GCTAY - Siemens Energy Might Be Well Positioned To Profit From Energy Transformation

Summary

- Siemens Energy offers a range of products and services from gas turbines, electricity infrastructure to wind turbines.

- The renewable subsidiary Siemens Gamesa has been a catastrophe over the last years, dragging down Siemens Energy.

- Siemens Energy is in the process of fully taking over Siemens Gamesa, while at the same time, the macroeconomic environment for the renewable business is improving significantly.

- Energy Transformation is a long-term trend and substantial investments will go into electricity and renewable energy for years if not decades, providing significant tailwinds to Siemens Energy.

- But profitability is low, and investors should wait for clear signs that the company manages to achieve higher profit margins on the back of the macroeconomic tailwinds.

Investment Thesis

(Note: all amounts in the article are in EUR. At the current exchange rate this is almost equivalent to USD.)

Unique range of services in the energy sector

Siemens Energy ( OTCPK:SMEGF , OTCPK:SMNEY ) has a wide and unique range of products and services in the energy sector, from gas turbines, power infrastructure to wind turbines, and future technologies such as hydrogen production with electrolysers. Its scale and geographic reach give it an outstanding position to benefit from macroeconomic trends and the energy transformation over at least the next decade in Europe, but also other geographies:

Several macroeconomic trends create significant demand over the next decade and probably longer

The transition to renewable energy requires installation of power-generation capacity but also significant investment in the electricity grid itself. Siemens Energy has a leading market position in low- and zero emission power-generation, and the transport and storage of energy. With over 100 GW installed wind-turbine capacity is the company is #1 outside of China in offshore wind and #3 in onshore wind.

Replacement of combustion engine cars with electric vehicles will aggravate the need for more electricity infrastructure. According to the German newspaper Handelsblatt , Germany alone needs to add 4.2MW additional net wind capacity (without replacements of existing installations) every day from 2023 to 2029 to reach the goal of having 115 GW capacity installed by 2030. By way of comparison: From 2010 to 2021 Germany managed to only install 2.3MW per day, about half of the future demand.

If you follow Siemens Energy, you will notice a steady stream of deal announcements across the full product range. Just a few days back Siemens Energy announced that together with Spain's Dragados Offshore they will build converter stations for two 2GW offshore wind links for the German transmission system operator Amprion. The links will connect the North Sea offshore wind farms to the grid. The deal is worth a whooping 4bn euro including maintenance over 10 years. Two days later Siemens Gamesa signed a preferred supplier agreement with German energy group RWE AG to deliver 1 GW turbines for what should become Denmark's largest offshore wind farm. Siemens Energy ended its fiscal year 2022 in September with an order backlog of 97.4 bn euros, especially notable given that revenue for the year was just 29bn.

And, sooner or later, the war in the Ukraine will come to an end or a stalemate, and the severely damaged electricity infrastructure will have to be repaired and renewed. Siemens Energy is in a very good position to benefit from here.

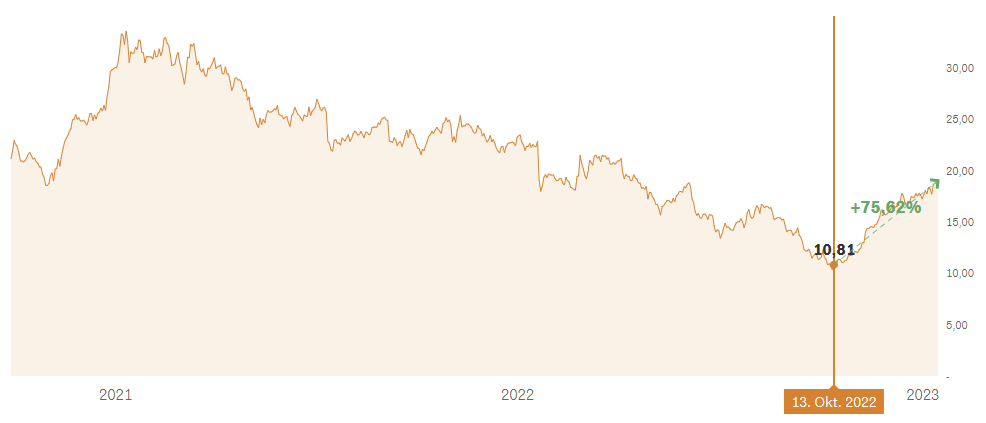

Shares still trade lower than at the IPO in September 2020

After the spin-off from the Siemens group in September 2020, the price of Siemens Energy increased from 22 to 33 euros at the beginning of 2021. In the face of more and more bad news from the Siemens Gamesa Renewable Energy ( OTCPK:GCTAF , OTCPK:GCTAY ) subsidiary, the share price dropped to not much more ten euros in October 2022. In the meantime, the group even had to leave the German DAX index due to its reduced market capitalisation.

Things have improved recently though - shares have gone up 75 percent from their low in October 2022, but they are still below their IPO price of 22 euros and far below the highs they achieved after the IPO.

Siemen Energy share price since IPO (Source: Handelsblatt)

{kind=link}

The growing optimism has one reason above all: Investors hope that Siemens Energy will get the problems at Siemens Gamesa under control. The company has successfully completed a public cash tender off to take over Siemens Gamesa at the price of EUR 18.05 per share. Operational improvements in the wind turbine business are now expected.

Risks to the investment thesis

In theory all this is really good, but at the same time Siemens Energy certainly did not have a great year 2022 (the fiscal year ended in September). Due to losses and restructuring cost at Gamesa, and additional cost of restructuring the business in Russia, the financial year ended with a net loss of EUR 647mn. The dividend for the year will be cancelled. At least FCF was 1.5bn, but company guidance is that it will turn negative this year.

So, the positive investment thesis needs to explain why things should get better going forward. I think Siemens Energy needs to achieve two objectives for the positive thesis to work out:

- A general increase its profit margins, and

- A clear turn-around at Siemens Gamesa.

Low profit margins

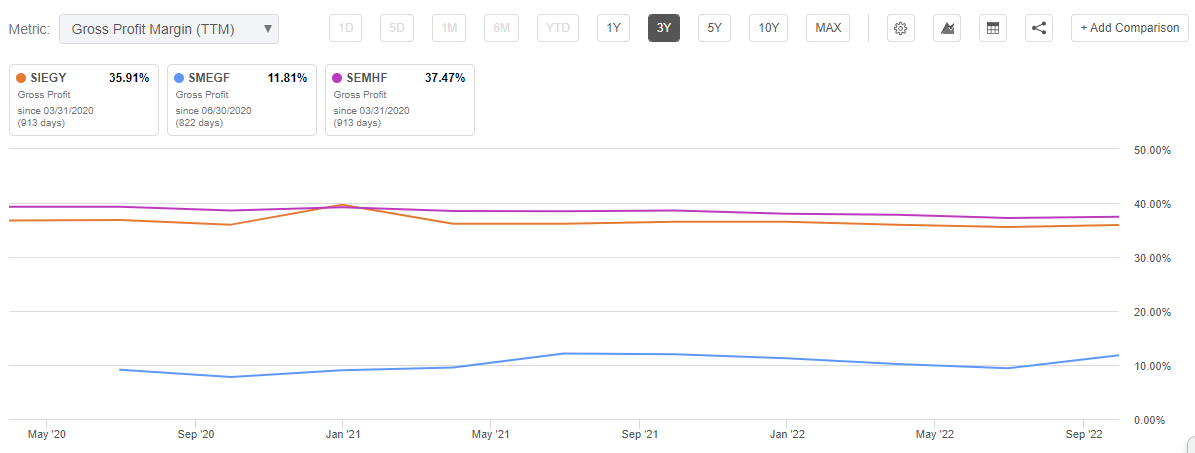

Siemens Energy was spun off from Siemens ( OTCPK:SIEGY , OTCPK:SMAWF ) in 2020 and this included a 67% share in the wind-turbine manufacturer Siemens Gamesa. Siemens still owns 35% of Siemens Energy (23% directly and 12% through Siemens Beteiligungen Inland GmbH). Siemens has clearly said that it wants to sell off its stake in Siemens Energy at the right price either through the stock market or an investor. There is an obvious reason, and Siemens has not been shy about it: weak profit margins in the energy business.

The chart below compares the Gross Profit margins of Siemens, Siemens Energy and Siemens Healthineers ( OTCPK:SEMHF ). Siemens Healthineers is another Siemens spin-off from 2018:

Gross Profit Margin of Siemens ((SMAWF)), Siemens Energy ((SMEGF)) and Siemens Healthineers ((SEMHF)) (Seeking Alpha)

{kind=link}

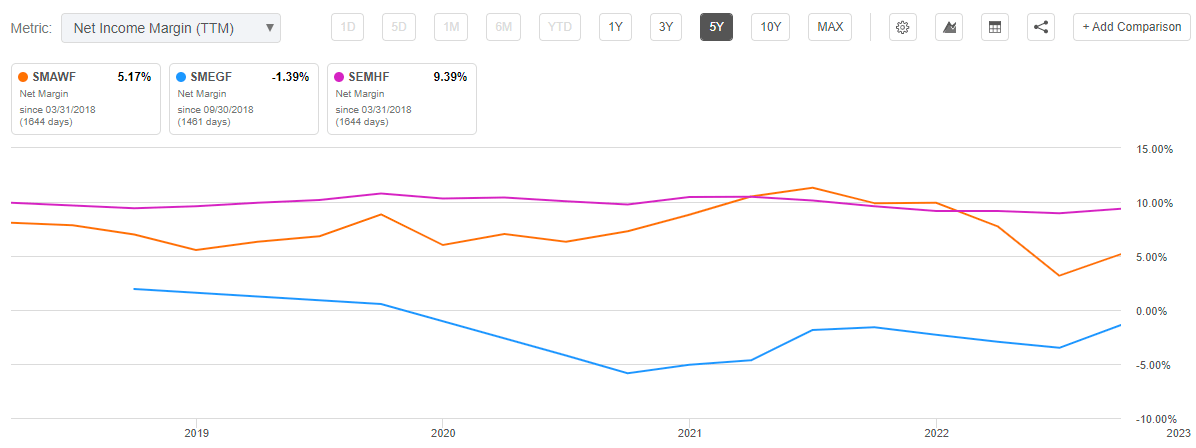

Comparing the Profit (Net Income) margins of the three companies shows a similar picture:

Profit (Net Income) Margin of Siemens ((SMAWF)), Siemens Energy ((SMEGF)) and Siemens Healthineers ((SEMHF)) (Seeking Alpha)

{kind=link}

You can clearly see the difference. Siemens Energy is significantly less profitable, or actually mostly not profitable at all. Accordingly, Siemens has kept 75.8% of Siemens Healthineers while it wants to get rid of Siemens Energy completely. If you take a look at the Equity Story presentation on the Siemens website; you will notice that Energy is not there, but Healthineers is the largest of the four industry segments (Digital Industries, Smart Infrastructure, Mobility, Siemens Healthineers) by revenue.

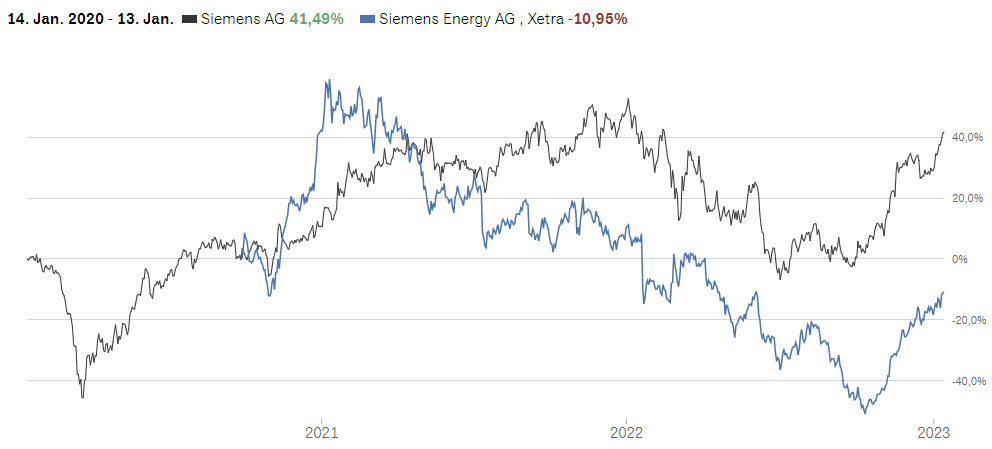

In fact, despite the recent gains Siemens Energy still trades more than 10 percent lower than at their September 2020 IPO, but Siemens is up more than 40 percent since that time. Siemens even had to write off 2.8bn in Q3 2022 after the Siemens Energy's share price had collapsed:

Siemens versus Siemens Energy share price (Source: Handelsblatt)

{kind=link}

So, if you were a Siemens shareholder at the time of the IPO, you would have done significantly better selling your Siemens Energy shares at the IPO and reinvesting the money back into Siemens.

How does Siemens Energy plan to improve profitability?

Siemens Energy guidance for fiscal year 2023 (which has started in October 2022) is for revenue growth between 3% to 7%, a profit margin (before special items) of 2% to 4%, and a significant reduction of Net loss compared to fiscal year 2022. The comparable profit margin for the fiscal year 2022 was 1.2%.

The table below is from a recent Siemens Energy investor presentation . It shows the key financial performance data for its four reporting segments - in the fiscal year 2022 and the FY 2023 guidance and, and additionally the mid-term target numbers. Mid term here means fiscal year 2025:(Note - Transformation of Industry includes Hydrogen electrolyser systems, Integrated EAD solutions and Services, and Industrial steam turbines.)

Siemens Energy key financial data and targets 2022 to mid-term (2025) (Source: Siemens Energy)

{kind=link}

I do find the aspirations on revenue growth conservative as the assumption is that the segments will grow in line or below their respective addressable markets. The company assumes that the addressable market for gas services stays stable with a minor increase from 32bn euros in 2021 to 34bn in 2025. They assume that the TAM for grid services will increase from 50bn to 62bn in the same timeframe. The TAM for Transformation of Industry is assumed to increase from 20bn to 31bn. Those numbers seem reasonable to me.

I think they are more aggressive on the Profit margins. At this time I am especially missing a more detailed execution plan how the target numbers will be achieved. I really want to root for the company since energy transformation is such an important step that needs to be accomplished for human development. But as an investor I also think that management does not provide enough tangible information yet on how they will improve the low profit margins, as this has been the situation for some time.

And there is the second thing that needs to be accomplished: the turn-around of Siemens Gamesa. Here I think management plans are even less tangible, although concrete steps have been taken to take full control of Siemens Gamesa.

Siemens Gamesa turnaround

It is an astonishing problem that global demand for wind energy has been very strong over the previous years, but no manufacturer has managed to be profitable, at least for the long-term.

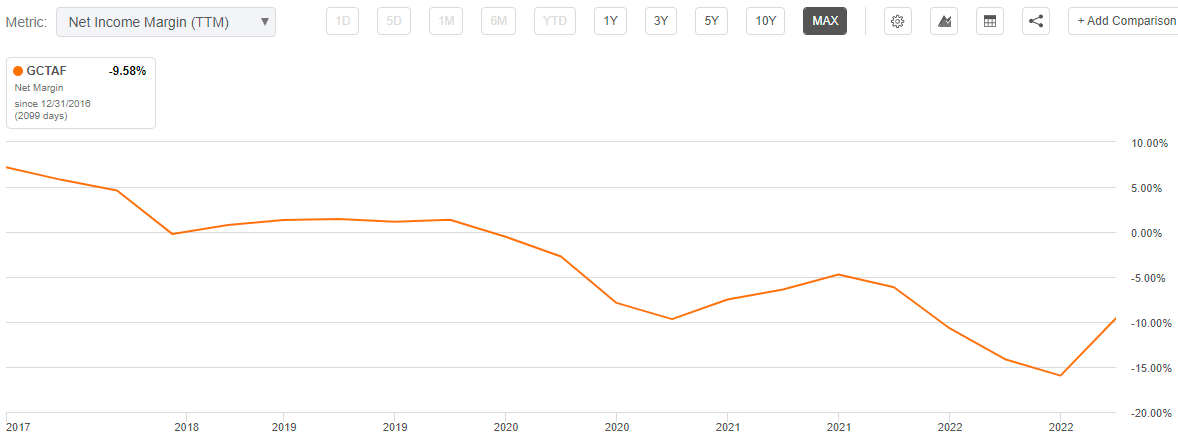

According to Blackridge Siemens Gamesa is the second largest wind-turbine manufacturer world wide - Vestas ( OTCPK:VWDRY , OTCPK:VWSYF ) being the largest - and it has been plagued by operational issues for years. A look at the development of their Profit margin gives a good impression what Siemens Energy needs to accomplish here:

Siemens Gamesa Profit (Net Income) margin (Source: Seeking Alpha)

{kind=link}

Siemens Energy made a public cash tender offer to take over Siemens Gamesa Renewable Energy at the fixed price of EUR 18.05 per share. In December it secured 92.72% which is more than enough to delist the company. This should be approved in a Siemens Gamesa special general meeting on January 25, 2023.

However, around 97 percent would have been necessary to squeeze out the free shareholders. Siemens Energy emphasized that it continues to pursue the goal of acquiring 100 percent of the share capital and fully integrating of Siemens Gamesa. Therefore, after the general meeting the remaining shareholders will have the opportunity to tender their shares to Siemens Energy at the offer price of EUR 18.05 per share.

While Siemens Energy sees annual cost synergies of up to EUR 300 million within three years after full integration, the main objective is clearly to control and restructure Gamesa to improve its dismal economic performance.

In total the take-over should cost around 4.04bn , and shareholders should expect that additional capital will be necessary. Siemens Energy intends to finance up to EUR 2.5 billion of the purchase price with equity and hybrid capital, the first part of which is a EUR 960 million convertible bond issued in September. Additionally, the Annual General Meeting in February is to resolve the creation of new authorized capital. Investors should keep this in mind to understand the potential dilution of their capital. Siemens Energy has a market cap of around 15bn euro at the moment.

Despite the macroeconomic tailwinds, I do not expect a quick operational trend reversal from Siemens Gamesa. In the 2022 fiscal year (which ended September 30), Siemens Gamesa made a loss of almost one billion euros. Besides the general low profitability that also plagues its competitors, many homegrown problems contributed to this. In addition to supply-chain issues and high materials cost, Gamesa suffered from project delays, cost overruns, and problems in its product development.

Conclusion

Siemens Energy is uniquely positioned to benefit from the energy transition and will experience macroeconomic tailwinds for years, if not decades to come.

At the same time, the company does not have a good track record regarding its profitability and it remains to be seen whether management can execute on their mid-term plans to improve profit margins. The share price has increased by more than 75 percent since October last year - although it is still below the 2020 IPO price of 22 euros.

Therefore, I do not recommend buying at the moment. Investors should wait for clear signs of increasing profitability or a meaningful setback in the share price, whichever comes first.

For further details see:

Siemens Energy Might Be Well Positioned To Profit From Energy Transformation