SEMHF - Siemens Healthineers: Still A Company Worth Looking At

2023-05-29 09:31:04 ET

Summary

- I looked at Siemens Healthineers in my last article back in March, which makes it suitable for an update at this time.

- Siemens Healthineers remains a solid company to look at for long-term investment - even if the company has outperformed and is more expensive now than before.

- I remain at a "BUY" on Healthineers - albeit at a somewhat reduced upside next to where I was a few months back.

Dear readers/followers,

Another good reason for an update to Healthineers ( SEMHF ) at this time is the fact that the company recently, on the 10th of May, reported its 1Q23 results. Dissecting these and updating my thesis on the company at this time, therefore, makes sense. Siemens and Healthineers are solid holdings in my long-term portfolio - but I have mentioned the importance of recognizing overvaluation and doing away with it when necessary, which is what I've been doing over the past valuation increases we've seen for Siemens ( SIEGY ).

Let's see what sort of trends and expectations we can apply to Healthineers, and what to expect from the company at this time.

Healthineers - a good 1Q23 paves way for good trends for the remainder of the year

The company confirmed very good 1Q23 results. With a book-to-bill ratio on the equipment side of >1, with excellent revenue growth of 11% YoY (excluding Antigen, which cragged things down), things are looking mostly positive for this company.

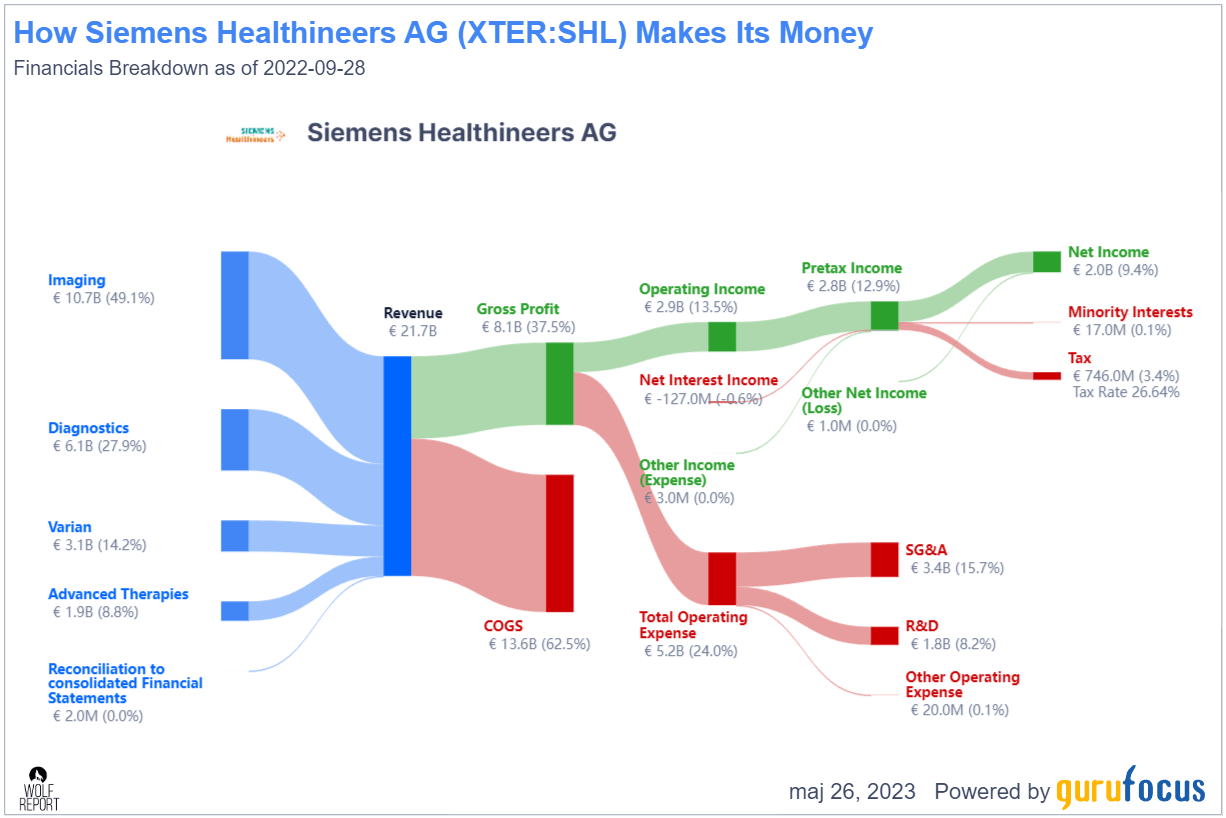

If you recall my last article on the company, where I went ahead and presented the company, Siemens Healthineers is made up of the following revenue flows from the following segments.

Siemens Healthineers revenue/net (GuruFocus)

{kind=link}

If you follow my articles, at this point you likely know some of what I look for in a business I want to invest in. A working business model includes a logical and competitive flow from revenue to net profit with little or no "funny business" in the way. Healthineers certainly delivers this, with net margins of close to double digits.

The company's margins make it a sector outperformer, with 8 consecutive years of profitability increases, and its various margins put the company at the 65th-70th percentile in the sector, which is Medical Devices & Instruments.

Siemens Healthineers also happens to have one of the best debt situations of any company in this segment, with a debt/EBITDA of less than 0.2x, and a debt/equity of 0.04x - truly impressive trends that put the company in the 80-85th percentile in the segment.

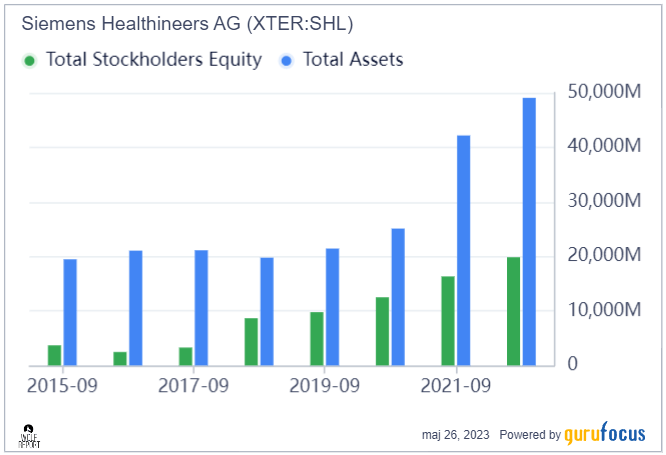

It is a cash-heavy company that while seeing an increasing use of debt has not really compromised on what it does, rather it has expanded the Shareholder equity portion of its assets. Remember, SE represents the total amount of capital linked to the owners (of which you likely are one). If the company ever needs to be liquidated, SE is the amount of money that would be returned to these owners after all other debts are satisfied.

This metric is one I often use to determine the overall financial health of a company. When things turn sour, SE is one of the metrics that tend to grow volatile or worse as one of the first. It alone is not enough, of course - but used in conjunction with other tools, it's valuable. And this is what Healthineers SE looks like.

Siemens Healthineers SE (GuruFocus)

{kind=link}

The company's other segments had excellent performance, with the large Imaging segment showing a 13% YoY growth rate, together with a 130 bp worth of margin expansion.

Diagnostics had it worse - this was down nearly 40%, mostly due to antigen sales, which were close to zero. Profitability here was mostly due to transformation costs and is likely to turn around - at least, that is my forecast.

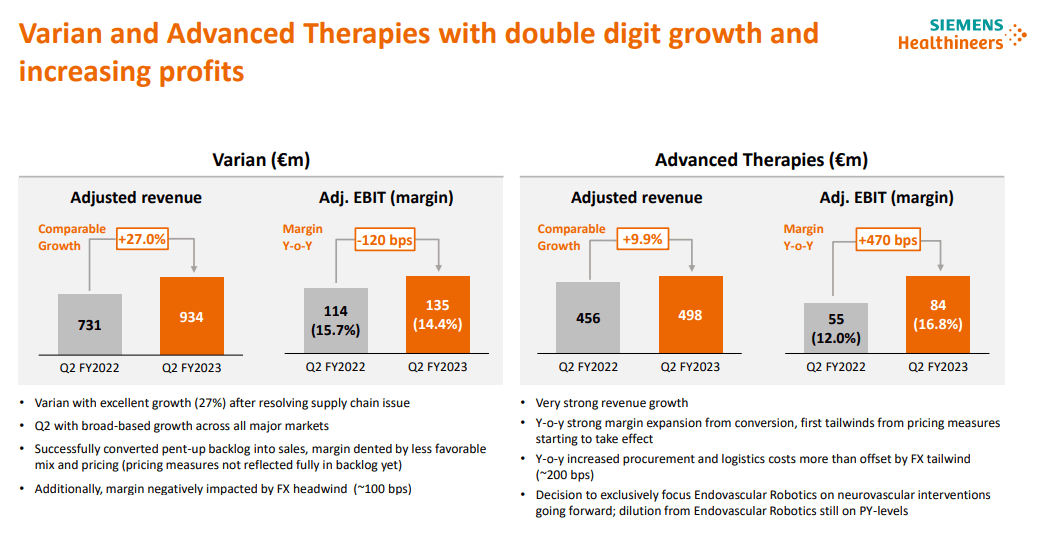

The company's Varian segment is also showing impressive trends, with 27% growth following a resolution of its SCM issues, with margins at nearly 14.5%.

With the exception of Diagnostics, things look positive for the company - but that diagnostic impact brought EPS to €0.43, which is down significantly due to that, and some transformation costs.

However, Healthineers' business model remains very much intact.

Siemens Healthineers IR (Siemens Healthineers IR)

{kind=link}

What we should focus on, as I see it, is the step-by-step improvements in imaging, which has seen broad-based growth from the impact of its pricing measures. This can also be taken as indicative of what happens to companies in the segment once the pricing changes take effect, which, for instance, has not fully happened with Baxter ( BAX ), another company that I invest in.

I also want to point to Varian and AT as segments for improvements in the company.

Healthineers IR (Healthineers IR)

{kind=link}

The company has implemented a successful focus on pricing, which when continued and expanded upon, will result in further margin improvements in H2, and with its book-to-bill improvement of >1, continues to drive growth. This current book-to-bill of around 1.17x is to be compared to 2020 when the number was close to 1x. This results in a favorable skewing of the margin, with positives to be interpreted from the financials in the form of increased productivity, better cost increases to mitigate inflation and developments, and demand balancing out.

This latest set of results has left the company at a 1.37x FCF conversion, based on cash-in of company receivables, something that's likely to continue going forward given the current positive trends.

Healthineers is a company that's active across the world in a myriad of healthcare segments. It's a resilient company with proven fundamentals and an excellent track record. Remember, it piggybacks Siemens' credit rating, which is A+, and its fundamentals remain one of the primary reasons why I would be positive for investing here, even at a somewhat more elevated price point.

You won't be getting a lot of dividends. Following the recent increase in valuation, this dividend is now at 1.8%, though this is not unheard-of-low in this particular segment. Medical devices tend to be a segment with not a whole lot of dividends due to the massive amount of R&D spent involved with keeping a company such as this "in the now".

Other risks/downturns to keep an eye on?

What we want to look at is for Diagnostics to revert to profit and Antigen with it. That was the reason why this quarter wasn't essentially a "blowout". Once this normalizes, we should be able to see some impressive trends for this company, even better than what we're seeing here.

Assets are growing faster than revenues on an annual basis, which is not a good thing as it implies inefficient use of assets that are not generating sales - and gross/operating margins are declining, though we know this is due to the current market environment.

This recent decline in diagnostics will make it difficult for the company to reach its mid-term ambition, that's another thing we want to look at. With this now in the bag, the 8-12% mid-term margin range seems unrealistic to me - though I want to state that the company still considers it quite likely to materialize here based on its transformation program.

Those are the major and significant risks I see to Siemens Healthineers - let's look at the updated valuation.

Siemens Healthineers - The updated valuation implies a slightly lower upside long-term

While I still see the company's targets as intact, including my previously-given €56/share PT, because this included the assumption of a potential downside, I can understand why some might be lowering their Siemens Healthineers targets as of this last article. I, however, am not doing so.

First off, analyst targets. My own PT has always been conservative compared to what other analysts are expecting. Most analysts started out at around €70/share for the native and are now down to around €60/share. I still think that €56/share is fairer, and does include the realistic impact of even a somewhat more sustained set of margin pressures on diagnostics and Antigen.

Out of 16 analysts following the company, 13 are still at a "BUY" or equivalent, and while I may not agree with their particular targets, I do agree with this stance on a general basis.

From a peer perspective, Healthineers is a now decently-attractive potential due to how cheap relative to its usual premium it has become. The current native share price for SHL, its native share of €52.8/share, is a normalized P/E of close to 23x, compared to a usual P/E of 26-28x. So despite it not being as cheap as it was in my last article, I still consider the upside to be enough to warrant your attention - and your investment, should you decide that Siemens Healthineers suits your goals.

Don't expect Healthineers to make you rich quickly. It won't - this is a company that requires patience and growth, especially with a sub-2% dividend, but it's attractive enough to generate a double-digit upside on a 23-24x P/E, which is where I would forecast the company at this time.

We could see further pressure in diagnostics - but I don't consider this likely with the company's transformation program currently in place. Simply put, the more pressure we do see from this, and other negatives in the company, the more I would say the company needs to be considered at a somewhat lower multiple.

If we do see another quarter without improvements in the segment, I may need to slightly adjust my price target to reflect the company not reaching its margin targets.

Remember, this company works in a segment with impressive market leaders that include Abbott (ABT), Medtronic (MDT), and Stryker (SYK) - all of which are businesses I know and invest in. Medtronic in particular is a significant position for me that I bought at an impressive undervaluation. And while Siemens isn't at the same degree of undervaluation here, it's nonetheless an attractive potential at this time.

For that reason, I will continue to consider Siemens Healthineers a "BUY" at this time, albeit not one of my top ones. The company is an attractive potential with A+ and a double-digit upside, but there are companies out there that offer substantially higher and better upsides, should you choose to invest in such a manner.

Here is my thesis on the company.

Thesis

- Healthineers is among a class-leading group of companies in the medtech/equipment sector. While not the most profitable nor the most qualitative, nor the highest yield available, it nonetheless presents an appealing thesis with the potential for a double-digit upside at a parent's credit safety of A+/A1. This is worth noting and worth considering.

- I give the company a rating of "BUY" due to the aforementioned combinations of fundamental stability, strength, peer/comp appeal, and relative upside in an uncertain world. What challenges there are, I believe Healthineers will master.

- My PT is €56/share for the native - and I won't change this PT here as of May 2023.

Remember, I'm all about: 1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I won't call the company "cheap", but it fulfills every single other metric I look for.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Siemens Healthineers: Still A Company Worth Looking At