SMAWF - Siemens: I Am Buying The Dip

2023-08-29 17:20:29 ET

Summary

- Siemens' stock has recently lost almost 20% in value, presenting a buying opportunity.

- The company's Q3 figures were solid, with order bookings and sales showing growth.

- Despite concerns about the Chinese market, Siemens is still growing strongly and has a positive outlook for the future.

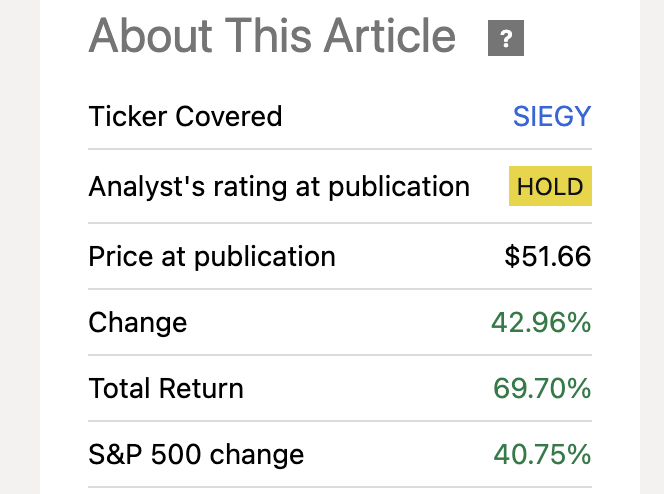

It has been more than three years since I wrote about Siemens AG stock ( SIEGY ; SMAWF ) here on Seeking Alpha. My conclusion was mixed in March 2020 given the global uncertainties, but I recommended investments in the stock via several smaller tranches. I myself have also had the stock in my broadly diversified retirement portfolio for many years. The stock has been a very solid performer in recent years and has clearly outperformed the S&P 500 since my last update.

Performance Siemens vs. S&P 500 after my last update (Seeking Alpha)

{kind=link}

Recently, however, the stock has lost almost 20 percent in value which is a great opportunity to take another look at the company.

3Q figures were solid

The figures for Q3 2023 published on August 10 were very solid. Order bookings (orders), for example, rose by 15 percent. Sales grew by 10 percent to almost €19 billion. FCF even increased by 30 percent to €3 billion. In the prior-year quarter, by contrast, FCF was still €2.3 billion.

The strong growth of Siemens' Smart Infrastructure and Digital Industries business units is worthy of particular mention. Revenue in the Digital Industries segment increased by 11 percent to €5.3 billion. The software business saw an earnings increase of 24 percent to €1.1 billion, corresponding to a margin of 21.1 percent. Sales at Smart Infrastructure grew by 15 percent to €4.9 billion. Earnings rose by almost 40 percent to €770 million, corresponding to margin growth of almost 3 percentage points.

Reasons for the weak share price performance?

Although the quarterly figures were solid, overall, investors did not get back on the buying side. There were several reasons for this.

For one, Siemens has felt a drop in demand in China. This primarily affects the Digital Industries segment. For example, orders in the segment fell by 35 percent to €4.1 billion. This also caused Siemens to reduce its profit forecast. The company expects revenue to reach only between 13 percent and 15 percent instead of between 17 percent and 20 percent. Management has also lowered the profit margin by half a percentage point.

After raising guidance twice this year, this outlook seems like a bit of a party crasher. In fact, we are starting to see the economic weakness in China having an impact around the world. At €16.7 billion, Siemens generated nearly 25 percent of its revenue in Asia (including Australia) last fiscal year. Of this, a significant portion falls on China, so the German industry giant has a strong exposure to China and to the Chinese economic development. Siemens management also seemed to have been somewhat surprised by the sharp decline in its China business:

China's market recovery in manufacturing is materializing slower than expected and we anticipate some further subdued development. Besides the macro situation, this is also depending on the timing and implementation of governmental stimulus activities and the private consumption to pick up.

The price weakness is a buying opportunity

Although the latest quarterly figures were solid, they were less good than hoped for and even disappointing with regard to China.

In my view, such small dips are always good opportunities to add to existing positions in companies. In the case of Siemens, we must not forget that the company is still growing very strongly. If you read the forecast, you don't get the feeling that you are dealing with a stumbling industrial giant. Yet the market focus is very much on China. The drop in orders in China of more than 60 percent in the Digital Industries segment is indeed frightening. However, little consideration is given to the fact that Siemens still grew by 10 percent in terms of sales in China. Besides that, order intake increased by 56 percent in Q3 2021 and by more than 30 percent in Q3 2022. It is clear that there cannot be such growth figures every year.

Also, not taken into account is Siemens' strong growth in its U.S. Smart Infrastructures business. Sales there, for example, rose by 22 percent. New orders also rose by 10 percent. This makes the U.S. business one of Siemens' fastest-growing businesses.

Overall, management expects full-year revenue growth of between 9 percent and 11 percent, with double-digit percentage growth in all three segments (Digital Industries: 10 to 15 percent; Smart Infrastructures: 14 to 16 percent; Mobility: 10 to 12 percent). Siemens is also targeting higher EPS of €9.60 to €9.90. This forecast excludes the Siemens Energy stake, which already contributed €1.14 to EPS in the first three quarters. On average, analysts expect Siemens to increase adjusted EPS to more than €11.70 by 2025. Based on the current share price in €, this results in an adjusted P/E ratio of less than 12 for 2025, compared with a historical adjusted P/E ratio of 18 for the last ten years.

In addition, February 2024 will again be the dividend season at Siemens. Analysts expect the company to raise its dividend by more than 13 percent to over €4.82 per share. The expected dividend yield on the current share price is thus 3.58 percent. This is above the average of the last 5 years of 3.29 percent. Siemens is thus clearly undervalued in terms of earnings and dividends. With a payout ratio of 38 percent on earnings and 44 percent on FCF, as well as the expected growth in earnings, an increase in annual payouts in the low double-digit percentage range is not really at risk in my view.

Lastly, the Mobility segment should also be highlighted. Here, Siemens posted a quarterly record. In particular, major orders in Egypt and Germany resulted in new orders of €8.3 billion. Sales revenue even grew by 12 percent.

But I also note the risks. For example, the economic weakness in China may deepen further. It is already stronger than management expects. In addition, economic growth could slow down globally. Order intake is already declining in other regions. In Germany, for example, order intake in the Digital Industries segment fell by 38 percent (although sales still rose by 19 percent). In Italy, order intake in the Digital Industries segment fell by 53 percent (although here, too, there was strong sales growth of 27 percent).

Conclusion

The recent share price losses are due in part to disappointing quarterly figures. Here, investors have focused primarily on business in China and the slowing growth momentum there. In my view, these are rather short-term developments. Yes, Siemens has strong exposure to China, and I am one of the voices that are rather skeptical about the future growth potential of China. However, the world is big and Siemens is a global player that is very well positioned in the growth markets for digital transformation, energy transition and infrastructure.

I will take advantage of the current share price weakness and expand my Siemens holdings.

For further details see:

Siemens: I Am Buying The Dip