JBHT - Significant Changes Might Greatly Alter America's Rail Transportation System

2023-09-07 13:00:38 ET

Summary

- The American railroad network has condensed into six major freight entities, with Burlington Northern Santa Fe and Union Pacific being two of the largest.

- The railroad industry has undergone significant changes throughout history, including deregulation in the 1970s and the loss of passenger services.

- The future of the railroad industry faces challenges such as compressed capacity, increased operational risk, and competition from other modes of transportation.

- Coming changes are likely to drastically alter both freight and passenger patterns enabling significantly higher growth in the American Railroads.

- Watching how the private majors react to these changes will become important in wise investing.

The American railroad network has played important roles in the expansion of economic growth for over two centuries: it's clearly long-term. During its existence, change, forced marketplace change, dominated the landscape. Today's network condensed itself from its multitudes of flags into six major freight entities: Burlington Northern Santa Fe (BNSF), the Union Pacific ( UNP ), Norfolk Southern ( NSC ), CSX ( CSX ), Canadian National ( CNI ) and Canadian Pacific Kansas City with significantly less trackage or usable right of way ((ROW)). The majors are supplemented by a multitude of short lines, over 600, Genesee and Wyoming being the largest. Our discussion centers around long-term investing. For some this seems irrelevant; for us, it isn't. One of our holdings exceeds 25 years, a similar length of time considered here. For investors who don't understand possible values in long-term visions, perhaps this opens new thoughts, " [I]f you were around to snag a share [of Coke] at $40 [in 1919]... it would be worth about $10 million today."

Change, the ever-present constant, is once again afoot. Among the coming is the ever-increasing population redistribution driven by political, technological or other forces; demand growth opening new doors into more options; and a coming world dominated with significantly higher energy costs, particularly for airlines and trucks. Before we head into the forest to extinguish some fires (discussed later), we note that picking investments especially for the long run requires a comparison between a company's vision and its relative reactions to paradigm shifts. Now, would you grab the gear and come along?

A Short History of Rail

From the dawn of time, transportation of all kinds challenged the minds and skills of the human race. Whether the task involved mankind or necessary goods, the endeavor to increase efficiencies, reduce societal costs while increasing speed, was ever present.

By the early 1800s, a technology largely developed in England, the iron horse, found its way into American business, i.e., Baltimore & Ohio (B&O). By 1840, lands east of the Mississippi hosted near 3,000 miles of track. The importance of railroads proved itself during the American Civil War thus opening doors into its Golden Age between 1860 and 1930. In that period, four major railroads constructed lines from the Mississippi to the West Coast, knitting together the continent.

The roads leading west demanded enormous resources. In the case of the Union Pacific/Central Pacific, Congress passed legislation assisting the project through the Pacific Railway Act . Lobbied for by interested business representatives, the Act offered generous subsidies including: 200 feet of land on each side of the right of way, 30-year construction bonds of $16,000 to $48,000 depending on the landscape and odd sections of public land. At maturity, the law required railroads to repay bonds. Later, testimony offered from the two companies stated that the total capital was $50 million for the Central and $60 million for the Pacific, an enormous amount in the 1800s. This ACT also assisted in building the rest of the western roads except James J. Hill's, Great Northern. Without a sizable level of government involvement, these projects would have been drastically delayed or never built.

The Golden Age, a period without significant competition, continued through the 1920s being stunted with the effects of an enduring, deep depression and early competition from autos and air. A short resurgence appeared during the 2nd World War continuing shortly thereafter.

In the sixties, the multiple of flags faced the reality that freight traffic was the only route to profitability forcing an exit from passenger services, the last straw being thrown by Lyndon Johnson with his canceling of the lucrative 1st class mail contracts. The Nixon Administration created a highly disjointed passenger service through a corporation primarily owned and funded by the Federal Government (AMTRAK) . Service began i n 1971. In its creation, law dictated a relatively strong mandate requiring now freight-only railroads to give priority dispatching to the Amtrak service with timely operation being a requirement for viable service. Over time, a very bitter and fiery relationship developed between the two for many reasons, but primarily a result of this dispatching mandate.

1970s Through 1990: A Truly Transformative Period

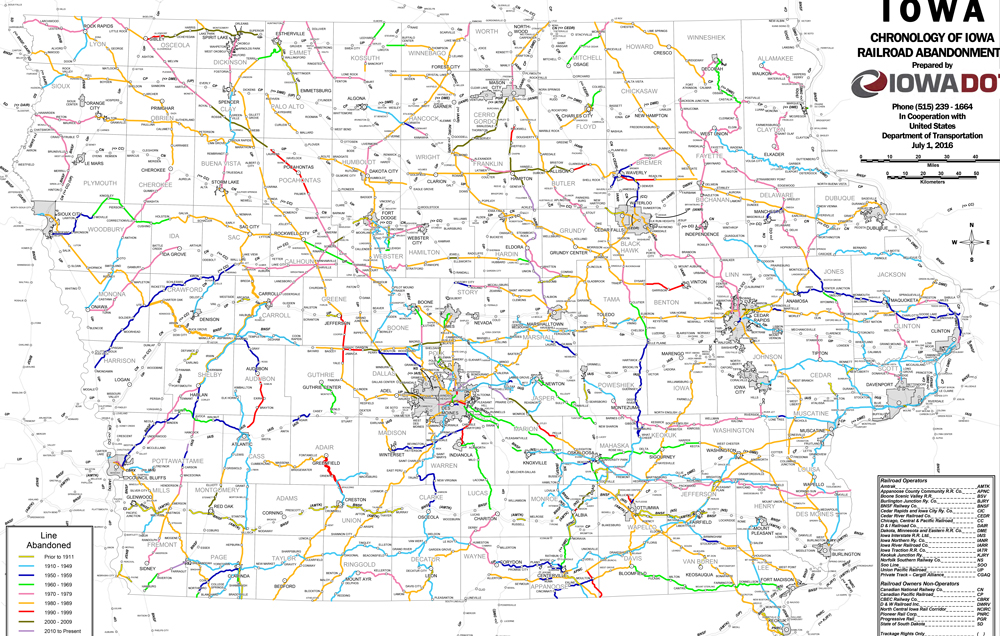

The private railroads shrink in physical size shown in a time-telling graph with a radical the rate of abandonment during the late 70s lasting through the early 90s.

Rail Serve

This period included a critical change by the Carter Presidency, deregulation of the freight rails through the Staggers Act. This action both saved the group financially, lowered costs for shippers and consumers, yet induced this cascade of damaging abandonments with transporters seeking only profitable ROWs. The unfortunate list of abandonments includes several types:

- Loss of double trackage, an essential element in both capacity and timely delivery or travel.

- From a 2010 Trains article : "Over the past 50 years, double-track mileage in the U.S. has shrunk, while the number of ton-miles has more than doubled."

- The article did also note massive investment in additional trackage by the BNSF and UP primarily in the west.

- From a 2010 Trains article : "Over the past 50 years, double-track mileage in the U.S. has shrunk, while the number of ton-miles has more than doubled."

- Abandonment or downgrading of multitudes of critical alternative routing exampled by:

- Ex-PRR mainline Chicago to Pittsburg.

- Ex-MoPac line across KS and CO onto the D&RGW line over Tennessee Pass from Kansas City into eastern Utah.

- Loss of a multitude of possible cross connections for emergency rerouting exampled by:

- Twin Falls, Id to Elko, NV. (An old single track UP branch line).

- Loss of multitudes of branch lines exampled by:

- Iowa and similar agricultural states were particular hit hard.

- Multiple scenic routes such as St. Anthony to Yellowstone.

{kind=link}

The draconian purposeful loss of ROW came during periods of continued significant growth .

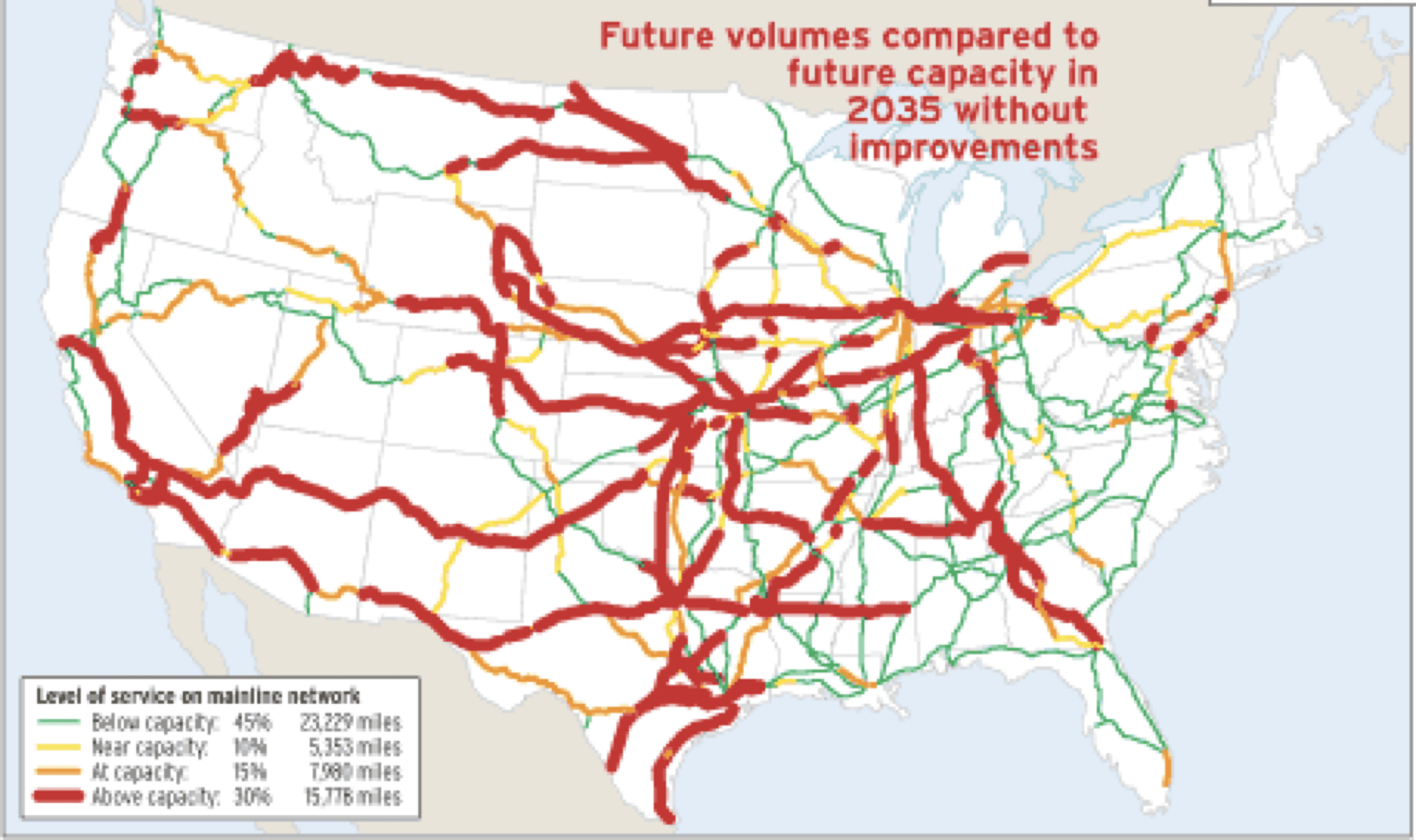

Rail Serve

Again, from Trains Magazine , we included a map predicting regions of over-capacity by 2035. This map, generated twelve years ago, is certainly dated, yet still offers an important view. For example, the mostly single trackage, shown in green, between Birmingham, AL and New Orleans, LA suffers precipitously with major capacity issues.

{kind=link}

Put in bold and distinctive words in a 2023 article from BCG ,

- "Following years of underinvestment, however, most national rail networks are already overused-meaning that the demand for existing infrastructure capacity, either for carrying trains or for maintenance work, exceeds supply. The result: poor punctuality and reduced customer satisfaction. For many train operators, such issues come on top of the growing challenge of securing sufficient rolling-stock capacity."

In our view, the needed capital is massive. For example, unrealistically costing the approximate 2500 miles for a third track along the entire old Santa Fe's Transcon as a siding from Chicago to Los Angles, still yields costs more than $5B.

A drastic physical transformation coupled with expected increased business foretells a future of compressed capacity and great operational risk without funding similar in size to the transcontinentals.

Determiners & Competition

Railroads operated in an almost perfect monopoly for nearly 100 years. In time, competition from air and truck/auto cramped the market. In times of low energy costs, the competition, truck/auto/air, shine. But energy isn't always cheap. Thus, reviewing a few comparative facts opens the door into a different vision. On energy, load bearing, land consumption and costs a multitude of give and takes exist. Each plays a role in determining viable options. In real applications, the comparisons are more complicated, but purposely we tried to highlight a or the driving characteristic. A table summary follows.

| The Comparisons |

| Construction Cost (IS per mile) |

| Energy Consumption (Ton miles/gallon) |

| Load Bearing *** |

| Land Consumption (Acres) |

| Auto/Truck |

| $4-12 Million (2016) * |

| 10-150 |

| Limited to tire contact **** |

| 1.5 Million ***** |

| Air |

| Airports See below. |

| Priority Freight Only |

| N/A |

| 3.1 Million |

| Rail |

| $1-2 Million ** |

| >500 |

| 400 sq. ft. |

| <<700,000 # |

* Unclear whether eminent domain costs were included.

** Expansion cost per mile for freight rail. Brightline completed a high-speed rail line including land, maintenance structures, and train stations at a cost of $25 million per mile. Kansas City Southern completed its Rosenburg to Victoria on an abandoned ROW (without track, tie and ballast) for $1 million per mile.

*** Concept of load bearing equates to the lateral spreading of weight across a surface. For rail, it's the area of the tie across the length of a car (Approx. 60 and 10" by 100"). For trucks, it's the tire surface area contacting the road.

**** A four-wheeled car contacts at a limited area of 100 sq. in.. Truck data was not found, but is relatively limited.

***** The interstate highway by specification is approximately 200 ft. wide from fence to fence. With approximately 50,000 miles, the system consumes a minimum of approximately 1.5 million acres.

# Class I trackage shown above equals 100,000 miles. Double track consumes approximately 50 ft., triple equals approximately 70 ft. equaling about 7 acres per mile. The total consumed equals approximately 700,000 acres. Note: most of the US is single track. This purposefully excludes yards, other miscellaneous entities and actual ownership (It is about estimating actual consumed for use).

We fully recognize that the above considers new construction and that expansion and repairs have differing factors. What is important is that when considering new opportunities or major repairs with the existing paradigm shifts, the rough concepts offer clear rule-of-thumb guidance. But the advantage for rail to carry heavier loads using considerably less energy, can't be overstated.

Continuing, a table shown next outlines expenditures for highways, railroads and airports.

| Expenditures (Billion) |

| Private |

| State |

| Fed |

| Total |

| Highways |

| < $200 |

| $50 |

| $200 + |

| Airports |

| Something |

| $30 |

| $30 ++ |

| Rail |

| $25 * |

| Minor |

| $1.3 |

| > $25 |

* 40 year yearly average.

Clearly, investment in rail even with its strong competitive advantages, lags significantly.

In addition, freight rail, on average, is three to four times more fuel-efficient than trucks with a single freight train can replace several hundred trucks.

Market Driving Trends

With comparisons in tow, now enters change, that ever-present constant. Among a multitude of the possible, two or more systemic shifts approach. First, drastic increases in jet fuel demand will fuel massive higher prices . This will also spread into diesel. A slide estimating future demand follows.

IATA

This critical air travel factor, fuel, becoming more expensive, perhaps four to eight times higher, will drive air travel cost significantly higher. In today's environment, fuel costs equal approximately 30% of the ticket price. This will be a paradigm shift. Again, this type of change isn't reserved just to passengers but will hit freight through increases coming through the capacity-driven need for renewable diesel. We could write about demand and the availability of fossil resources, but this comment suffices. The likelihood for fossil sources to carry the entire load doesn't exist, if the EIA is correct.

A second systemic change, increased viability for specialization through increased demand continues. This natural law appears often and across all businesses. A prime example was the long-time contentious battle between Apple's ( AAPL ) culture of developing highly specialized products vs. Intel's ( INTC ) drive to cheaply create a one solution fits all. In the early period with lower volumes, Intel reigned. With changes in technology coupled with budding volumes, Apple jettisoned into the lead. The same principle applies with transportation.

A sampling of America's geographical and social landscape illustrates the next shift. A glaring example follows:

| Population ((K)) |

| Demographics of Cleveland - Wikipedia |

| Phoenix* |

| 1940 |

| 875 |

| 65 |

| 1980 |

| 575 |

| 800 |

| 2000 |

| 475 |

| 1300 |

| 2020 |

| 375 |

| 1500 |

The advent of compressed air conditioning in the 60s played an enabling role. Drastic divisions in political ideology now influences a second. This structural change forces reallocation of assets.

Continuing, with the higher projected fuel costs coupled with geopolitical tensions, a return in American manufacturing naturally accompanies. Local manufacturing drives a different freight networking strategy from the now vision of picking up massive volumes at ports and transport for as long as possible. This will:

- Significantly increase the necessity and viability for smaller unit volumes increasing necessity in classification yard approaches.

Finally, on growth, "The Federal Highway Administration forecasts that total U.S. freight movements will rise 30%" over the next fifteen years. With the above systemic changes, we wonder if this is low-balled .

A Bitter Tiff & Common Needs

Thus far, our discussion centered completely with freight. Excluding passenger mispresents the truer picture. An interest in passenger rail surged in recent years. Some believe it is essential in managing climate change. We aren't so certain. But even outside of the climate belief, coming changes enable major expansion for passenger rail. With this in mind, at least two common themes merge: ensuring the legal ability to reclaim abandoned ROWs and gaining significant government aid for adding capacity. A good example for reclaiming abandoned ROW is the Spokane, Portland & Seattle's Pasco, at least through Hooper, WA main.

With respect to synergy between freight and passenger, the Investment in Infrastructure Act allocated $100B for passenger rail. Would wise freight management seek common grounds to enhance its infrastructure? Thus far, unfortunately, the answer seems an exclamation, NO, with the bitter tiff existing between majors and Amtrak outlined in our, For All Rail Freight, Amtrak's Fight With The Union Pacific Signals More Change.

Investors Take Away

For the long-term investor, watching for a laundry list of acceptance and patterning by management will be helpful. Our list includes:

- Willingness to invest synergistically with the passenger rail organizations.

- Develop long-term strategies which wisely increase the blending of truck with rail, i.e., Norfolk Southern's growing relationship with J.B. Hunt ( JBHT ).

- Long-term strategies for transporting smaller unit sized car loadings. (An opportunity now mostly forgotten).

Of note: we like Norfolk Southern's vision. It encompasses advantageous actions embracing future trends including:

- Designing and building strategically located transfer points, not just at ports (Intermodal).

- Increasing track capacities designed for competitive delivery times.

- Hiring practices designed for keeping employees especially the blue collar.

What we didn't observe with Norfolk is a vision for the natural progression toward smaller unit rail-only shipping. In time, an increased viable market size will likely occur. (The majors might approach this through granting trackage rights to new or existing short lines with their natural operational flexibility).

Risks

In our view, the major risk with railroads is the railroads themselves.

"Put another way, the fact that the overall freight transportation "pie" might grow in the years ahead does not mean railroads are guaranteed a larger slice of that pie. Railroads will have to earn it by making significant additional investments in infrastructure, equipment, and new technologies and by providing freight transportation services more safely, reliably and cost effectively than competitors."

We couldn't agree more. During the steady flowing shifts, the signs, enabling change, might be missed without careful attention coupled with the unfortunate short-term thinking.

Others might dream of a differing vision, one driven by cheaper fuel alternatives. On this issue, investors must recognize the massive investment required and with it time and non-existent viable technology. Personally, we can't envision any significant penetration in the timeframe considered.

Again, in our view, freight rails must put the fire out with passenger entities followed by smartly and willingly joining together, i.e. Union Pacific's, the State of Illinois', Amtrak's and the Federal Government's Illinois trackage upgrade project, being a prime example.

Wise investing requires careful observations. Although this article isn't intended to focus on any one company, Norfolk Southern's vision seems leading in spite of its recent struggles. The future could be bright very bright for freight rail heading forward. The forest is now rich with younger trees ready for growth. The railroad harvest can grow especially if it chooses to put out fires and embrace synergic relationships. Majors, which chose to do so, are likely to be the more lucrative long-term investments.

For further details see:

Significant Changes Might Greatly Alter America's Rail Transportation System