SBNYP - Signature Bank: When Preferred Equity Goes To Zero

2023-03-13 09:48:01 ET

Summary

- Last night the New York state's Department of Financial Services took over Signature Bank.

- The regulator created a new entity, Signature Bridge Bank, which will hold Signature Bank's assets of $110.4B and total deposits of $82.6B.

- Any residual amount left over from a sale or wind-down of Signature Bridge will be passed to the old entity.

- Most slices of Signature Bank's capital structure are now almost entirely wiped out.

- A bank run moves preferred securities to having the same recovery as common equity.

Thesis

Last night, the New York state's Department of Financial Services took over Signature Bank ( SBNY ). That was a surprising move, given that other "problem banks," as identified by their stock moves on Friday, seem to continue to be ongoing entities. Let us have a closer look at what happened:

The FDIC on Sunday night established Signature Bridge Bank as the successor to now shuttered Signature Bank ((SBNY)).

The new bank is operated by the FDIC. All deposits from Signature Bank ((SBNY)) and almost all of its assets are now with Signature Bridge Bank.

As of Dec. 31, 2022, Signature Bank had total assets of $110.4B and total deposits of $82.6B.

So in actuality, the regulators created a new entity called "Signature Bridge Bank" where they are stuffing all of the deposits and assets from SBNY. So what is the old entity left with? Well it is left with liabilities in the form of senior unsecured bonds, and equity in the form of common and preferred equity.

New Entity Creation

The regulators are presumably either going to work through the new entity or try to sell it, but given the first look at the bank's balance sheet to us the probability of some net recovery is high. Firstly, the method utilized for SBNY is different from the SVB debacle:

A bridge bank is an institution that has been authorized by a national regulator or central bank to operate an insolvent bank until a buyer can be found.

A bridge bank is charged with holding the assets and liabilities of the failed bank until the bank becomes solvent again—either through acquisition by another entity or through liquidation.

A bridge bank is usually established by a publicly backed deposit insurance organization, such as the Federal Deposit Insurance Corporation ((FDIC)), or a financial regulator. In the United States, the FDIC was given authority to charter these temporary banks by the Competitive Equality Banking Act ((CEBA)) of 1987.1

Right now the regulator is telling us the new bank has $110.4 billion in new assets and $82.6 billion in deposits. So, mathematically (ignoring mark-to-market for a second), there seems to be a significant residual here after all the deposits are wound down. We are not going to speculate what that actual figure is going to be and will let the claims market do that.

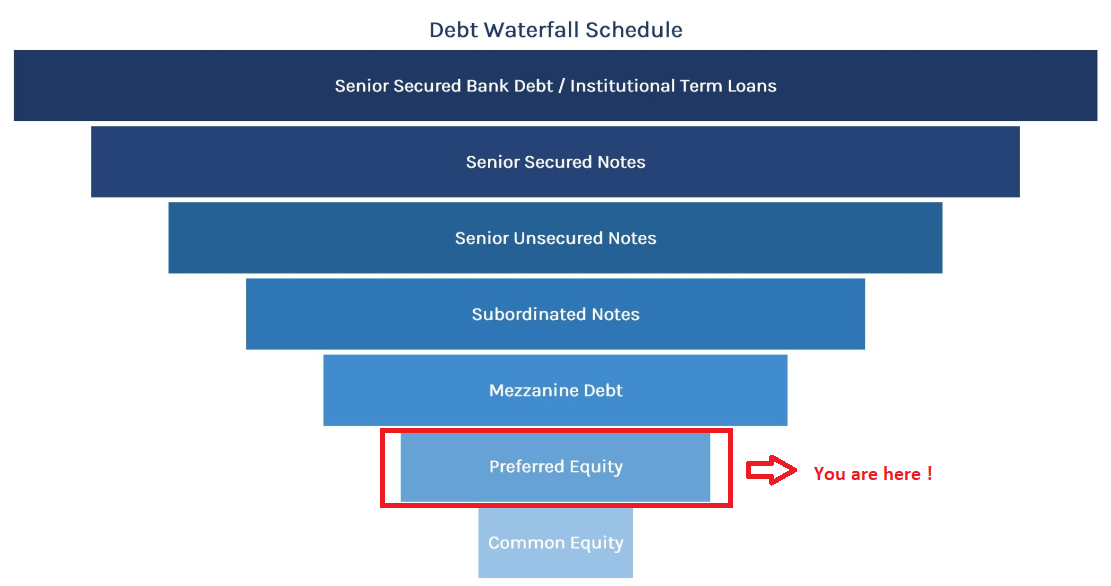

As a reminder, even after Lehman failed, there was a secondary market for the claims to the estate, and the ultimate recovery was somewhere around 31% . The pressing question is though if the SBNY preferred shares, namely ( SBNYP ), which we unfortunately hold in a small amount, will get anything. Let us revisit the capital structure waterfall for a corporation.

Capital Structure Waterfall

In a bankruptcy or restructuring, the monies available from the estate have a well-defined distribution pattern:

{kind=link}

Common equity is at the bottom, and in SBNY's case we see zero recovery here. Similarly, the second lowest piece of the capital structure, namely preferred shares will get zero in this instance.

We believe that any residual dollar figure from Signature Bridge Bank will be used to pay general liabilities for the bank first (such as rent, professional services, utilities, etc.) and then utilized to pay down Senior Unsecured notes. Shockingly, the bank's debentures were trading at 85 c/$ on Friday:

SBNY Bonds Pricing (FINRA)

We think they will now trade in the teens, depending on where the market sees recovery on these by pricing the bank's investments.

Bank Runs upend all other rules

It is still a bit shocking that SBNY was taken over while the likes of First Republic Bank ( FRC ) were not, but the rumors are that the bank saw massive deposit outflows on Friday. We cannot confirm any of these discussions, but the reality is that a bank run upends all prior capital rules. If faith in a banking entity disappears, then all rules go out the window, and most capital slices are dented.

The debentures shown in the graph above are investment grade, and in the span of a few days went from 96 c/$ to probably low teens. On Friday, the bond market was telling us that SBNY was still very much solvent.

Unfortunately for the preferred equity, it has been completely wiped out, and in this case we can be sympathetic because the next slice of the capital structure is similarly affected. A recovery in the teens (i.e., a total loss above 80% for the bonds) is not a good story, or something to envy.

All investors in SBNY's capital structure are pretty much wiped out. And that is what the regulators wanted and their messaging - they will protect the depositors, but investors in banks that were mis-managed will suffer almost complete wipeouts.

Conclusion

SBNY was a New York-based commercial bank. The bank was taken over by regulators this past Sunday (March 12), and all its assets and deposits transferred to a new bridge entity. Irrespective of whether the wind-down is protracted or there is a buyer, the residual amount will not be sufficient to cover more than the general claims on the bank (rent, utilities, etc.) and some of the Senior Unsecured bonds balances. As preferred shareholders in the old entity, we are penciling in a zero recovery here for SBNYP.

For further details see:

Signature Bank: When Preferred Equity Goes To Zero