NVO - Should You Buy Baxter Or DaVita After The Fallout From The Ozempic Trial?

2023-10-12 10:54:14 ET

Summary

- Novo Nordisk ended its kidney outcome trial early after interim results showed the efficacy of its drug-Ozempic in delaying the progression of chronic kidney disease.

- Stocks of medical equipment major, Baxter International, and kidney care servicing specialist, DaVita, have faced significant declines since the news.

- We posit why the market may be overreacting to the news.

- We analyse other facets of BAX and DVA and believe that the former is a better buy at this juncture.

Novo Nordisk Ignites A Fire

A couple of days back, pharma major- Novo Nordisk A/S (NVO), dropped a bombshell by stating that it was bringing to close its kidney outcome FLOW trial (which had been in place since 2019), well ahead of schedule.

The objective of the trial was to ascertain if the company’s drug - Ozempic , which contains the active ingredient – Semaglutide (a GLP-1 agonist), was effective in delaying the progression of chronic kidney disease (CKD), and reducing the risk of death linked to renal and heart challenges. Note that over 3,500 candidates (across 28 countries), with type 2 diabetes, and CKD, had enrolled for this clinical study.

Interestingly enough, the decision to put an end to this trial was not taken in isolation by NVO, but rather, taken on the advice of an independent data monitoring committee, that was satisfied with the interim results which proved the efficacy of the drug in meeting “certain pre-specified criteria”.

Whilst this development is no doubt great news for NVO, the same can’t be said for medical equipment major - Baxter International (BAX), and kidney care servicing specialist - DaVita Inc (DVA). This is validated by the beating that both stocks have faced since the news came out; BAX is down by -12% whilst DVA is down by -17%.

DVA and BAX- Key Victims For Now, But Are Market Participants Jumping The Gun?

Why have these stocks reacted so poorly to the news?

Prima facie, the fact that the effectiveness of the drug was able to come through just in an interim study and not the whole study, provides some indication of what a promising alternative this could be in managing kidney diseases compared to the dialysis-oriented status quo.

For DVA, this feels like a particularly pronounced blow, as it is one of the two big players providing dialysis services in the US (last year, US dialysis revenues accounted for a whopping 91% of group sales).

In that regard, BAX is better placed, as it has a wide product base, beyond just dialysis products, but it too will have to take it on the chin. We say this because its Renal Care (dialysis therapies) and Acute Therapy (mainly renal replacement therapies) divisions contributed close to 30% of group sales last year. Then, even as recently as H1-23, renal care sales still accounted for the largest chunk of group sales (one-fourth).

Quarterly report

Admittedly, as part of its quest to become a more focused and nimble entity, BAX intends to spin off its renal care and acute therapy division in July-2024 , but given this latest Ozempic development, surely there will be some downward adjustments to the value-unlocking target that management initially had in mind.

Having said all that, it's worth pondering if this is a classic market overreaction, as a lot of things are still up in the air, and we won’t have definitive clarity until the FLOW is read out in H1-24. It’s also worth highlighting that the drug won’t cure CKD or stop it, but it will rather only slow the progression, which means there will still be an ample market for dialysis servicing and products that BAX and DVA are involved in, particularly considering the surprisingly rapid pace by which diabetes looks set to afflict the youth of this country. Every day, 170 people with diabetes get into kidney failure treatments, and this is unsurprising when you consider that 1 in 3 adults with diabetes suffer from CKD. The growing incidence of adverse climate events will also only give another leg up for CKD.

Besides, this drug is not going to suit every Tom, Dick and Harry; for instance, recent research has shown that patients who take GLP-1 medications such as this, face the risk of developing pancreatitis, bowel obstruction, and gastroparesis.

All in all, by the looks of it, this CKD wave will likely only snowball over time, and we are not necessarily convinced that Ozempic will serve as an adequate and consummate panacea in addressing the challenges.

What To Do With BAX and DVA Now?

Whilst this is not pleasant news for either BAX or DVA, it’s worth pondering if there’s a bargain-hunting opportunity here, given the magnitude of the selloff.

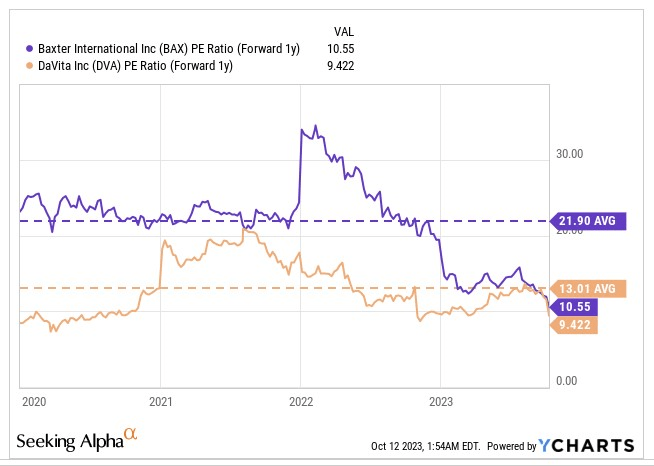

Well, from a forward valuation perspective, both stocks look remarkably cheap, particularly the former. On a 1-year forward P/E basis (based on the FY24 EPS), BAX can currently be picked up at a whopping discount of well over 50% relative to its long-term P/E average of roughly 22x. With DVA at 13x forward P/E, the discount differential versus its average isn’t as attractive, but it is still sizeable enough at 27%.

{kind=link}

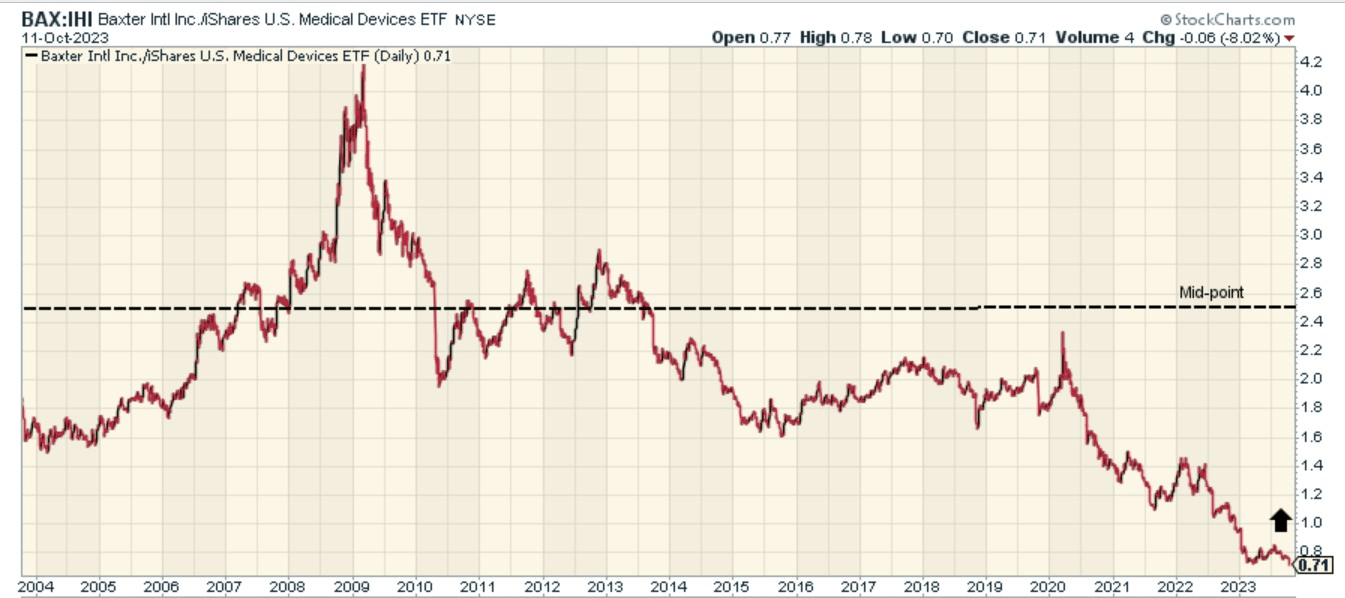

We also view these stocks as ripe candidates for rotation within their respective universes. The first chart highlights how oversold BAX looks relative to its peers from the medical equipment space, with the relative strength ratio currently at record lows!

{kind=link}

Then, whilst DaVita’s relative strength versus other healthcare providers is not yet at record lows, it is still around 50% off the mid-point of its long-term range, raising the prospect of some decent mean-reversion momentum.

{kind=link}

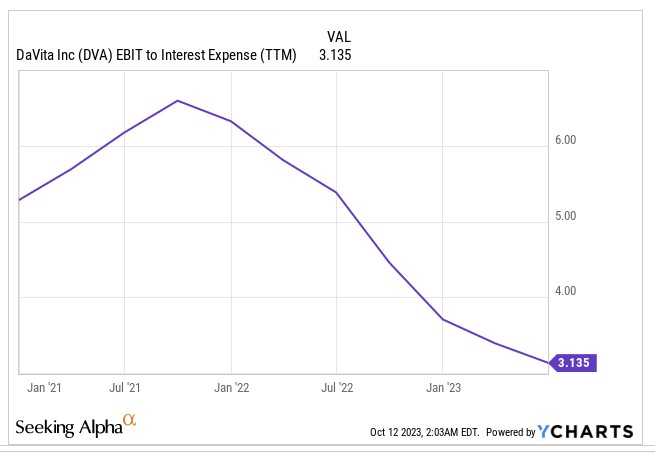

Nonetheless, whilst the valuation and rotational prospects for DVA look enticing, we do have some concerns about the elevated financial leverage that the company is coping with. As things stand, DVA’s leverage ratio is at 3.7x, above its target range of 3-3.5x. It also doesn’t reflect well that the 5-year CDS on its senior debt is currently at its highest point since the onset of the pandemic.

Also consider how its interest coverage has halved in recent periods. Management has also reiterated that despite having the authorization to buyback shares to the tune of $1.6bn, they won’t be in a position to get into this anytime soon.

{kind=link}

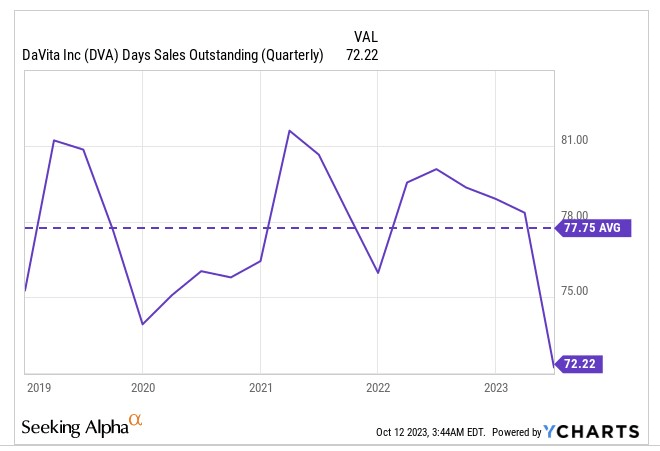

In the recently concluded Q2, the company benefited from seasonal patterns which we’re not convinced will necessarily linger. Even otherwise, the guidance on volumes will at best be flat, or more likely a decline of -3%. Management was also keen to point out how revenue per treatment ((RPT)) and FCF dynamics were benefitting from better collections, but we wonder if they can extract any further benefits here as the DSO (Days in Sales outstanding) levels have already dropped well below the 5-year average.

{kind=link}

With BAX, we are prepared to be a little more optimistic. Firstly, it is a more diversified play than DVA, and will be less impacted by adverse developments on the Ozempic front. Then, also note that the company’s FCF (free cash flow) this year will likely double and operating margins in H2-23 will expand by 200bps as it will likely extract better leverage from an improving topline.

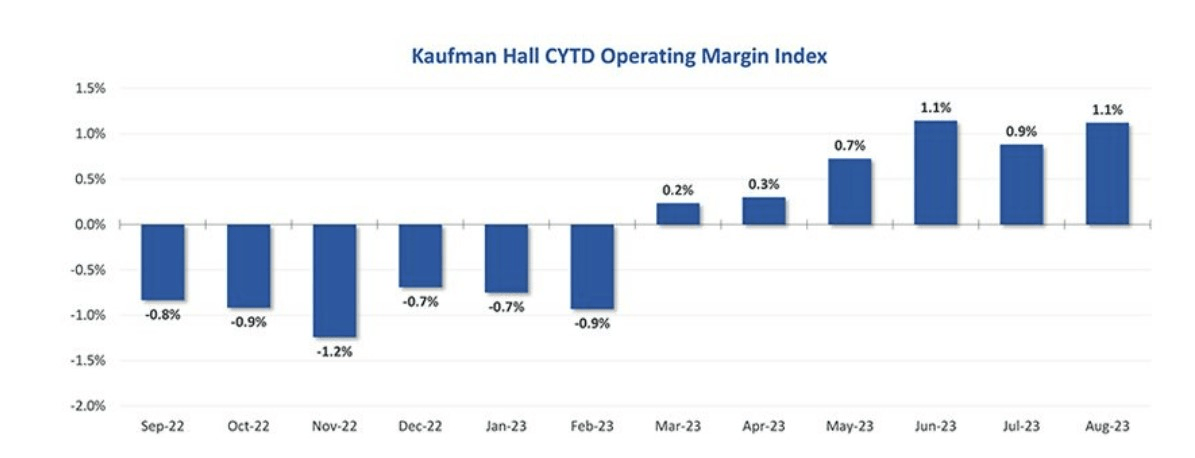

We are also enthused to note that conditions in their end markets appear to have stabilized, with better hospital volumes and a pickup in procedural volumes. Management expects capital spending plans of hospitals to pick up , and we could be inclined to go with that view, as the financial profile and the operating margins of hospitals are now in a better place (as highlighted in the image below). Even before this encouraging outlook, BAX was already witnessing a 30% sequential pickup in orders for their hospital beds.

{kind=link}

Finally, it is also worth considering that unlike DVA, BAX also offers a useful dividend (the current yield of 3.5% is more than 2x higher than the 4-year average), and its cash position is likely to be enhanced even further next year, when it receives around $4.25bn in cash proceeds from the sale of its BioPharma Solutions Division.

Considering all these factors, we would reiterate our BUY rating on BAX and go with a HOLD rating on DVA.

For further details see:

Should You Buy Baxter Or DaVita After The Fallout From The Ozempic Trial?