SIBN - SI-BONE: Rating Higher On Fundamental Economic Grounds

2023-06-15 12:14:52 ET

Summary

- SI-BONE is pushing higher in revenues and gross profit, clipping another strong quarter.

- It pulled in 80% gross margin and expects this on a revised FY'23 outlook.

- Additional fundamental catalysts are the revised Granite segment outlook and increase in surgeon engagement.

- Reiterate buy, looking to $32 as the next target.

Summary of investment updates

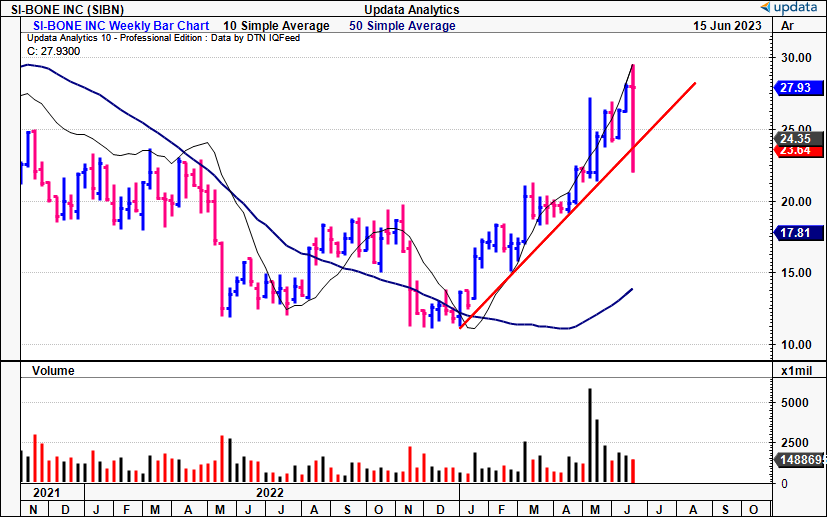

The buy rating on SI-BONE, Inc. (SIBN) from December has been vindicated in the near-term with a 105% return on capital from then until the time of writing this report. The appreciation comes from a multitude of factors, including reimbursement tailwinds, financial results, and asset factors.

Data: Author Previous SIBN Publication

{kind=link}

Since December I've been heavily active on SIBN and following the latest updates I am more constructive on the firm moving forward. Hence I am reiterating buying SIBN at its current market values. This report will amalgamate the critical investment facts to illustrate my informed opinion on the company. Breaking it down to first principles, there are catalysts both on the fundamental, sentimental and valuation fronts in my view, a rare triple-offering that could outperform the market return.

Net-net, there is sufficient data to corroborate buying SIBN at the current market value, looking for the next price objective of $32.

Figure 1.

{kind=link}

Key risks to the investment thesis

Before proceeding, investors must understand the following risks that could either deviate or nullify the investment thesis:

- The major risk at this level is that small-cap equities present with market risks that can lead to excessive volatility. This can occur even when fundamentals are strong, leading to loss of capital.

- Much is hinging on the company's ability to gain new surgeons, as you'll see here today. If it fails to do this, its growth route will be disrupted.

- There are broader macroeconomic risks that must be realized too, in particular, interest rates, inflation, and the market's sensitivity to data on both. It would be wise to consider these within the broader portfolio.

- The company's 80%+ gross margin is central to its ability to it generating high levels of income going forward. Should this erode, I am not sure I would be as bullish on the company.

These risks must be recognised in full before proceeding, as, any one presents risk to the thesis, and could nullify it completely as mentioned.

Critical facts in SIBN investment case

After a strong quarter from the company, my eyes are drawn to several facts that I'll run through with you here now. Principally, these are all quantitative- not unexpected when a company is objectively performing well. However, beyond the financial results, there are additional talking points.

Fundamental catalysts

SIBN clipped another strong set of numbers in Q1 FY'23. The company booked global sales of $32.7mm, another ~46% YoY gain. Growth was underscored by the pull-through from physician education over several years (growth in active surgeons, discussed later), in addition to market-specific tailwinds. Additional takeouts are also a delight to read:

- U.S. turnover reached $30.5mm, up 50% YoY. Growth was all demand-driven, with volumes up c.48% YoY. Sequential revenues were up as well, underlined by more surgeons on the base from Q4 last year.

- It booked 82% gross on these revenues, in-line with the company's superb gross margin of times gone by. This is a critical point, not to be overlooked. The term "growth" company is conned all too often from loose lips who see revenue expansion as the single defining factor. What matters is the income a firm pulls from its revenues too. In first principles investing, gross profitability is a firm's ability to make money. A gross of 50% versus 80% is a huge difference between growth in earnings. SIBN justifies itself as a legitimate growth company that can "make money", as observed by the following record of accounts:

Table 1. SIBN revenue and gross profit, 2017-2023

Note: 2023 is shown as the TTM to Q1 FY'23 (Data: Author, SIBN 10-K's)

- Persistent 80-90% gross margin is statistically meaningful and tells me the company has something in its grasp in the realms of creating value. Income is less meaningful without the asset factors to produce it, either. You can note SIBN's attention to gross profitability below. Number one, is the gross profit generated of $1 in assets has curled up from $0.36 to $0.657 since FY'18, on a relatively similar asset size. Hence, growth is largely "organic", not consuming enormous piles of capital to get there. You're getting more than 65% of gross return on assets at this rate- a generous turnaround in my view. Gross margins are estimated at 80% minimum for FY'23.

Figure 2.

Data: Author, SIBN 10-K's

Business economics

The company's business model is fairly easy to ascertain. A combination of obtaining and retaining active surgeons, launching new products, and increasing the price and volumes of existing ones fuels the growth engine. Chief to that formula is surgeon engagement. To that point, observe the following points highlighting the company's progress:

- The company exited the first quarter with over 950 active surgeons, representing a growth of over 40% compared to the first quarter of 2022. As such, Q1 saw average revenue per surgeon of $34,421. For comparison, Q1 FY'22 revenue/rep was $33,034. Hence, a gain in number of active surgeons, and average revenue per surgeon- both key growth drivers.

- The company intends to target 7,500 surgeons in its core market in total. A colossal number, but audacious one must be to outperform competitors. It already has 12.6% of this market as of Q1.

- As an exercise, if it captures 50% and 100% of this surgeon base respectively, at the same revenue/rep as Q1 FY'23, the quarterly turnover would reach $129mm and 258.2mm, respectively -$516mm and $1.03Bn annualized (7,500x0.5 x 34,421 = 129mm; 7,500 x 34,421 = 258.2).

The fact SIBN' selectively places its instrument sets in high-volume hospitals is conducive to it marching towards this end goal in my view. This allows it the exposure to much larger "foot-traffic" if it were to focus on lower-volume sites.

SIBN has a habit of gaining exposure to oversized markets. Case in point- its revised view of the market opportunity for its Granite segment. Recently approved in May last year, SIBN has been heavily investing to growth this division. As the name would suggest, the Granite implant provides sacroiliac fusion and sacro-pelvic fixation. The sacral region is a complex domain that has few surgical interests compared to its spinal cousins. Hence, this could be a meaningful growth market for SIBN in my view. As another differentiator, it can be incorporated with other forms of spinal fusion.

Originally, it estimated 30,000 cases as the goal, but were focused on long-construct spino-pelvic fixation. Curiously, management revised their assumptions on the market opportunity, on the data that ~40% of its Granite procedures are being performed using the short construct technique (the two just use different approaches for different candidates).

The major benefit- from the 30,000 potential patients, the number stretches up to 100,000 cases, creating an incremental market opportunity of $600-$700mm on management's estimates. Per the CEO on the earnings call: " [i]f you add together the opportunity that we have in pelvic fixation, we think the opportunity overall, the TAM is around a $1[Bn] in total"

Naturally, this discovery has prompted revised internal expectations. Guidance now stands at $128mm-$131mm for the year, calling for 20-23% growth at the top line. As mentioned, the company forecasts a gross margin of 80% in FY'23, or $104mm at the upper range, indicating its focus on maintaining profitability while driving revenue growth.

Valuation and conclusion

Investors are selling their stock at 8x forward sales and are therefore holding with strong hands in my view. That's a high ask and with the recent price action investors aren't accepting any lower bids than that for the time being. I believe the market is looking more to the revised expectations in SIBN's earnings power going forward.

At the current market cap of $1.08Bn, and a 12% discount rate (long term market averages), the market expects $121mm in future earnings from SIBN- most likely gross profit, in my view (121/0.12 = 1,008). From the TTM gross profit of $98mm, this calls for 23.5% annual compounding growth into FY'23-'24.

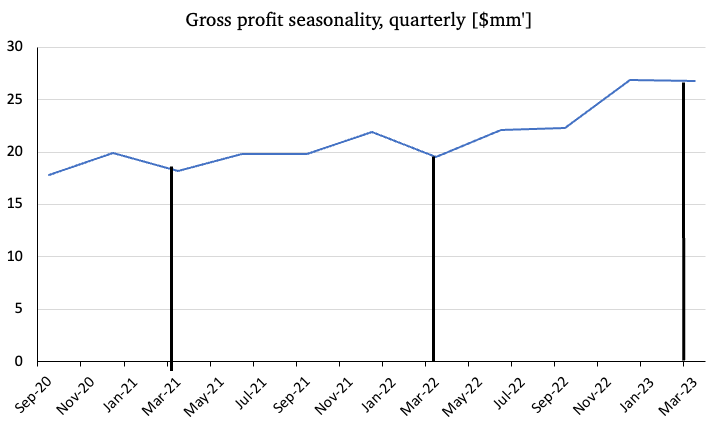

There is reason to believe the market hasn't fully priced in the company's growth potential. For one, Q1 is typically the lowest in terms of seasonality for SIBN (this is in-line with the industry, given the timing of insurance payments and surgeon holidays). Hence, the $107mm Q1 annualized gross profit can stretch higher. Two, the pace in new active surgeons and higher average revenue/surgeon is telling of the company's growth curve. In my view, the company can book another 380 surgeons this year, and increase the average quarterly revenue/surgeon to $35,000 based on volumes. This would call for $186.2mm in turnover, and at an 80% gross, gets me to $149mm in profit- $1.24Bn market value, or $32 per share.

Figure 3. Gross Profit per quarter, 2020-date

{kind=link}

Net-net, the bulk of these findings are supportive of a revised buy thesis. It has smashed out the previous target of $19, and I am looking to $32 as the next target with the latest data. There are reasons to believe SIBN can grow revenues to $180mm+, with the broader scope in its Granite segment, pace of new active surgeons, and >80% gross margin. As such, I am reiterating the company as a buy for investors.

For further details see:

SI-BONE: Rating Higher On Fundamental, Economic Grounds