ALB - Sigma Lithium: Risk-Reward Profile Improved Significantly Despite Strong Rally

2023-06-20 12:51:55 ET

Summary

- Sigma Lithium's stock has seen a 55% appreciation in 10 months since my previous article. Recent developments necessitate an updated investment thesis.

- The new technical study indicates that the NPV-8 for the expanded Grota do Cirilo project is 3X that of Phase 1. As a result, Sigma appears to be cheaper now.

- The successful commencement of Phase 1 production, along with the sale of lithium concentrate and tailings, and the receipt of first revenue, has significantly derisked the project.

- Therefore, the risk-reward profile has improved significantly.

So much has happened since my last article on Sigma Lithium Corp. ( SGML ) (SGML.TSX-V).

- In December 2022, Sigma completed a technical study , expanding the mineral resource and reserves at the Grota do Cirilo project, Brazil. This extended the mine life, and confirmed the economic viability of constructing Phase 2 and Phase 3 of the project. Shortly thereafter, the company secured $100 million in debt financing and initiated detailed engineering for the plant expansion.

- Following the commissioning of the Grota do Cirilo plant from December 2022 via January 2023 to February 2023 , Sigma obtained the environmental operating license in April 2023. They began producing lithium concentrate in mid-April 2023, shipped the first batches of lithium concentrate and tailings at the end of April 2023, and received the first payment in May 2023, marking a significant milestone of revenue generation.

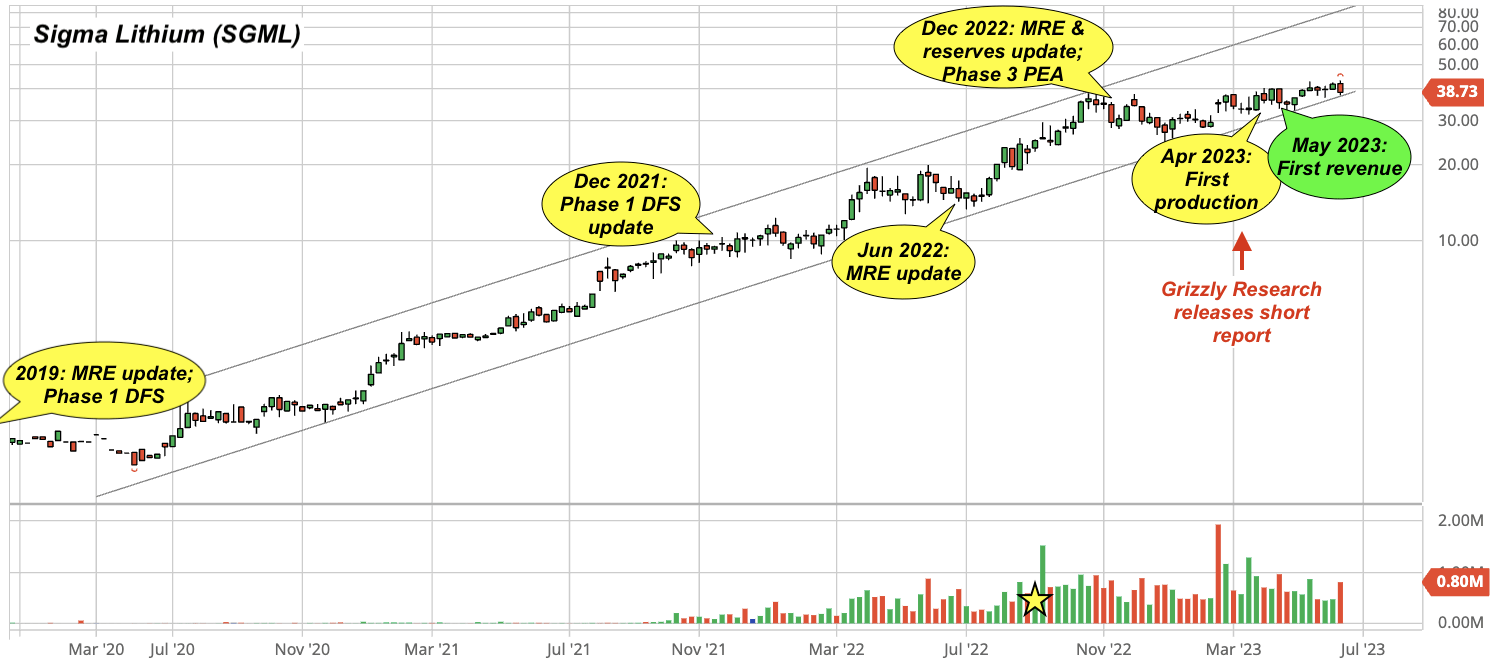

- Despite a peculiar short seller attack in late March 2023, just before the start of production, Sigma Lithium persevered. As a result, the stock has delivered a 55% gain from September 2022 - when my previous piece was published - to the present, as depicted in Figure 1.

Fig. 1. Stock chart of Sigma Lithium, shown with major operational events, with the gold star being the publication of the article by Laurentian Research (Laurentian Research for The Natural Resources Hub based on Sigma Lithium, Barchart and Seeking Alpha)

{kind=link}

With operations reaching a critical juncture after the start of Phase 1 production, investors may find themselves contemplating their next move regarding the stock: should they sell and secure their profits or hold on for potential further capital appreciation, driven by the anticipated Phase 3 production? In the following analysis, we will delve into the details.

The Grota do Cirilo project

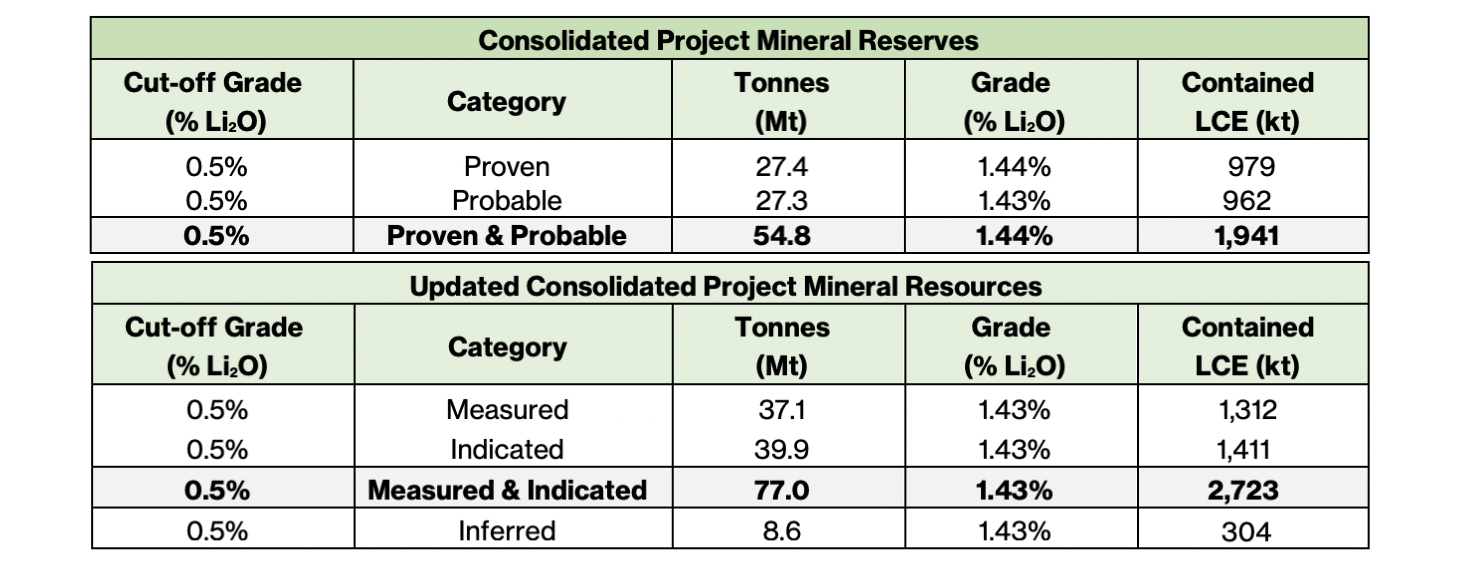

According to the updated technical report from December 2022, the Grota do Cirilo project holds a total of 3,027 kt of measured, indicated, and inferred lithium carbonate equivalent (LCE) resources. These include 1,941 kt of proven and probable LCE reserves, as depicted in Figure 2. The consolidated mineral resources encompass 984 kt of LCE in the measured and indicated categories for Phase 3, while the consolidated mineral reserves include 759 kt of proven and probable LCE reserves for Phase 3.

Fig. 2. Consolidated project mineral reserves and resources in the Grota do Cirilo project of Sigma Lithium, mineral resources being inclusive of mineral reserves (modified from Sigma Lithium)

{kind=link}

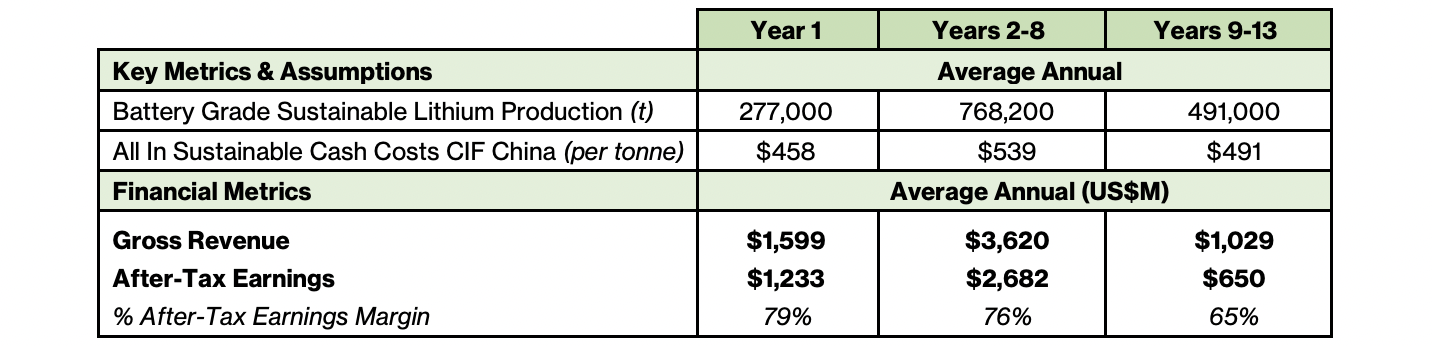

The aforementioned mineral reserves provide support for a 13-year mine life, producing 277 ktpa of battery-grade sustainable lithium concentrate in year 1, 768 ktpa in years 2-8, and 491 ktpa in years 9-13. With an additional capital investment of $155 million for project expansion and benefiting from low all-in sustaining costs (or AISC) ranging from $458/t to $539/t, the combined three phases of Grota do Cirilo exhibit strong project economics. This is demonstrated by an after-tax NPV-8 of $15.3 billion, as illustrated in Figure 3, which is 200% higher than the after-tax NPV-8 for Phase 1 that was used in my previous article analysis of the risk-reward profile.

Fig. 3. Key economic parameters of the Grota do Cirilo project, as in the December 2022 updated technical study (Sigma Lithium)

{kind=link}

Upside and risks

As of June 16, 2023, Sigma Lithium had a market capitalization of US$4.15 billion and an enterprise value of US$4.08 billion. In terms of the P/NAV multiple, Sigma is valued at 0.27X. It is worth noting that Sigma has only delineated lithium resources at five of the nine known artisanal deposits so far, and future exploration success is expected to support additional phases of development and production growth. Sigma is clearly undervalued compared to its peer, Lithium Americas Corp. ( LAC ), another new producer, which is currently valued at 0.44X when all four projects are considered, including Thacker Pass (100%), Caucharí-Olaroz (44.8%), Pastos Grandes (100%), and Sal de la Puna (65%).

Sigma Lithium is valued at an implied P/FCF multiple of 7.0X for Phase 1 or 2.3X for Phase 1, 2 and 3, which is notably cheaper than established lithium producers such as Allkem ( OROCF ), Albemarle ( ALB ), and Sociedad Química y Minera ( SQM ), whose P/FCF multiples range from 21X to 27X, or even Pilbara Minerals ( PILBF ) at 8.4X. In terms of the EV/EBITDA multiple, Sigma Lithium is valued at 2.8X, compared to 6.5X for the aforementioned established lithium producers.

Between September 2022 and the present, the estimated NPV-8 for the Grota do Cirilo project tripled, while the Sigma Lithium share price only appreciated by 55%, indicating that the stock has actually become cheaper.

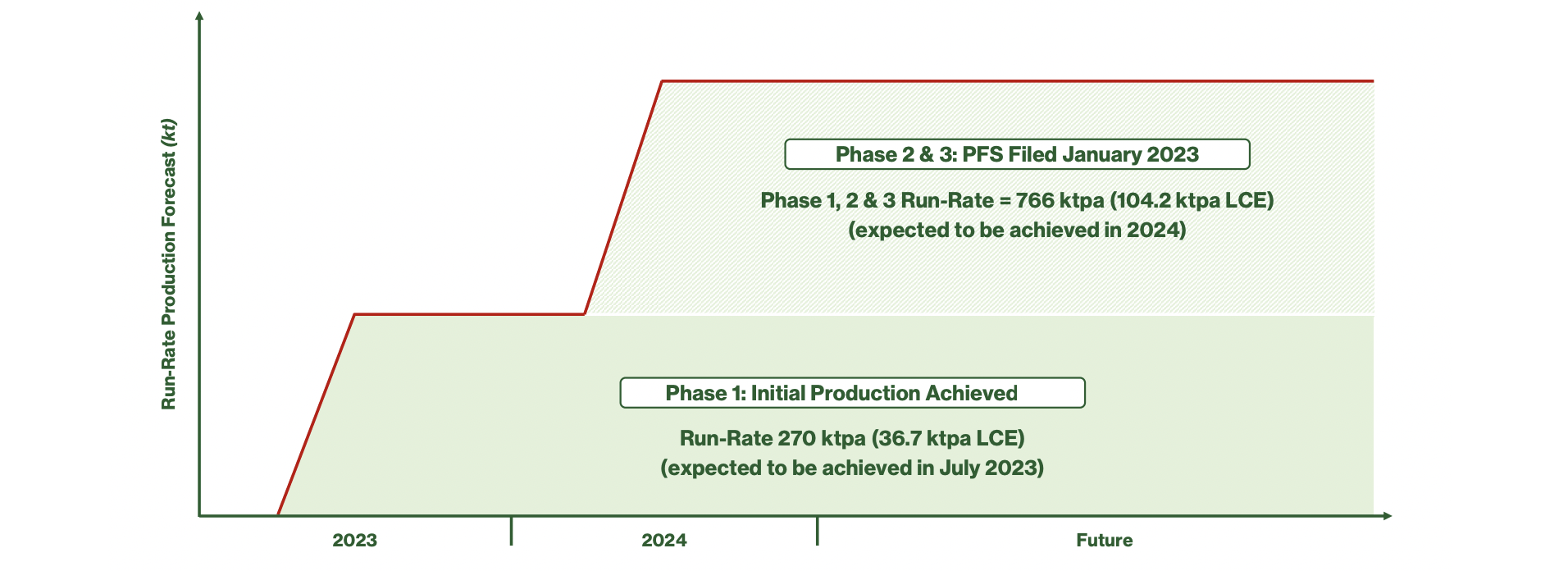

The undervaluation of Sigma Lithium may not last long, considering the near-term catalysts, including the fully-funded Phase 2 production expansion, expected to start in mid-2024, as shown in Figure 4. By then, Sigma Lithium will emerge as one of the top five lithium producers in the world, following SQM, Albemarle, and Allkem-Livent , and surpassing Pilbara Minerals, which provides a compelling reason to believe that it will no longer remain under the radar.

Fig. 4. Anticipated production profile of the Grota do Cirilo project of Sigma Lithium, including Phase 1, 2 and 3 (Sigma Lithium)

{kind=link}

Perceived risks associated with Sigma Lithium may include Brazil as a mining jurisdiction, the technical ability of the management, and offtake agreements. However, the successful commencement of the Phase 1 project, the sale of lithium concentrate and tailings, and the receipt of first revenue indicate a significant decline in these risks. Such derisking greatly enhances the risk-reward profile of Sigma.

To those investors who have stayed on the sidelines due to the short seller attack launched in late March 2023, I can only say that the operational accomplishments of Sigma Lithium since then have effectively refuted each of the key arguments against the company. Additionally, the ad hominem attack on CEO Ana Cabral Gardner did not contribute to the credibility of the short thesis.

Investor takeaways

Since the publication of my previous article in September 2022, Sigma Lithium has successfully delivered on all of its promises. These operational achievements have significantly improved the company's upside potential and substantially reduced project-related risks. However, despite these significant advancements, the share price has only experienced a modest 55% appreciation.

When evaluating Sigma Lithium's current valuation, it becomes evident that the company is undervalued compared to both its peers and the intrinsic value derived from its in-situ reserves, projected EBITDA or free cash flow. With the completion of the project expansion expected by mid-2023, Sigma is poised to emerge as one of the top five lithium producers globally. As a result, I anticipate continued appreciation in the share price over the next 12 months.

Considering these factors, I maintain a buy rating on Sigma Lithium at this time.

Allow me to conclude this piece with a quote from Peter Lynch:

"It takes remarkable patience to hold on to a stock in a company that excites you, but which everybody else seems to ignore. You begin to think everybody else is right and you are wrong. But where the fundamentals are promising, patience is often rewarded..."

For further details see:

Sigma Lithium: Risk-Reward Profile Improved Significantly Despite Strong Rally