SIGA - SIGA Technologies: Impressive Net Sales Guidance FDA Approval And Cheap

2023-11-20 00:14:35 ET

Summary

- SIGA Technologies delivered impressive net sales expectations for Q4 and is working to expand its treatment of human smallpox in new jurisdictions.

- The company has regulatory approvals for its oral antiviral drug Tpoxx and is exploring expanding its FDA label to include post-exposure prophylaxis against smallpox.

- SIGA stock has established significant agreements with government entities and international organizations to supply its Tpoxx product, which could drive net sales growth.

SIGA Technologies, Inc. ( SIGA ) delivered impressive net sales expectations for the fourth quarter and appears to be working in many jurisdictions to get its treatment of human smallpox accepted. The FDA did approve SIGA's treatments. Hence, with know-how from the United States, cash in hand, and no debt, I believe that new agreements in new jurisdictions could bring net sales growth. There are obvious risks from failed commercialization or failed testing of new products, however with very conservative free cash flow projections, I believe that SIGA appears undervalued.

SIGA Technologies

SIGA Technologies is a pharmaceutical company that markets Tpoxx, an oral antiviral drug approved by the FDA to treat human smallpox. The company also offers the intravenous formulation of Tpoxx. I invite the investors interested in the efficiency, the data sets, and the approval of Tpoxx to read the literature about the product.

In this manuscript, we describe the path to approval for the first therapeutic against smallpox, identified during its development as ST-246, now known as tecovirimat and TPOXX®, a small-molecule antiviral compound sponsored by SIGA Technologies to treat symptomatic smallpox. Because the disease is no longer endemic, the development and approval of TPOXX® was only possible under the U.S. Food and Drug and Administration Animal Rule. Source: The development and approval of tecoviromat

The drug has regulatory approvals from the EMA, Health Canada, and MHRA in the United Kingdom to treat various smallpox-related complications. The company is exploring to expand the FDA label to include post-exposure prophylaxis against smallpox. It has initiated clinical trials to evaluate the effectiveness of Tpoxx in cases of monkeypox . The company plans to use this data to possibly seek FDA approval to treat this disease.

SIGA Technologies has established significant agreements with various government entities and international organizations to supply its Tpoxx oral product as part of response preparations for biological threats and pandemics. This includes a contract with BARDA, the Biomedical Advanced Research and Development Agency, for the delivery of Tpoxx and related activities. The company has also signed contracts with the United States Department of Defense and international customers, such as Canada, to supply oral Tpoxx. These agreements are managed through an international promotion agreement with Meridian Medical Technologies, where Meridian is the intermediary for international contracts, and SIGA is responsible for the manufacturing and delivery of the products. With that about the business model, I believe the recent words from the most recent quarterly report are worth having a look at. Management is expecting to deliver oral TPOXX worth $113 million in the fourth quarter to the U.S. strategic national stockpile along with a meaningful amount of international deliveries. In my view, the growth in quarterly net sales could bring the attention of more investors, and accelerate demand for the stock.

Deliveries of oral TPOXX to the U.S. strategic national stockpile, under the third quarter BARDA contract order, have recently started and we are targeting the delivery of approximately $113 million of oral TPOXX to the stockpile in the fourth quarter. Additionally, in the fourth quarter, we are targeting $15 million - $18 million of international deliveries of oral TPOXX, as well as the delivery of approximately $5 million of oral TPOXX to the U.S. Department of Defense and deliveries of up to $15 million of IV TPOXX to the strategic national stockpile. Source: SIGA Reports Financial Results for Three and Nine Months Ended September 30, 2023

Given the net sales reported for the three months ended September 30, 2023, I believe that the delivery of oral TPOXX worth approximately $113 million in the fourth quarter would represent a significant change in the net sales growth. The net sales in the most recent quarter did not even reach $10 million.

Source: SIGA Reports Financial Results for Three and Nine Months Ended September 30, 2023

There Are New Potential Revenue Catalysts From Mpox Treatments And Treatments In The United Kingdom, The United States, and the Democratic Republic of the Congo

The company is advancing its strategy to expand the indication for oral Tpoxx, completing the enrollment of immunogenicity trials. The company is planning an extended safety trial with the goal of submitting a supplemental New Drug Application for post-exposure prophylaxis against smallpox to FDA in the early stages of 2024, subject to positive results.

In parallel, in response to an outbreak of mpox, clinical trials have been initiated to evaluate the effectiveness of Tpoxx in patients with mpox in the United States, the United Kingdom, and the Democratic Republic of the Congo. These efforts reflect the company's commitment to the development of antiviral treatments.

Clean Balance Sheet With No Debt And A Lot Of Cash For Commercialization Efforts

As of September 30, 2023, the company reported cash and cash equivalents of about $71 million, accounts receivable of $8 million, and inventory close to $64 million. Total current assets are equal to $145 million, and the current ratio is well above 1x. Hence, I am not really worried about any liquidity issues. Property, plant, and equipment stands at close to $1 million, with deferred tax assets worth $7 million, and total assets of $158 million. The asset/liability ratio is larger than 3x, so the balance sheet does look pretty stable.

Source: SIGA Reports Financial Results for Three and Nine Months Ended September 30, 2023

Accrued expenses and other current liabilities are equal to $30 million, and total liabilities were equal to $34 million. The company does not report debt at all, which appears quite ideal. I think that bankers would offer financing if necessary.

Source: SIGA Reports Financial Results for Three and Nine Months Ended September 30, 2023

Contractual Obligations: Debt Reduction Will Most Likely Bring The Interest Of More Investors

In March 2020, the company made a prepayment of $87.2 million to voluntarily extinguish a $80.0 million loan agreement, mutually releasing all obligations. The loan agreement, initiated in September 2016 with OCM Strategic Credit SIGTEC Holdings, LLC, had a maturity date based on the fourth anniversary of the Escrow Release Date or the acceleration of certain obligations.

Revenue From Research And Development Could Increase If SIGA Technologies Signs More Contracts

The company noted revenue from R&D as a result of the PEP Label Expansion R&D Contract and the 19C BARDA Contract. Given the expenditure in sales and marketing and the expertise accumulated with Tpoxx in patients, I believe that we could see agreements with international organizations. As a result, we could see net sales growth. The following is information from a recent quarterly report.

Revenues from research and development activities for the three months ended September 30, 2023 and 2022, were $1.3 million and $6.6 million, respectively. These revenues are mostly earned in connection with performance of research and development activities under the PEP Label Expansion R&D Contract and the 19C BARDA Contract. The decrease of $5.3 million of revenue is primarily related to a decrease in clinical trial activity. Source: 10-Q

Valuation Of Other Companies In The Same Sector

According to Seeking Alpha, the EV/EBIT sector median is close to 16x-19x, and the price/cash flow is equal to 15.8x-16x. SIGA Technologies is a very small company, so I believe that the trading multiple may be way lower than that of competitors. In my DCF model, I assumed an exit multiple of close to 5x-9x FCF, which I believe is significantly conservative.

Source: SA

DCF Model: I Believe That The Company Is Undervalued

Under my financial model, I did not include the acceptance of new treatments from the FDA. I took into account previous cash flow statements and the potential new agreements with new governments in Europe and outside the United States. I also included potential revenue growth from research and development done for new entities. Given the knowledge accumulated in the United States, I do not see why the company could fail elsewhere.

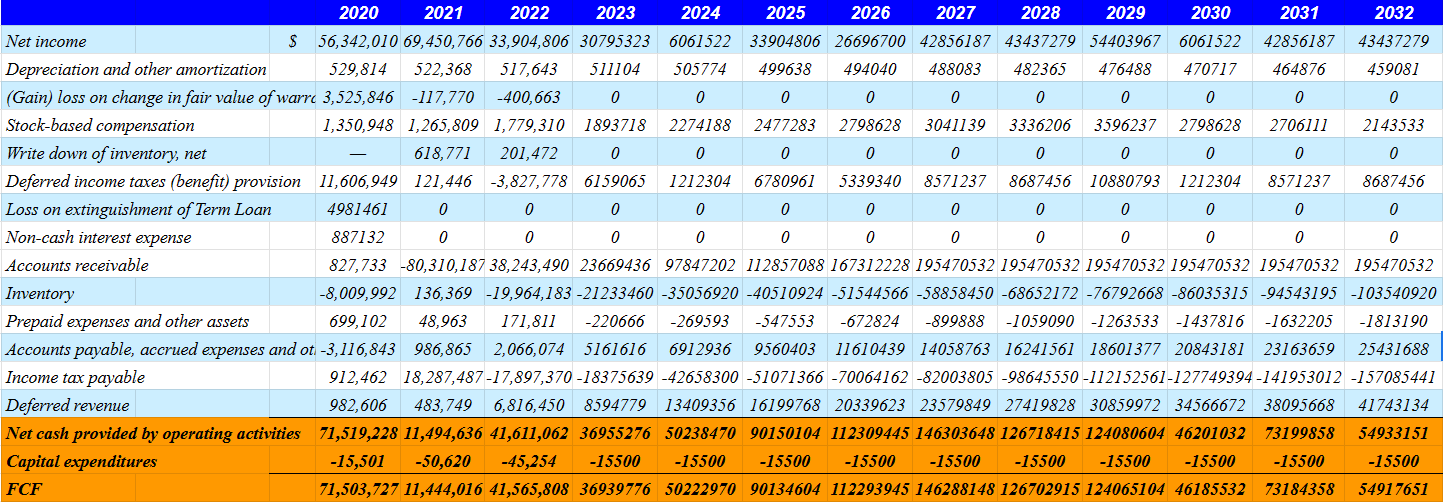

My expectations include a 2032 net income of about $43 million, 2032 stock-based compensation of close to $2 million, changes in accounts receivable of $195 million, and changes in inventory of about -$104 million.

Besides, with prepaid expenses and other assets of close to -$2 million and changes in accounts payable, accrued expenses, and other liabilities of $25 million, I also included deferred revenue of $41 million. Finally, 2032 net cash provided by operating activities would stand at $54 million, with FCF of about $53-$54 million.

{kind=link}

I believe that my FCF expectations are in line with previous FCF results. Moreover, my FCF expectations are also in line with the expectations noted in the most recent quarterly release.

Source: Ycharts

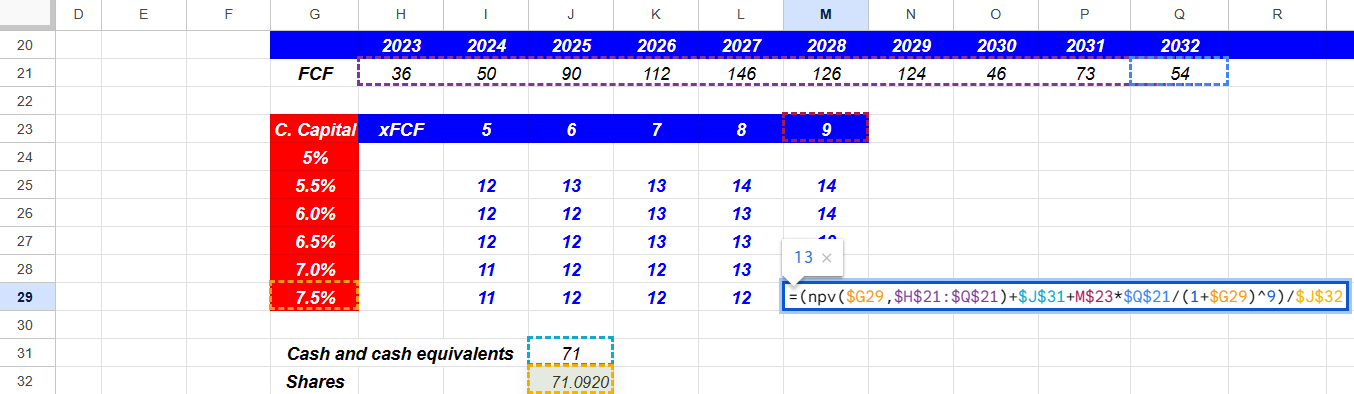

From 2023 to 2032, I expect FCF to range from $36 million to $146 million. With an exit multiple of 5x-9x and cost of capital close to 5% and 7.5%, my DCF model implied price forecasts between $11 and $14 per share.

{kind=link}

{kind=link}

In addition, the internal rate of return would be close to 13% and 19% with a median IRR of 15%-16%. Other financial analysts may use different assumptions and EV/FCF exit multiples, however, I do not think that their expectations will be far from mine. In sum, I believe that the company is undervalued.

Source: DCF Model

Risks And Competitors

In my opinion, the company faces significant risks in connection with government contracts. Fixed price contracts can result in losses if not managed properly, as the company must deliver products at a fixed price regardless of actual costs. Government agencies, such as the DCAA, regularly audit contractors, and failure to comply with laws and regulations can result in civil penalties, which would negatively impact the company's profitability and reputation. It is crucial for the company to maintain rigorous internal control systems and policies besides effectively managing costs to mitigate these risks.

In my opinion, operating in a highly dynamic and competitive environment, SIGA Technologies faces fierce competition in the pharmaceutical and biotechnology industries. Its competitors, which include renowned pharmaceutical companies with abundant technical and financial resources, as well as medical countermeasures companies, such as Emergent BioSolutions Inc. ( EBS ) and Bavarian Nordic A/S ( OTCPK:BVNKF ), are also competing in seeking government funding for emergency preparedness products. The company is at constant risk of losing business opportunities if it is unable to develop safe, effective, and affordable products that meet government requirements, particularly those of the United States. Innovation and efficiency are essential in its competitive environment.

My Opinion

SIGA Technologies is a pharmaceutical company that has a flagship product, Tpoxx, approved by multiple regulatory agencies. Its business strategy involves expanding Tpoxx's indications and participating in clinical trials to address emerging diseases. Given the recent announcement about the incoming delivery of TPOXX to the U.S. strategic national stockpile, I believe that SIGA's revenue growth could increase in the coming years. Besides, the company managed to extinguish a loan in 2020, therefore it no longer has debt. There are risks from changes in laws and regulations, which could result in civil penalties, as well as failed new products or testing. With that, SIGA Technologies does appear undervalued.

For further details see:

SIGA Technologies: Impressive Net Sales Guidance, FDA Approval, And Cheap