ISHG - SHY Vs. ISHG Bond ETFs For When The Economy Slows Further

2023-09-06 07:55:02 ET

Summary

- As the odds of a global economic slowdown grow, bond ETFs are an interesting potential investing opportunity, if well-timed to coincide with central banks lowering interest rates.

- The SHY ETF offers bond exposure with no currency exchange risks/rewards involved, while the ISHG bond ETF offers exposure to bonds denominated predominantly in euros.

- Uncertain global macroeconomic situation and potential negative surprises make bonds worth considering, but timing is crucial.

Investment thesis: After more than a decade of low interest rates, a reversion back to normal, where money is no longer essentially free to borrow makes for an interesting investment case for sovereign bond ETFs. I last covered the iShares 1-3 Year International Bond ETF ( ISHG ) in 2019. At that point, I highlighted its potential as an investment down the line, once the bond bubble we were in will burst. Its profile offers certain specific investment opportunities. For instance, most of the sovereign bonds in the fund are euro-denominated, with Japanese yen-denominated bonds being the second major category. It therefore acts as a currency bet, not only as a bet on bonds.

Alternatively, investors can consider the iShares 1-3 Year Treasury Bond ETF ( SHY ), which offers exposure to US treasuries and takes out the currency fluctuations aspect of it. It thus moves far less in terms of price. It is also arguably less risky, given that as bad as the debt and deficits situation may seem, it arguably pales in comparison to being exposed to Italian bonds.

As the global economy is starting to show signs of slowing even more than the already previously forecast slow rates of growth, gaining some exposure to bonds that are deemed to be mostly secure is something worth considering. First and foremost, the regional and global macro trends need to be considered in light of the need to time such an investment right. The macro factors that need to be considered range from economic growth trajectories, to the risk of arguably tight global energy supplies triggering a second wave of inflationary pressures. Second, the question of whether one of the two options I am comparing is better than the other. Third, the general overall risk involved in investing in bond ETFs, given growing global uncertainty, where the unthinkable tends to happen needs to be accounted for. As I have been doing recently, I tend to try to time investments as well as possible, to minimize the overall downside risk.

The global macroeconomic situation is seemingly deteriorating, and it could be further exacerbated by ongoing and arguably intensifying geopolitical tensions.

As I pointed out in an article I wrote earlier this summer entitled "Tis The Summer For Taking Profits", my expectations for the stock market for the second half of this year are not particularly rosy. Despite a slowing economy, there are strong odds that energy prices will remain high, and potentially head even higher on tight supplies, which can further dampen economic growth.

{kind=link}

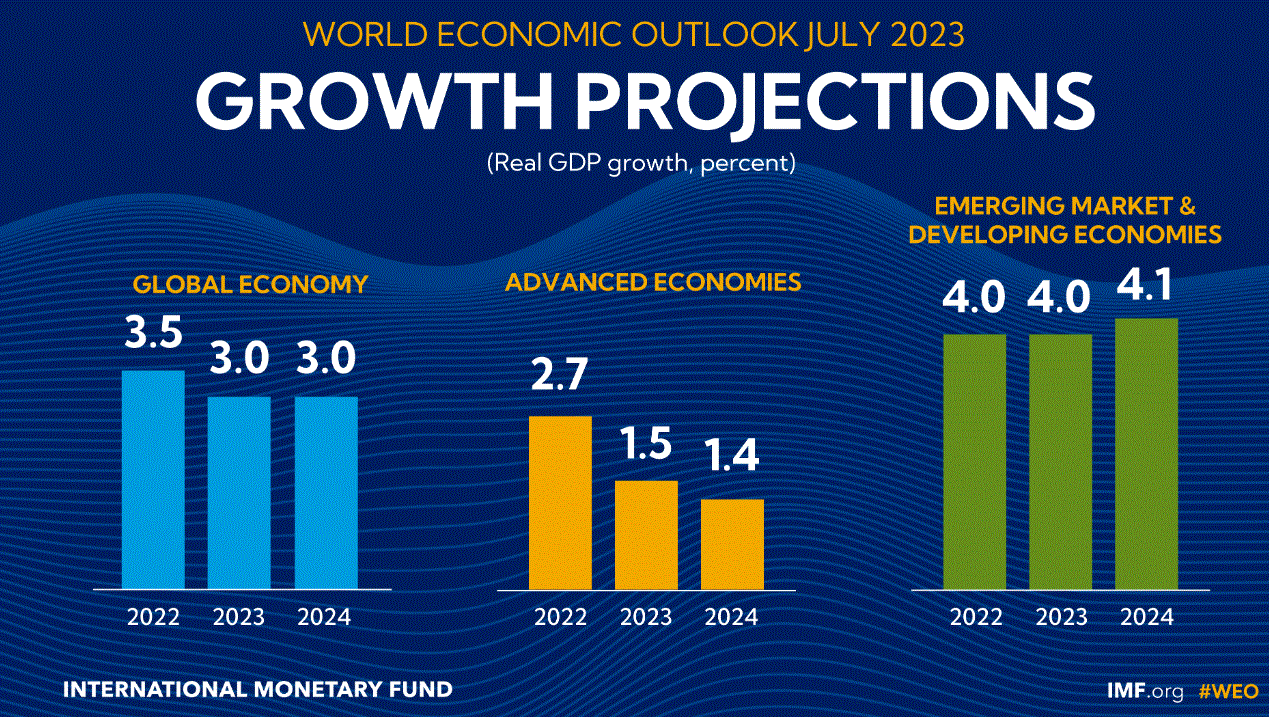

It should be noted that the IMF forecast for July does not take into account the seemingly dire situation in China , where things got so bad in the last few weeks that the government decided to stop publishing youth unemployment stats. This alone probably brings the growth forecast down for the entire world by a few tenths of a percentage point.

Other potential negative surprises that could impact the global economy or regions & nations within it are diverse. They span in terms of variety from potential disruptions in the global supply chains due to continued big power rivalries, to a colder-than-average winter in the Northern Hemisphere that has the potential to plunge the EU in particular into a severe energy crisis .

Even if there is no spectacular energy crisis on the horizon, energy prices remain stubbornly high, even as the global economy is anything but robust. This creates a potentially awkward situation for central banks, given that they are stuck between having to fight inflationary pressures, even as the economy needs monetary & fiscal stimulus. What this might mean for the outlook for bonds is that there is increased uncertainty. If central banks continue to raise interest rates to try to tame higher-than-desired inflation, then bonds currently held in both ETFs I chose for comparison will decline in value, because yields will continue to rise. If however, the need to fight the economic downturn outweighs the need to keep inflation in check, yields on freshly issued bonds will decline, providing a boost to currently-held bond prices, which is positive for both ETFs.

ISHG & SHY ETFs are likely to remain mostly positively correlated in relation to each other in terms of share price movement, but several factors could affect the magnitude of the share price move.

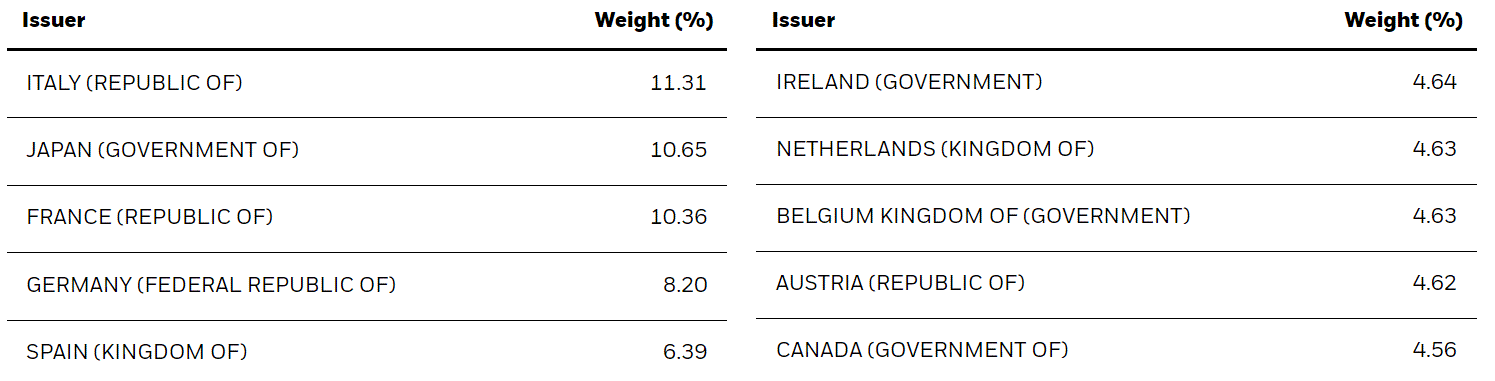

The ISHG ETF mostly offers exposure to major EU economies, as well as Japan & Canada.

{kind=link}

One of the main differentiating factors that could determine whether this ETF outperforms or underperforms the SHY ETF is the euro/USD exchange rate going forward. The SHY ETF is likely to continue to trade within a tighter range due to a lack of currency fluctuation.

{kind=link}

{kind=link}

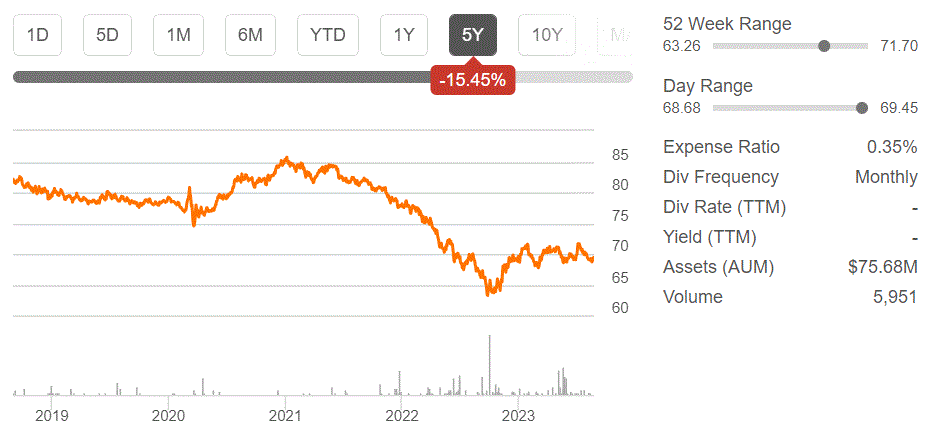

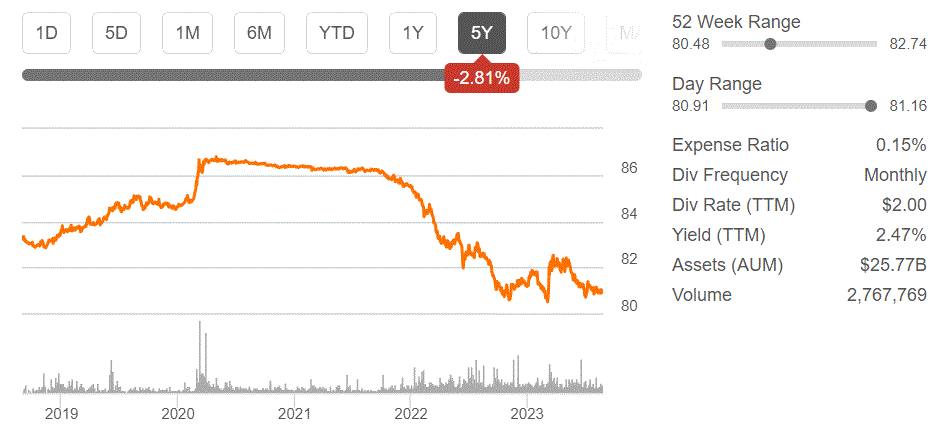

As we can see, there is a roughly 3% gap between SHY's 52-week low and high, while ISHG saw a roughly 10% gap in terms of the same metric. The one factor that both of them have in common is the fact that both ETFs started moving down in terms of share price as interest rates started moving up.

Other metrics of note, include the average yield to maturity, with SHY currently at just under 5%, while the ISHG fund has an average yield of 3.2%. This is an important factor because, in my view, it signals that currency exchange fluctuations notwithstanding, SHY may have more upside potential if interest rates start to move down. We should keep in mind that these funds will probably rise when interest rates move down because bond prices that have higher yields will gain, versus freshly issued bonds that will have lower yields. The expense ratio also favors SHY, with a cost of .15% versus .35% for ISHG

Investment implications:

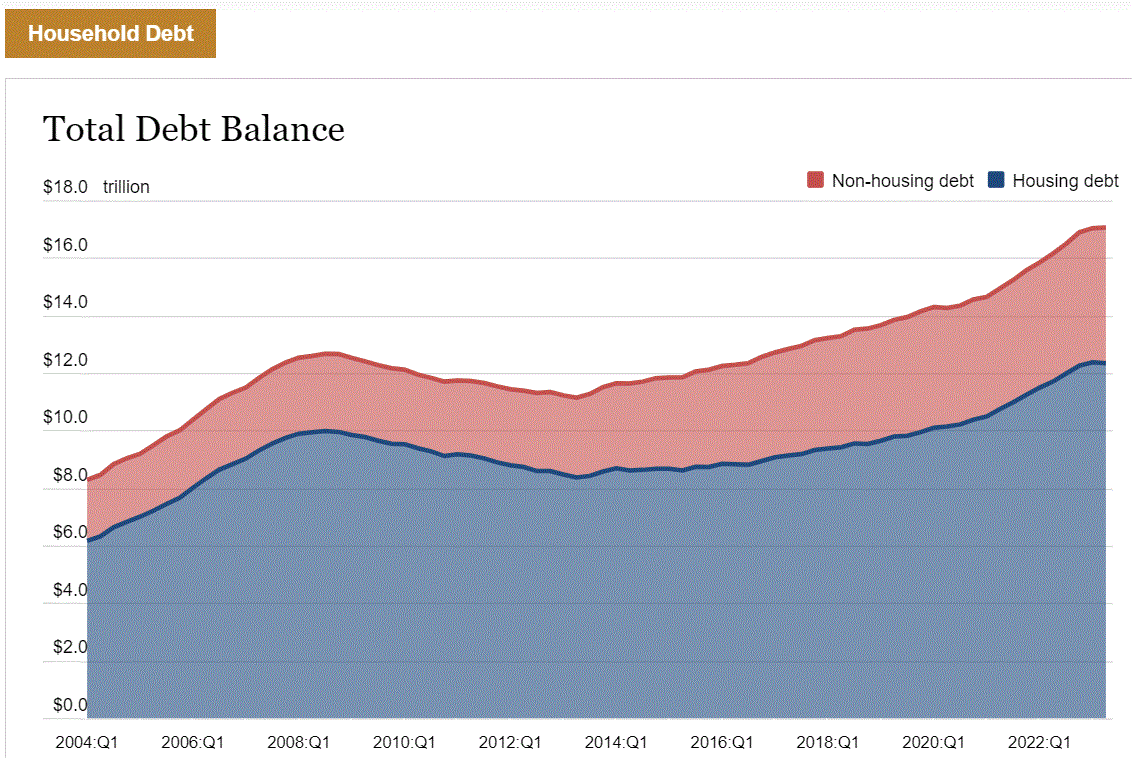

The overall US, EU, and global macroeconomic situation currently makes for one of the most uncertain environments for bonds. On one hand, we have a constant inflow of data points that tell us the economy is slowing. There are data points such as consumer savings rates, as well as growing indebtedness that tell us that consumer spending is likely to dive soon.

{kind=link}

We should bear in mind that in addition to household debt levels being high, the rise in interest rates is adding an extra burden by increasing the cost of carrying debt. At some point, probably rather soon, we should see a softening in consumer demand, which accounts for about 2/3 of the Developed World economy. This signals a future interest rate policy that is likely to trend towards a downward trend.

{kind=link}

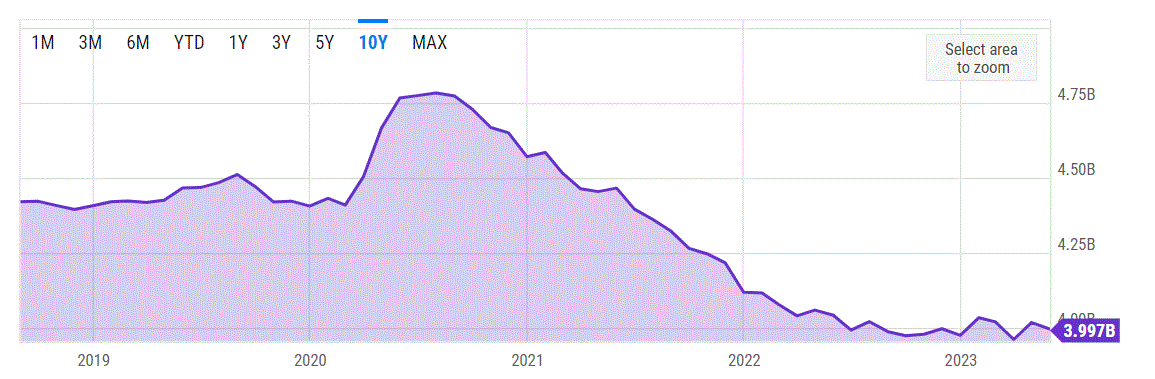

As we can see, despite a less-than-robust global economic growth trajectory, OECD oil inventories are currently roughly 10% below the historical levels we saw in normal times, in other words, before the COVID-19 pandemic. In my view, there is a roughly 1-3 mb/d global supply/demand gap currently based on OPEC's demand forecast, versus current production data we have available, until the end of the year, meaning that OECD oil storage stocks are headed for a significant decline from current already low levels, which should in theory trigger a market response in the form of an oil price spike in the next few months. This is a factor that could in theory keep central banks from lowering interest rates, despite the softening pace of the global economy.

Summing up the net effects of the two determining factors I identified as being crucial to the future outlook of the trajectory of the bond markets, one might argue that the two factors may have a net effect that is close to zero since they might largely cancel each other out. These two ETF funds should therefore in theory see very little movement for the foreseeable future until something changes. I believe this to be the most likely scenario for the next few months, after which we will see a greater level of concern for declining economic activity, as opposed to inflationary pressures, mostly pushed higher by rising energy costs.

As for which of the two ETFs is more attractive, the main differentiating factor is the outlook for the currency exchange fluctuations going forward, between the US dollar on one hand and the euro & Japanese yen on the other. Given the uncertain times we live in, there is potential for a great deal of currency fluctuation in the months and years ahead. In my personal view, the euro and the yen both share a particular potential risk factor, namely the need for both of their economies to import a significant volume of energy, within the context of a seemingly less-than-ideal global supply situation. In other words, their currencies could end up chasing spiking LNG and oil prices, with their push to buy at any price leading to their currencies losing value. On the other hand, the US is running what seems to be deficits approaching $2 trillion as an institutionalized reality, in other words, this is the new normal even in the best of times. Taking these factors into consideration, the currency issue is a potential risk but also a potential reason to be more bullish on ISHG. The way I see it currently, it could go either way.

At the moment, I am watching the price of oil, as well as the evolving supply/demand situation as a main indicator of when it might be a good time to buy into either or both of these ETFs. It seems that the price of oil might still have a long way to go on the upside, which suggests there could still be some upside surprises for inflation in the coming months, therefore interest rates could still rise, which tends to be negatively correlated with the movement of both ETFs. At some point, possibly in the next twelve months, global economic growth will likely slow down sufficiently for global oil & energy demand growth to come back into line with tight supplies. At that point, it will likely be a good entry point for both ETFs. Personally, if I manage to time this right, I will most likely invest in both ETFs, with the proportions yet to be determined, based on prevailing realities at the time.

For further details see:

SHY Vs. ISHG Bond ETFs For When The Economy Slows Further