ELMUY - Should You Buy Telenor For Its High-Dividend Yield?

2023-06-21 09:36:19 ET

Summary

- Telenor offers a high-dividend yield, but its dividend sustainability is questionable due to it not being supported by recurring earnings and free cash flow generation.

- The company has a strong presence in Scandinavian countries and growth opportunities in Asia, but its exposure to Asian countries contributes to higher revenue and earnings volatility.

- Telenor's dividend yield is attractive in the short term, but long-term income investors should be cautious until the company can cover its dividend with its own earnings and cash flows.

Telenor ( OTCPK:TELNY ) offers a high-dividend yield, but its dividend sustainability is not great and the risk of a dividend cut should not be overlooked by income investors.

Company Overview

Telenor is the incumbent telecom operator in Norway, with a strong presence across Scandinavian countries and some growth opportunities across Asia. Its major shareholder is the Norwegian State, with a stake of 54%. Its current market value is about $15 billion and trades in the U.S. on the over-the-counter market.

Its operations include the offering of mobile and broadband services to residential and business customers, plus the offering of a broad range of wholesale services. It’s also a leading provider of television and broadcasting services in the Nordic countries. Beyond its domestic market, it also operates in Sweden, Denmark, and Finland, while in Asia it is present in Thailand, Malaysia, Bangladesh, and Pakistan.

While in Scandinavia the company’s geographical footprint is not expected to change much in the near future, on the other hand Telenor has been making some de-risking measures in its Asia footprint. It performed a merger of its Thai operations with Charoen Pokphand Group at the end of last year, it sold its Myanmar operations, while it also made a merger of operations in Malaysia with Axiata Group Berhad.

Following these transactions, Telenor now holds equity stakes in both the Thailand and Malaysia’s operations, being therefore deconsolidated from its accounts. This means that from a geographical perspective, Telenor will be more concentrated in less countries, with Norway’s weight on total revenues increasing from 22% to about 31%, remaining the largest market for the company, followed by Bangladesh, Sweden, and Finland.

In Norway, Telenor has a leading position across mobile, broadband and TV, being the market leader in each segment, with market shares ranging from 28%-43%. Its largest competitor is Telia ( OTCPK:TLSNY ), which enjoys market shares between 18-35% depending on the segment. The two companies’ combined hold some 78% of the mobile market in the country, which means market concentration is quite significant, which bodes well for the profitability of established players.

In other Nordic countries, Telenor does not hold leading positions, being nevertheless a large player in each market, being a competitor to larger local companies, such as TDC in Denmark or Elisa ( OTCPK:ELMUY ) in Finland. Generally speaking, Nordic markets are mature and have somewhat muted growth prospects over the long term, while on the other hand Telenor’s exposure to Asia gives it better growth prospects in the long haul.

However, its exposure to Asian countries also contributes with higher revenue and earnings volatility, for instance from currency movements, plus it also increases Telenor’s political risk. A good example was Myanmar’s coup in 2021, which led the company to write-down its operations in the country and subsequently dispose them for some $105 million. While Telenor received $50 million at the closing of the transaction in 2022, the remaining value is to be received over the next five years in equal installments, but the company decided not to book the remaining value in its accounts due to the uncertain situation in the country.

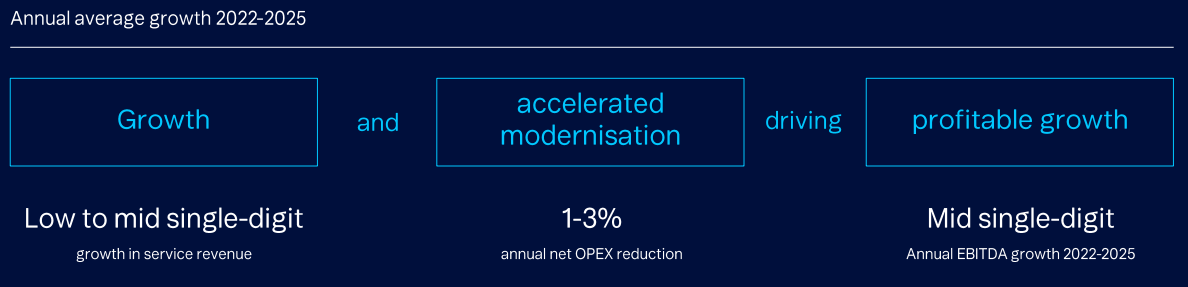

Beyond its Nordic and Asian operations, Telenor also has some adjacent businesses, such as infrastructure which it can potentially monetize as some other European operators have done recently, which can be important to generate value over the next few years. Despite that, reflecting the company’s relatively low growth prospects, its financial targets are to grow revenues at low to mid-single digit from 2022-25, reducing annual expenses by 1-3%, and growing earnings by mid-single digit during this period.

These aren’t particularly impressive growth targets as usual within the telecom industry, even though Telenor’s Asia exposure gives it somewhat better prospects when compared to other European incumbent operators.

{kind=link}

Financial targets (Telenor)

Financial Overview

Regarding its financial performance, Telenor’s track record can be considered positive compared to its peers, as the company has been able to grow its revenues slightly in recent years, while its profitability level is higher than average due to its leading position across relatively concentrated markets.

In 2022 , Telenor reported positive service revenue growth, increasing by 2% YoY, supported by strong growth in Denmark, Sweden, and Bangladesh, while Norway and Pakistan were among the weakest markets. Over the past year, some 53% of the company’s revenues were generated in the Nordic countries, 43% in Asia and 3% in others.

Its total revenues amounted to $9.3 billion during the year, an increase of 1.85% YoY, while its EBITDA was $4 billion (+5.4% YoY). This represented an EBITDA margin of 43%, a slight improvement from the previous year, a good result considering higher energy costs that negatively impacted its profitability in 2022, which were offset by other measures, such as the decommissioning of the copper network. Its reported net profit was above $4 billion, as Telenor booked a one-off gain from the deconsolidation of its Malaysia operations, while its adjusted net profit was about $1.3 billion.

During the first three months of 2023 , Telenor maintained a positive operating trend in its mobile services revenue, especially in the Nordic markets (+4.8% YoY), leading to overall service revenue growth of 3% YoY. Its EBITDA increased by 2% YoY, a smaller increase than revenue, as operational expenses increased by 4% YoY due to rising costs across the group, of which higher energy costs in Asia had the most impact on the group’s total costs.

{kind=link}

Costs (Telenor)

Regarding its bottom-line, the company booked another one-off gain related to its Thailand operation, boosting its net income in Q1 to $1.7 billion.

Regarding its infrastructure assets, Telenor signed a deal in February to sell 30% of its fibre business to KKR and a domestic investor, for an enterprise value of around $3.4 billion. This will allow Telenor to increase its free cash flow generation in 2023, which is also expected to be boosted by cost synergies in Asia, and lower capex needs in the Nordic markets. Its free cash flow is expected to be about $1.05 billion in 2023, a slight increase compared to the previous year, a trend that is expected to remain in the next few years as the company is targeting lower capital intensity in the next few years.

Regarding its balance sheet, Telenor’s leverage position is good compared to its peers, given that at the end of Q1, its net debt-to-EBITDA ratio was 2.1x, within its medium-term target range of 1.8-2.3x. This compares well with other European telecom companies, which have leverage ratios above 2.5x, which means Telenor’s balance sheet is in a strong position and can distribute a large part of its earnings to shareholders.

Indeed, its dividend history is quite good, considering that it has delivered a growing dividend over the past few years, as shown in the next graph.

Dividend (2023)

Its last annual dividend , related to 2022 earnings, was increased to NOK 9.30 ($0.87) per share, an increase of 3.3% YoY. Its dividend payout ratio compared to reported profits was quite low (about 31%), but this includes one-off gains, thus compared to its adjusted profit its dividend payout ratio was above 100%.

Furthermore, its dividend outflow is about $1.24 billion (considering its two distributions, one made last May and another one in next October), which is not covered by its free cash flow. This is a worrying sign regarding its dividend sustainability, even though the company seems to be committed to provide a growing dividend over the long term.

Indeed, its dividend per share is expected to grow over the next couple of years, which is also supported by recent share buybacks, even though is not expected to be covered by free cash flow until 2025. This explains to some extent why Telenor is currently offering a high-dividend yield of about 8.3%, as the market clearly does not see its dividend as sustainable over the long term. Therefore, while its yield is clearly attractive and a dividend cut is not expected to happen in the short term, for long-term income investors Telenor seems to be risky until the company is able to cover its dividend by its own earnings and cash flows.

Conclusion

Telenor offers one of the highest dividend yields across the European telecom sector, but this is due to questionable dividend sustainability given that its dividend is not supported by recurring earnings and free cash flow generation. Considering that a sustainable dividend payout ratio would be around 70% of its annual earnings, its ‘sustainable’ dividend would be quite lower than its current level and Telenor’s yield would be below 6%, more in-line with its peers. For this reason, Telenor does not seem to be a good income investment right now, at least until its dividend sustainability improves and the risk of a dividend cut is reduced in a meaningful way.

For further details see:

Should You Buy Telenor For Its High-Dividend Yield?