SMAWF - Siemens: Buy The Weakness And Potentially Enjoy Double-Digit Returns

2023-09-27 14:50:08 ET

Summary

- Siemens, though subject to cyclical business trends, has seen its stock fluctuate between undervalued and overvalued levels over the past few years.

- Siemens reported solid Q3 earnings, with €18.9 billion in revenue, up 10% YoY, and anticipates future EPS growth.

- The recent 20% stock price drop presents a chance for value and income-focused investors to acquire a high-quality business at an attractive valuation.

- At a Forward PE Ratio of 11.1x FY25 earnings and a 3.69% forward dividend yield, the company appears undervalued compared to its historical standards.

- According to my analysis, purchasing Siemens shares below €130 per share could potentially yield annualized low double-digit returns in the coming years.

Investment Thesis

Siemens (SIEGY)(SMAWF), is a company I've been following for many years now, and while somewhat cyclical in its nature, it's a high quality business, and I've been actively trading in and out of the stock. What I've observed is that Siemens tends to fluctuate between undervalued and elevated valuations. In my view, it's often a smart move to sell shares when they're at their peak and then patiently wait for a more favorable entry point. This strategy aligns with the understanding that Siemens isn't a rapid-growth company, so making the most of its stock often involves timing your investments carefully.

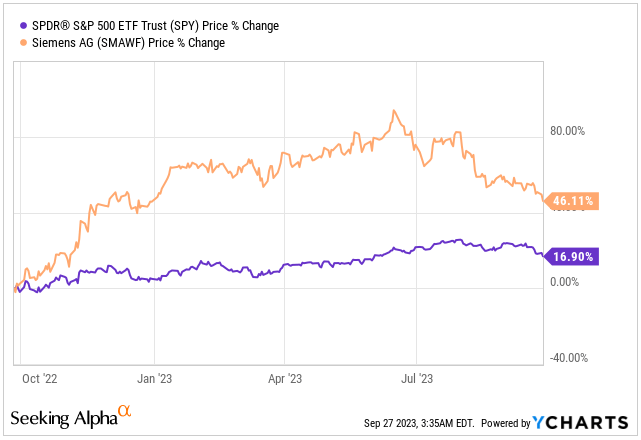

Siemens had quite the successful year in 2023. When we look at its performance over the last year, comparing it to the S&P 500 Index (SPX), it's clear that Siemens outperformed the index by a significant margin, close to 30%. What's interesting is that the S&P 500 itself had a strong year too, being fueled by the explosive growth of companies like Microsoft (MSFT), Nvidia (NVDA) and Broadcom (AVGO).

Price Return (Seeking Alpha / YCHARTS)

{kind=link}

However, it's important to note that Siemens has recently stepped back from its recent peak, with its stock price dropping by more than 20% from its high of €167. Right now, Siemens shares are trading at around €130, and I believe this presents an appealing opportunity for investors. It's worth keeping in mind that Siemens isn't known for lightning-fast growth, so historically, a solid return on investment has often meant getting in at an attractive valuation. Given the current situation, I think it's a great time to consider acquiring some shares below €130.

When you're fortunate enough to snag Siemens' stock at an attractive valuation, it opens up the potential for profit not only when the stock bounces back but also through a reliable yield, usually falling in the range of 2.5% to 4%.

When all these stars align - buying at the right price, securing that dividend yield, and benefiting from potential stock price gains - the combined upside often adds up to a double-digit return. It's this well-rounded blend of safety, income, and growth potential that makes Siemens an enticing choice for many investors in my view.

Note that my comparison here is based on the Price % return rather than the Total Return, as Siemens has already paid out a dividend of €4.25 for the year 2023.

Business Update

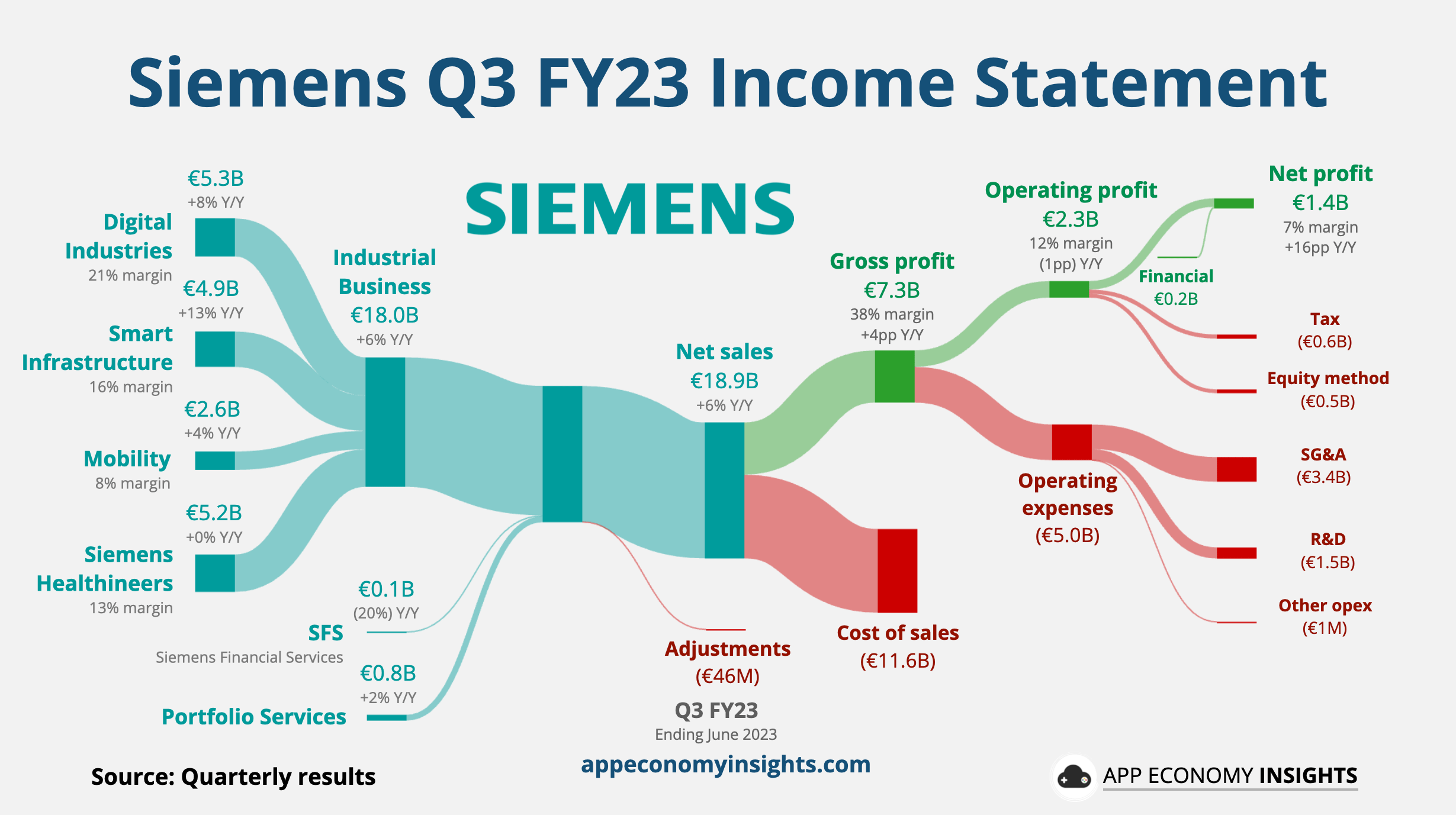

Siemens is undoubtedly a top-tier business with a long-lasting presence. It ranks among the most prominent industrial conglomerates globally, even after undergoing various divestments, spin-offs, and joint ventures that have reshaped its business portfolio. To get a broader understanding of the company's revenue sources, including its joint ventures, you can easily glean insights from a graph like this one.

Siemens Financial Breakdown (App Economy Insights)

{kind=link}

To understand how the company generates revenue, we can break-down Siemens' business into 4 major business areas :

Digital Industries "DI", 30% of Revenue, 21% Margin:

- DI is at the forefront of Siemens' operations, primarily dedicated to providing software solutions and cutting-edge automation technologies across various industries. Within its portfolio, DI offers a wide array of products and services, such as automation systems, industrial software, control systems, and digitalization solutions, all geared towards optimizing manufacturing and industrial processes.

Siemens Healthineers "SHS", 29% of Revenue, 13% Margin:

- SHS is Siemens' healthcare-focused segment, specializing in medical technology and healthcare solutions that cater to a wide range of medical needs. Its product range spans medical imaging, diagnostic equipment, laboratory instruments, and healthcare IT solutions.

Smart Infrastructure "SI", 27% of Revenue, 16% Margin:

- SI, Siemens' third-largest segment, is dedicated to delivering innovative infrastructure solutions for buildings, urban areas, and energy systems. SI offers a diverse range of products and services, including building automation, energy management, lighting solutions, and intelligent transportation and grid management solutions.

Mobility "MO", 14% of Revenue, 8% Margin:

- Siemens Mobility focuses on developing innovative solutions for transportation and mobility, covering rail and road transportation, including signaling and control systems, rolling stock, and intelligent traffic systems.

Siemens, given its substantial size, enjoys a remarkable level of diversification across its business segments. None of these segments contributes more than 30% of the total revenue, and the revenue streams are effectively spread across all areas. As a result, Siemens tends to maintain a robust net income margin in this sector, typically averaging around 5% to 8%. This diversification strategy adds a layer of stability and resilience to the company's financial performance.

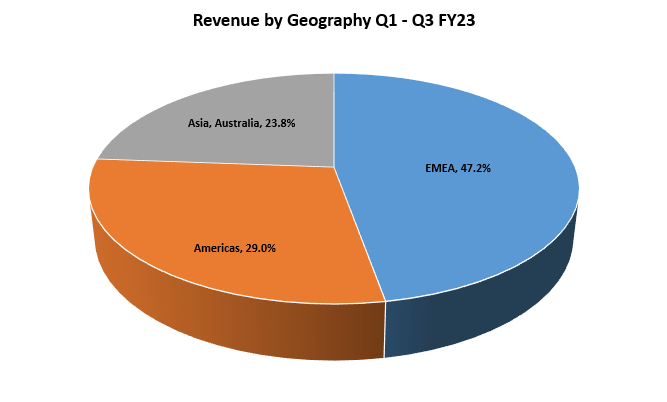

Siemens' strength lies not only in its diversified business segments but also in the geographic distribution of its revenue, contributing to its remarkable stability. The company operates in three major regions: Europe, Middle East, and Africa "EMEA" accounting for 47.2% of revenue, the Americas with a 29% share, largely driven by the United States, and Asia and Australia, contributing 23.8% of revenue, with China accounting for less than half of this share. This global presence underscores Siemens' resilience.

Revenue by Geography (Author's Graph (Data Siemens IR))

{kind=link}

You might be wondering, with such impressive diversification, what could have caused Siemens' stock price to drop by over 20%? The Q3 2023 earnings release presented very robust results.

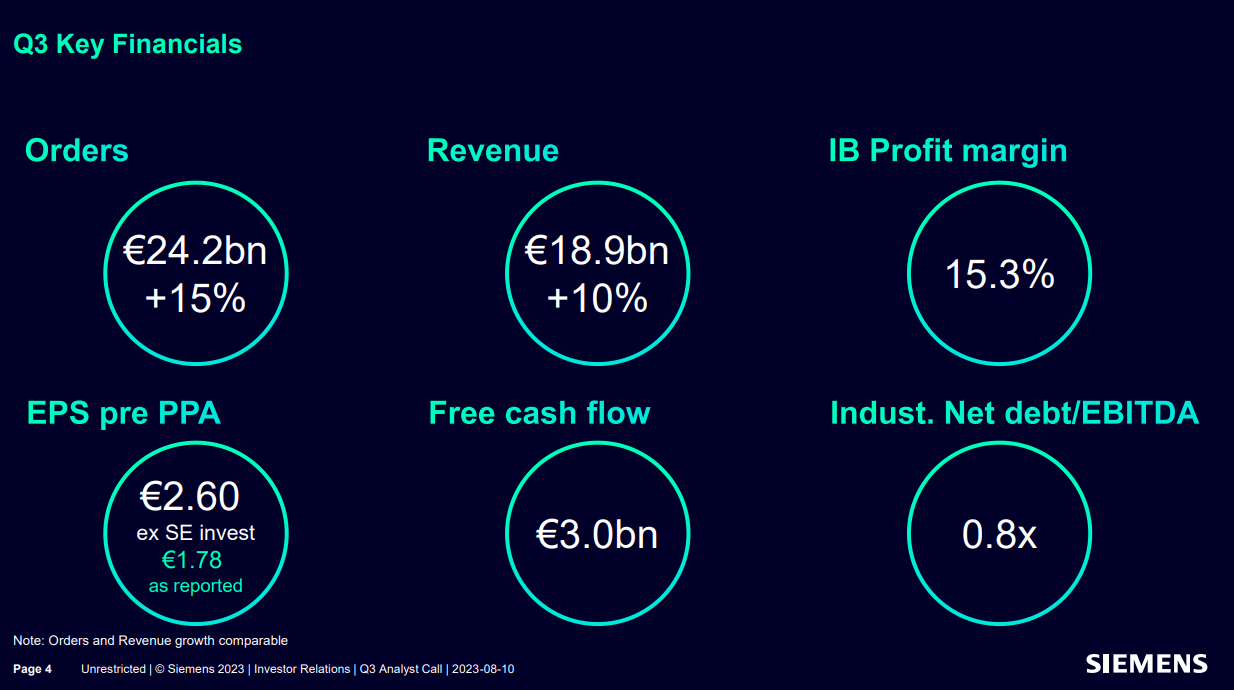

Order bookings surged by 15% to €24.2 billion, and sales showed a solid growth of 10%, reaching nearly €19 billion. Furthermore, the FCF increased significantly by 30%, totaling €3 billion, in contrast to the prior-year quarter's €2.3 billion.

Q3 Key Financials (Siemens IR)

{kind=link}

Siemens' SI and DI business segments performed exceptionally well. DI reported an 8% increase in revenue, amounting to €5.3 billion. The software segment within this unit experienced a remarkable 24% earnings boost, reaching €1.1 billion, with a noteworthy margin of 21.1%. SI, on the other hand, saw sales grow by 13% to €4.9 billion, and earnings surged by almost 40% to €770 million, resulting in an impressive margin increase of nearly 3 percentage points. Despite these strong financials, the market's reaction seems to have prompted a significant drop in Siemens' stock price.

After the earnings, Siemens encountered a lukewarm investor response for several reasons. Notably, there has been a dip in demand in China, which predominantly affects the DI segment. Orders in this segment experienced a 35% decline, amounting to €4.1 billion. Consequently, Siemens adjusted its profit forecast , now anticipating revenue growth to fall within the range of 13% to 15% for this business segment, as opposed to the previously projected 17% to 20%. Management also reduced the profit margin expectations by 0.5%.

{kind=link}

This adjustment comes as a bit of a surprise, especially considering that Siemens had raised its guidance twice earlier in the year. It signals the impact of China's economic weakness on a global scale. Siemens generated nearly a quarter of its revenue, approximately €16.7 billion, from Asia (including Australia) last fiscal year, with around 50% of that coming from China. Consequently, the German industrial giant has a substantial exposure to China and its economic development. Siemens' management and investors appeared to be somewhat taken aback by the decline in its Chinese business.

Embracing Weakness as a Potentially Lucrative Opportunity

Looking ahead, Siemens' management anticipates full-year revenue growth falling within the range of 9% to 11%, with all three segments expected to achieve double-digit percentage growth: DI 13% - 15%, SI 14% - 16%, and MO 10% - 12%. At the same time, the company is expecting slight improvement of margins in its largest segment, the DI segment, improving by 1% - 2%. Siemens has set its sights on achieving higher EPS ranging from €9.60 to €9.90 for the year, which represents a substantial increase from the prior year of only €5.47 , which was negatively influenced by reconciliation and tax expenses.

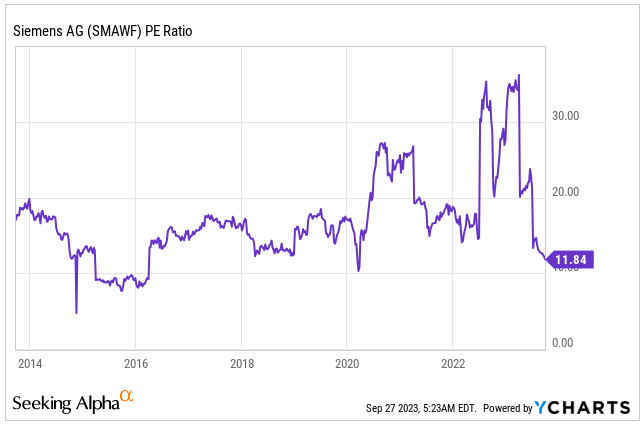

It's worth noting that this forecast does not take into account the Siemens Energy stake , which already contributed €1.14 to EPS in the first three quarters. Analysts, on average, expect Siemens to further boost adjusted EPS to over €11.70 by 2025, which translates to 18% growth over next 2 years. Given the current share price, this translates to an adjusted PE ratio of 11.1x for 2025 earnings. This is noteworthy when compared to a historical adjusted PE ratio of 16 over the last decade, indicating the potential for attractive valuation in the coming years.

Siemens PE Ratio (Seeking Alpha / YCHARTS)

{kind=link}

Furthermore, in February 2024, Siemens will enter the dividend season once again. Analysts are anticipating that the company will boost its dividend by more than 13%, bringing it to over €4.80 per share. This expected dividend yield, based on the current share price, stands at a notable 3.69%, surpassing the five-year average of 3.30%. These figures underscore that Siemens is currently undervalued both in terms of earnings and dividends.

With a payout ratio of 38% coupled with the projected growth in earnings, it appears that the potential for an annual dividend increase in the low double-digit percentage range is very likely, in my opinion. This reinforces the attractiveness of Siemens as an investment choice for those seeking both income and potential for dividend growth.

Bottom line is, Siemens' stock being somewhat cyclical exhibits enough volatility to allow for a strategic entry point below €130, which should be your personal buy threshold. It's worth noting that less than three years ago, the company's stock was trading at around €60 per share, representing an opportunity of lifetime to accumulate shares. Ultimately, the return on investment in Siemens will be greatly influenced by the price you pay, emphasizing the significance of timing.

Conclusion

Siemens, as a big conglomerate, does have its ups and downs due to the nature of its cyclical businesses. However, what makes Siemens stand out is its strategy of spreading its operations across four main business segments. This diversification means that Siemens doesn't depend too heavily on any one segment, with no single area contributing more than 30% of its revenue. Plus, the fact that it operates in across EMEA, Americas, and Asia & Australia adds an extra layer of reliability and stability to its overall performance.

During Q3 FY23, Siemens showed some strong earnings. Though they did adjust their guidance expectations slightly downwards for their largest segment, Digital Industries, mainly because of a slowdown in China, Siemens still looks set for solid growth in its EPS in FY23 and beyond. This suggests there's potential for investors to enjoy double-digit total returns if they can grab Siemens shares at a price below €130.

With Siemens' recent stock price dip of over 20% from its peak back in June, I personally see this as a fantastic opportunity for investors to snag this company at a very reasonable valuation. When you consider the attractive pricing, promising growth prospects, and Siemens' track record of stability, it's no wonder I'm giving this stock a BUY rating.

For further details see:

Siemens: Buy The Weakness And Potentially Enjoy Double-Digit Returns