can be justified by differences in the quality of their businesses. Based on my analysis, I believe that GEO should trade at a premium to CXW on an unlevered basis (i.e., not considering the difference in capital structure). This is due in large part to GEO's electronic monitoring segment, which has a higher EBITDA margin than CXW. As this segment is accretive to the consolidated margin, GEO has a structurally higher margin overall, which justifies a higher EV/EBITDA multiple.

Seeking Alpha

Beyond the pure quantitative comparison, having a dominant position in the electronic monitoring space is a natural hedge for the detention side of the business, which is currently in decline. The Intensive Supervision and Appearance Program (ISAP) is undoubtedly a more effective, cost-efficient, and overall better alternative to incarcerating people for 3-6 months while they wait for their court hearings. This is a huge advantage that CXW does not have. This advantage is apparent in the numbers as well. GEO's EBITDA previously peaked at ~$487 million in FY2019, but with the help of the exponential growth of the electronic monitoring segment, GEO's EBITDA reached a new high of ~$550 million in FY2022. On the other hand, CXW's EBITDA also peaked in FY2019 at $440 million, but because it doesn't have the natural hedge that GEO has, CXW's EBITDA guidance is only 70% of FY2019 level.

Seeking Alpha

Scenarios & Risks

Obviously the risk to the GEO/CXW pair is if CXW outperforms GEO. If a positive development happens for the entire private detention industry (e.g. lifting of Title 42), this long/short pair should do well as GEO is the higher-beta name. The ISAP factor is only specific to GEO as CXW doesn't have exposure to this as explained above. While GEO's management guided a decline in ISAP participants, since it's clearly a better alternative to incarcerating illegal immigrants, I believe there is still growth potential, which will only benefit GEO. The only scenario where I can see the GEO/CXW pair doing poorly is for CXW to accelerate shareholder return via either a sped up share buyback and/or initiating a common dividend.

The mitigating factor is that CXW's EBITDA is in decline and there is not much clarity on when it will return to growth, so I don't think CXW management is in any hurry to initiate a dividend, knowing that cutting or eliminating it later would greatly hurt the company's credibility (again). Facing a potential recession on the horizon, CXW probably prefers to keep ample liquidity as the industry still doesn't have good access to the financial markets. On the other hand, regardless of what happens GEO will be forced to delever and the value creation will accrue to the equity.

Conclusion

I could be missing something here (so please let me know in the comment section), but I think this is one of the most obvious relative value mispricing that I've seen in a while. CXW shouldn't trade at a premium to GEO on an unlevered basis given the business quality difference, and yet right now the market is awarding CXW and ignoring GEO. This relative opportunity exists perhaps because institutional money managers cannot touch this space due to ESG constraints, and so this mispricing is not being arbitraged away yet. The market doesn't care until it cares. I expect this valuation gap to close and reverse (i.e. GEO starts to trade at a premium to CXW) as my standalone thesis on GEO starts to play out. In any case, I believe shorting CXW against GEO can be a good alpha source alone, but also a great hedge against the industry and equity market exposures.

For further details see:

Short CoreCivic Against GEO: Both An Alpha Source And A Natural Hedge