SMAWF - Siemens Energy: The Right Time For A Contrarian Buy (Rating Upgrade)

2023-08-10 17:36:48 ET

Summary

- Siemens Energy announced a loss of almost 3bn euros in the recent quarter due to a provision for ongoing troubles at its wind turbine subsidiary Siemens Gamesa.

- All other business lines of Siemens Energy are performing exceptionally well and will continue to grow.

- The market is reacting negatively, but this could also be the moment for a contrarian Buy.

(Note: all amounts in the article are in EUR. At the current exchange rate 1 EUR is around 1.1 USD.)

Investment thesis

Siemens Energy ([[SMEGF]], [[SMNEY]]) this week announced the financial results for the third quarter of its fiscal year 2023 (the company has an irregular fiscal year from October to September). As was expected (there had been a profit warning in June) the numbers were bad, but Siemens Energy still managed to disappoint with the guidance for the full year.

Costs for rectifying quality defects in onshore wind turbines as well as significantly higher project costs and expenses for the ramp-up of offshore turbine manufacturing capacity had a negative impact. Siemens Energy lost around 3bn euros in Q3, and for the full fiscal year, the losses should add up to 4.5 billion euros.

Siemens Energy did put a number on the expected losses in the wind turbine subsidiary and made a provision of 1.8bn euros. Such a move was demanded by the Siemens Energy supervisory board and investors. During the earnings call the Siemens Gamesa CEO Jochen Eickholt, who was installed last year to clean up the house, said that this was based on a probabilistic failure model. He could not confirm that the root causes for the quality had been fully identified yet. The company also needs to reduce its growth ambitions until the quality issues are under control. So things are really not looking good.

I have warned about the risk that Siemens Gamesa means for Siemens Energy in previous articles on Seeking Alpha. I started my initial coverage in January, Siemens Energy Might Be Well Positioned To Profit From Energy Transformation , and gave a Hold recommendation. Despite the promising prospects for Siemens Energy across the full spectrum of the energy transformation, I recommended that investors wait and see how the troubles in the renewable energy business turn out before they buy. This was not in line with most analysts, but I thought that Siemens Gamesa would further drag down Siemens Energy. I switched to a Sell recommendation in February, Siemens Energy: No Quick Turnaround For The Renewable Business In Sight, Sell .

After a detailed look at the Q3 numbers and listening to the earnings call, I am starting to feel more positive though. I think this could be the right time for a contrarian Buy – and I used the low share price of around 14 euros to start building a position in Siemens Energy again. I did say in my last article on Siemens Energy that I would start to think about buying below 14 euros, and we might still get there in my view. But the risk/reward ratio starts looking good to me now.

The other three business segments of Siemens Energy – 1) Gas Services, 2) Grid Technologies, and 3) Transformation of Industry – are doing exceptionally well, and it looks like this will be the case for the next years to come. The FCF from those segments should exceed the cost of cleaning up Siemens Gamesa (more on that later). Being an engineer myself, I do not have an issue with a probabilistic failure model. Siemens Energy management emphasized, and I think rightfully so, that the failures were created in the past and now the governance is working as the actions they are taking are not based on customer complaints, but their own proactive service management.

That said, the two key risks I have pointed out in previous articles are still there.

Siemens Energy overpaid for Siemens Gamesa and it has now a lot of goodwill on its books. This could lead to a write-down of several billion euros. The second risk is that the quality problems could go on and even more problems could come up. While the usage of a probabilistic failure model looks reasonable to me, probabilistic still means there is no certainty.

What is in the Q3 numbers?

The attention-grabbing headline numbers are obviously the 3bn loss in the recent quarter and the guidance for a 4.5bn loss for the full fiscal year 2022/2023 (ending in September). Siemens Energy reported a net loss of around 2.93bn (3.42 euros per share) versus a loss of 564mn in Q3 of the previous year (which was also due to Gamesa problems).

This was not unexpected and the German newspaper Handelsblatt had reported rumours with those numbers last week already. Siemens Energy is making a provision of 1.6bn euros for future losses. This is a non-cash provision, as the actual losses will arrive over the next years when the quality issues will be rectified preferably through normal service cycles. So, while earnings should be positive going forward (unless of course, more problems come up), cash flows will be diminished.

Siemens Gamesa's problems overshadow the exceptional performance in the other segments

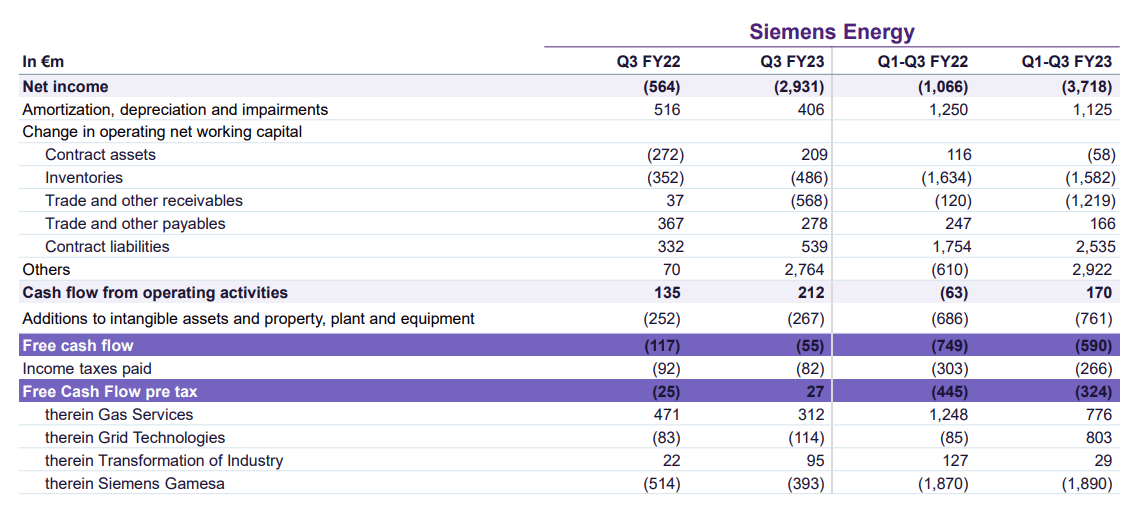

In Q3 free cash flow was barely positive at 27mn euros. The material cash outflow at Siemens Gamesa was offset by a positive FCF from the other segments. Over Q1-Q3 of FY 2023, the three segments have produced a positive FCF of 1,608bn. Siemens Gamesa FCF was a negative -1,890bn. (Note – those numbers are pre-tax.)

{kind=link}

Siemens Energy Cash Flow Statement (Source: Siemens Energy)

If it were not for the problems with the wind turbine segment, business would be booming. In Q3 revenue increased by 8% YoY to 7.8bn euros. The book-to-bill ratio (ratio of orders to revenue) came in at 1.98 and led the order backlog to a new record high of 109.0bn. Excluding Siemens Gamesa, profit increased to 513mn, after a negative -76mn in the previous year.

The balance sheet is robust

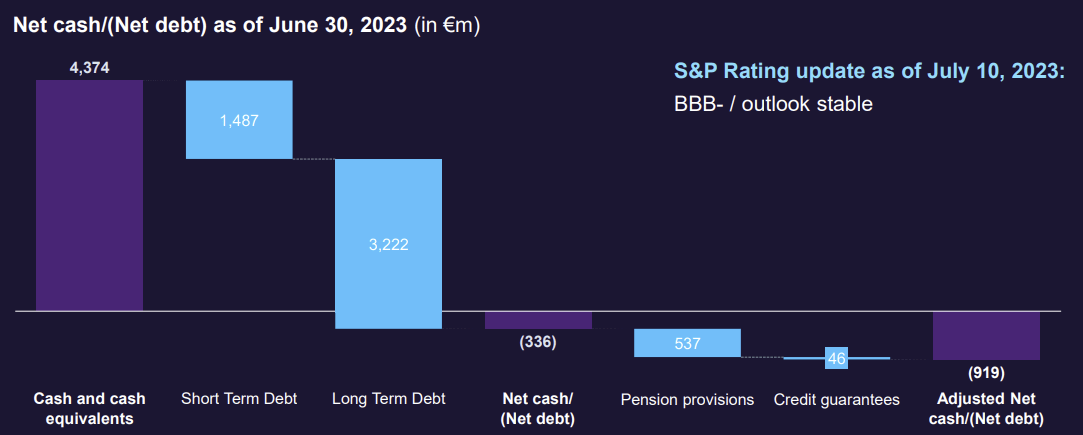

While Siemens ([[SIEGY]], [[SMAWF]]) burdened Siemens Energy with Siemens Gamesa and low-profit margins when it spun off the energy business in 2020, it left Siemens Energy with a very clean and robust balance sheet. This is still the case, although Siemens Energy has increased the debt to 4.7bn (the full take-over of Siemens Gamesa being a main driver). But Siemens Energy has cash and cash equivalents of 4.37bn, so the net debt is at a relatively low 336mn. Including pension provisions, net debt is still only 909mn . The total available liquidity (cash plus undrawn credit facilities) is 9.6bn euros.

{kind=link}

Siemens Energy liquidity position (Source: Siemens Energy)

The low debt, strong liquidity position, and positive cash flows from all segments except Siemens Gamesa make it unlikely that the company will need a capital injection – even if things do not get better soon at Gamesa. The CFO also specifically made that point during the earnings calls.

This makes me think that now – when things look darkest – is a good time to start buying again. Any good news coming from Siemens Energy could make shares increase considerably going forward, while the bad news seems to be priced in.

Risks to the investment thesis

I have already mentioned the two key risks investors need to consider – a possible write-down of the Siemens Gamesa stake and the possibility of further problems from the subsidiary.

Siemens Energy overpaid for the full take-over of Siemens Gamesa

As I have noted in previous articles, in my view, Siemens Energy overpaid to get full control of Gamesa. The Siemens Energy CEO Christian Bruch seems to agree now and said very clearly in a recent interview that Siemens Energy paid too much.

It paid 3.15bn euro to acquire a 25.6 percent stake , valuing the company at over 12bn euros. The current Siemens Energy market capitalization, which now includes 100% of Siemens Gamesa, is lower than that at 11.64bn euros. If you include the net debt of 909mn euros, the Siemens Energy enterprise value now is about the same as what it paid for Siemens Gamesa. So, Siemens Energy has a significant amount of goodwill on its balance sheet and could be forced to do a write-down.

More bad news from Siemens Gamesa could come up

Siemens Gamesa usually signs long-running contracts for installations including maintenance and service that go for 10 years or longer. This is a risk as service and maintenance are calculated in advance for quite a long time. In a worst-case scenario, the bad news could go on for years and further loss provisions could be necessary.

Conclusion

Siemens Energy is in a very good position to benefit from the ongoing energy transition. The order book of over 100bn euros is a testament to the excellent market position the company is enjoying. But Siemens Energy is continuously dragged down by problems in its Siemens Gamesa subsidiary. Everybody seems to finally agree that things are really bad there and the share price is suffering. The contrarian in me thinks that this is the moment to start buying again – in a cautious way considering the risks.

For further details see:

Siemens Energy: The Right Time For A Contrarian Buy (Rating Upgrade)