SBSW - Sibanye Stillwater: When A Solid Business And Market Fundamentals Are Not Enough

2023-11-20 07:26:01 ET

Summary

- Sibanye Stillwater is a major player in the PGM industry, owning and operating two of the largest platinum mines globally.

- Since 2019, the company reduced significantly its leverage to 25.9% Total Debt/Equity and 44.5% Total Liabilities/Total Assets.

- The lower PGM prices affect SBWS's profitability, reducing its returns and margins. SBSW's profitability is average compared to its peers, with 12.1% ROTC and 15.2% ROE.

- SBSW distributes dividends with respectable yields at 7.2%(TTM). It is the highest compared to Impala (7.15%) and Anglo-American (6.52%).

- SBSW trades at 2.2 EV/EBITDA, 0.8 EV/Sales, and 0.8 Price/Tangible book value. Such figures are much lower than the five-year average and previous bottoms.

Introduction

Sibanye Stillwater (SBSW) is one the major players in the Platinum Group Metals ((PGM)) industry. It owns and operates two of the largest platinum mines globally. The company's operations are primarily in South Africa, Bushveld Ingeneous Complex . South Africa holds 80% of the global platinum reserves in Bushveld. Despite that, SBSW has mining and recycling operations in the US. The company entered the lithium and nickel markets in the last years, buying assets in Europe. However, they represent a tiny fraction of the company's revenue and bottom line.

Despite declining PGM prices, the company has robust balance sheets, pays solid dividends, and is undervalued compared to its historical multiples and industry peers. The freefall of PGM miners' stocks offers an opportunity to buy a solid business for cents on the dollar. However, I prefer to wait until the price action starts bottoming. In other words, the price forms a trend reversal pattern. Being too early or too late for the party costs money.

My verdict for now is a hold rating. However, I follow up closely on the developments in the PGM industry, and once the price forms a bottom, I will start building a position.

Platinum Group Metals Market

Like all industrial metals, PGMs suffer from similar issues: lack of capital investments, declining ore grades, and lack of skilled personnel. Conversely, I expect the demand to keep growing, thus widening the deficit. I will argue my thesis for the potential PGM bull market in a few charts.

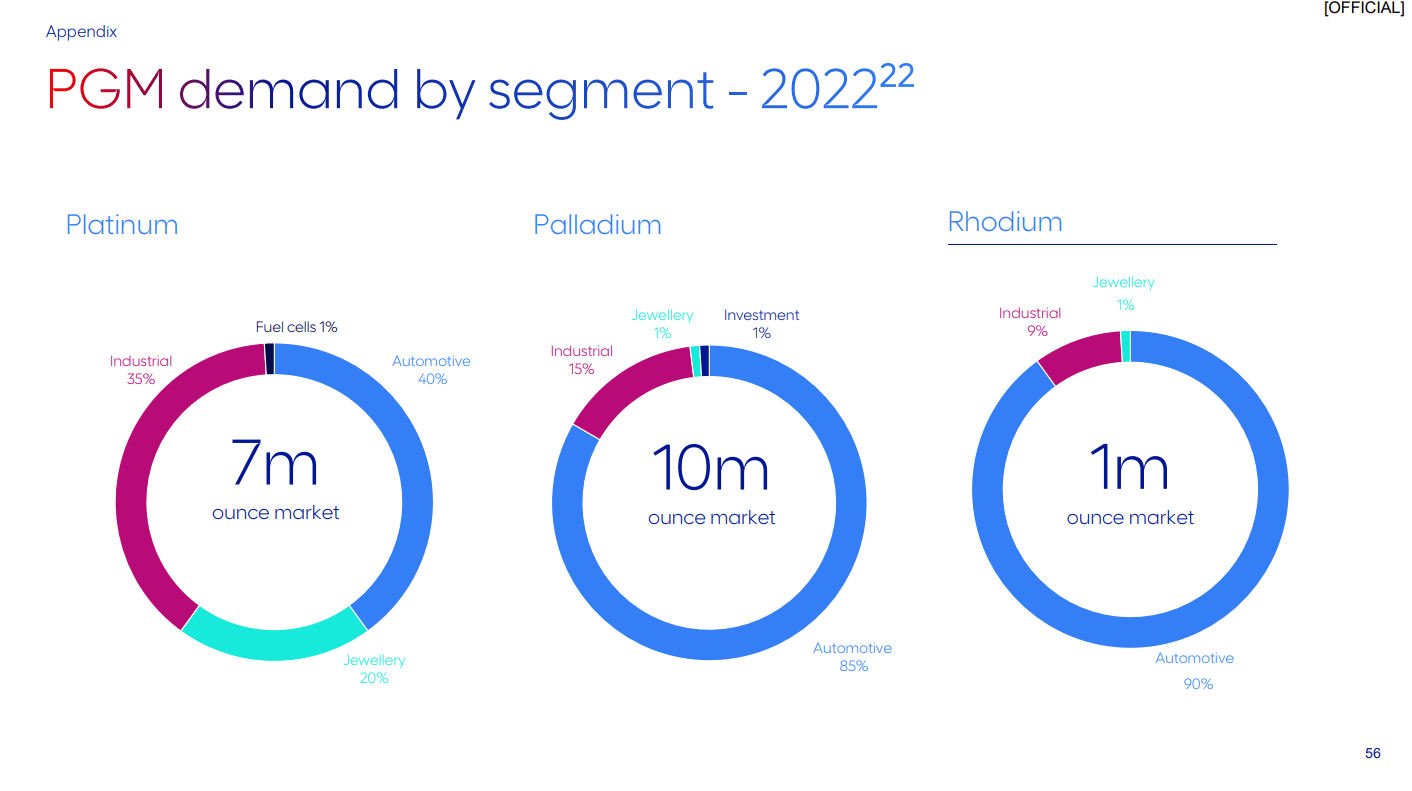

Let's see how we use PGMs by metal and by industry. The chart is from the Anglo American Platinum (AGPPF) presentation .

{kind=link}

Platinum has the most diversified demand compared to palladium and rhodium. 35% is used by tech and energy industries, 20% by jewelry, 40% by auto manufacturers, and 1% for fuel cells. The automotive industry consumes 85% of palladium and 90% of rhodium globally. The remaining quantities are distributed across tech, energy, and jewelry businesses.

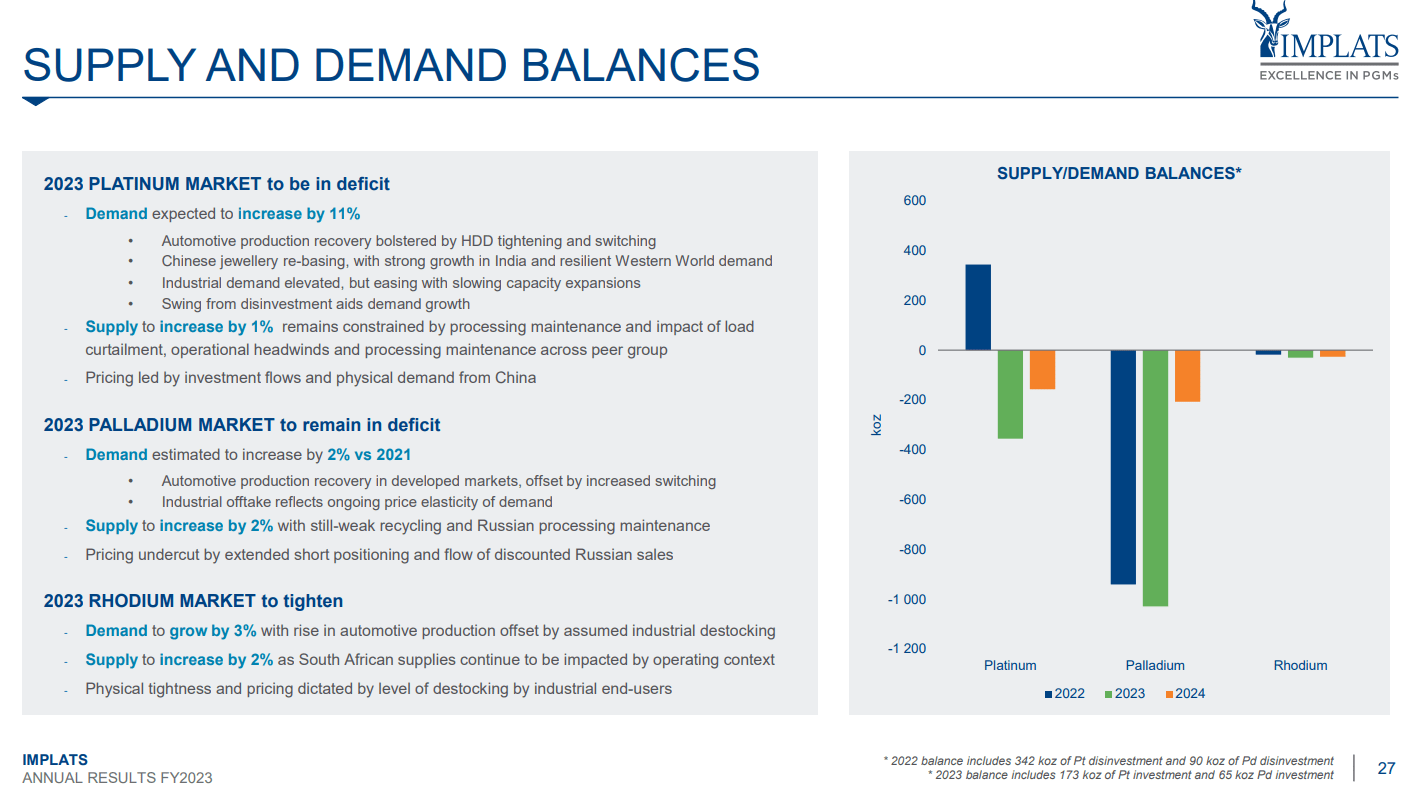

The chart below from the Impala Platinum (IMPUY) presentation shows the expected PGM demand and supply dynamics.

{kind=link}

The platinum and palladium deficit is expected to grow in the next year. The primary driver is the automotive industry. ICE cars are here to stay longer than anticipated by clean energy proponents. To be environmentally compliant, they are equipped with exhaust gas catalytic converters, consuming large quantities of PGMs. A lack of capital investments constrains the supply side.

On top of that, two countries dominate the PGM market: Russia (palladium) and South Africa (platinum and rhodium). Russian palladium exports have not been sanctioned; however, some mines are in care and maintenance, and recycling is still weak. South Africa has profound economic and political problems affecting deeply the mining industry. The primary issue is the power supply cuts exercised by ESCOM (the national utility company).

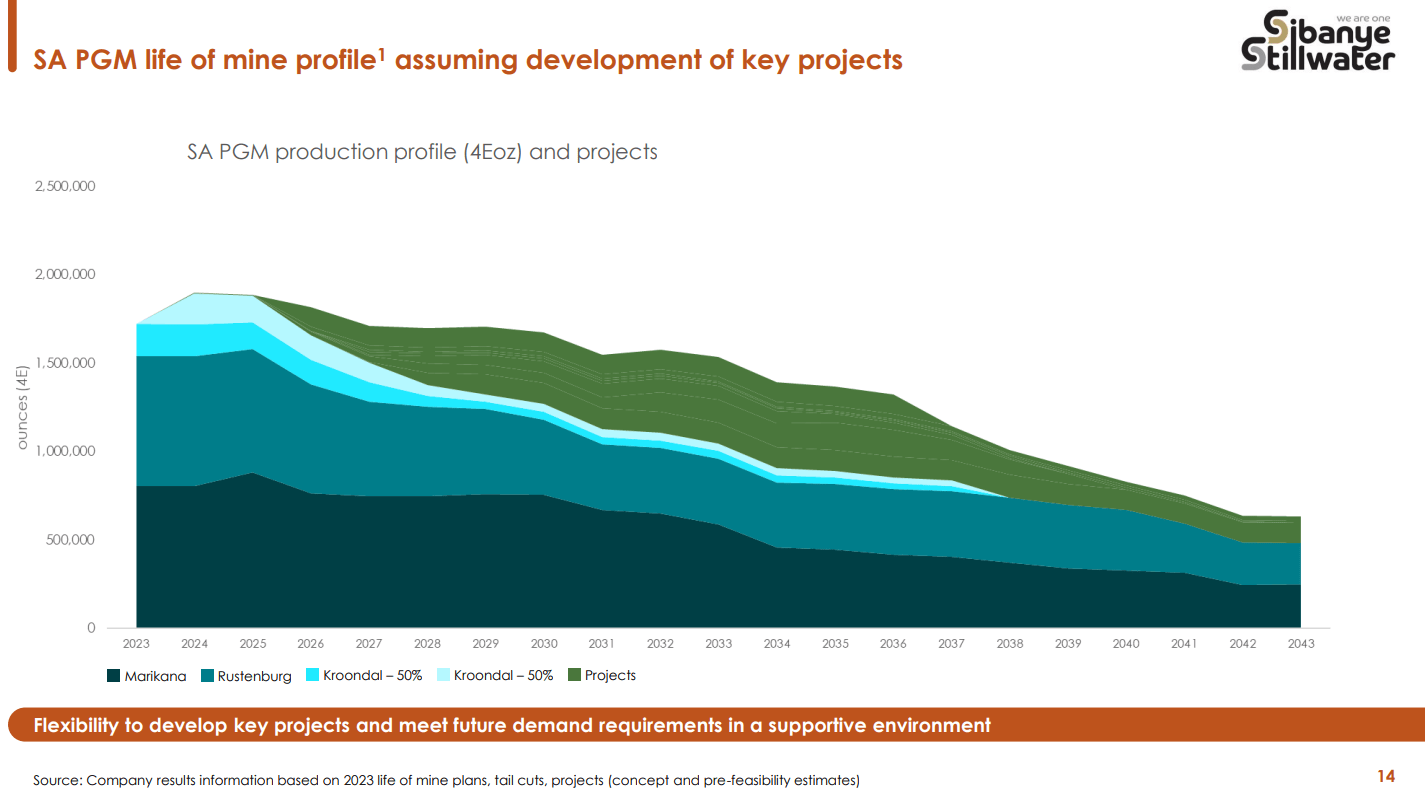

As I mentioned earlier, more than two-thirds of global platinum comes from the Bushveld complex in South Africa. The chart is from the last SBSW presentation .

{kind=link}

The chart above shows it is expected to reach the PGM supply cliff in the coming years. The Life of mine for a few of the largest PGM mines globally after 2025 will shrink significantly unless there are new notable discoveries. Developing a new mine from scratch usually takes over ten years of PGM and noble metals (gold and silver). Even if we invest all the money needed in CAPEX, we will see the results at the end of the decade if we are lucky.

Now, let's move on to the SBSW business.

Sibanye at glance

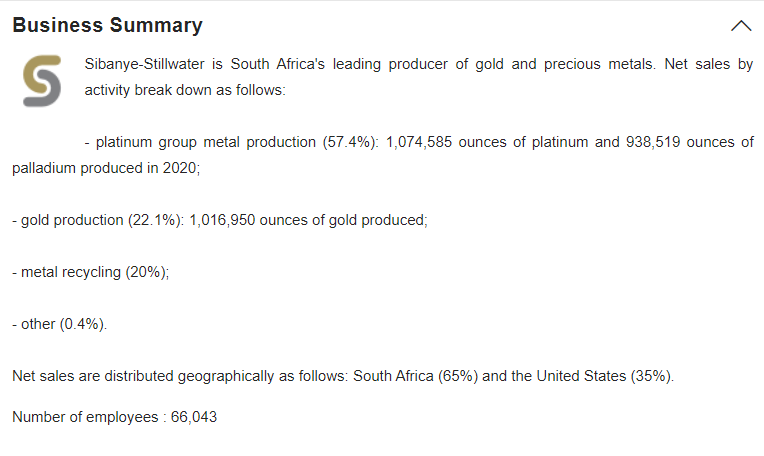

SBSW is a diversified PGM miner. The image below shows the company`s net sales by activity.

{kind=link}

57% of the sales come from PGM mining, 22% from gold mining, and 20% from scrap recycling. Geographically, the sales are divided between South Africa (65%), the US (33%), and Europe (2%).

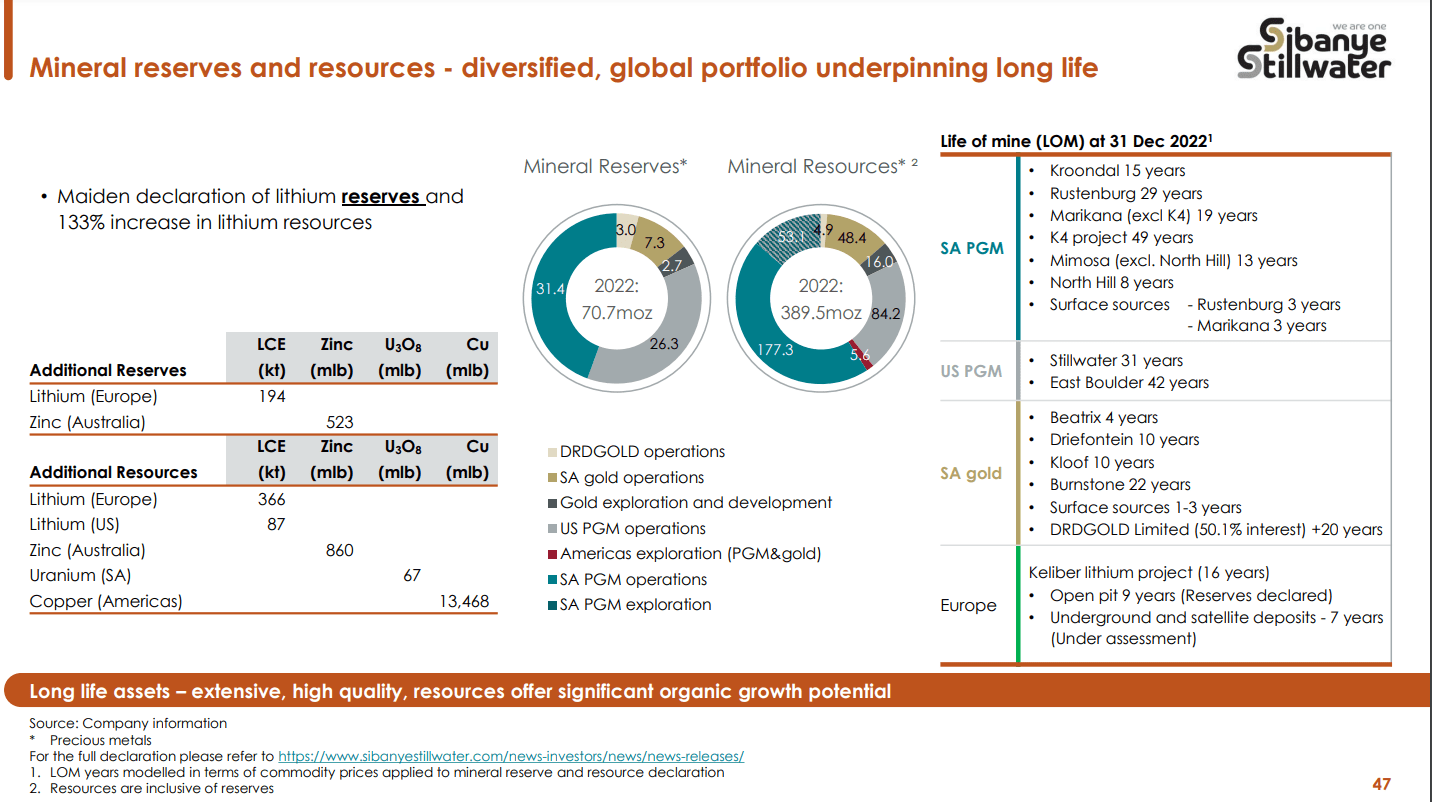

SBSW owns several mines in South Africa. Marikana is the second largest platinum mine globally, while Rustenburg is the fifth one. The chart below gives some details on the SBSW reserve and resource base.

{kind=link}

South Africa's PGM operations hold 31.4% of the reserves, and the US PGM operations 26.3%, respectively. The remaining is distributed between gold operations. The resources are more diversified. However, PGM (US and South Africa combined) are 67%. The company owns some uranium, zinc, copper, and lithium assets, though their contribution to its bottom line is negligible, at least for now.

The company`s assets' average life of mine (LOM) is as follows: South Africa PGM mines 18.5 years, the US PGM mines 36.5 years, and South Africa Gold mines 11.2 years.

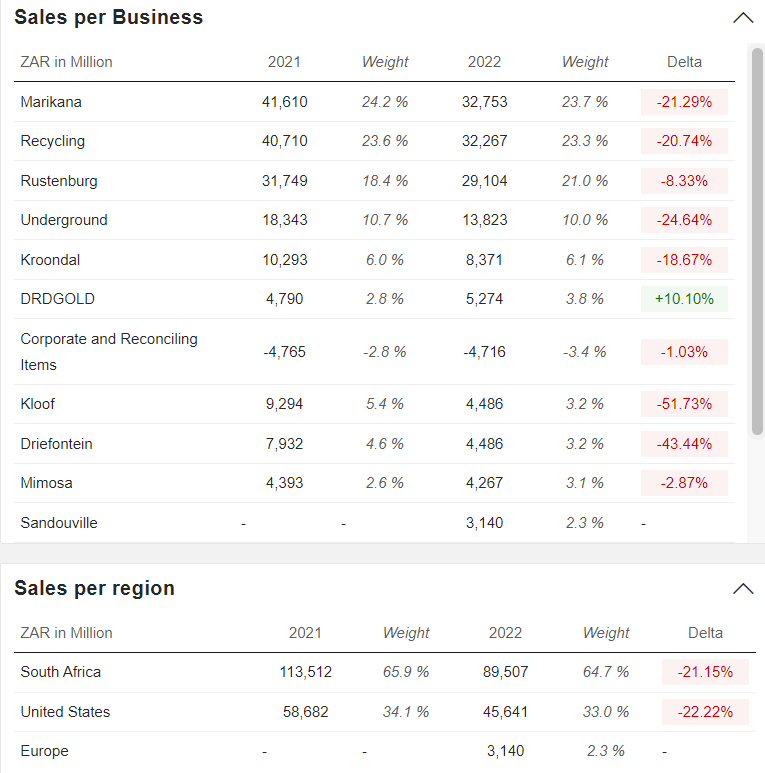

The primary revenue drivers are the Marikana and Rustenburg mines and the US recycling division. Combined, they contribute 66% of the company`s sales.

{kind=link}

The remaining 34% comes from other PGM operations and gold mining in South Africa. It's worth mentioning SBSW's 50.1 stake in DRD gold . The latter is specialized in retrieving residual gold from tailings. It has three metallurgical plants: Ergo, City, and Knight; apart from that, the company owns 3.0 M oz reserves and 4.9 Moz resources. DRD's annual gold production is 178,919 l oz at $1,528/oz AISC.

Operations overview

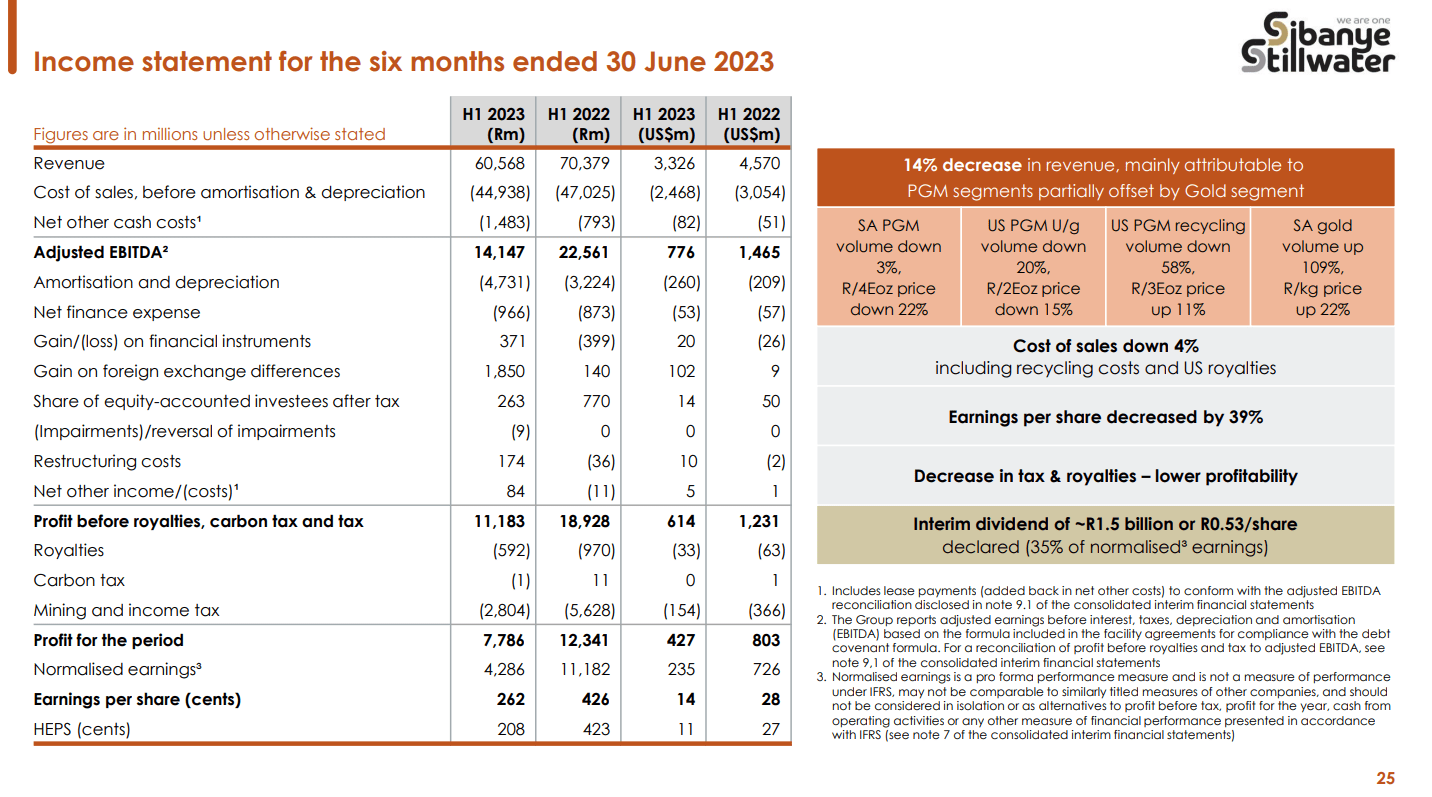

SBSW revenue declined HoH due to falling PGM prices.

{kind=link}

The company realized $776 million Adjusted EBITDA in 1H23 compared to $1,465 million in 1H22. The primary driver for 1H22 strong performance was the parabolic move in PGM prices caused by the Russian invasion of Ukraine. The war caused fears for the future PGM supply and pushed the prices to reach new highs. For a few weeks after the invasion, palladium prices were above. $2100/oz and platinum $1100/oz. SBSW's net profit for 1H23 is $427 million compared to $803 million for 1H22, resulting in 1H23 $0.11 EPS and 1H22 $0.27 EPS.

Gold operations

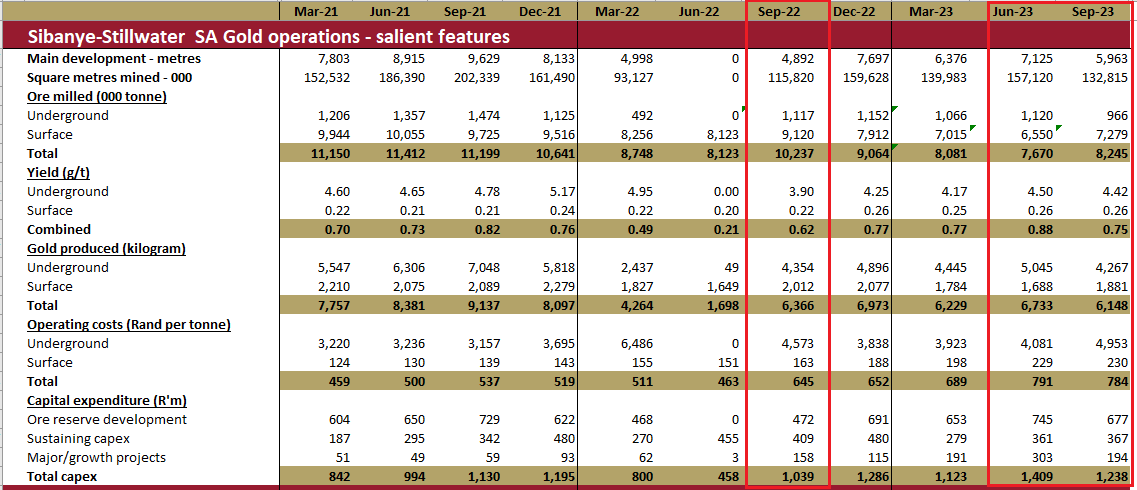

SBSW gold production had declined QoQ but remained stable YoY. The company produced in 3Q23 6,148 kg gold (216,864 oz), 2Q23 6,733 kg gold (237,499 oz), and 3Q23 6,366 kg gold (224,544 oz).

{kind=link}

The significant production decline came from the underground mining division. The output dropped from 5,045 kg in 2Q23 to 4,267 kg in 3Q23. Three mines, Driefontein, Kloof, and Beatrix, had lower underground outputs QoQ, resulting in lower total output.

SBSW AISC in 3Q23 was $2062/oz, in 2Q23 $1800/oz, and in 3Q22 $2207/oz. The primary reason for such growing costs is the declining mine yield. The combined mine yield (underground and surface) in 3Q23 was 0.75%, 2Q23 0.88%, and 3Q22 0.62%.

PGM operations

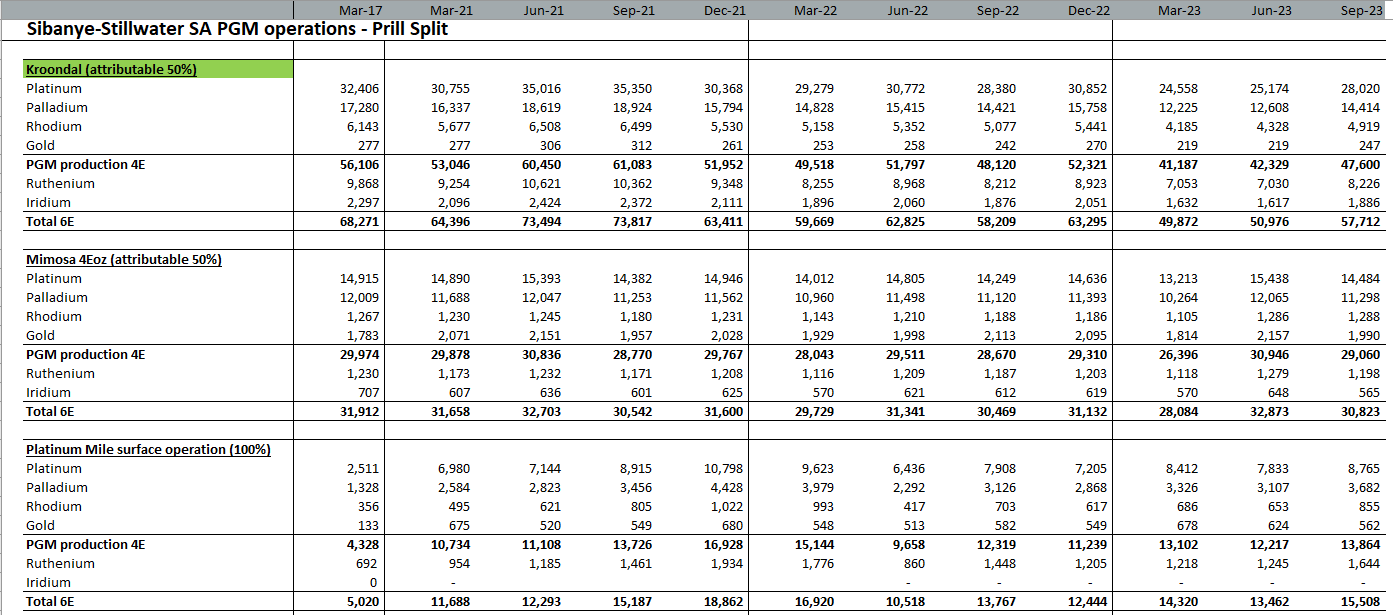

Let's look at South Africa's PGM results. The first chart shows the smaller mines and the second shows the flagship assets.

{kind=link}

Kroondal and Platinum Mile realized higher 4E (platinum, palladium, rhodium, gold) production figures than 2Q23. Ruthenium and iridium production increased across the mines QoQ and YoY.

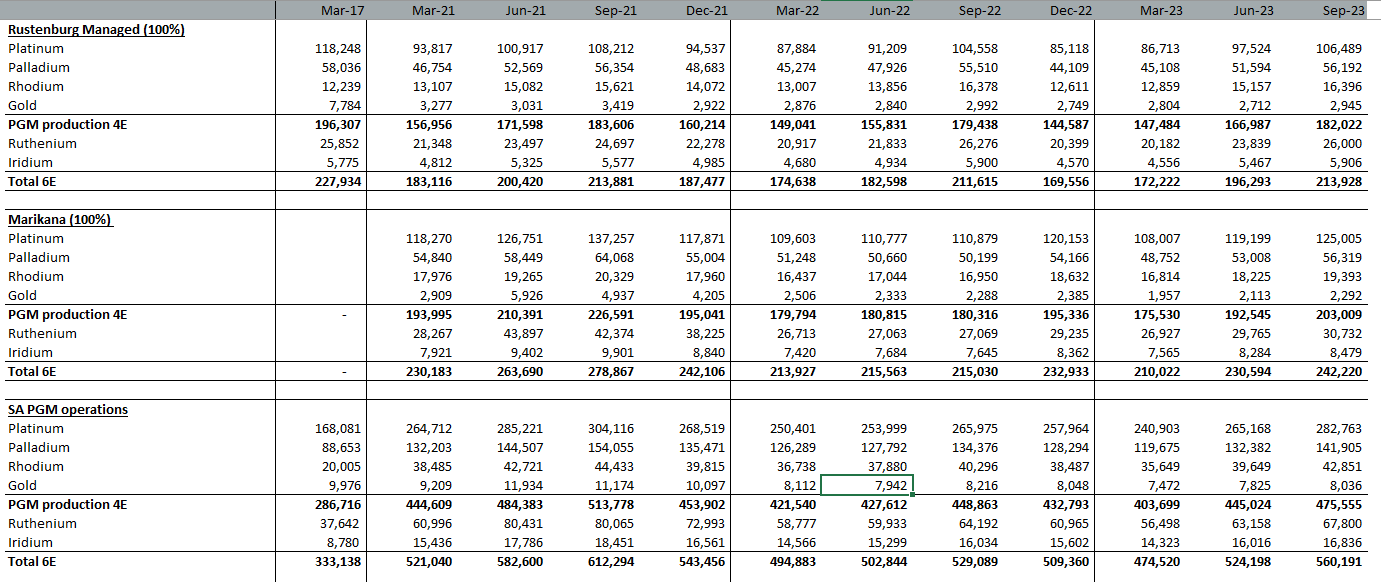

SBSW's flagship assets are Marikana and Rutenberg, producing 81.0% of SBSW South African PGMs.

{kind=link}

Rustenburg produced 182,000 oz 4E in 3Q23, or 9.6% growth QoQ and 1.6 YoY. Marikana realized similar production growth: 5.6% QoQ and 12.7% YoY. Looking deeper in detail, production figures of all 4E metals improved QoQ and YoY. The total 6E (4E + iridium and ruthenium) figures show consistent growth for the last six quarters.

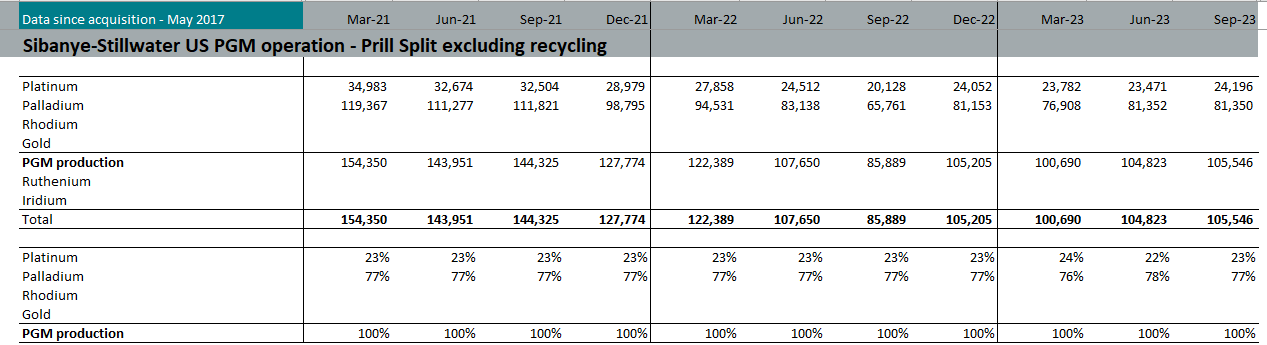

US PGM mining has realized negligible growth QoQ. However, YoY, the output grew 23%.

{kind=link}

SBSW mines only platinum and palladium from its US assets. The latter has been the primary revenue source of the SBSW US division. Let's look at the recycling business. The figures for the last quarter have not been published yet, as seen in the tale below.

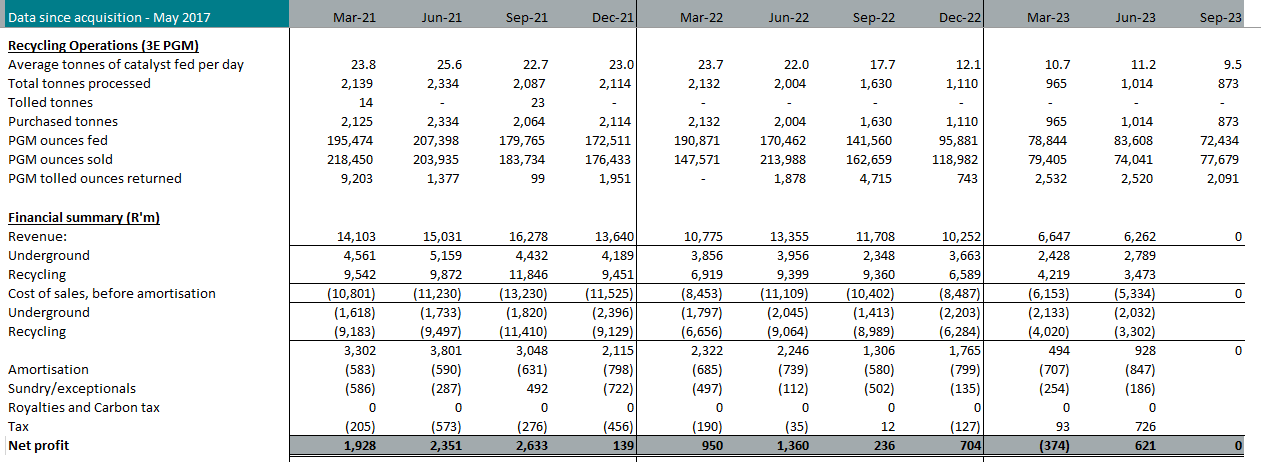

{kind=link}

The revenue from recycling has been declining over the last quarters. In 3Q23, it reached record low figures of 189 million dollars, well below the company`s average for the previous nine quarters. The primary reason is the lower daily input, averaging 9.5 tons in 3Q23. This figure is 46% lower than 3Q22.

SBSW has a European operation, the Keliber lithium project in Finland, and the Sandouville nickel refinery in France. The lithium project has a long time to go, while the refinery brings in 2.3% of the company's revenue.

Company Financials

Despite the steep bear PGM market, SBSW maintains a neat and clean balance sheet. It has $1.18 billion cash and $1.38 billion debt. Compared to Impala Platinum and Anglo American Platinum, the company is not in the best position. The former has $1.43 billion cash and $137 million debt; the latter has $1.77 billion and $411 million. However, the SBSW cash-to-total debt ratio is still excellent, at 85.8%.

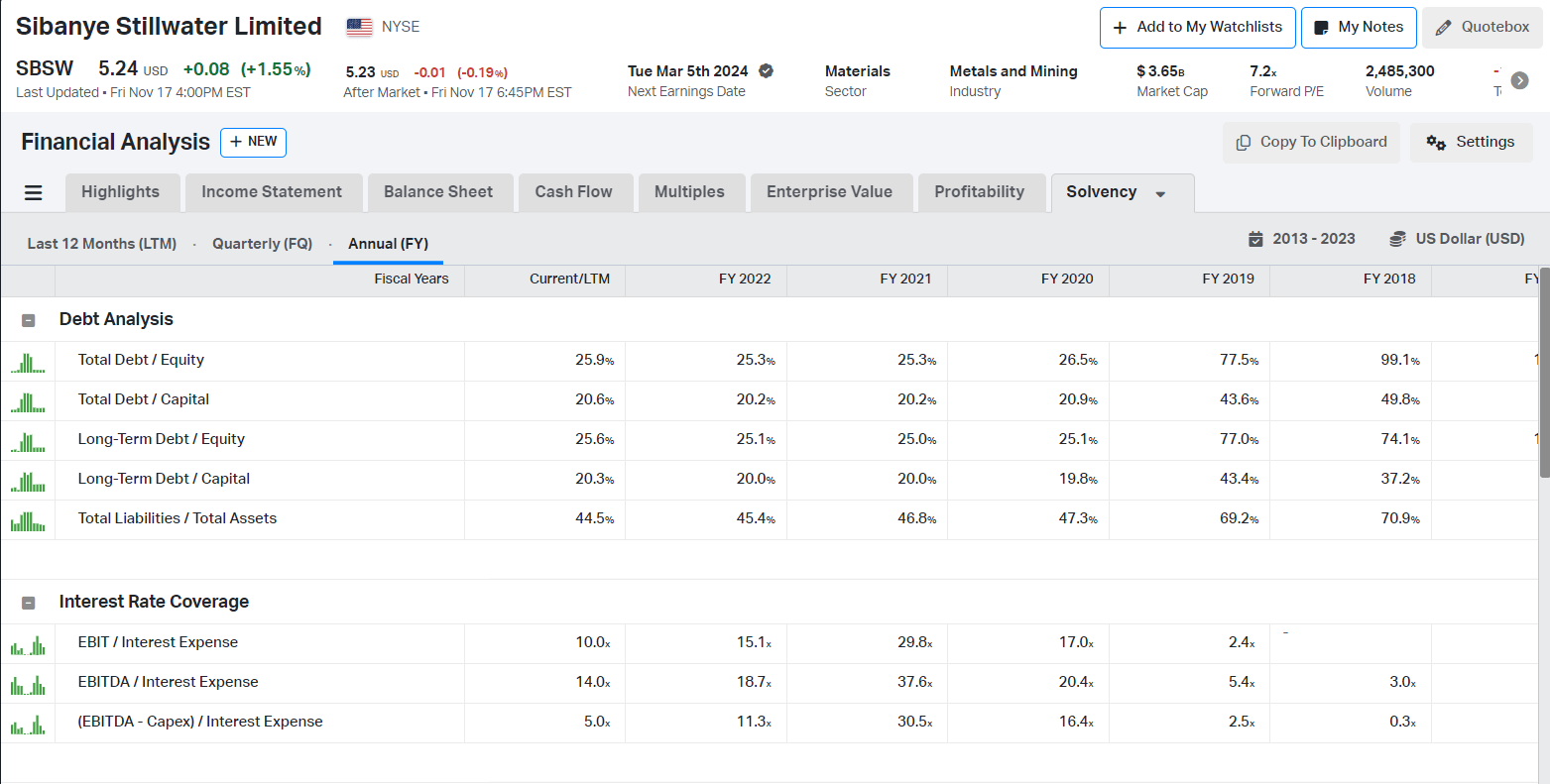

Despite that, SBSW has notably improved its balance sheet since 2018.

{kind=link}

In 2019, the company had Total Debt/Equity at 99.1% and 70.9% Total Liabilities/Total Assets. The last figures are much better: 25.9% Total Debt/Equity and 44.5% Total Liabilities/Total Assets. SBSWS's low leverage results in solid interest coverage. Even at declining EBITDA, the coverage remains adequate. For the last three years, EBITDA/Interest expense has been higher than 10.

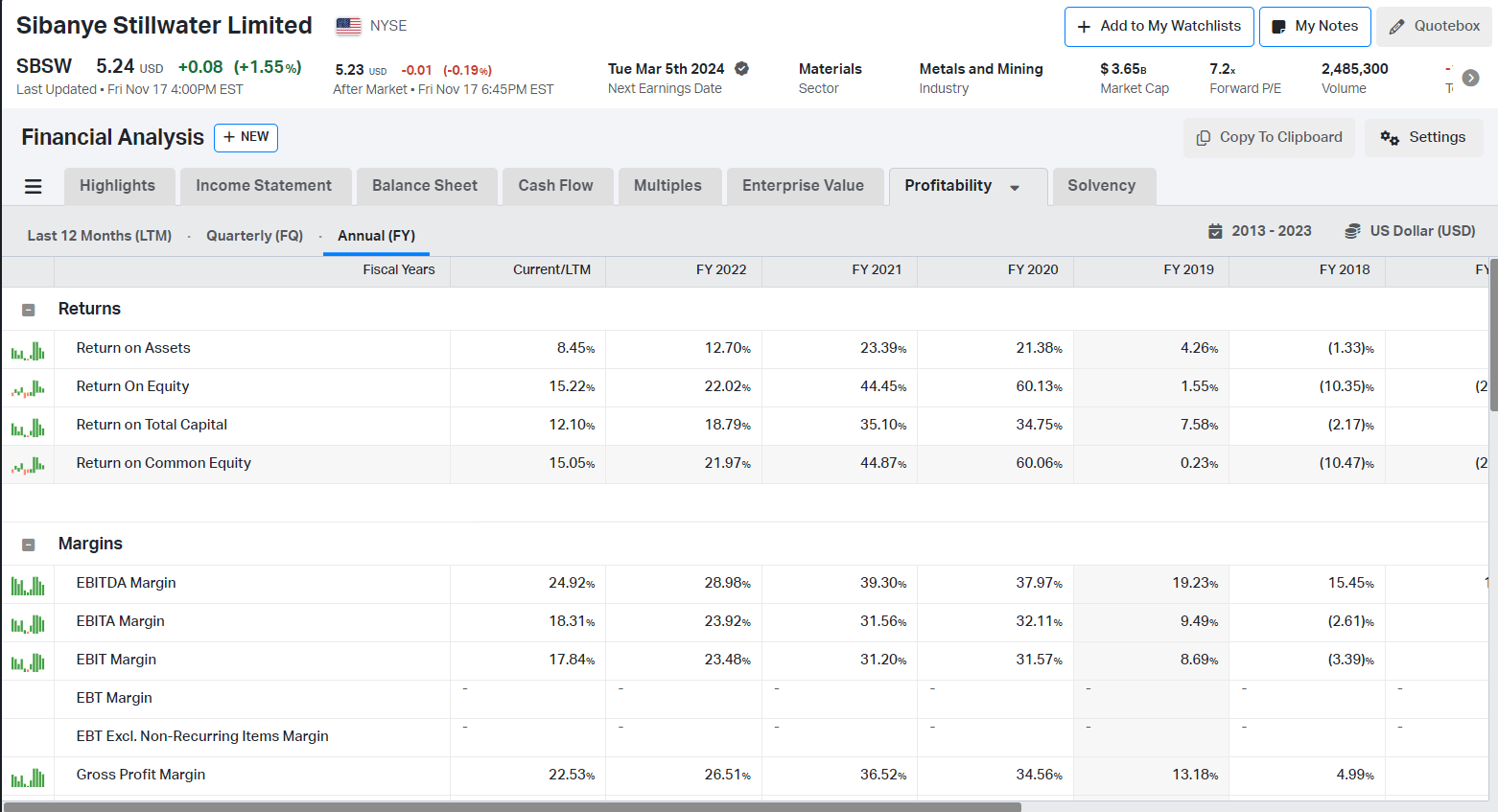

SBSW's profitability is average compared to its peers, with 12.1% ROTC and 15.2% ROE. Impala has 10.8% ROTC and 5.04% ROE, while Northam Platinum (NPTLF) has 20.7% ROTC and 8.2% ROE. The top performer is Anglo-American Platinum, with 23.2% ROTC and 23.20% ROE.

{kind=link}

The lower PGM prices affect SBSW's profitability, reducing its returns and margins. The gross margin remains in the lower percentile for PGM miners. For reference, Northam realized 41.9% gross margin and Anglo American 27.6%. Impala is the laggard among SBSW peers, with a 20.9% gross margin. Going further down in the income statement, the EBITDA margin has declined following the PGM bear market. Compared to its competitors, SBSW is the last, while Northam is the best performer.

It is essential to mention that those figures do not mean SBSW is not profitable. The difference comes from distinct revenue structures between the companies. SBSW has more revenue sources not limited to PGM mining and South Africa, while Northam is focused on PGM mining in South Africa, with leading revenues from rhodium mining.

SBSW distributes dividends with respectable yields at 7.2% ((TTM)). It is the highest compared to Impala (7.15%) and Anglo American (6.52%). Northam does not distribute dividends.

SBSW valuation

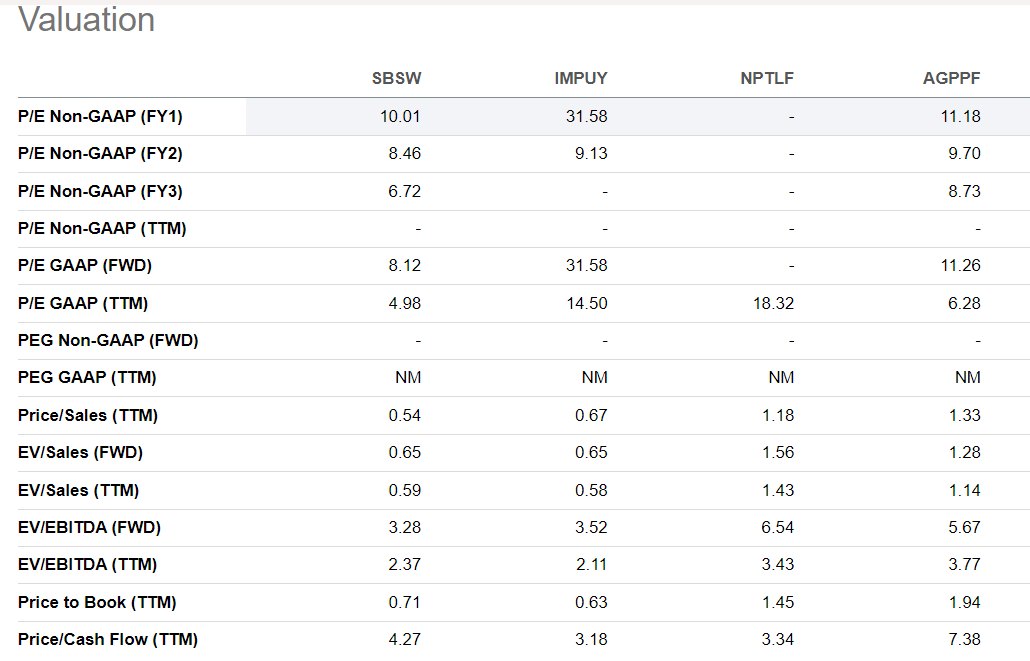

All platinum miners are cheap, but some are cheaper. In the table below, I compare SBSW with Impala, Northam, and Anglo American.

{kind=link}

Impala is the most undervalued of the group based on all three multiples, being tightly followed by SBSW-Northam and Anglo American command much higher multiples. The latter is the most expensive, with a 1.94 Price to Book, 3.77 EV/EBITDA, and 1.14 EV/Sales.

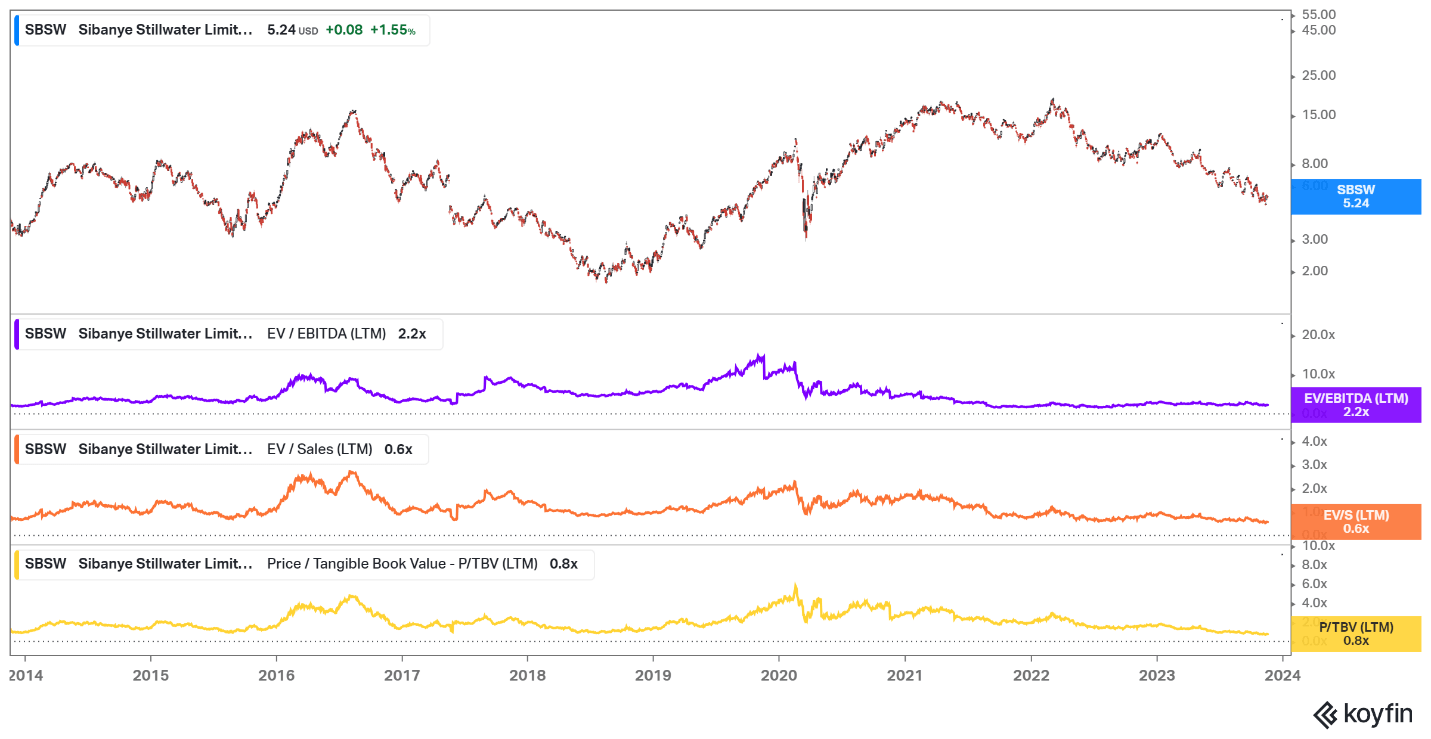

Looking at the historical SBSW multiples, I reached the same conclusion - the company is deeply undervalued.

{kind=link}

SBSW trades at 2.2 EV/EBITDA, 0.8 EV/Sales, and 0.8 Price/Tangible book value. Such figures are much lower than the five-year average and previous peaks. Besides that, those multiples are the weakest for the last ten years. In 2015, the palladium traded at $500-600/oz, and platinum was at similar prices as today's. However, at the same time, SBSW traded at 5.9 EV/EBITDA, 1.6 EV/Sales, and 3.2 Price/Tangible book value.

Price Action

Platinum and especially palladium prices are in a free-fall regime. To fade such a strong trend is not the cleverest thing investors can do. In the long term, I expect the platinum price to increase, resulting in a bull market of PGM stocks. However, now it's time to sit tight and wait patiently.

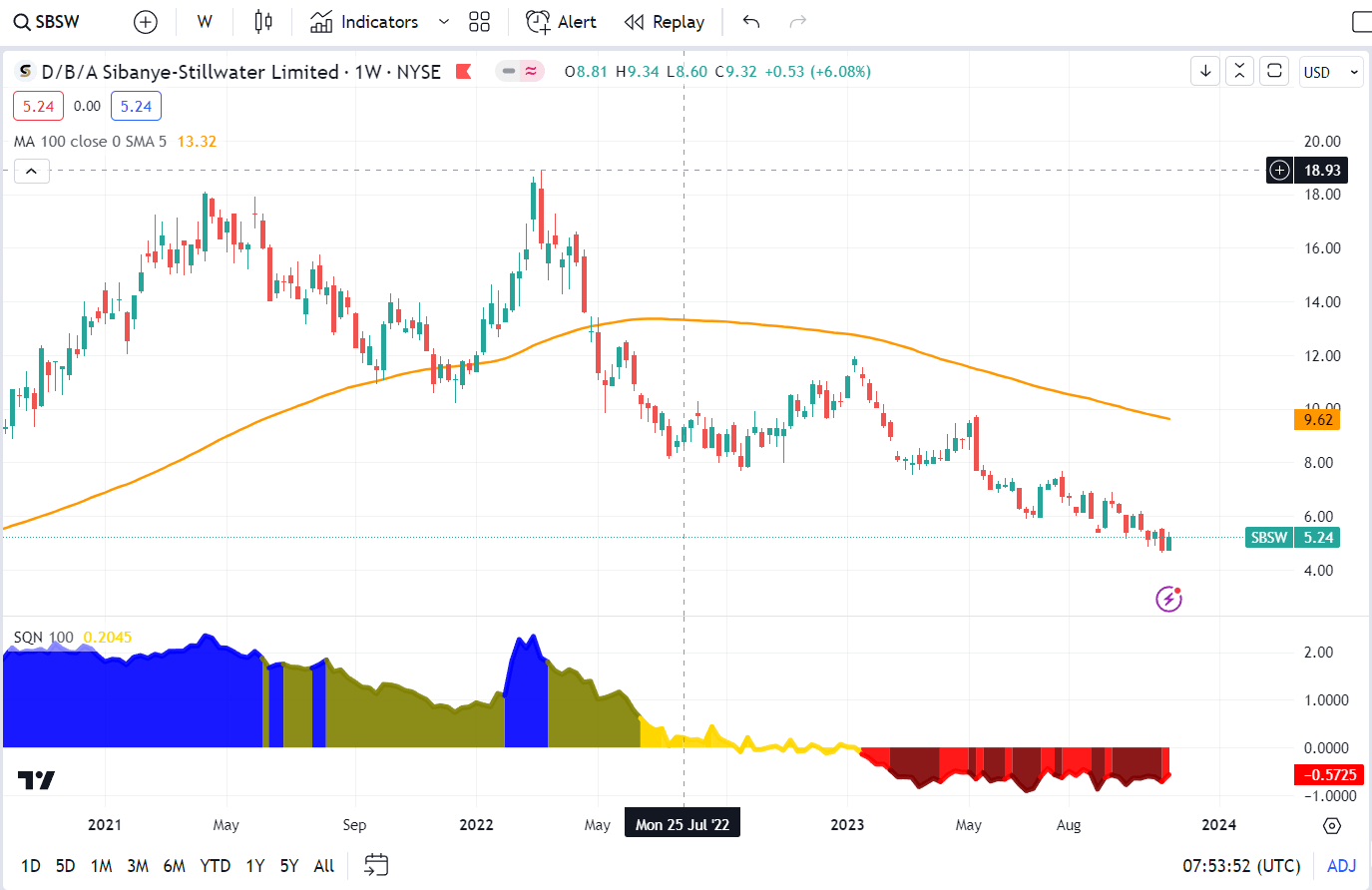

Let`s see SBSW weekly chart.

{kind=link}

The price is well below the 100 weekly simple moving average and shifts between bull quiet and bull volatile regimes. The over-extended trend has an advantage; sooner or later, the reversion to the mean comes into force, and the price reverses in the opposite direction. To consider an entry, I like to see a bottom pattern, such as an inverted head and shoulders, or at least several candles moving in a narrow range. I stay on the fence and patiently wait for supportive price action.

Risks

South Africa dominates platinum and rhodium production. Russia leads in palladium production. On top of that, we have a few public companies in South Africa responsible for 90% of the global PGM output, operating in one region. PGMs, especially platinum and rhodium, are the most exposed industrial metals to country-specific risk. Even uranium is not so concentrated in one region.

The political risk of operating in South Africa is least high given the multiple issues in the country. On the other hand, I believe this is why a solid company such as SBSW trades at such a steep discount. The market already priced the country's risk. Yes, it can go much worse from here with ESCOM's regular power outages and potential miners' strikes.

The most pronounced risk in China as a primary global importer of commodities. If the Chinese economy is in a bad mood, almost all industrial metals dive, and PGMs are no exception. China's GDP in 3Q23 grew by a surprising 4.9% compared to 3Q22, beating the forecast of 4.6%. If the Chinese economy's growth remains resilient, the demand for PGMs will keep rising.

Financially, SBSW remains stable despite the severe PGM price fluctuations. I do not expect any issues, even at lower PGM prices, due to the company's robust balance sheet and diversified revenue sources.

Investors takeaway

SBSW is a major player in the niche industry of PGM mining. The company owns and operates two of the biggest platinum mines globally. Despite the declining PGM prices, the company remains profitable and maintains a healthy balance sheet. SBSW distributes dividends with respectable yields at 7.2%. The company is extremely cheap compared to its historical multiples. Even in 2026 when palladium traded 40% lower and platinum traded at a similar price, SBSW commanded higher multiples. Despite company strengths and a creeping PGM deficit, I prefer to wait. I am not keen to fade strong trends. My verdict is a hold rating.

For further details see:

Sibanye Stillwater: When A Solid Business And Market Fundamentals Are Not Enough