PANDY - Signet Jewelers: Still A Nice Fit If You Can Handle The Volatility

2023-08-18 12:41:54 ET

Summary

- Signet Jewelers Limited is an interesting firm that historically generates attractive cash flows, and shares have outperformed the broader market in recent months.

- This year has been particularly interesting, due in large part to a sizable decline in revenue.

- But the price of the stock makes it worth the uncertainty, so long as you can handle the volatility.

In recent years, one of the companies that I have come across that has had some of the most extreme volatility from a financial perspective is none other than, perhaps surprisingly, Signet Jewelers Limited ( SIG ). From any given period of time to any other, the business will report wild swings in revenue, profits, and cash flows. Beyond any doubt, this requires us to apply some sort of discount to the company because of the increased risk that comes with volatile results.

But if the stock is cheap enough, that volatility could well be worth it. That is what I determined back in June of last year. And since then, shares of Signet Jewelers have significantly outperformed the broader market. Fast-forward to today, and the same situation applies. Financial results are all over the map, but shares look very cheap, both on an absolute basis and relative to similar firms.

Given all of this, I have decided to keep the company rated a "buy" to reflect my view that shares should continue to outperform the broader market for the foreseeable future.

Interesting times

Personally, I don't care much for jewelry. But it doesn't necessarily matter what I like. What matters is where the opportunities are. And in June of last year, I found myself drawn toward Signet Jewelers. In the article that I wrote at the time, I was talking about expectations for the first quarter of the company's 2023 fiscal year. The firm was just about to announce results for that quarter. My argument was that the data reported by management would go a long way toward determining whether or not the company was seeing success when it came to its turnaround initiatives.

Given how cheap the stock was leading up to earnings, I had no choice but to be bullish about the firm. And since then, the "buy" rating that I assigned it has played out well. Shares are up 23% at a time when the S&P 500 (SP500) is up only 7.5%.

{kind=link}

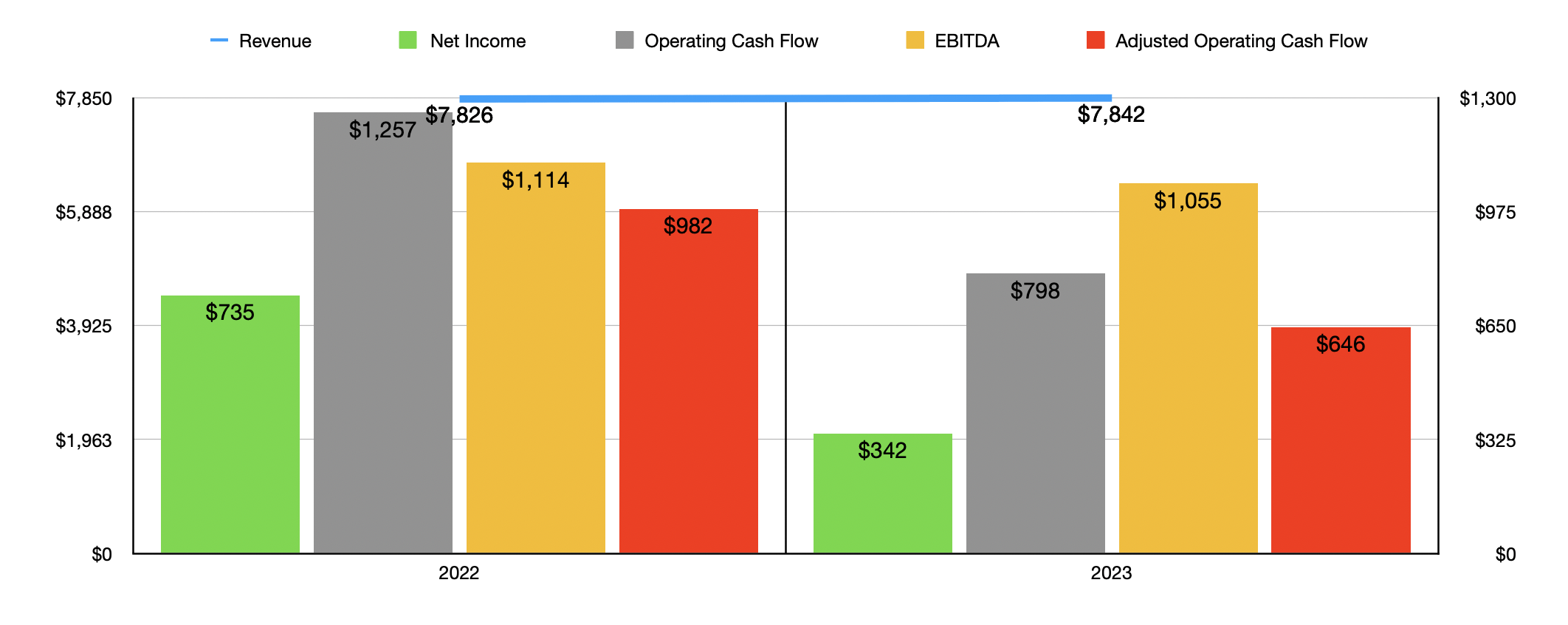

You would think, given this returned disparity, that all has been going great with Signet Jewelers from a fundamental perspective. But the truth is more complicated than that. Let's look at how the company performed for the entirety of its 2023 fiscal year . During that time, revenue came in at $7.84 billion. That's only marginally higher than the $7.83 billion the company reported one year earlier. We need to dig down deep into the company, however, you find that the picture is more complicated than a small uptick in sales. Actual same-store sales for the company declined during that time by 6.1%.

Management attributed this pain to high inflationary pressures that impacted, obviously negatively, the discretionary spending of consumers. Shifts in consumer spending to focus more on experiences and travel, as well as the dying down of economic stimulus payments and a weaker British pound internationally, all combined to hurt the company. The only reason why sales increased was because of the firm's acquisitions of Diamonds Direct and Blue Nile. It is worth mentioning, however, that sales would have been higher had a not been for foreign currency fluctuations. On a constant currency basis, overall revenue was up 1.1%. So investors should give the company credit for that.

Even though revenue increased nicely, profits for the business took a beating, plunging from $735.4 million in 2022 up to $342.2 million in 2023. There were two key drivers behind this pain. First, the company went from reporting $8.5 million in other operating income in 2022 to reporting $209.9 million of other operating expenses. This was largely the result of a $203.8 million pre-tax litigation charge that the company had to contend with. But this is the kind of pain we should like to see if we have to have pain. And that's because it is something that should not be repeated in the future.

Non-operating expenses, outside of interest, went from $2.1 million to $140.2 million. This swing was driven largely by additional litigation-related costs of $133.7 million on a pre-tax basis, and that were non-cash in nature. Other profitability metrics for the company followed a similar path. Operating cash flow went from $1.26 billion to $797.9 million. If we adjust for changes in working capital, we would get a drop from $982.3 million to $645.7 million. And finally, EBITDA fell from $1.11 billion to $1.06 billion.

{kind=link}

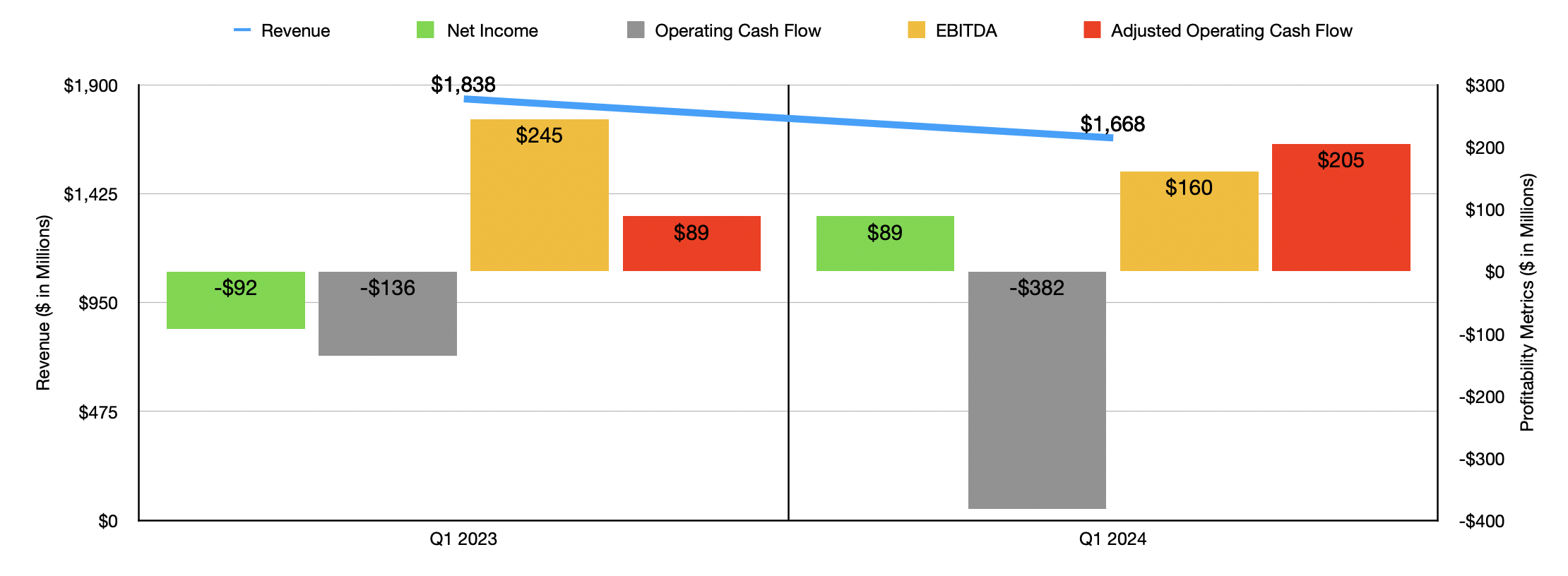

The volatility that the company experienced during 2023 also was present in the first quarter of 2024. Revenue dropped from $1.84 billion to $1.67 billion. That decrease, totaling 9.3% in all, would have been only 8.7% had it not been for foreign currency fluctuations. The real pain for the company, however, was the 13.9% drop in same-store sales. The same issues that impacted same-store sales in 2023 also were at play here. The bottom line, however, was even more radical than it was last year.

The company went from generating a net loss of $92.1 million in the first quarter of 2023 to generating a profit of $88.8 million the same time of the 2024 fiscal year. The aforementioned litigation charges last year were responsible for the downside the company experienced. But for the current fiscal year, it is worth noting that the firm's gross profit margin declined from 39.4% to 37.9%. So had it not been for the litigation-related costs, bottom line results for the company would have worsened this year relative to last year. And that is because of the impact of inflationary pressures and the company's inability to pass all of that impact onto its customers.

Even though profits increased nicely year over year, the same cannot be said of operating cash flow. It went from negative $135.5 million in the first quarter of 2023 to negative $381.8 million the same time this year. If we adjust for changes in working capital, we would get an increase from $88.6 million to $205.3 million. Normally, you would expect an increase of this magnitude to result in EBITDA also climbing. But the metric ultimately dropped from $244.6 million to $160.4 million.

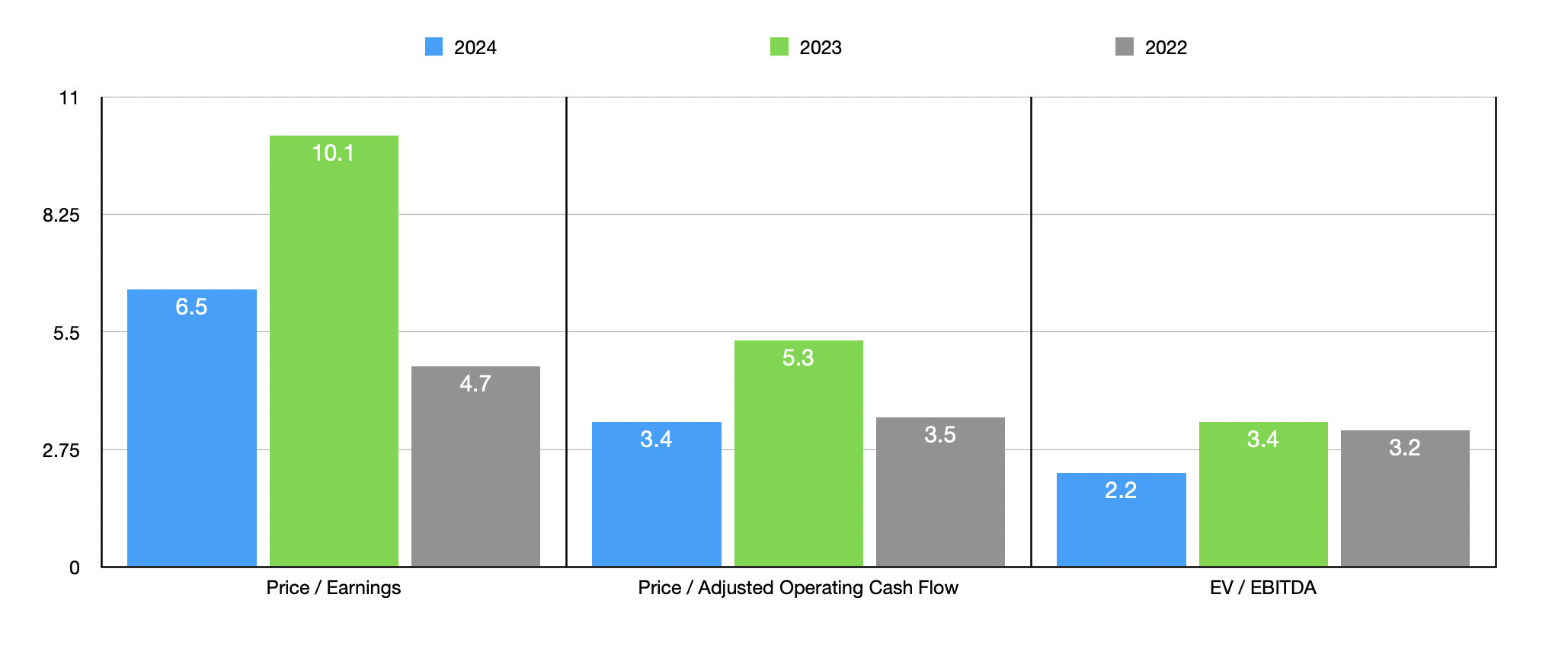

When it comes to the current fiscal year, management is forecasting revenue of between $7.10 billion and $7.30 billion. Even at the high end, that would be a substantial drop compared to what the company reported for 2023. Earnings per share, meanwhile, should be between $9.49 and $10.09. That would translate to net income, at the midpoint, of $533.6 million. If we assume that other profitability metrics increase at the same rate that net profits are forecasted to, we would expect an adjusted operating cash flow of $1.01 billion and EBITDA of approximately $1.65 billion.

{kind=link}

Using these figures, I was able to create the chart above. It shows how the company is priced on a forward basis. It also shows how the stock is priced using data from both 2022 and 2023. Even if we use the more conservative results from 2023, the stock still looks very attractive from a valuation perspective. And in the table below, you can see that I compared the enterprise to three similar firms. On a price to earnings basis, one of the three companies ended up being cheaper than Signet Jewelers. But when it came to the price to operating cash flow multiple and the EV to EBITDA multiple, our prospect ended up being the cheapest of the group.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Signet Jewelers |

| 10.1 |

| 5.3 |

| 3.4 |

| Pandora A/S ( PANDY ) |

| 14.0 |

| 10.6 |

| 7.9 |

| Movado Group ( MOV ) |

| 7.4 |

| 11.7 |

| 3.5 |

| Fossil Group ( FOSL ) |

| 19.0 |

| N/A |

| 8.7 |

Takeaway

There's no doubt that this year is something of a challenge for the company. Signet Jewelers seems to be used to that kind of volatility. Likely, its investors are as well.

Even with what is looking to be a difficult year, shares of the company look very cheap. And they are still cheap if we use the results from last year. This is true on both an absolute basis and relative to similar firms. So because of that, and in spite of the fact that shares have already drastically outperformed the broader market since I last wrote about the company, I have decided to keep Signet Jewelers Limited rated a soft "buy" at this time.

For further details see:

Signet Jewelers: Still A Nice Fit If You Can Handle The Volatility