VTV - Should You Be A Factor Or Dividend Investor?

2023-11-17 08:56:32 ET

Summary

- Dividend investing is often looked down upon by factor investors, but research shows that dividends play a crucial role in long-term investment returns.

- Factors like market, size, and value have been identified as key drivers of investment returns, but implementing factor strategies can be costly and may not outperform simple index funds.

- Global evidence supports the importance of dividends, with studies showing that dividend stocks outperform non-dividend paying stocks and contribute significantly to total returns.

Global Evidence for the Superiority of Dividend Investing: A Comparative Analysis of Dividend vs Factor Investing

I am often perplexed as to why the topic of dividends causes such consternation within the personal finance community. It seems to be one of a handful of issues that can cause serious disagreement. This is especially true in the factor investing camp, where members routinely, look down on dividend investors as uninformed. The factor investment argument goes like this: You are far better off targeting factors rather than dividends. Dividend investors would retort with an argument that focuses on the dividend income, as if they get paid in addition to holding the stock. This is incorrect.

In this piece I want to explore the misconceptions around dividends and do an exploration of the research on dividends vs factor investing. I will end with my conclusions based on the evidence of who wins the dividend investing vs factor investing argument not by looking exclusively at research but the results of real funds, that real investors could have invested in, in the real world.

Introduction to Factor Investing

Put simply factors in their modern form, come from the research done by Kenneth French and Eugene Fama, who found that the decomposition of investment returns comes down to exposure to certain risk factors. These risk factors, they argue, are embedded in market structures and thus tilting a portfolio towards these factors will allow one to outperform over the long run.

They identified three factors, market, size, and value, that together make up the three-factor model. Market is the return from moving from the risk-free rate to the equity market. Size is the tendency for small cap stocks to beat large cap stocks, and finally, value, is the tendency for things that are cheap to beat things that are expensive. A further iteration of the model added profitability and investment, to create the five-factor model. This is a very simplistic view of the factors but for our purposes it will work to give you a basic understanding of factor investing.

Discrepancies of Research vs Practice

Fama, and French produced outstanding research but implementing it was another matter. Few realize that their so-called "premiums" for value investing came from the use of a long/short portfolio, not offered to real investors.

In addition, for a long period of time, getting exposure to the strategies that implemented an iteration of this research required one to pay a high-priced financial advisor an annual advisory fee, then pay additional costs to be invested in their portfolio of mutual funds that were tilted toward the factors.

Any outperformance that was created was usually eaten up by the advisory fees. Today, investors have access to a broad array of factor-based investment products through the introduction of factor ETF's offered by a number of providers including iShares, Vanguard, DFA, and Avantis to name a few. Still challenges of implementation remain. (See my previous piece The Problem with Factor Investing for a more detailed analysis.)

Let us use the following factor investing model as an example to represent "the factor portfolio":

| DFUSX |

| DFA US Large Company I |

| Large Blend |

| 20% |

| DFLVX |

| DFA US Large Cap Value I |

| Large Value |

| 20% |

| DFSCX |

| DFA US Micro Cap I |

| Small Blend |

| 10% |

| DFSVX |

| DFA US Small Cap Value |

| Small Value |

| 10% |

| DFREX |

| DFA Real Estate Securities |

| Real Estate |

| 10% |

| DFIVX |

| DFA International Value |

| Foreign Large Value |

| 10% |

| DFISX |

| DFA International Small Company |

| Foreign Small/Mid Blend |

| 5% |

| DISVX |

| DFA International Small Cap Value |

| Foreign Small/Mid Value |

| 5% |

| DFEMX |

| DFA Emerging Markets |

| Diversified Emerging Markets |

| 3% |

| DFEVX |

| DFA Emerging Markets Value |

| Diversified Emerging Markets |

| 3% |

| DEMSX |

| DFA Emerging Markets Small Cap |

| Diversified Emerging Markets |

| 4% |

| TOTAL |

| 100% |

Looking at the last 20 years of data available for this portfolio, we can see that the factor portfolio produced a return of 9.69% vs 9.79% for the unmanaged and ultra-low-cost S&P 500 index fund. Even worse, this was before deducting the fees for the advisor that was needed to gain access to the factor portfolio. When we do this calculation, the returns come down to 8.69%. What makes this even worse, as we can see below, is that the factor portfolio also carried more risk for less return, as is evidenced by the Sharpe, and Sortino ratios. Also, with a 0.96 correlation level, the factor portfolio is startlingly similar to the market portfolio meaning you have a closet index fund.

So, investors who paid their advisor the 1% per year, and the investment manager higher investment management fees, year after year for 20 years, got nothing in return, and actually lost money compared to a simple S&P 500 index fund with rock bottom costs. Now let's analyze dividend investing.

Portfolio Visualizer/Authors Calculations

{kind=link}

The Mechanics of Dividends

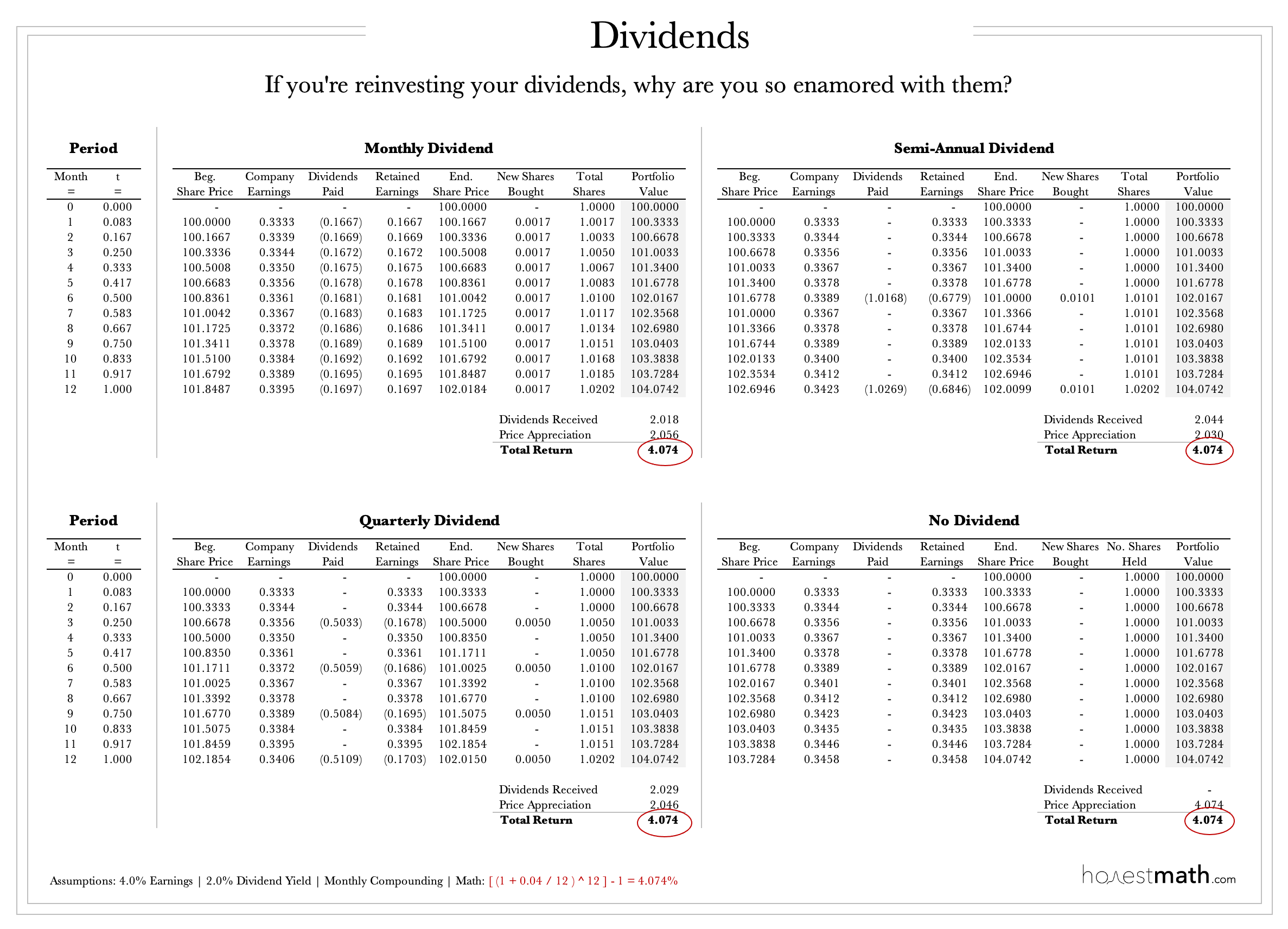

Dividend investing comes in a number of strategies. There are those who target high payout, or high yield, and those who target dividend growth, some combine the two. Let's begin by talking a bit about the mechanics of dividends so everyone is on the same page. Much of the correcting done by factor investors is when a dividend investor talks about getting "paid" to hold a security, incorrectly thinking this comes on top of their investment holdings. This is not actually how dividends work.

When a corporation does business and has additional capital in retained earnings, they have a decision to make. Do they take that capital and buy back their own stock, invest in the business, or return that capital to shareholders? The total value of a business is encapsulated in the price of a security, this is the notion of an efficient market, that all available information is embedded in the price. So, when a dividend is paid out, the company reduces the price of their stock to pay the dividend.

For example, let's say XYZ Inc is trading for $100/share. They decide to pay a $1 dividend to shareholders of record as of December 1. The share of the stock will be reduced by $1 on the ex. date, and you the shareholder will have a $99/share stock, and $1 in dividend income.

{kind=link}

From this illustration, we see that regardless of dividend policy the investor is in the same place. So now that we have a good understanding of what a dividend is, the question remains whether targeting corporations based on dividend policy is a good investment strategy. Based on this graphic many would likely conclude it is not. To better answer this question, we have to look at the global evidence.

Global Evidence for Dividend Investing

In their text, Triumph of the Optimists: 101 Years of Global Investment Returns , authors Dimson, Marsh, and Staunton (2002) examined the composition of asset returns in both the US and U.K. market from 1900-2000. Their research found that long term returns were driven by reinvested dividends. In fact, the return from reinvested dividends was 85 times that of a portfolio consisting of capital appreciation alone. The chart below demonstrates their findings.

Triumph of the Optimists

"Figure 11-2 shows the equivalent UK returns both with and without dividend reinvestment. With dividends reinvested (the green line), an investment of £1 made at start-1900 in the UK stock market would have grown to £16,160 by the end of 2000. By coincidence, this is very close to the terminal wealth of $16,797 from a $1 investment in the US market. Since UK inflation was higher than US inflation, the United Kingdom had an annualized real return of 5.8 percent compared with 6.7 percent in the United States. If dividends had been spent rather than reinvested, the UK investment of £1 would have grown to just £149 (the red line), a nominal return of 5.1 percent. Over the same period, UK consumer prices rose 55-fold, so this corresponds to a real capital gain of 1 percent per year, compared with 2 percent real in the United States. The longer the investment horizon, the more important is dividend income. For the seriously long-term investor, the value of a portfolio corresponds closely to the present value of dividends. The present value of the (eventual) capital appreciation dwindles greatly in significance. The analysis above shows why, throughout this book, we have stressed the importance of dividends in computing total returns." (Pg 151)

Additional research by Robert Arnott of Research Affiliates further proves the importance of dividends to long term investment returns. In a 2003 editorial in the Financial Analysts Journal , entitled Dividends and the Three Dwarfs, Arnott explored the returns of equity securities for 200 years, ending in 2002. He found that dividends were the most important component of return. Of the total annualized return for the period of 7.9%, 5.0% of that was from dividends, 1.4% from inflation, 0.6% from rising valuation levels, and 0.8% from real growth in dividends. He states:

"The importance of dividends for providing wealth to investors is self-evident. Dividends not only dwarf inflation, growth, and changing valuation levels individually, but they also dwarf the combined importance of inflation, growth, and changing valuation levels. This result is wildly at odds with conventional wisdom, which suggests that, while the return from bonds is wholly dependent on income, stocks provide growth first and income second. It is startling to realize that dividend growth has averaged less than 1 percent above inflation during the past 200-year period. And it is shocking that real per-share dividend and earnings growth on the S&P 500 Index since 1965 has been zero…" He ends "Dividends, unequivocally, matter."

Financial Analysts Journal

In a further global study of equity returns, entitled The Importance of Dividend Yields in Country Selection , in the Journal of Portfolio Management, A. Michael Keppler, studied the relationship between a firm's dividend yield and their overall return. He found that an investment in the highest yielding quartile, produced the best investment return overall.

Journal of Portfolio Management

This is further demonstrated in Triumph of the Optimists: 101 Years of Global Investment Returns. In the 10th Chapter, the authors show the cumulative returns from 1926 to 2000 of U.S. stocks that rank each year in the highest or lowest yielding 30% of companies. They found that higher yielding stocks outperformed their low yielding counterparts, 12.2% to 10.4% respectively. Demonstrating again the importance of dividends.

Triumph of the Optimists

Often cited, Wharton School Professor Jeremy Siegel wrote a book entitled The Future for Investors . In this text he ranks the components of the S&P 500 by dividend yield, for the time period 1957-2002. He found that the highest yielding stocks beat their lowest yielding counterparts and the S&P 500 index.

The Future for Investors

A further look at stock returns by dividend policy from 1973-2022 found that stocks with dividend payers and dividend growers in particular beat their counterparts who did not pay a dividend or cut their dividend.

Ned Davis Research and Hartford Funds

Given the global evidence I have presented it would seem that dividends surely matter to the total returns one can expect from equity securities. But let's go a step further and look at the components of the total return from the S&P 500 index from 1922-2022. During this 100 years of market data, the CAGR was 3.45% when we exclude dividends and adjust for inflation. $1 invested in 1923 grew to $30.65. When we include dividends the CAGR skyrockets to 7.51%, a 118% increase causing $1 invested in 1923 to grow to $1,497.24. Considering that the average yield on the 10-year Treasury from 1922-2022 was 4.73%, it is not overstating to say that relative to the risk-free rate, all of the premium from equity investing comes from dividends.

Conclusion: Real World Results

In conclusion, the data demonstrates that dividend stocks beat their non-dividend paying counterparts. The evidence on dividend investing is robust, and global in nature. The real question for investors is how to implement these strategies in their investment portfolios. For equity income investors, a factor-based strategist would tell you that you are better off buying a large cap value fund, as they are targeting the same risk factor of value stocks. But when we look at the implementation, we see a different analysis.

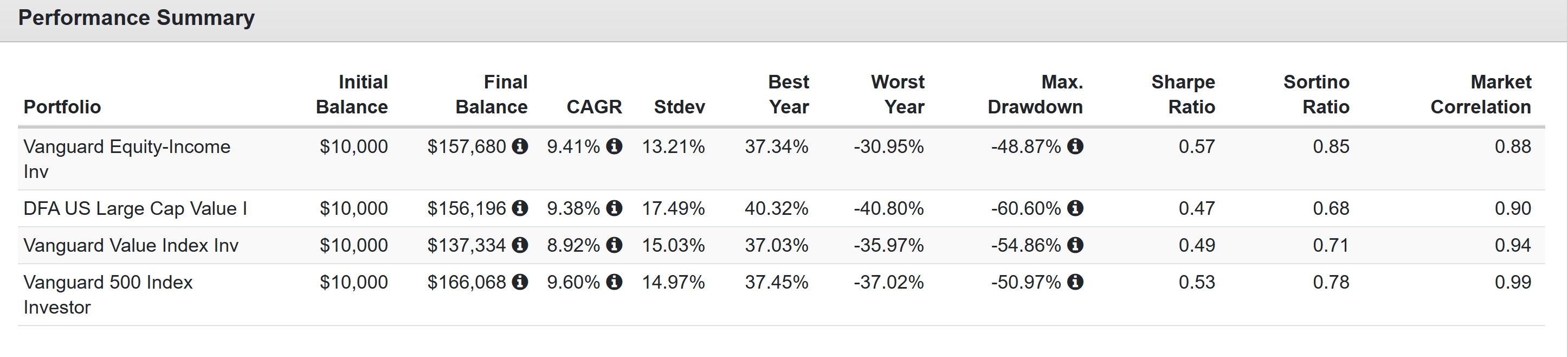

So, let's compare two representative examples of dividend investing vs. factor investing. In order to get the most data, we are going to use Vanguard Equity Income fund ( VEIPX ) vs DFA US Large Cap Value I ( DFLVX ). I have also included the Vanguard Value Index ( VIVAX ) and the S&P 500 Index ( VFINX ) for comparison purposes.

Portfolio Visualizer/ Authors own Calculations.

{kind=link}

From its inception in March of 1993, an investor who chose the factor strategy and invested in DFA US Large Cap Value I achieved a return of 9.38%, which underperformed the Vanguard Equity Income Fund by 3 bps. What was worse was that the DFA fund exhibited 32% higher volatility and had a lower Sharpe and Sortino ratio over the period, both ratios that indicate your return per unit of risk. So not only did the dividend fund beat the factor fund, but it did so at lower volatility and lower risk per unit of return.

Let's look at some international funds in practice to see if our evidence holds.

In this analysis we compared the Vanguard Intl. High Dividend Yield Index ( VYMI ) and the Vanguard Intl. Dividend Growth Index ( VIGI ) against a similar factor portfolio of DFA International Value ( DFIVX ) and DFA International Core Equity ( DFIEX ), both portfolios are equally weighted 50/50. Unfortunately, this data set only goes back to 2017, but in that period, the Vanguard International Dividend Portfolio returned 6.05% vs 5.22% for the factor portfolio, which also had 20% higher volatility. Again, it achieved these results with less risk and a better overall Sharpe and Sortino ratios.

Portfolio Visualizer/Authors own Calculations

{kind=link}

In conclusion, we have ample evidence from academia, live data indexes, and testing from real strategies which were tested in both domestic and international markets, to conclude that the debate between factor funds and dividend investors is over, and dividend investors won.

For further details see:

Should You Be A Factor Or Dividend Investor?