SMAWF - Siemens: My 'Hold' Was The Right Choice Going Into 2024

2024-01-09 05:00:27 ET

Summary

- Siemens underperformed both my portfolio and the S&P 500.

- The company has strong profitability and quality metrics, but its valuation is currently high.

- Siemens is well-positioned in the automation, electrification, digitization, and ESG sectors, but faces risks from cyclicality and valuation.

Dear readers/followers,

My last coverage on Siemens ( OTCPK:SIEGY ) was all the way back in March of 2023. You can find that last update article here, if you're interested. despite appearances, my rating at the time (as the title suggests), was in fact a "HOLD" for the company. While the company has gone up, and I probably should have provided an update article during September or October, when the company briefly touched on a "BUY" valuation, the company has in fact underperformed both my portfolio and the S&P 500.

Seeking Alpha Siemens RoR (Seeking Alpha Siemens RoR)

So, overall, I'm very pleased with my strategy for Siemens. I've been reviewing and investing in Siemens Aktiengesellschaft for years. My current position is minor because the company is currently at a full valuation. As before, the company's current valuation doesn't exactly call for a superb upside for the long or the short term. I've been playing the company with options during this year in addition to my small, long position.

In this article, I'll look at what to expect for 2024, and where your considerations should, at this time, be.

Siemens and Its 2024E upside and potential based on recent results

Siemens shouldn't be a strange or new company to you. It's one of the most relevant Industrial conglomerates on earth, and even following a multitude of spin-offs that have left the company with a "hard core" of segments and assets, I often prefer to invest in Siemens itself rather than its many other businesses.

Why?

Because this company typically beats others in terms of profitability and quality. We have over 38% gross margins, over 11.5% EBIT and double-digit net margins for an industrial company, which is above every in every single metric that matters. It's RoE and other return metrics are equally stellar. The last few years have left the company somewhat higher leveraged than previously, with now at a 2.8x net debt/EBITDA and an interest coverage of less than 7x, which is sub-par to the sector, but most of the other KPI's are still very much in line.

The company has a decent amount of insider activity, it's seeing a solid amount of operating margin expansion, and is a very financially healthy business from a Beneish M-score perspective, implying a low likelihood of financial manipulation (Source: GuruFocus).

Quality has never been the problem for Siemens. It plays in a sector that also includes Schneider Electric, and my approach has always been to invest in the best-priced and best-upside alternative among these players.

Siemens is a capital goods manufacturer, one of the key players in working alongside the goal of reducing global warming and the other ESG targets. We work with multi-decade investments , and players like Alstom ( OTCPK:ALSMY ), ABB (ABB) and others are also worthy alternatives here. With over 100 countries pledging to work more and more with renewable capacities in the next few decades, Siemens and similar manufacturers has its work cut out for it.

Headwinds to this development do exist. The pricing for renewable projects has gone up significantly due to profitability problems. Wind turbines, as an example, are up 40% on average in selling prices in less than 4 years due to significant cost inflation, and this has led to canceling of key onshore and offshore projects.

However, I don't believe companies like Siemens or ancillary renewable players to enjoy any profit increases due to these price increases - competition is too high, and the high-intensity cycles for innovation and R&D are likely to prevent any period of significant pricing power from one singular player in the field.

The upside here is Siemens spinning off most of its cyclicality and keeping only the more "solid" businesses, enabling us to forecast with higher certainty where this company is likely to go.

We have 4Q23 - and the year was a strong finish, which is part of the reason we're seeing such a solid valuation at this time.

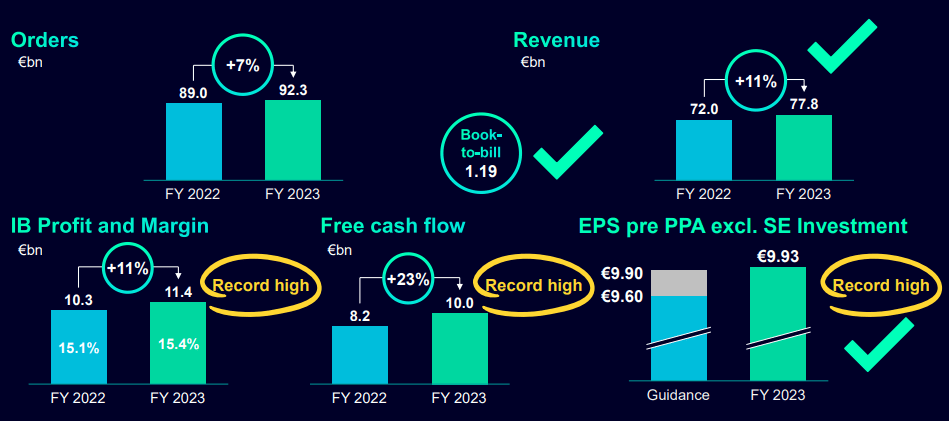

The secular demand trends of automation, electrification, digitization and ESG are not going anywhere. This lead to record performance for the company in 2023, with successful strategy execution, and expecting 2024E, to bring these results even higher.

Take a look at some of the impressive metrics reported here.

{kind=link}

Siemens IR (Siemens IR)

Every relevant KPI was at record-high levels. The DI segment and the SI segment saw record-high profit margins , and even mobility, despite the overall sector of automotive, saw margins within its target range of 8-10%. orders were up in every single segment , with a book to bill on a group basis of 1.02x.

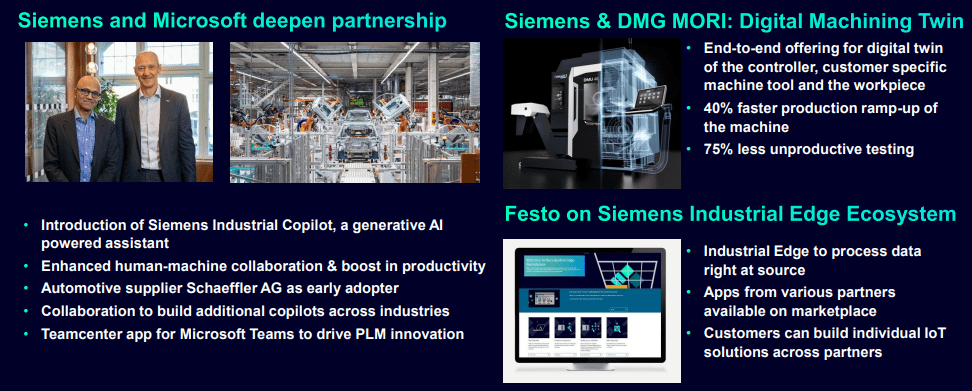

All of this saw a record high €3.4B quarterly profit, with an all time high margin and over €4B in quarterly free cash flow. The company is moving deeper into things like AI and its own digital ecosystem.

{kind=link}

Siemens IR (Siemens IR)

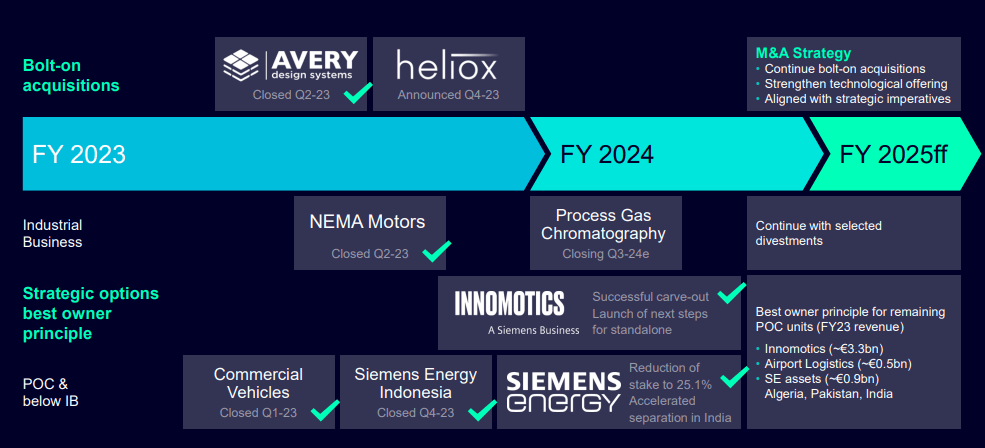

Siemens is building new manufacturing in the US in Smart infrastructure and is continually optimizing its manufacturing footprint- as well as its other assets. The company's portfolio optimization is ongoing. Siemens has reduced its Siemens Energy ( OTCPK:SMEGF ) stake to less than 26%, seeing the near-term writing on the wall in that company's turnaround, and divested the Indonesian Siemens Energy in 4Q23. But it's also adding more assets to its portfolio, to be able to strengthen its tech offerings.

{kind=link}

Siemens IR (Siemens IR)

There's the obvious risk here of the company moving far too heavily into divestments of businesses that could have significant profit potential in the longer term - so a positive thesis or assumption for Siemens requires you to have significant confident in management and its strategy here. For the time being, this is something I have - that's why I still hold a common share investment in Siemens.

And the company isn't divesting everything either. It continues to have a very high 75% stake in Siemens Healthineers ( OTCPK:SEMHF ), a business that I am also invested in.

All of the businesses that Siemens invest, and continues to own, benefit from the continued upside in these growth segments and "new tech" areas. But there will become a point when, despite the upside and safe growth and superb fundamentals, this company may be valued too highly. The company's yield at this time is less than 3%, and despite its A+ credit rating, the question is if the company can actually manage its estimated 5-9% growth rate for the next few years.

Let's look at Risks and positives.

Risks & Upside to Siemens

Aside from the obvious, meaning valuation, the primary concerns to Siemens would be the potential cyclicality of the underlying business that still make up the company's revenue mix. DI is especially guilty of this, because it's exposed to very short-cycle markets on the customer end side, which regionally may fall, and which again and again have led to book-to-bill falling below 1x. This is not a strange concern, with the current book-to-bill only at 1.02x.

It's legacy positions in businesses also impacts the company's quarterly and annual P&L's, because it results in below-the-line cost variables and items that need to be calculated into the valuation.

Beyond that, the upside for this company in the long-term is strong. Every segment that Siemens has in its core business benefits from the way things are going, and the company has established itself over decades as a market leader with a proven history of double-digit margin.

In this sector, that's close to "grace", above-quality implications making for a very attractive potential. The company's backlogs are currently also at very good levels, and the longer-term segments such as Mobility and Healthineers, which work across multiple years , sometimes a decade or more, weighs up the short-term cyclicality.

Valuation for Siemens

However, it all comes down to pricing, as usual.

And the simple fact is, that Siemens is close to priced for perfection here, and it's not a price I can get behind.

Yes, I own a small stake of shares. But truth be told, I am considering divesting even these at this price.

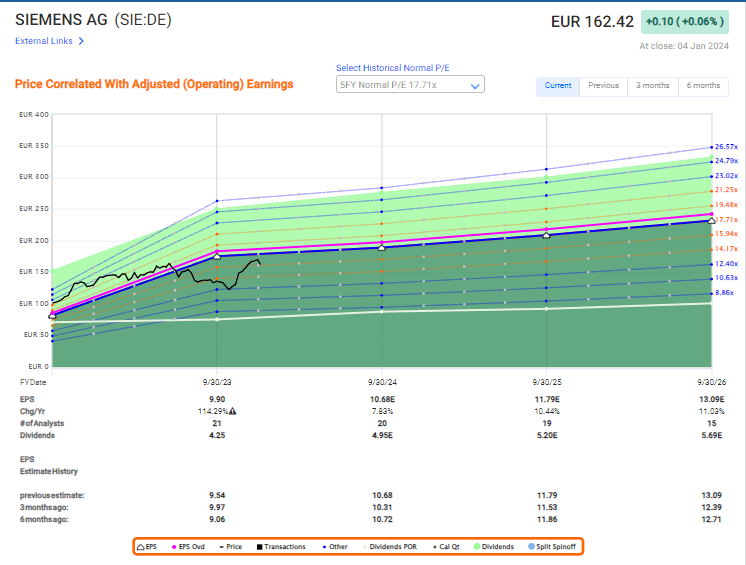

Siemens currently trades at a 16x P/E with a €162/share price with a projected earnings growth rate of just south of double digits until 2026E. Usually, I would have zero issues with a growth estimate such as the one you see here.

{kind=link}

Siemens Upside (F.A.S.T graphs)

However, there are trends here that give me an issue. Specifically, Siemens missing estimates negatively more than 65% of the time on a 10-year basis even with a 10% MoE. In layman's terms, Siemens is not good at hitting its forecast targets - or analysts are not good at forecasting the company, take your pick.

Because I pay heed to historical trends, this influences the valuation that I am willing to give Siemens, and despite the historical 17x, I would normalize it closer to 15x. That puts the upside below 12% per year, which is below where I would be interested in investing in terms of conservative RoR annualized.

It would also be wrong to say that I am the only one being somewhat conservative here. S&P Global analysts give the company a range of a low of €124 and a high €230/share. You can see in the estimate above what sort of outperformance that high range implies, including the FV estimate of €180/share from S&P Global (Source:TIKR.com).

However, they've increased their average targets for the company from an average of below €150/share to that €180 in less than a year. I don't view this as relevant, based on what the company's fundamentals and potential are, and I view this as an overreaction.

My previous PT was €135. I'm raising that to €140/share here, but not above that at this time. Morningstar gives the company a €166/share (Source: Morningstar). This gives you, in my estimate, a good picture of the expectation ranges and what could be possible for the company if it underperforms, or outperforms.

Because I'd rather expect a company to underperform than outperform, especially if statistics and historicals imply this.

For that reason, I'm saying that Siemens is a "HOLD" here, and I'm considering rotating my position here.

My thesis for Siemens in 2024 is as follows.

Thesis

- Siemens is a beyond-solid company. It's so far beyond solid that it's one of the 20 companies in my "Buy-and-hold-forever" list, along with businesses like BlackRock ( BLK ), Airbus ( OTCPK:EADSY ), and LVMH ( OTCPK:LVMUY ) - even though all of these companies, even Siemens, also do have trim targets - as I'm evidencing here, and given that I only retain a 0.3% portfolio position at this time and may rotate it.

- If you did not buy Siemens when it was below a normalized 10x P/E a few months back, you really missed the boat on this business and missed out on 30% RoR in a short time.

- At the right price, Siemens Aktiengesellschaft becomes a "BUY" strong enough to make me ignore or put second most other investments. I've been pushing capital to work for months now, and my stake is now 3.5%.

- My PT (price target) for Siemens is €140 - and it's a "Hold" here. I would not touch Siemens here and I am not changing my price target more than that.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Siemens Aktiengesellschaft stock isn't cheap enough to buy here - I say "HOLD."

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Siemens: My 'Hold' Was The Right Choice Going Into 2024