SBSW - Sibanye Stillwater: High Risk High Reward

2023-12-10 05:36:26 ET

Summary

- Sibanye Stillwater's share price has plunged over 50% year-to-date due to the decline in rhodium and palladium prices.

- The company's gold mining operations in South Africa are high-cost and about a third is unprofitable, even with gold at all-time highs.

- Sibanye's investments in battery metals and recycling ventures raise questions about the company's capital allocation strategy.

- An investment in Sibanye functions as a cheap call on PGM and gold prices.

- However, it also carries significant idiosyncratic risks related to how the management will be able to restructure current operations and make progress on their newer investments.

Sibanye Stillwater ( SBSW ) is a mining company with operations in South Africa, the United States, Europe, and Australia. It predominantly produces gold and platinum group metals (PGMs). The rapid year-to-date decline in rhodium and palladium has caused the share price to plunge by more than 50%. As a portion of their operations are now producing at a loss, stress on the balance sheet has increased. Inflationary pressures, coupled with labor strikes, mining accidents, and Eskom's load curtailments, have further squeezed margins. Sibanye appears extremely inexpensive based on backward-looking multiples. However, the reality is that at current prices, its profitability is severely compromised.

Here is a statement from the CEO, Neal Froneman:

[…] we are mindful of the commercial environment and, where necessary, will consider restructuring in areas where commercially viable operations cannot be sustained. In this regard, we recently announced potential restructuring at our SA gold and SA PGM operations. Potential closure or rightsizing of high cost and underperforming shafts will ensure that operations remain profitable and sustainable at current precious metal prices and beyond, while retaining significant leverage to improvements in the commodity price outlook.

Let's begin with Sibanye's gold mining business. Its primary operations are situated in the Witwatersrand Basin, in South Africa. These are among the largest single gold fields in the world. However, production is technically challenging. The mines are deep, with some shafts extending nearly 4 kilometers below the surface where temperatures can reach up to 60 degrees Celsius. The working conditions are demanding, which is why Sibanye has faced repeated labor-related issues. These operations are inherently high-cost. Additionally, as the mines age, it becomes necessary to pursue veins at even greater depths, necessitating substantial capital investments. The result is that with gold at $2000 per ounce, more than a third of Sibanye's production is currently unprofitable.

Cost curve for Sibanye's gold operations (Company's Presentation)

{kind=link}

This raises a crucial question: why hasn't management already arranged to discontinue the unprofitable operations? Unlike platinum-group metals, which have experienced a rapid and unexpected decline over a few months, gold is near all-time highs. In my opinion, the inability to control costs and focus on economically viable operations in a timely manner represents a red flag.

So, how has management decided to invest the windfall of the past few years? They have squandered it on a questionable and unnecessary venture into battery metals and recycling.

Let's examine the Sandouville nickel refinery in France. Nickel prices have halved over the past 12 months, while input energy prices have risen due to the conflict in Ukraine. It's therefore unsurprising that this new operation is operating at a loss. In the words of CEO Froneman:

Despite the improved operational performance, the Sandouville refinery remained loss making, due to continued inflationary cost pressures, elevated maintenance costs and a further decline in the average nickel price. The current operations are not commercially viable at current nickel prices, and management has made notable progress with optimisation studies aimed at securing a sustainable future for the Sandouville refinery. Positively, during these optimisation studies, the European region and Sandouville teams have identified an innovative alternative to the current process and are currently assessing its commercial and technical feasibility. In parallel, we continue to advance the studies on recycling and production of battery grade nickel products.

Uncertainty remains about these feasibility studies currently underway, but with hindsight, this was definitely not an example of good capital allocation.

Regrettably, the company has made other questionable acquisitions. In March 2023, it acquired 100% of New Century Resources in Australia, a zinc retreatment operation. Due to regional flooding and lower zinc prices, the facility operated at a loss during the first half of 2023. In the last quarter, with production levels restored, it managed to generate a marginal positive EBITDA profit of $3 million. Uncertainty remains about the long-term economic viability of this operation.

Sibanye is making another significant investment through the development of the Syväjärvi open-pit mine in Päiväneva, Finland. This is not a small project, with total estimated capital costs of €656 million. The construction of the lithium concentrator has already begun, but the first production is only expected in 2026. It's challenging to determine the NPV of this project at present, as it will depend on future lithium prices. Meanwhile, lithium carbonate prices this year have dropped from CNY 600,000 to below CNY 100,000 per tonne.

In November, Sibanye announced its latest acquisition of the U.S. metals recycler Reldan , for an enterprise value of $211.5M, with cash considerations amounting to $155.4M. Reldan, a Pennsylvania-based company, reprocesses industrial waste and electronic waste to recycle green precious metals. This latest venture also seems unnecessary at the moment, as in my opinion, the focus should remain on optimizing its mining business.

Until recently, Sibanye's balance sheet was in a very solid condition. The company planned to finance its green ambitions with the cash flow from its PGM business. Unfortunately, this business is currently under the most stress. As a result, Sibanye has announced plans to raise $500 million in convertible bonds (admittedly, they managed to negotiate a very good interest rate, between 4% and 4.5%). However, a more prudent capital allocation strategy would have probably made it unnecessary.

In my opinion, the company should have stayed focused on its core mining operations. It's understandable that management tried to diversify away from South Africa. The issue now is that they find themselves with multiple capital commitments at the worst possible time. Moreover, the profitability of their new investments remains questionable, or at least uncertain.

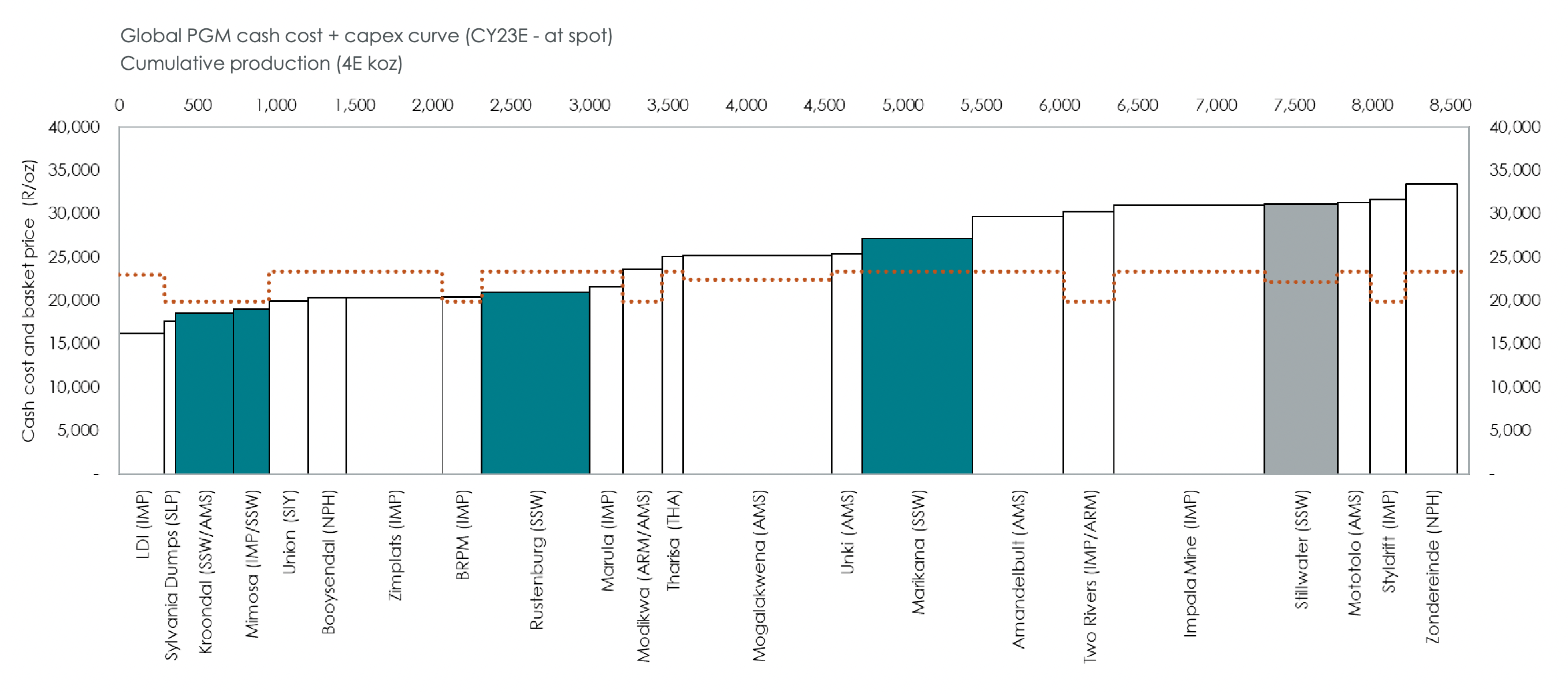

Let's examine their PGM business. Sibanye certainly owns some excellent assets. Looking at the global cost curve, Kroondal, Mimosa, and Rustenburg are all projects in the bottom 50% of the curve. Marikana is slightly above the middle of the curve. Stillwater, the US operation located in Montana, is quite high-cost and has recently been impacted by regional floods, accidents, and labor shortages.

{kind=link}

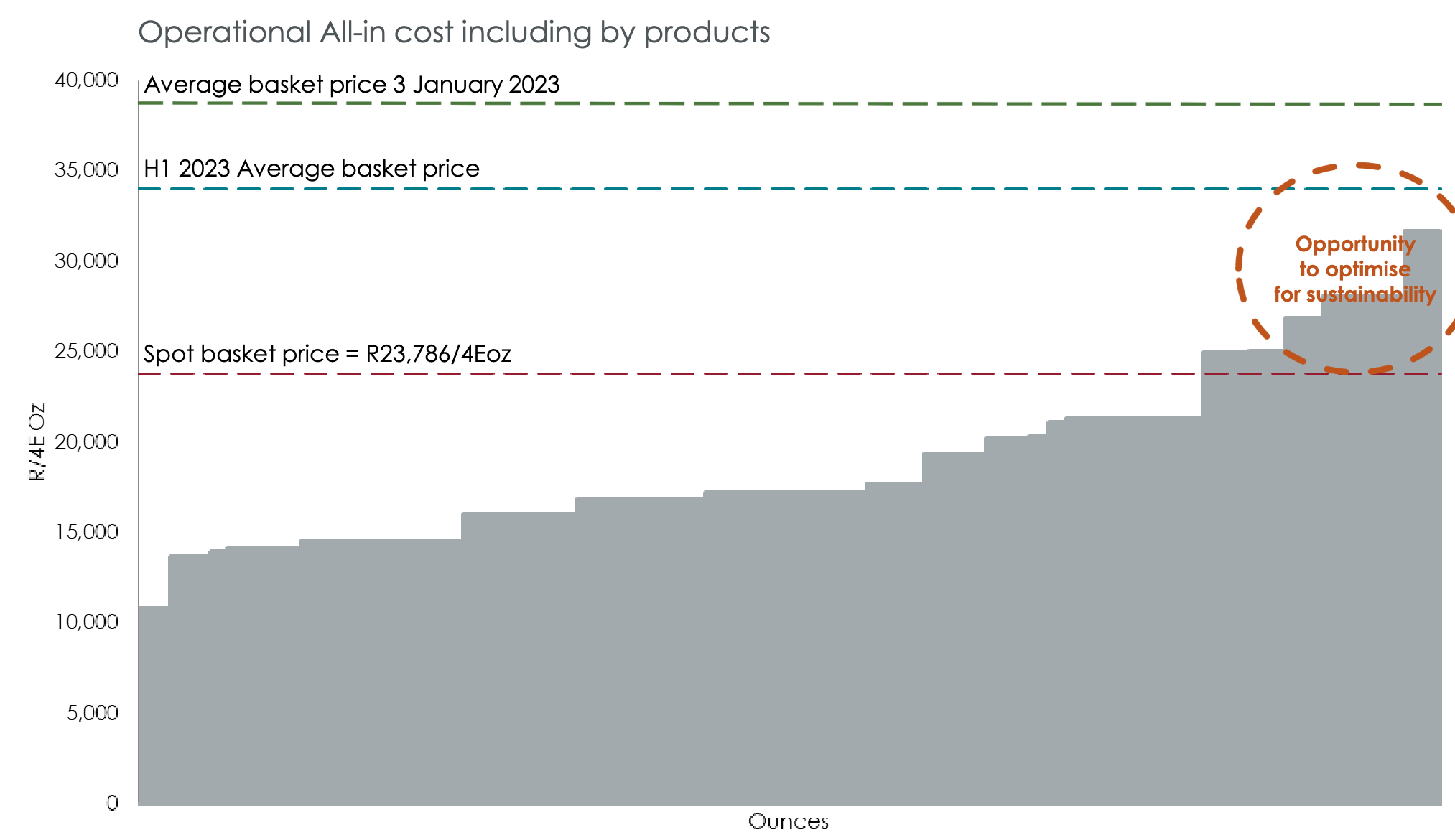

Current PGM prices are quite depressed and probably unsustainable long-term. However, in the meantime, Sibanye will face significant challenges. It may need to raise even more debt or dilute its shareholders if prices do not recover quickly enough.

{kind=link}

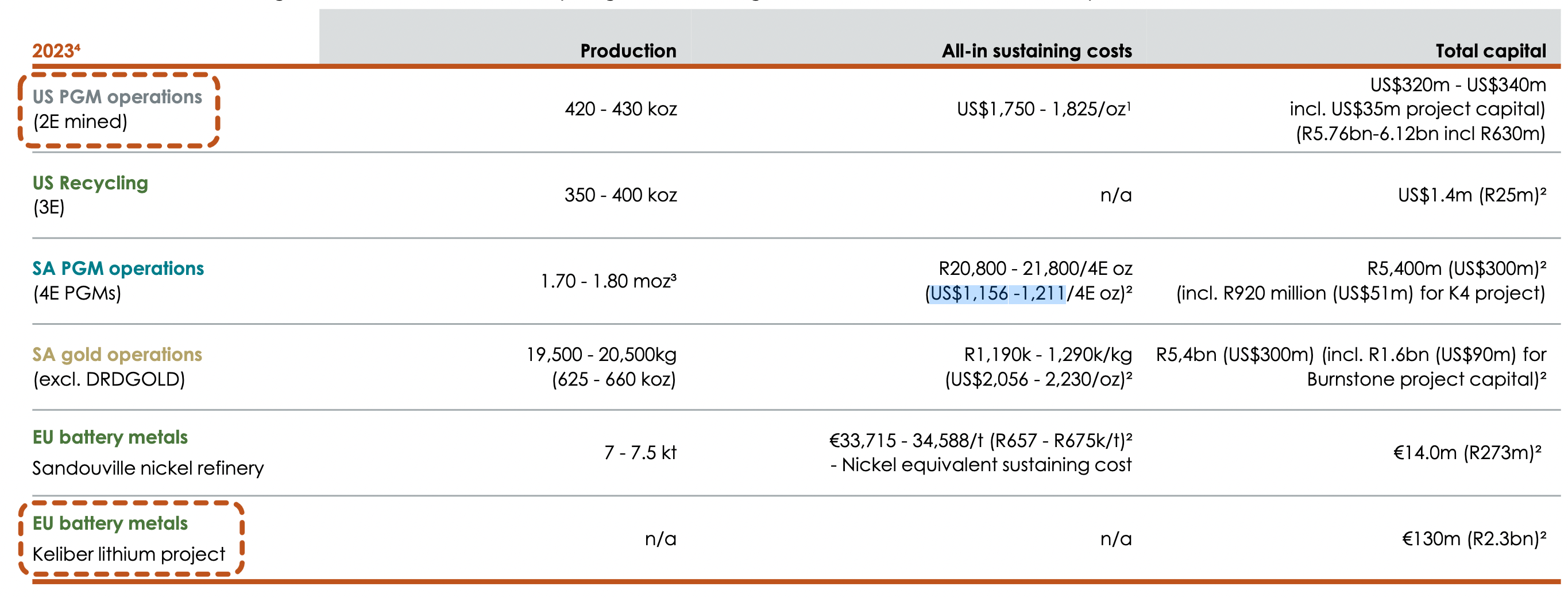

If the slide of PGM prices continues, most of its operations are or could become unprofitable. According to the most recent guidance for 2023, the company expects AISC for gold to be around S$2,056 - 2,230/oz, some of the highest in the sector. AISC for its US PGM operations are expected to be around $1,750 - 1,825 per ounce, while for its South African operation it is projected to be around $1,156 -1,211. The margins are razor-thin.

FY2023 latest guidance (Company's Presentation)

{kind=link}

In summary, Sibanye has a lot of torque. The stock price could easily double or triple from here, but it all hinges on the direction of PGM and gold prices. In other words, an investment in Sibanye functions as a cost-effective call option on PGM and gold prices. However, it also carries unique risks related to how management will optimize current operations and progress on their recent green investments.

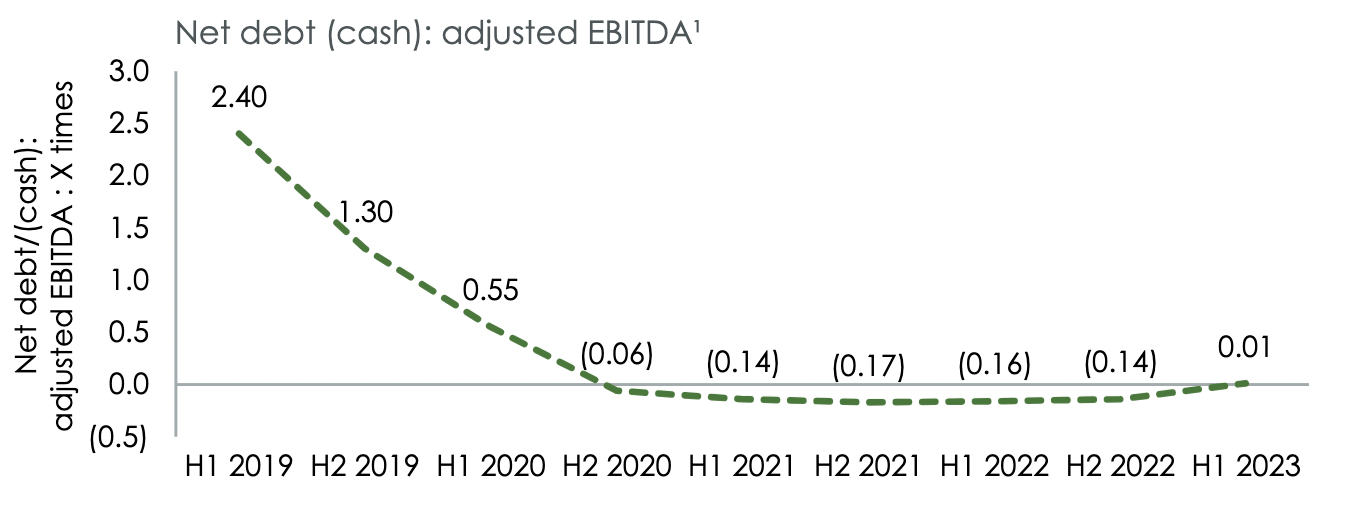

Sibanye has navigated difficult waters in the past. The net debt to EBITDA ratio was at 2.4 in 2019, but it fell to 0 in 2020, and today the company is in a net cash position. This has enabled it to pay substantial dividends and even buyback shares in the interim. It appears that Sibanye has a history of extricating itself from challenging conditions.

{kind=link}

However, it's vital to understand the drivers behind this turnaround story. I believe that, ultimately, it was more down to fortunate circumstances, rather than management’s skill. Sibanye's profits were significantly boosted by the rise of palladium and, especially, rhodium prices in the years leading up to COVID. The pandemic and the resulting semiconductor shortage caused a decline in demand from the automotive sector, which in turn halted the relentless rise of palladium and rhodium prices. Even with automotive demand now recovering to pre-pandemic levels, rhodium and palladium remain under pressure. The substitution of platinum for palladium in catalytic converters and the increased penetration of battery electric vehicles (BEVs) suggest that it's unlikely that both metals will return to their historical highs anytime soon.

Is Sibanye a buy right now? The upside is certainly significant given the depressed valuation. Platinum-group metals seem ready to bottom out and consolidate. I am particularly bullish on platinum, given its projected sustained deficits over the next few years and its crucial role in the upcoming hydrogen economy. With a significant part of the cost curve below the spot price, now is a good time to start deploying capital into this highly cyclical sector. I discussed my view on the platinum and palladium market in a separate article .

However, an investment in Sibanye carries very high risks. If metal prices do not recover quickly enough, then the company's near-term future will entirely depend on the management's ability to steer the company back on course through restructuring and optimization initiatives. I am not entirely confident.

The whole sector is undervalued based on normalized earnings. Considering that there are many other names that do not carry the unique risks of Sibanye, it would be advisable for investors to forgo some of the upside in exchange for reduced downside risk and instead opt for some of its peers, like Impala Platinum (IMPUY), or smaller profitable companies, like Sylvania Platinum (SAPLF).

For further details see:

Sibanye Stillwater: High Risk, High Reward