INFL - Should You Sell INFL As Inflation Slows Down?

Summary

- INFL invests in stocks with significant exposure to inflation, and which have outperformed as inflation skyrockets.

- Should investors be concerned about INFL as inflation moderates?

- No, at least I don't think so.

Author's note: This article was released to CEF/ETF Income Laboratory members on January 8th.

I've covered the Horizon Kinetics Inflation Beneficiaries ETF ( INFL ), an actively-managed ETF which invests in U.S. and international companies with the potential to outperform as inflation rises, twice in the past twelve months. Both times, I argued that INFL's effectiveness as an inflation hedge made the fund a buy. Both times, inflation has come in at very elevated levels, and the fund has outperformed, as expected.

Several readers have asked me about INFL these past few weeks, concerned about the impact that slowing inflation could have on the fund's performance. In my opinion, the impact should be negative, but not incredibly significant. INFL's underlying equity investments generate strong revenues and earnings at current prices . Inflation easing means revenues and earnings stabilize at reasonably strong levels, which should provide reasonably good returns moving forward. Inflation easing plus slower growth would likely result in some short-term pain, due to worsening investor sentiment, but fundamentals would remain good, as would long-term expected returns.

In my opinion, and considering the above, long-term investors should be confident in holding INFL long-term, at least at current prices and valuations. On the other hand, short-term traders might consider selling the fund as inflation eases and investor sentiment worsens, as doing so would lead to the strongest overall returns. Do bear in mind that timing the market successfully is difficult, and, in my opinion, unnecessary for a fund like INLF.

INFL - Quick Overview

A quick overview of the fund before looking at how it might perform during a period of slowing inflation. I have a longer, more in-depth look at the fund itself here .

INFL is an actively-managed ETF, investing in companies with the potential to outperform as inflation rises, or in inflation beneficiaries. The fund's strategy is quite particular, but effective, and explained in detail here .

In simple terms, the fund focuses on hard asset, capital-light companies.

Hard asset companies are those that derive most of their revenues and earnings from a tangible asset base, hence hard asset. As an example, the Texas Pacific Land Corporation ( TPL ), the fund's largest holding, generates most of its revenues and earnings from leasing oil-rich land. TPL's land is a tangible, hard asset, and so the company can be classified as such.

Hard asset companies tend to benefit from rising inflation, as rising prices allow them to more easily monetize said assets. As an example, TPL can lease its land for higher prices as oil prices increase.

Capital light companies are those with little capital needs. As an example, TPL requires very little capital to operate. TPL already owns the land, and its development and all necessary CAPEX must be funded by the lessee, not by TPL.

Capital light companies tend to easily, consistently benefit from rising inflation, as they can disregard issues of CAPEX, financing, debt, etc. Exxon Mobil ( XOM ) might need to build and finance new wells to take advantage of higher oil prices, which might prevent the company from fully benefiting from these. TPL does not need to build or finance new capital projects, so does not have these issues.

INFL's hard asset, capital-light holdings tend to benefit from higher prices, and so tend to outperform when inflation is high and rising. INFL significantly outperformed in 2022, a year of skyrocketing inflation, as expected.

INFL's holdings tend to outperform when inflation is high and rising. INFL's holdings should also underperform when inflation starts to come down, but the situation is a bit more nuanced and merits a closer look.

INFL - What To Expect As Inflation Normalizes

Some context first.

INFL invests in equities . Equity investors are entitled to their fair share of the company's underlying assets, earnings, and cash flows.

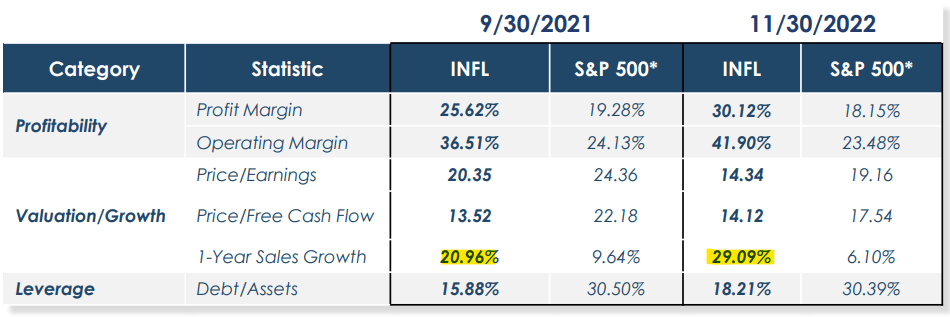

Investors in TPL, the fund's largest holding, are entitled to their share of the company's earnings, which have amounted to $346 million as of 3Q2022, a very hefty amount. A portion of these earnings is returned to shareholders, with the company paying $224 million as of 3Q2022, and repurchasing $58 million in shares as of the same. A portion of these earnings is retained by the company, for CAPEX, debt repayment, or as a cash reserve. These earnings underpin TPL's long-term returns, dividends, and share price/capital appreciation. Strong earnings lead to strong returns, although other fundamental metrics as well as market sentiment play an important role too.

TPL's earnings and cash flows, as well as those of INFL's other underlying holdings, are dependent on inflation, but the situation is somewhat nuanced. High inflation and rising energy prices mean that the oil on TPL's land is worth more, which allows the company to lease its land for higher prices, directly leading to revenue growth. As revenues grow, so should earnings, dividends, and buybacks, although these are dependent on other factors too. TPL saw significant growth in this and other financial metrics during 2022, a period of heightened inflationary pressures, as expected.

INFL's underlying holdings have seen strong, above-average revenue growth these past few months too.

{kind=link}

Strong revenue growth should lead to strong, market-beating returns, partly due to higher dividends and buybacks, and partly due to improved investor sentiment.

Inflation easing means revenue growth decreases, but revenues, earnings, and cash flows themselves should remain more or less the same. If oil prices remain the same from here on out, meaning zero inflation, then TPL land lease prices would remain the same, and so would the company's revenues. Earnings and cash flows would remain more or less the same too, but these might see some marginal improvements due to cost-cutting, debt repayment, and similar initiatives. Importantly, earnings and cash flows at today's prices are quite strong, with the fund sporting a below-average PE and P/FCF ratio (see above). Earnings, cash flows, and valuations are quite good at today's prices and would remain good even if inflation normalized, so the fund's long-term returns would likely remain reasonably good too.

Considering the above, inflation easing might not necessarily lead to losses or underperformance for INLF. Inflation has started to slow down these past few months, and the fund continues to outperform, as it did during the last quarter of 2022. Further decreases in inflation might lead to losses and underperformance in the future, but neither fund fundamentals nor past experience shows this to be certain.

Due to the above, I believe that INFL would remain a reasonably good investment opportunity even as inflation goes down. Significant deflation /lower prices would almost certainly mean losses for INFL, but the fund should be able to handle a slower, more moderate pace of decreased inflation just fine. Currently, inflation is decreasing but remains positive.

On the other hand, lower inflation could lead to worsening investor sentiment , resulting in lower share prices for INFL, and capital losses for its investors. Fundamentals might remain good, but sentiment could always worsen, and by a lot. Investors, especially short-term traders, might wish to avoid these possible losses, by selling INFL before inflation normalizes and sentiment changes. Do bear in mind, successfully timing the market is quite difficult, as forecasting economic and industry variables into the future is also difficult, and as investor sentiment is fickle and sometimes irrational. Inflation started to normalize in mid/late 2022, but selling INFL then would have been a mistake. Inflation could continue to go down these next few months, and INFL could continue to perform well. Timing the market successfully requires correctly forecasting relevant economic and industry variables, as well as investor sentiment. This is not an easy task and seems unnecessary for a fund like INFL.

In my opinion, INFL is a reasonably strong long-term investment, and it should perform reasonably well even as inflation eases. Under these conditions, trying to time an investment in the fund is unnecessary, so a long-term buy and hold strategy seems best.

Conclusion

INFL invests in companies with the potential to outperform as inflation rises. Under current prices and valuations, the fund should perform reasonably well even as inflation eases, so I see no reason to sell the fund. INFL remains a strong investment opportunity, and a buy.

For further details see:

Should You Sell INFL As Inflation Slows Down?