SMAWF - Siemens: Options Were Successful Siemens Is Still Expensive A 'HOLD'

2023-03-29 17:33:20 ET

Summary

- I've been reviewing and investing in Siemens Aktiengesellschaft for years. My current position is minor because the company is currently at a full valuation.

- Siemens is a great business, but at this price, I wouldn't be overly excited at investing here. The company has held up very well in this chaos.

- The Siemens upside may be there at below €135 for the native, but this is my 2023 update for a €141 price together with potentials for the next few years.

Dear readers/followers,

Siemens Aktiengesellschaft ( SIEGY ) has been one of my primary German investments for a few years. I've been investing at times when the company goes below €100/share, holding my shares at good valuations and yields until we see overvaluations. I know Siemens well , so I know my price targets well. Without wishing to toot my own horn, I believe myself apt at pricing Siemens in a "normal" sort of market.

Seeking Alpha Siemens (Seeking Alpha)

Siemens is a quality business that's going nowhere. For more basic information, I refer you to my last few articles where I go through the history and basics of the business.

In this article, I'm establishing my thesis for 2023, for the remaining 3 quarters of the year, and what you might expect. Remember, Siemens has already paid its annual dividend - so what you're looking at is where the company goes without dividends for the next 10 months or so.

Let's look at what we have going for us.

Updating on Siemens

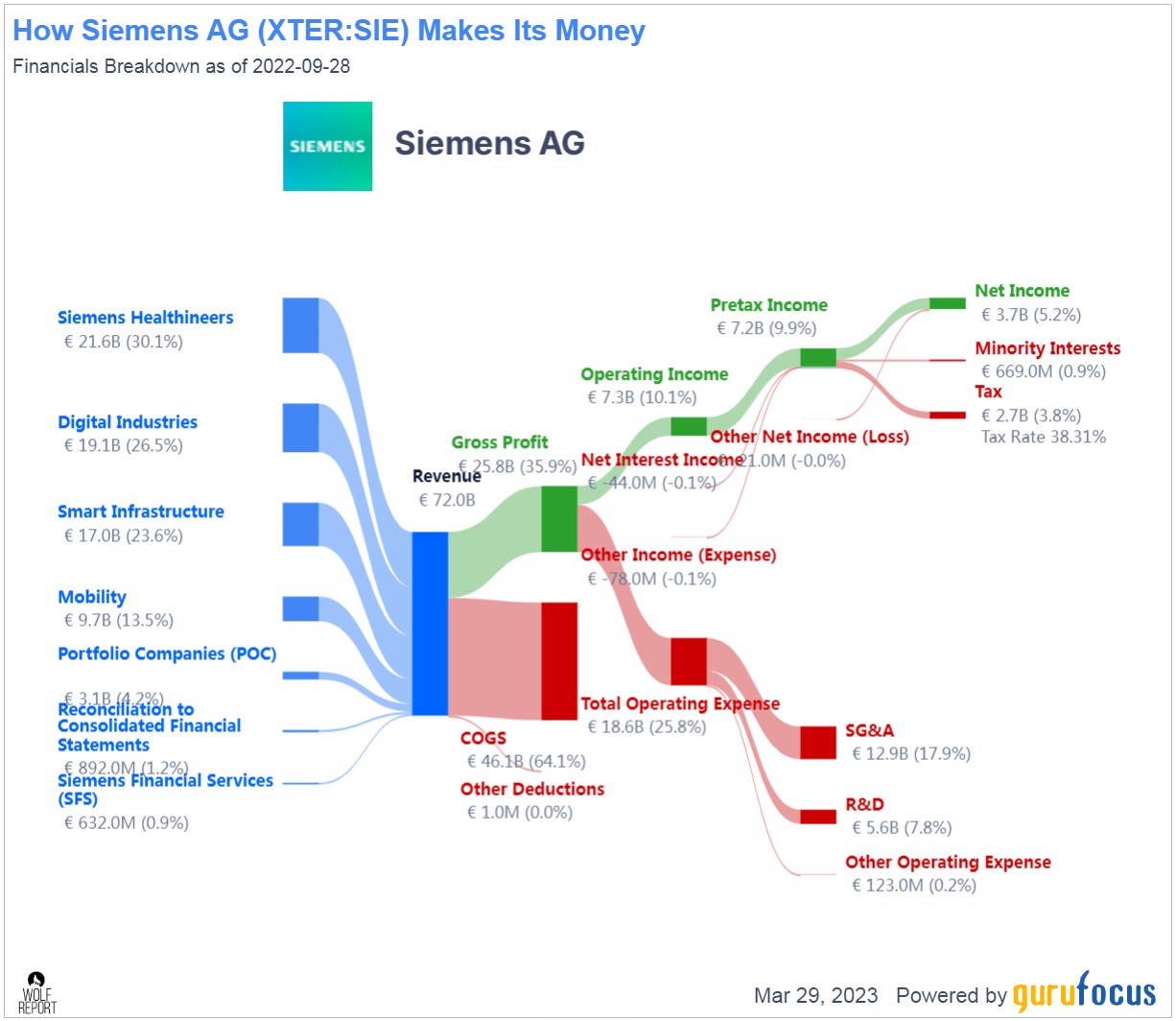

Siemens is one of the more significant industrial conglomerates on the planet, even after divesting, spinning off, and JV'ing most of its previous segments. We can get a high-level view of where the company generates its money, including JVs, by looking at a graph such as this.

{kind=link}

A company the size of Siemens, as you can see, will be averaging net income in this sector of around 5%, sometimes up to 7-8%. One of the primary reasons for investing in this company is its size and safety. If you can get the company at a cheap valuation, you're also able to make money on reversal, while earning a 2.5-4% yield. The combined upside can easily be double-digits if you buy at the right price.

From a geographical mix, Siemens has weighted more China into things, up to about 13.3%. Germany and Europe together is over 45% of the company's revenues, while another 24% is the USA alone. So the company's correlation in terms of performance remains heavily tilted toward Europe. However, it's not as simple as 1 or 3-year macro trends. That might be how the company trades publicly, but it's not how its earnings and sales flow. Siemens is a macro play - its orders often come from entire countries and states, and the terms are usually years - or even a decade or more.

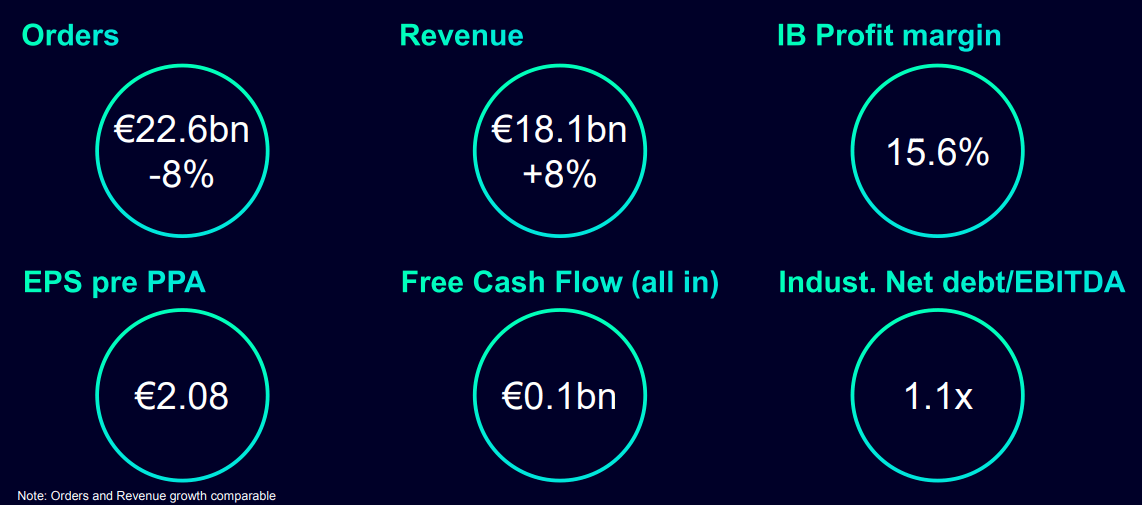

The company had an excellent 1Q23 - which we've already seen reported. Top-line results were superb, with very strong revenue growth in both SI and DI, with a new book-to-bill of 1.25x.

This is a record order book, now over €100B. The company is also continuing to gain market share in DI automation, seeing growth here.

More importantly, and despite increasing costs and inflation, the company has recorded a record 1Q23 profit of €2.7B, coming to a margin of 15.6%.

{kind=link}

Due to the company's massive backlog and how it currently flows in terms of finishes, the company has arguments for its significant growth expectations. Supply chain issues are easing a bit due to both effective management and the overall macro in terms of SCM improving. Siemens has also been able to localize its supply chains somewhat.

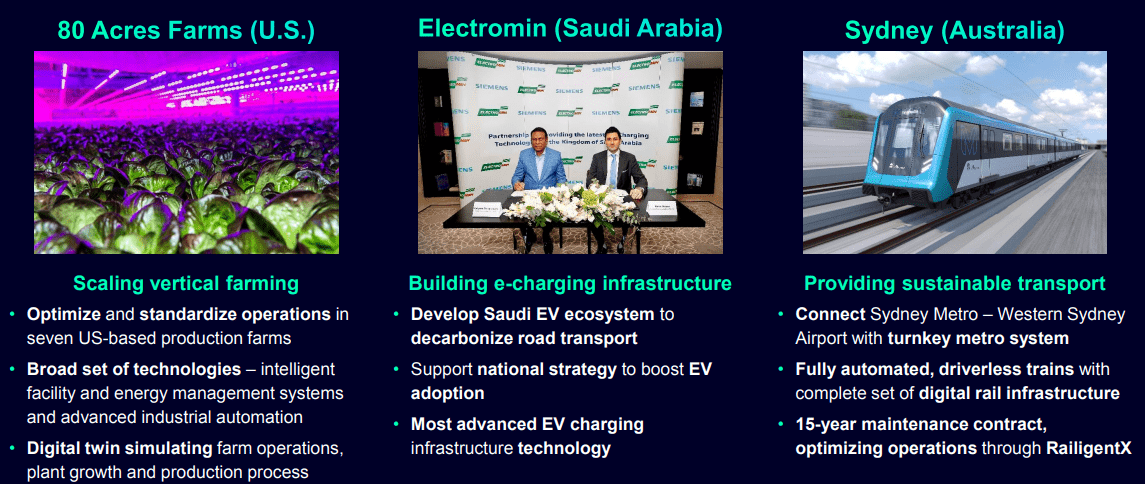

The company's projects, both current and future/orders are, of course, favorably tilted towards sustainability and resilience. This is a global sort of picture, and here are some examples of this.

{kind=link}

These sorts of projects have also become the company's focus, now introducing Co2 reduction targets, additive partnerships to promote renewables and sustainable technologies, and new applications of learning software. All of these things sound great on paper, but I'm more interested in how they affect the overall bottom line. Top-line development is excellent - and this goes for all segments, by the way. As far as I can see, the margins are either intact of improving.

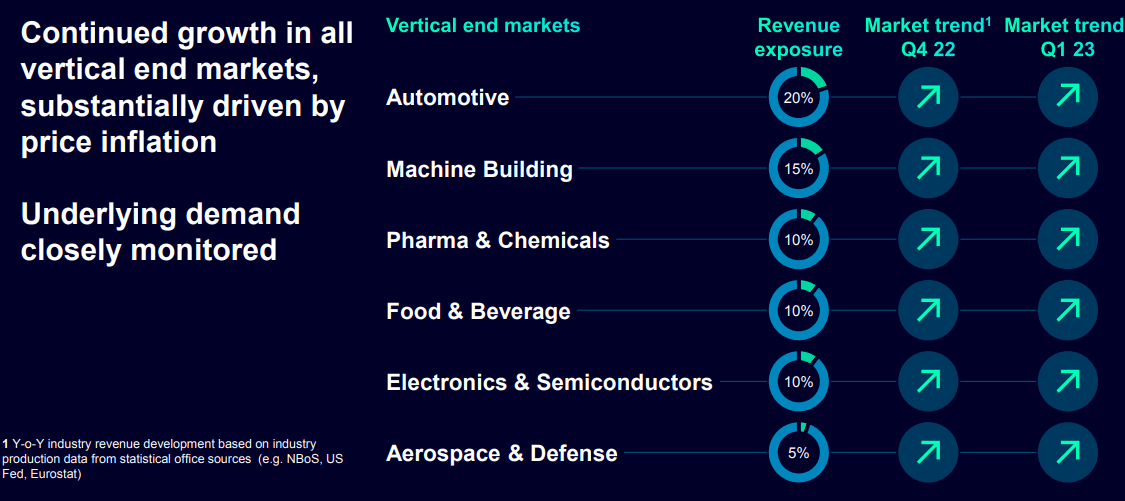

DI, for instance, I saw an expanding 70 bps profit margin improvement, with 24% increase in free cash flow ("FCF"). DI specifically is seeing growth in all verticals/industries, and much to expect from the segment going forward.

{kind=link}

There wasn't a single decline in revenues or profit margins in any one of the company's various segments - except mobility and the infrastructure segment. But this is accompanied by a major current win in the Sydney metro, but with a lot of competition on the rolling stock/railroad segment. However, the company's backlog remains strong, and more than a third of the total just looking at the Mobility orders.

The primary reasons why the company's margins are declining are due to supplier impacts, a less favorable sales mix, and some positive effects related to the sale of previously written down inventories. The bridge is an interesting read for 1Q23.

{kind=link}

The FCF was obviously not a great read, barely positive on a quarterly total basis, but, this is mostly due to temporary inventory build-up to secure company momentum in the execution of that massive backlog, as well as known timing effects. This is the way industrial companies work. However, when these unwind, starting in 2Q23, we can expect significant improvements here.

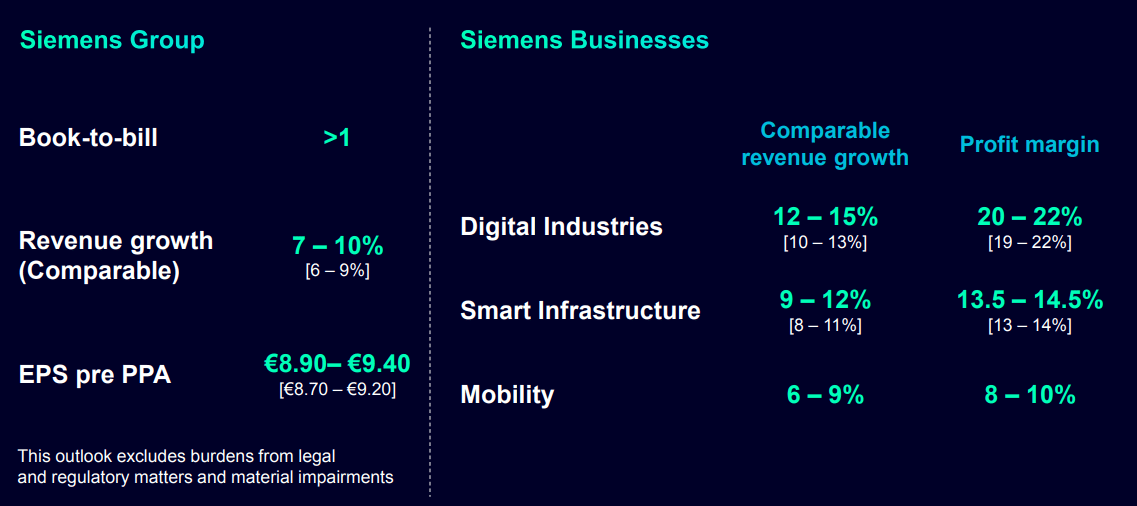

The company's outlook has been raised for the 2023E period.

{kind=link}

Overall, I want to showcase that the company has excellent operational performance relative to its circumstances. 3Q22 was a "down" quarter in terms of ROCE, with improvements here, and the company targets an average ROCE of 15-20%. Siemens is also significantly below its leverage target of around 1.5x, at about 1.1x, which leaves ample room for further M&As and moves, as well as favorable interest cost development. The company's capital structure is a fortress with very few risks.

For 2023, I'm expecting revenue growth in the mid-range single-digit numbers, with EPS forecasts above €2/share, and that's without what's known as the antigen portion of the company's earnings.

Siemens is a very long play - the holding period should, ideally, be indefinite as long as the company stays below its highest acceptable fair-value price.

For me, the highest acceptable price is simple - it's around €150/share.

Let me show you why that is in terms of valuation.

Siemens Valuation - It's Relatively Prohibitive Here, Despite Expected Growth

Siemens needs to be put in context to other industrial conglomerates worldwide because it works worldwide. On a global basis, which is where I work, the company can be put in context to LG, General Electric ( GE ), Schneider ( SBGSY ), Illinois Tool Works ( ITW ), Eaton ( ETN ), and businesses like Atlas Copco ( ATLKY ). There are plenty of qualitative businesses in this segment.

The more predictable of the companies (including in terms of earnings) are ITW and Atlas Copco, but Siemens is excellent as well.

Insider moves when we look at Siemens aren't anything worth noticing - except that some insiders have been dropping shares at similar prices to me - but a few thousand shares one way or another when it comes to insiders like this isn't anything that should cause you to go one way or another.

Predictability due to the cyclical nature of the business makes discounted cash flow ("DCF") difficult, but we can give it a shot with a simple 10-11% discount rate, estimating 4-6% in perpetuity growth rate, which gives us an FV range of €130 to €160. While I believe this range to be too wide overall, I believe the overall implications of this range to be correct. The fact that yeah, it's attractive below €130, and yeah, it's no higher than €150-€160.

But for me, no matter if you look at DCF, at peers, or at NAV (as I've spoken about before), anything above €125/share is really not something I'd want to be buying here - not for Siemens. What I look for is a double-digit upside - that's combined yield and appreciation - and I want it conservative risk/reward ratio.

If that's not something I can get, then I won't be investing.

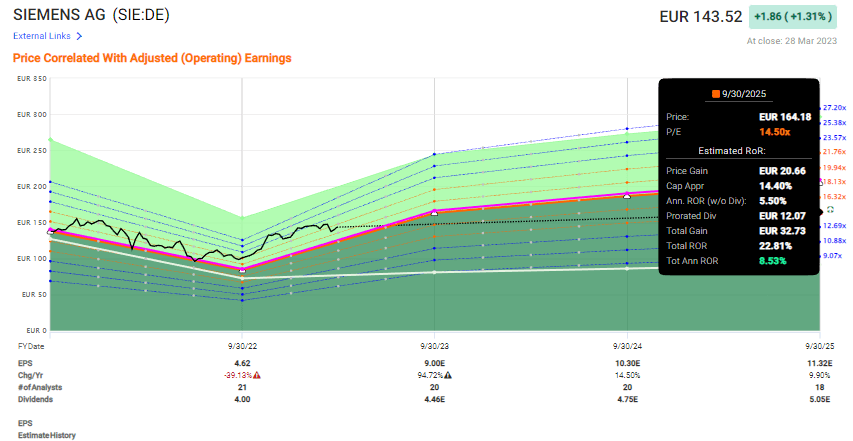

Siemens right now is certainly not buyable. The company averages a 14-15x P/E, and the upside to that multiple for 2025E is no more than 8-9% here, close to double digits - and there isn't much room for error here for the company. This is the definition of somewhat too high.

It might go higher - but I prefer cheaper alternatives, still safe, but with a higher upside.

Siemens Upside (F.A.S.T graphs)

{kind=link}

What about analysts aside from myself? Where do they see the company?

Street targets for this business reflect exuberance. 21 analysts follow Siemens, all of them at a price between €126 and €218 on the high side. Some might say that this means I'm not accounting for the company's growth correctly - I say these analysts are taking the victory too early, given that they haven't been below €125 in target for over 2 years. The current average PT based on these 21 analysts comes to €170.6, implying an upside of 19%.

Compared to a year ago, we're definitely seeing a lower number of positive indicators for the company, compared to the risk/reward ratio at this valuation. Some of the worrying indicators that imply that the company isn't as attractive here as you might think include declining Revenue/share, insider selling, a high P/O ratio, and pricing at close to 10-year highs, with dividend yields at lows and other ratios more towards the unfavorable in terms of historical contexts here.

Where Siemens really shines is the gross and operating margins - here it's both better than the average in the industry, above the 75th percentile - but when it moves to RoE, RoA, and net margins, the company is among the lower 40th percentile - and declining from its own historical position, related to how the company is structured, and the specifics of its SCM/costs in Mobility and other industries.

Bottom line is, Siemens is volatile enough to where you can wait for it to go below €135 - that's the very highest I would buy it. I want to remind you, less than 3 years ago, this company was priced at around €60/share.

That's when I bought it. That's what you should have bought.

This brings me to the following thesis.

Thesis

My thesis for Siemens Aktiengesellschaft is as follows:

- Siemens is a beyond-solid company. It's so far beyond solid that it's one of the 20 companies in my "Buy-and-hold-forever" list, along with businesses like BlackRock ( BLK ), Airbus ( EADSY ), and LVMH ( LVMUY ) - even though all of these companies, even Siemens, also do have trim targets - as I'm evidencing here, and given that I only retain a 0.3% portfolio position at this time.

- If you did not buy Siemens when it was below a normalized 10x P/E a few months back, you really missed the boat on this business and missed out on 30% RoR in a short time.

- At the right price, Siemens Aktiengesellschaft becomes a "BUY" strong enough to make me ignore or put second most other investments. I've been pushing capital to work for months now, and my stake is now 3.5%.

- My PT (price target) for Siemens is €135 - and it's a "Hold" here. I would not touch Siemens here and I am not changing my price target more than that.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

Siemens Aktiengesellschaft isn't cheap enough to buy here - I say "HOLD."

For further details see:

Siemens: Options Were Successful, Siemens Is Still Expensive, A 'HOLD'