SEMHF - Siemens Healthineers: The Decline Makes The Upside Better

2023-09-15 07:00:00 ET

Summary

- Healthineers, a healthcare company formerly part of Siemens, offers potential market-beating upside.

- The company's main segments include imaging, diagnostics, advanced therapies, and Varian.

- Despite challenges from cost inflation and macro factors, Healthineers' solid company-wide results make it an appealing investment opportunity.

Dear readers/followers,

Finding quality in the current investment context isn't easy - but more difficult still is finding undervalued quality in some sectors. This is especially true for lower-yielding companies. A few years ago, a yield of 1-2.5% wasn't a big deal - risk-free rates and interest rates were so low that low dividend yields caused a shrug, no more.

That's not the situation today. If you can get almost 5% risk-free, the bar that a company has to clear in order for you to invest at a yield half that has risen significantly - as it should. This has resulted in a devaluation of companies that typically trade at significant premiums. Not for all - Healthineers (SMMNY) still trades at what I would consider a premium, even if that premium is certainly below where this company typically trades.

In this article, I'll be revisiting the upside case for Healthineers, a quality healthcare company that was once (and in some ways) still is part of Siemens.

Siemens Healthineers - The longer-term upside could be market-beating

What was once Siemens Healthcare, Medical Solutions, and Medsystems is now simply called "Healthineers." Spinning these off into one was part of the conglomerate's now 10+ year strategy of retaining only a very core group of power/infrastructure businesses, while spinning most of what previously made Siemens into one of the largest conglomerates on earth,.

My heaviest investment was in the main company, Siemens (SIEGY). I actually sold most of my shares when the company went above €150/share. Siemens also remains the company I keep the closest eye on, and would like to enter at an appealing valuation the most, due to the mix of the businesses we're talking about here.

This does not make Healthineers bad. Healthineers is essentially a large number of medical patents and quality technologies - a wide range of arms and spin-offs. Unlike most of Siemens's other spin-offs, the parent company has actually kept a very tight set of reigns on Healthineers, including a 75% share ownership of the company.

60,000+ people and over €20B in annual revenues make money for the company's shareholders, which is expected to grow significantly following this recent year, expected to be a tough year for Healthineers due to cost inflation and unfavorable macro.

{kind=link}

The company's main treatment vectors are imaging, diagnostics, advanced therapies, and what is known as "Varian". Varian is an American business with a strong focus on radiation oncology and software, including things like linear accelerators - Varian itself was acquired by Healthineers back in 2021, but the company continues to operate independently - so a very solid mix, with a 49%+ split towards imaging.

3Q23 results were posted in early August of this year. Those results continued what I view as positive trends for the company, including broad-based double-digit revenue growth, and a book-to-bill of 1.1x. Antigen continues to weigh things down here - inclusive of that, top-line growth was less than 3.6%.

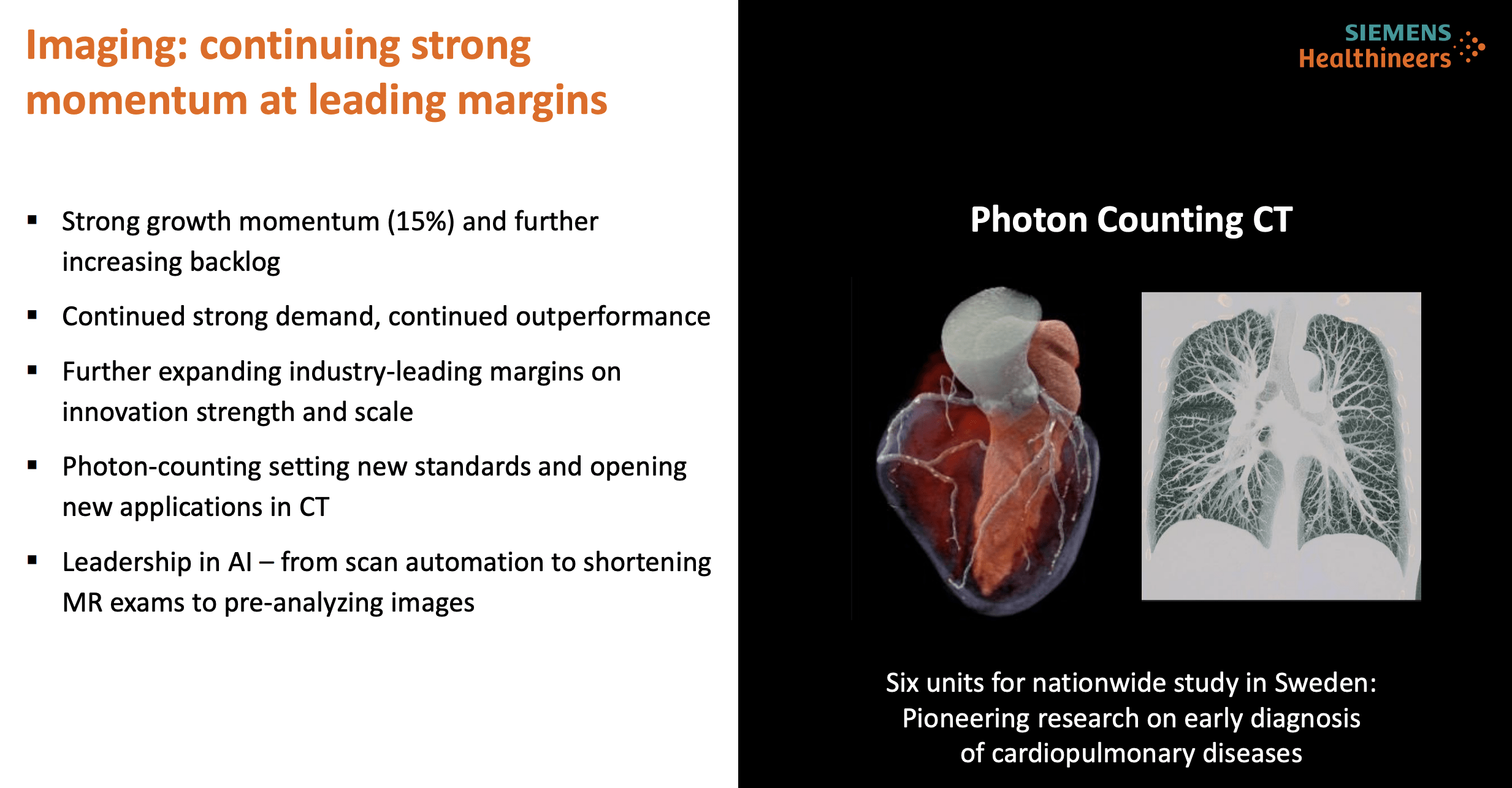

Imaging, the company's main segment, grew by 15% and saw significant margin expansion. This is the single most important takeaway from the quarter, given the segment's relevance to company results.

{kind=link}

The other sectors are more in a holding pattern. The diagnostics sector portfolio revision is completed, and the first savings from the transformation program is kicking in. The company recently released its Aticella CI analyzer, now cleared by the FDA. This is a chemistry analyzer with electrolyte and photometric testing capabilities, capable of testing a whole host of different samples, already receiving good reviews from hospitals and labs around the globe (Source: Healthineers IR).

Varian? The segment generates continued order momentum with the Hypersight technology gaining significant traction and implementation of AI. 3Q was somewhat held back by logistics - not an odd report if you look at the overall larger market today - but between pricing measures kicking in, and continued order momentum, I expect continued positives from Varian.

Advanced therapies, as the last segment here, also showed good growth. Revenue grew by 12%, and margins are stable or expanding, with over 1,000 units of the new Icono system sold since launch. Looking at some of these products, it seems to me that we're getting closer and closer to the sort of sci-fi products for surgeries and therapies that are able to operate more or less independently, which is exciting (even if it's currently mostly optics/scanning).

{kind=link}

Company results were very solid, on a company-wide basis. We saw adjusted basic EPS improvements of 24%. Margins, looking company-wide, are somewhat flattish - most of the negative trends came from Antigen, much as they came during the last quarter. Imaging and Advanced Therapies were the stars, with Varian on a growth trajectory but with margin impacts. None of the challenges are new or unexpected. it's inflation/costs, logistics, some SCM challenges, and overall macro, and related challenges. Book-to-bill is down very slightly, but up over several years, from a 1.06x low in 2020.

The company confirmed its 2023E outlook, which in this case actually means a flat revenue growth and a significant variance in adjusted EPS due to antigen issues for the company. On the low side, adjusted EPS is expected to come in at €2/share, but on the high side, it could go to €2.2/share. This means as much as a 12% EPS drop, or as low as a 3% EPS drop within the company's own forecasts. I would tend to estimate towards the lower end, to stay conservative, and this would mean we should expect a double-digit EPS decline for this year.

To be clear, antigen isn't going to be turning around or anything like that - at least not to levels seen in 2021 or 2022. This has to do with the sheer amount of COVID-19 volumes to this segment, which I don't view as recovering. EPS growth on a forward basis will come from the other four segments, with some overall normalization in the mix. I don't see the sort of EPS growth that most estimates go for here, I would prefer to be more conservative, but even conservatively speaking, there's an upside to be had here.

What I would specifically be on the lookout for are continued logistical issues not only in Varian but in the rest of the segments. Issues of the macro kind have the potential to send results south, which would likely further impact short-term growth, and in turn impact valuation.

The main driver for the future results growth will likely, as I see it and other analysts see it be a recovery/turnaround in Varian. Once we have this, that's what's driving results. So Varian, together with continued flat or slight sales growth in other segments, is what we want to see or keep a close eye on.

Let's see what possible scenarios for returns we can consider likely here.

Upside in Healthineers - Double digits are possible under enough premiumization

The company's peers are some extremely strong companies, including names such as Abbott ( ABT ), Medtronic ( MDT ), Stryker ( SYK ), Boston Scientific ( BSX ), and a few others. All of those mentioned are larger than Healthineers, with the former Siemens company in fifth place in terms of size. I own several of the positions, with my largest stake in Medtronic.

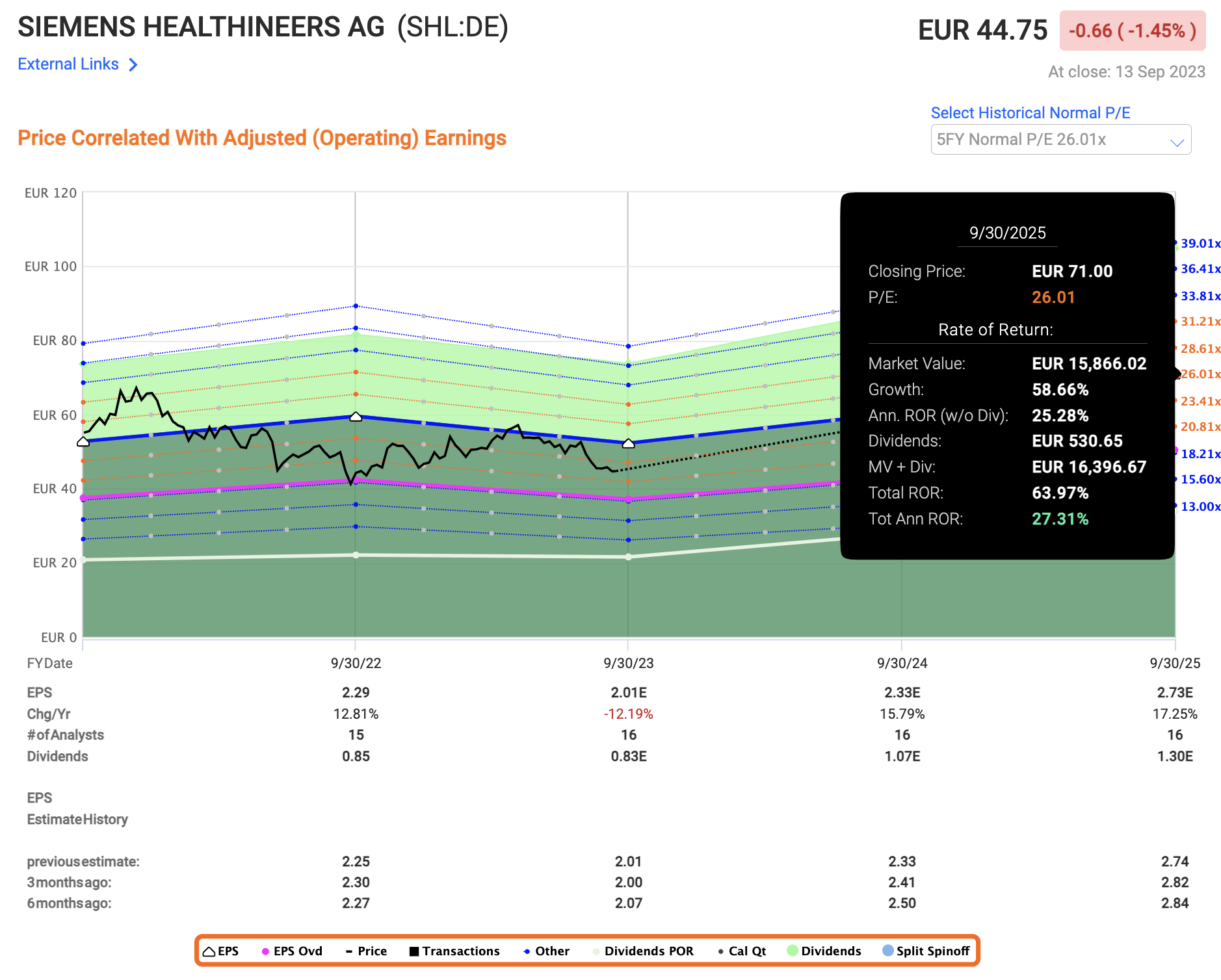

The same appeal which I pointed to in my last article is still relevant here. More importantly, the upside at this point is in fact far higher than it was in that article because the share price is now lower. If we accept a high premium of 26x P/E, the relative upside to normalization inclusive of the company's current forecasts coming at a 75% accuracy on a 1-year basis comes to a 27% annualized RoR, of which 2.12% at this valuation is dividends.

{kind=link}

At €44/share I also consider the company to be significantly undervalued relative to its peers. S&P Global averages for the company are at around €49 to €65/share with an average PT of €57.5, denoting a 28.3% upside to a fair value here.

Even if you were to forecast the company at a significantly lower multiple, let's say at or around 20x P/E, your RoR would still be close to 15% annually, which is, as I consider it, is still more than enough to keep me interested in investing in this business.

Now, this company isn't as cheap as some of its peers. But Healthineers offers as I see it, almost unparalleled levels of fundamental safety. in investing. Challenges may come to this company, but operating cash flow trends are extremely strong here. It lacks, as I see it, risk factors that could see similar trends to the ones seen in Baxter ( BAX ). There are cheaper alternatives, but Healthineers offers something that for many of you might be worth the money.

I gave the company an introductory PT of €56, and this is not a price target I intend to shift even a little as of this update. My previous characterization of this company as a business with significant upside is now added to by the fact that I'm also calling the company "cheap" here.

You know what happens when a company gets cheap. My investment in Baxter is actually a good example of this - up significantly in a short time, then down again. For Healthineers I expect more stable trends - and my official expectation and forecast is around 15% annualized return conservatively - which justifies my "BUY" rating here.

Thesis

- Healthineers is among a class-leading group of companies in the medtech/equipment sector. While not the most profitable nor the most qualitative, nor the highest yield available, it nonetheless presents an appealing thesis with the potential for a double-digit upside at a parent's credit safety of A+/A1. This is worth noting and worth considering.

- I give the company a rating of "BUY" due to the aforementioned combinations of fundamental stability, strength, peer/comp appeal, and relative upside in an uncertain world. What challenges there are, I believe Healthineers will master.

- Healthineers is now a company that I am able to consider "cheap" as it has dropped significantly from my latest set of results and overall estimates.

- My PT is €56/share for the native.

Remember, I'm all about : 1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is now "cheap" to me, as we're down almost double digits from my last article, turning this into a "BUY" fulfilling all of my criteria.

For further details see:

Siemens Healthineers: The Decline Makes The Upside Better