SMAWF - Siemens - I'm Moving To Call Options With This Giant

Summary

- I've been writing about Siemens and my investment in the company for some time - my last article wasn't even that long ago, but the company has still outperformed.

- Siemens is up almost 10% in less than 2 weeks. This causes me to change my overarching thesis for my significant holding in certain ways.

- I'm not selling or trimming - instead, I'm making use of options to boost my income and make sure I'm getting what i want out of the company.

Dear readers/followers,

Siemens ( OTCPK:SMAWF ) is not a complicated company for me. I've been investing in it when it's been cheap for as long as I've been on the stock market overall. The reason for my overall positivity on Siemens is just how good the company is - and how good it has always been and managed to evade and prevent declines such as the ones we've seen in many of the company's international industrial conglomerate peers.

Combine fundamental qualities with a good dividend, superb management, and a set of portfolio assets that are positioned extremely well in relation to the next 20-50 years of international challenges, and you have a company for the ages - or at least for as long as you may be around, if you're reading this and investing.

However, the following still applies.

Updating on Siemens

As I said - the company has outperformed even to the relatively recent of my articles, climbing nearly 10% to the overall broader 5% of the market. That means that the company is now trading above €140/share, which marks the company going below or close to 3% overall yield, and a 30x+ P/E.

This, dear readers is a problem.

Because I'm a valuation-oriented investor and have grow increasingly active in my portfolio management over the past couple of years, I can't in good conscience ignore when a company reaches above where I believe it should be.

It's not as though the company has performed badly. 4Q22 was absolutely amazing, given the environment that the company delivered those results in. Siemens delivered on its annual guidance, and operational performance was superb, with double-digit growth in terms of orders, and close to double-digit revenue growth, breaching the €70B mark. But this isn't the reason we've seen such outperformance on par with the company - these results have been out for several months.

Siemens IR (Siemens IR)

The company's operational segments at this time are DI, SI and MO - and all of these delivered revenue growth and margins according to expectations, with DI at the highest margin close to 20% and MO at around 8.2%, within its target range.

And this does give Siemens a superb position for starting the fiscal of 2023. The reason for this is that the expectation was for inflation to normalize sometime in 2023, as well as recessionary trends - but it was still uncertain when exactly this would occur. And it's still uncertain.

However, with inflationary trends reversing across most of NA and EU, companies with cyclical tendencies are instead showing positive trends. Even with boosted dividends, great FCF, and good overall metrics, I want to raise a hand of warning here.

Remember, the market has a tendency to overreact. The valuation trends we're seeing are not backed up by much more substantial data then when the company traded closer to €110. Very few of my readers seemed interested in the company here - yet it's now when the company is over €30 more expensive, that I'm getting messages about whether people should buy the company - that wasn't something I got about 3 months back.

That is why I manage a list of companies, with valuation and trim targets, that has over 100 names in it - from across multiple geographies and markets and multiple sizes. What they have in common is that they share my fundamental demands for investing - good management, good fundamentals, and a dividend.

Valuation is the most determining factor. And that is what Is now out of "whack", so to speak.

While Siemens has traded more expensively than we see here, it has not done so often. The most we've seen in the past 5 years, is €151/share. As you'll see in the valuation section, that begs a few questions.

First off - Siemens has a good order backlog, and I expect the company to continue to do well in the future as well. Its strategy is solid. The concept of "streamlining" a conglomerate is one that Siemens over the past decade, has perfected.

This is why I'm looking for industrials like this, and also why I own stock in Schneider ( OTCPK:SBGSY ) as well as ABB ( ABB ). They're very good examples of a "European" model being by far the more effective, turning to tech focus and asset-lighter structures for more flexibility and slowly proving their profitability here.

There are plenty of examples where the company's approach is yielding incredible dividends. That's the thing about Siemens. It's a company that works not in one continent or even two - it develops infrastructure and high-level solutions for the entire world. This is a slow business. That's why any time there are massive, or violent movements, i pay attention - not only to Siemens but to other companies in a similar situation.

When that movement goes in the wrong direction too far in any direction, this really "begs" for your attention, and for you to act.

Let me show this to you in this updated valuation section.

Siemens - An updated valuation for the overvaluation

30x P/E is too much for Siemens, and that's more or less where we currently are for the native share as its hit over €142 today, on Friday on the 13th of January.

As I've said, my previous pounding the table for Siemens, never really seems to get the result I'm hoping for.

I can only hope that my pointing out this company's upsides and qualities will turn investors onto it so that next time Siemens does take a dive, more people take the opportunity and load up on quality.

Siemens's valuation remains complex in the sense that all of its various portfolio companies and assets need to be properly accounted for in every single model, and my updates in these models are typically a process of a few hours every time the numbers come out.

But at the same time that it's a complex venture, it's also relatively simple because it has traded within a relatively limited price range for the past 15 or so years. Whenever the company goes below 15-18x, that's when you start paying some real attention to "BUY"ing Siemens. The respective price for that today is below €100/share and below around €90/share. When it goes above 25x, that's when you stop buying - and when it goes above 30x, that's when things are moving really out of what I would consider the normal range here.

I have not trimmed Siemens once in the past years - not even when it hit €150/share last time.

Valuation for the company is dictated, as I see it, by DCF, NAV, and some from peers as well as historical trends. I went to 3% in my DCF model in terms of EBITDA growth during my last article, and despite these positives, I'm not raising that.

It's important not to underestimate the company's potential due to the correlation to infrastructure spending, but it's equally important to not believe the company is immune to downturns - because it isn't. And that is what the market seems to be currently ignoring.

This isn't a bad thing - neither over nor undervaluation is a "bad" thing, as long as you know how to handle it and have a plan for it. Less than 2 weeks ago, I specified that there's still some upside, but at €130+ native, that's when we need to start being careful with this company and its valuation. At €140, I consider any sort of realistic upside to be gone, and it is high time to do something about Siemens.

Analyst PTs for Siemens are elevated here - a 21-analyst range of €94 on the low side to €190 on the high side, a fairly extreme range. However, 17 out of these analysts have a "Buy" or similar rating at this time. The average PT for Siemens is €152/share here, implying an analyst upside of around/slightly above 5%. My own PT was €135 - and that's going very high for Siemens. This isn't a company that I've just started covering either, where my models are perhaps somewhat new or not yet "proven" or in practice. When it comes to Siemens, I do stringent and meticulous calculations, combining NAV, DCF, historicals, forecasts, and analyst targets based on real company cash flows and potentials that in turn are based on year-old historicals and models which have enabled me to invest in Siemens profitably. I don't shift them lightly because the "mood changes".

So, when the company went above €140, I started looking at options, I changed my thesis, and this is my current thesis on Siemens.

Thesis

My thesis for Siemens is as follows:

- Siemens is a beyond-solid company. It's so far beyond solid that it's one of the 20 companies in my "Buy-and-hold-forever" list, along with businesses like BlackRock ( BLK ), Airbus ( OTCPK:EADSY ), and LVMH ( OTCPK:LVMUY ) - even though all of these companies, even Siemens, also do have trim targets - as I'm evidencing here.

- If you did not buy Siemens when it was below a normalized 10x P/E a few months back, you really missed the boat on this business, and missed out on 30% RoR in a short time.

- At the right price, this company becomes a "BUY" strong enough to make me ignore or put second most other investments. I've been pushing capital to work for months now, and my stake is now 3.5%.

- My PT for Siemens is €135 - and it's a "Hold" here. I would not touch Siemens here.

The way to play Siemens here - Covered calls

I don't mind selling even good companies when they become too expensive. I know that, the market being exactly what it is, every company will become relatively cheap again sooner or later - and there are always good companies to "BUY" and to invest in, provided that one follows a valuation approach.

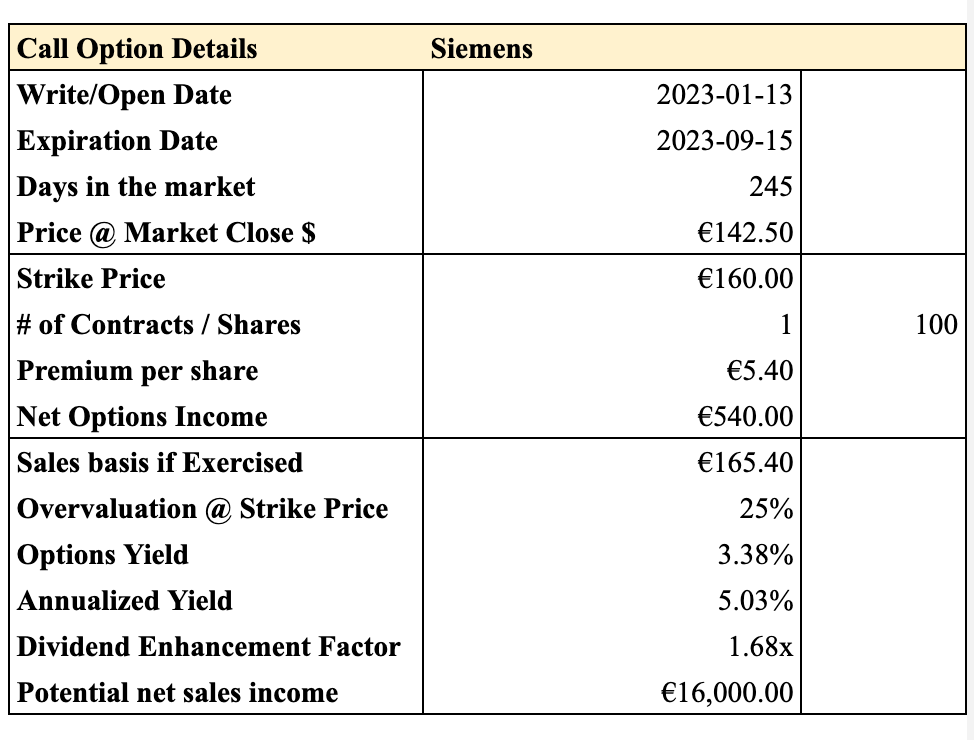

For that reason, I don't hesitate to plan or strategize at what levels I would write calls or puts on companies that I like. Here is the current covered call i found on Siemens.

{kind=link}

This is a good example of what I would be looking for. I want a strike that's well outside the range the company has traded at historically, I want a over 1.5x dividend enhancement factor, and I want a price I would not mind selling the company at. I also want an annualized yield that's at least 5% for a good covered call on a holding I consider "core".

We get all of that here. While I don't put my entire position on the line at one time, I go by thirds. So 1/3rd would be sold as covered calls here, and if we go up more, I would sell another third at around €145 or above, if the company climbs that high.

The most important thing is, I really don't mind selling Siemens at a €165/share including premiums - and if you are a conservative valuation investor, neither should you.

This is a view I did not hold at €130 - but I do hold it here at €140/share or above.

For further details see:

Siemens - I'm Moving To Call Options With This Giant