SIBN - SI-BONE: Multiple Inflection Points On The Horizon In FY 2023

Summary

- SI-BONE, Inc. presents as a niche operator in the surgical intervention of sacroiliac disorders.

- There are multiple inflection points on the horizon for SI-BONE in FY 2023.

- Market punishment has been severe for SI-BONE, Inc. stock over 2021-2022, however, a contrarian view is needed in this case, by estimation.

- We see scope for SI-BONE stock to re-rate to price objectives of $13.75 then $19.40.

- Net-net, we rate SI-BONE, Inc. a buy.

Investment Thesis Summary

As patient and surgical volumes begin to normalize to pre-pandemic ranges for orthopedics, there's now scope for several names within the domain to re-rate to the upside in our opinion. We recently reviewed the investment case of SI-BONE, Inc. ( SIBN ), and noted it has several potential inflection points at the helm for 2023.

As a reminder, SI-BONE has its expertise in the development of surgical implants designed to remedy musculoskeletal disorders of the sacroiliac region. This is a complex anatomical region, with a multitude of under-diagnosed and misdiagnosed conditions. Hence, treatment outcomes are equally as mixed. Considering our search to position against a basket of names that are aiming to provide solutions to otherwise complex disorders, SIBN presents as an adequate case for review. Hence, I'm back today to reveal our examination findings of the company. Net-net, we rate SIBN a buy, and suggest price objectives of $13.75, then $19.40, for the coming periods.

Exhibit 1. SIBN 18-month price evolution vs. S&P 500, with corresponding equity beta.

Data: Updata

Q3 numbers a standout, indicative of the SI-BONE, Inc. growth curve

Turning to the company's latest financial results, it's worth highlighting the growth period SI-BONE, Inc. has exhibited across the entirety of FY22'. Specifically, the sequential growth pattern in revenue from 2021 is a standout in our estimation. The Q1, Q2, Q3 FY22' growth rate[s] levered up to 10%, 15%, and 19% from their corresponding periods in FY 2021, respectively, indicating the momentum obtained as the year progressed.

For Q3, the 19% YoY uplift booked turnover of $26.4mm, also 300bps higher sequentially. Its U.S. market proved to be particularly lucrative, with the company raking in $24.6mm in revenue, an increase of 21% compared to the previous year. The growth was fueled by a 25% increase in procedure volumes during the quarter, but was underlined by the sustained refraction in SIBN's procedure volumes throughout FY22' in spite of the tight labor market observed in hospitals and ASC's. To us, this is further indication of the steep demand curve for SIBN's solutions.

Another data point is that SIBN's Q3 gross margin compressed by ~400bps YoY to 84% on gross profit of $22.26mm, up 12.4% over the year. We'd suggest the decrease in gross margin is a reflection of the insatiable demand for the company's products, as it ramped up production and shipping, and therefore booked higher COGS and freight costs.

Moving down the income statement, it's worth noting that Q3 OpEx rose to $35.8 million in the quarter, an increase of 900bps YoY. However, this was arguably expected given the revenue ramp and focus on increasing sales, and therefore variable costs associated with this. In fact, on a sequential basis, OpEx decreased ~10% compared to Q2 FY22'. In both cases, these are good numbers to go by, and we'd note that revenue increased at a pace more than 2.1 turns above OpEx for the Q3 period. It pulled this down a loss of $14.2mm, or $0.41 per diluted share, a slight improvement from the Q3 FY21 ness loss of $15.9 million [$0.48/share].

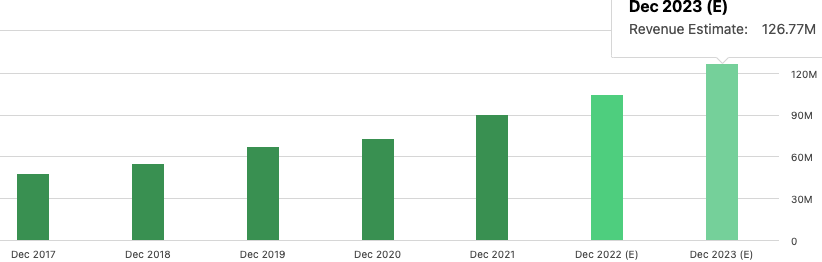

As a result of the momentum at the back end of FY22', SI-BONE, Inc. management projects full-year revenue of ~$105mm at the upper range, calling for ~17% YoY growth. This is reflected in consensus revenue estimates as well [Exhibit 2], and follows-through to a FY23' revenue of $126.7mm, creating a reasonable ramp looking ahead.

Exhibit 2. Consensus revenue estimates for FY23–24', reasonable ramp up looking ahead, should SIBN convert on this.

Data: Seeking Alpha. SIBN, see: "Revenue"

{kind=link}

At the end of the third quarter, SIBN's sales team was comprised of 85 territory managers and 72 clinical support specialists. The average revenue generated by each territory manager in the quarter was therefore ~$310,590. As the company's sales force becomes more seasoned, management estimate the average trailing 12-month revenue per territory manager is expected to experience a growth of >10% looking ahead.

In terms of surgeon engagements, the company ended Q3 with its highest number of active surgeons, totaling >800. This represents a YoY increase of 27% and a sequential increase of 12%. This also marks seven consecutive quarters of double-digit YoY growth in number of active surgeons using its devices.

A quick note on SI-BONE, Inc.'s liquidity

The company left the quarter with $104mm in cash and equivalents, on a debt load of $35.1mm. This is on the back of an accumulated deficit of $346mm since inception. SIBN also burnt $43.4mm in cash over the 12 months to September 30, 2022, comprised mainly of a $34.9mm cash outflow from operations. Part of the outflows were assigned to the increase in inventories of its new products.

At the end of Q3, SIBN's current ratio was 7.5x, and still ~6.6x when excluding the inventory build up. Moreover, the company has no goodwill booked on its asset base, whereas its interest expense is covered by more than 29x from gross profit. Based on this assessment, we estimate the company has sufficient cash runway over the coming 12-18 months of operations.

SIBN tailwinds for 2023

There are several tailwinds building momentum for SIBN in FY23' by our estimation. To name a few:

1. The foremost tailwind in our estimation stems from CMS' ruling on reimbursement figures on hospital and ambulatory surgical centers ("ASCs") for the coming 12 months. Specifically, its final ruling on sacroiliac joint ("SIJ") fusion procedures [performed in hospitals and ASCs] will observe a 26% and 33% increase to $17,109 and $21,898 respectively. This has multiple benefits for SIBN in our opinion. First, as it stands today, ~80% of its SIJ procedures are performed in outpatient or at surgical centers. As these roll over to be performed in ASCs, SIBN will realize the higher reimbursement rates. Second, this will allow the company to maintain and even increase its average selling price[s] ("ASP") at the various ASCs where it has exposure. Therefore, should it convert here, we estimate this to be a meaningful tailwind for the company looking down the line.

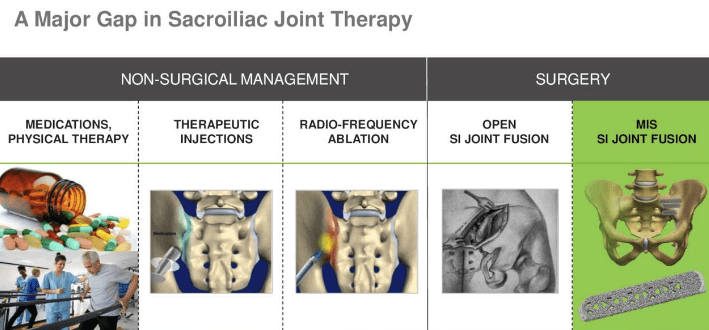

2. SIBN also reported an increase in the use of its iFuse-TORQ device to treat sacral fragility fractures, a type of injury that affects ~120,000 people in the U.S each year. For reference, fragility fractures, also known as stress fractures, occur as a consequence of low-energy, sustained trauma/loading to the affected site. More often than not, in the SIJ, the condition [which is also associated with other complex conditions such as osteoporosis and osteopenia] is often treated with non-surgical intervention. Unfortunately, success rates from conservative treatment are therefore low in population. Hence, the fragility fracture market has an unmet clinical need and this presents SIBN with a strategic advantage in our opinion.

Exhibit 3. SIBN has a potential strategic advantage in providing a minimally invasive surgery ("MIS") solution for sacral fragility fractures.

{kind=link}

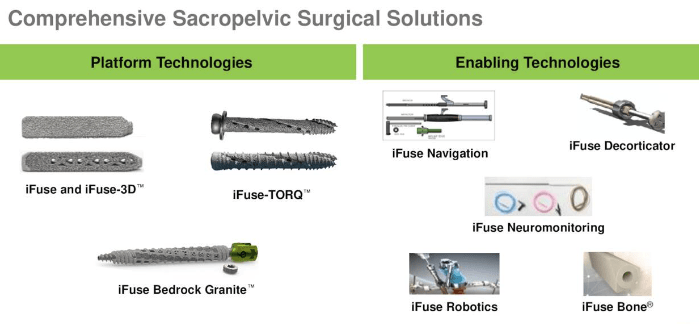

3. In June 2022, SIBN received expanded clearance from the FDA for its iFuse Bedrock Granite device, which is used to immobilize and fuse the sacroiliac joint and serve as foundational support in spine fusion surgeries. As a reminder, the Bedrock Granite segment was launched in May this year. It is indicated in immobilization and fusion of the SIJ alongside its indication as a foundational support at the base of a lumbar spinal fusion.

4. As another tailwind, on December 27th, 2022, SIBN announced that it had received further extended clearance for the Bedrock Granite device. The initial clearance included an indication for use with a single manufacturer's pedicle screw system, but the expanded clearance allows for use with a wide range of rods commonly used in multilevel spine fusion surgeries. This expanded clearance allows surgeons to use their preferred techniques and implant systems with confidence in conjunction with iFuse Bedrock Granite as the foundation for their construct. You can see the full list of SIBN's interventions in Exhibit 4, below.

Exhibit 4. SIBN's list of sacral surgery implements.

{kind=link}

5. We'd also point out that SIBN recently announced it had enrolled the first patient its randomized controlled SAFFRON trial. The trial will compare surgery using the iFuse-TORQ device to non-surgical management in patients with debilitating sacral fragility or insufficiency fractures. The company plans to enroll a total of 120 patients in the study. Investors can expect results from this trial in late 2024.

Valuation and conclusion

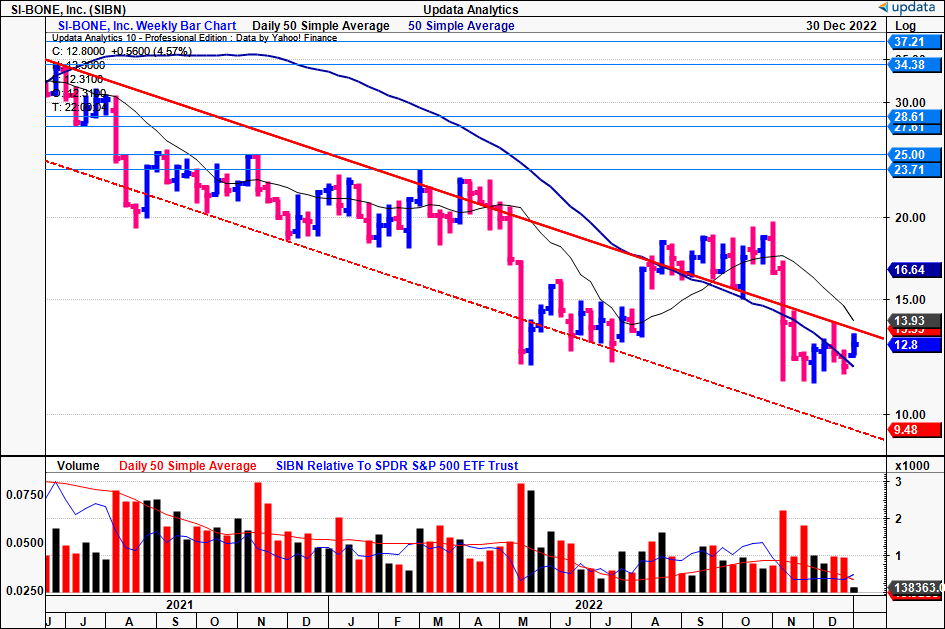

Market punishment of SIBN stock has been felt for the last 18-months. For those observing Exhibit 5, you'll see the stock has maintained within a tight downtrend over this time, unable to break out of the resistance band.

Exhibit 5. Market punishment for the SIBN share price has been heavy across the last 18-months.

{kind=link}

Consequently it's no surprise to see the stock rated poorly from Seeking Alpha's quantitative factor grading system. As an objective composite, the factor grading implies that the stock's current market value may be justified.

It also trades at more than 4.6x book value, which in itself raises an interesting debate. On the one hand, this could evidence SIBN's value creation above the book value of its equity. On the other, it might suggest it's overvalued.

It left the quarter with $2.99 in book value per share, and applying the 4.6x multiple derives a valuation of $13.75. Hence, we believe there's scope for the stock to re-rate to this level. Moreover, you'll observe in Exhibit 7 that we have upside targets to $19.40, which also confirms a bullish, yet contrarian view.

Exhibit 6. SIBN factor grading from Seeking Alpha's quant system, suggesting a low rating from valuation.

Data: Seeking Alpha, SIBN quote page, see: "Factor Grades".

Exhibit 7. Upside targets to $19.40, could suggest bullish reversal – this would confirm a contrarian view by estimation

Data: Updata

Net-net, there are multiple mid-term growth levers in place for SI-BONE, Inc. by our analysis. The stock has been heavily sold off across 2021-2022, providing scope for it to re-rate to the upside from its latest numbers and product launches. This is backed by its growth curve seen during 2022 versus the previous year.

The key downside risk to the investment debate is if SI-BONE, Inc. fails to maintain this level of trajectory, or is unable to roll the bulk of its MIS's over to the ACS setting, thereby clamping its exposure to CMS reimbursement figures for FY23. Moreover, there's chance the market will continue its selloff of SI-BONE, Inc. stock into the coming periods. Investors should be well aware of these risks looking ahead. Nevertheless, we are constructive on SI-BONE, Inc. and look to 2023 as a period with multiple inflection points. Rate buy.

For further details see:

SI-BONE: Multiple Inflection Points On The Horizon In FY 2023