SFFYF - Signify: The Past And The Future Of Lighting A Sound Portfolio Investment

2023-11-02 05:19:30 ET

Summary

- Signify N.V. is a well-known producer of LED and technological lights under various brands.

- The company has a strong brand name, financial health, and a reputation for innovation.

- Despite struggles with competition and economic cycles, Signify N.V. stock could be a good investment opportunity.

Signify N.V. ( SFFYF ) is a well-known producer of LED and more technological lights under the Philips, Philips Hue, Interact, Philips Dynalite, Color Kinetics, Wiz, and several more. The company has constantly been pioneering better, cozier, more efficient lighting solutions that benefit people's lives and the planet. A spin-off of Royal Philips ( PHG ) that changed its name from Philips Lighting N.V. to Signify NV in 2018. This well-established business commands a strong brand name, financial health, historical reputation of innovator, and seven-billion euros yearly sales. Still, it struggles to grow for different reasons, including competition and economic cycles. Yet, it could be a good investment, and we definitely owe it an investigation.

What The Company Does And Why We Love It

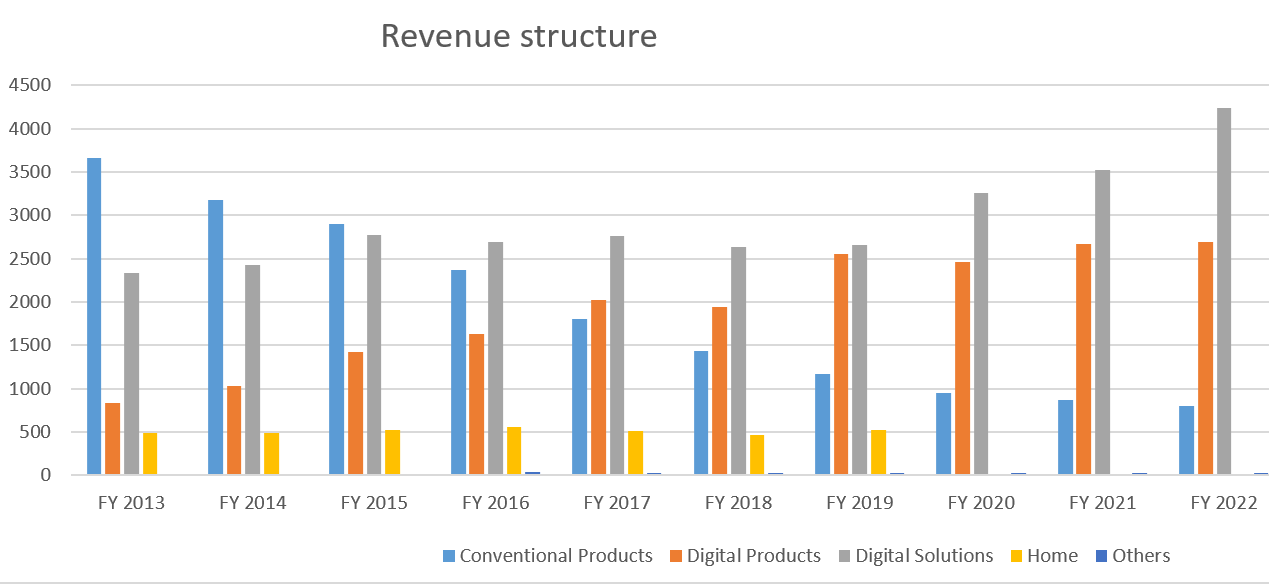

The business is divided into two and a half distinct segments:

- Digital Solutions (usually 50+% of Sales)

- Digital Products (about 35+% of Sales)

- Conventional Products (10+% of Sales)

The first two are slowly progressing, while the latter is being dissolved in history.

Revenue structure (Tikr.com, Author)

{kind=link}

Digital solutions mean lights, connection equipment, and overall systems for professional clients, such as offices, commercial buildings, shops, hospitality venues, industry, agriculture and outdoor environments, and even cities. A few headlines for the segment from the company FY2022 report tell the story: "Upgraded lighting solutions in all 69 Everlast Gyms across the UK", "Supplied horticultural lighting to Iceland's first vertical farm," "Installed solar lighting in the Algarve."

Digital products segment is a wholesale channel to sell lamps: spots, bulbs, and tubes. The company states in its Annual report for 2022 that according to internal research, it believes that Signify was the number one in sales in the global LED lamps and electronics market in 2022 . I must add here that the market is fragmented and saturated with competition, disabling that "number one" spot being a moat. The most known to a broad public and fresh products are Philips Hue and Wiz lights that add security or connectivity features to lamps.

Conventional Products segment sells non-LED lamps: HID, TL, compact fluorescent, halogen, incandescent, and lamp electronics.

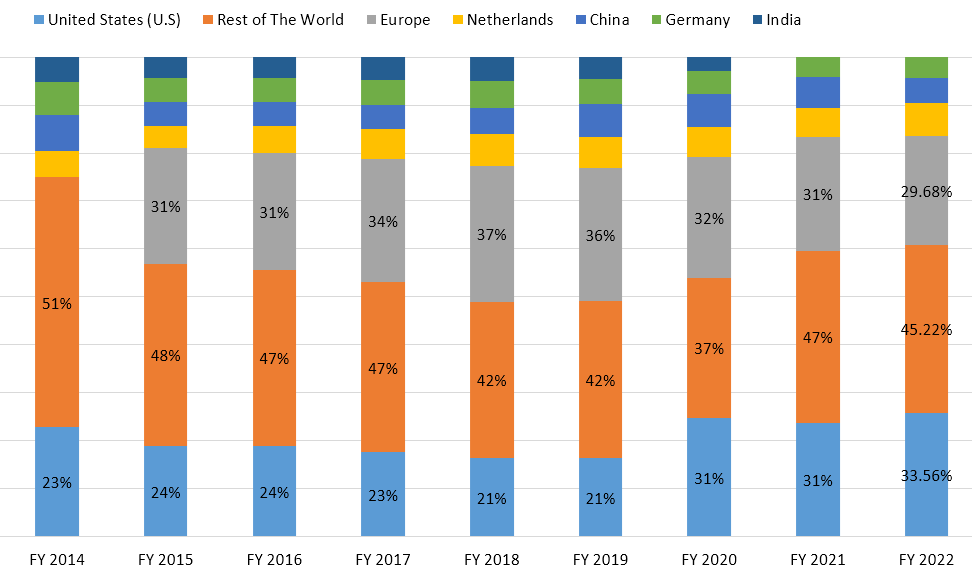

Geography of sales (Company reports, Author)

{kind=link}

So, what makes us love the company? Subjectively enough, but I grew up buying and using Philips lamps, all sorts of them, starting from home appliances and ending with bulbs H7 for my car. The brand has always summoned a connotation with innovation in my mind. I remember many years ago, maybe 20 or so, Philips Electronics was the first company to decorate their entire building exterior in New York with a myriad of tiny LEDs, which was highly innovative back in the day. Philips' scientists were the first to replace a 60W lamp with LED, which was also the most energy-efficient one. That brand image is still there; Signify offers breath-taking new ideas to illuminate and connect, like lamps+WiFi, or lamps+security cameras, lamps in the grand scheme of things of IoT, lights for cities, for agriculture, and points of sale, or lights to lift our moods by Philips Hue. As price action and Sales say, something needs to be tackled, but we discuss it later; nobody is perfect.

The Lamp Company Could Have Beamed Brighter

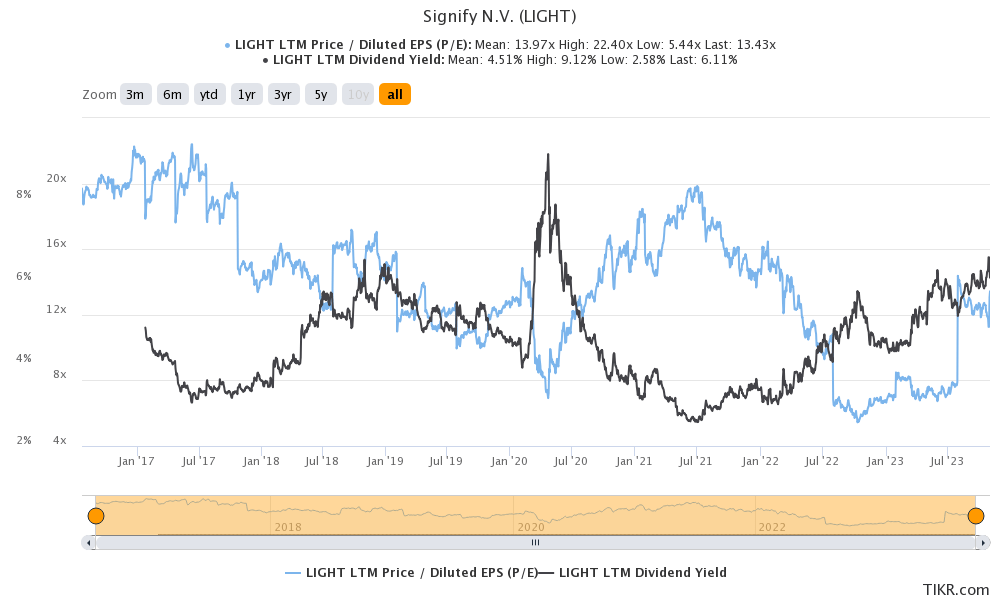

The stock trades at Euronext Amsterdam under an entirely original ticker (LIGHT) in EUR; I find it played in style. But on the following chart, you see prices in USD. After the Pandemic market bubble busted, stock gradually lost more than 50% of its value, bringing its Price-to-earnings ratio down to 5+ level, which was scandalous, before it became apparent that the business lost some sales and its EPS declined too. Presently, PE stands at 12.5, and its EUR-dividend yield is 4%, which is excellent.

The eye-catching and poetic article Signify: A 'Melting Ice Cube' Worth Considering puts the business into the 'Melting ice cube'- category but argues that the management gracefully steers through that phase. I concur. One of the company's constraints is that it doesn't always show a clear trend indicating sales growth. Seven and a half years have passed since 2015, but only once sales re-tested the 7.5 billion EUR mark. Conversely, operating income grew by 65%, points to Signify.

Income Statement's basic metrics (TIkr.com, Author)

{kind=link}

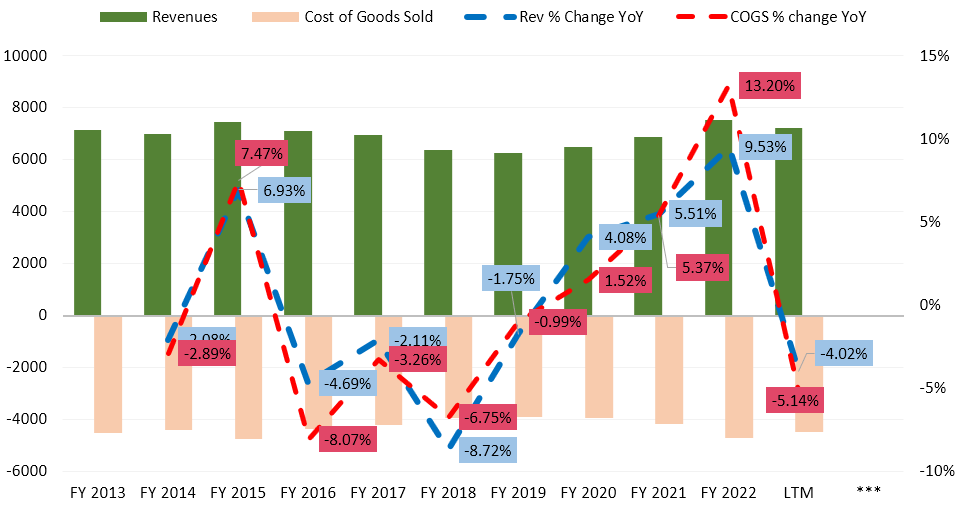

The business sure is cyclical; the soft landing occurred only in 2019, after four years of low single-digit sales decline, except for 2018, when it fell by 8.72%. The three-year recovery streak culminated with 9.5% growth in 2022 is seems to be over; Sales are now expected to subside at a single-digit pace in 2023. Again. Would 2023 be just an odd year or a one in a few?

The thing investors don't like about the stock is, which is pretty superficial in my opinion, that except for the dividend history, the company lost six years; it just slightly toppled the sales line of 2015, whereas the global economy changed approximately by one-third towards 100+ billion USD in 2022. The following picture is frankly not a jaw-dropping one.

Sales and COGS dynamics (TIkr.com, Author)

{kind=link}

However, it took 4.73 billion EUR of costs to make 7.46 in sales in 2015; fast-forward seven years, and Signify used the same 4.7 billion to deliver 7.51 billion. Recall the inflation story since 2021 and be impressed by the smoothness of handling costs in an equipment company. Here is the EU Producer price index for the sake of context.

European Union Producer Prices Change (Trading Economics)

{kind=link}

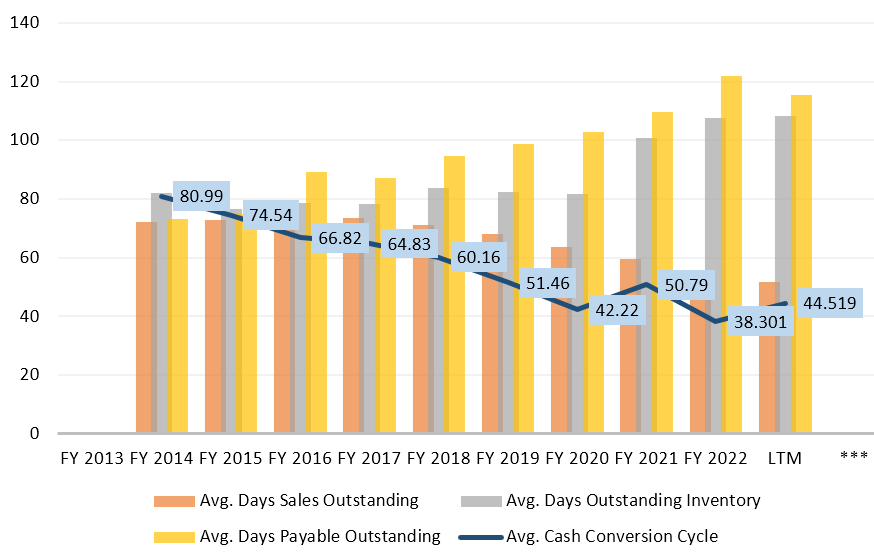

The hard-to-achieve feature is to keep the cash conversion cycle steady without deterioration, but what can be said about an international company that has been able to keep improving this metric? Perfect. However, the devil is in the details: Signify was able to squeeze a better deal for itself by simply paying even slower to suppliers (accounts payable) than already slowed enough purchasers (accounts receivable). The company itself couldn't work through better Inventory and accounts receivable management. Not so perfect after all, see the chart below.

cash conversion cycle (Tikr.com, Author)

{kind=link}

Another arguable change is that LIGHT's interest expense jumped from 46 and 40 million in 2019 and 2022 to 51 and 107 in 2022 and LTM (1H2023), respectively. Given current interest rates, that is going to hurt the business during the rest of the year and 2024 optimistically.

The cash level is currently at the lowest point in history after the IPO, sitting at EUR584 million or 8% of assets, but just a few years ago, the company had it between 850 and 1,000 million. Cash burn since the peak in 2020 is dancing between 170 and 200+ million EUR a year, rendering the cash pillow thin. The management will likely increase debt in 2024 to stabilize cash, but that would happen in a higher interest rate environment.

Cash and STI level (Tikr.com, Author)

{kind=link}

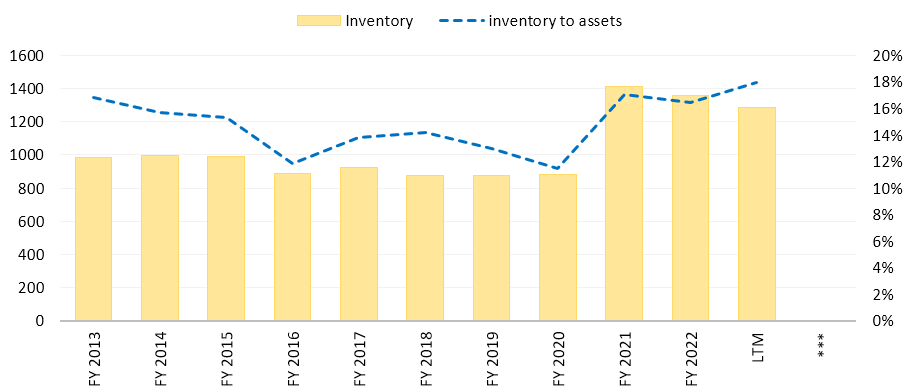

Inventories appear to be elevated, which isn't good, however, I believe that was caused by acquiring Cooper Lighting in 2020.

Inventory level (Tikr.com, Author)

{kind=link}

Debt to assets at the current 28.5% looks elevated, especially in light of the 12-m Euribor at 4.184%. Full-year 2022 Annual report of the Signify NV :

As of December 31, 2022, the company had outstanding long-term loans amounting to EUR 280 million maturing in November 2024 and USD 225 million maturing in January 2025. In addition, the undrawn revolving credit facility ((RCF)) of EUR 500 million is maturing in January 2027. As of December 31, 2022, Signify had outstanding EUR 675 million of fixed rate notes due in May 2024 with an annual coupon of 2.000% and EUR 600 million of fixed rate notes due in May 2027 with an annual coupon of 2.375%.

The company must re-finance at least 880 million EUR at a 4.5+% rate in 2024. Interest expense has already jumped from 51 to 107 million for 12LTM.

{kind=link}

Lastly, the business has a heavy Goodwill, currently at 38.9% of assets, with a historical average of 29%. With all due respect to R&D efforts, client relationships, and other things of all acquired companies, lighting equipment solutions are a bit short of being rocket science. Eventually, they must impair the Goodwill.

Here Is Where The Lamp Shines Right

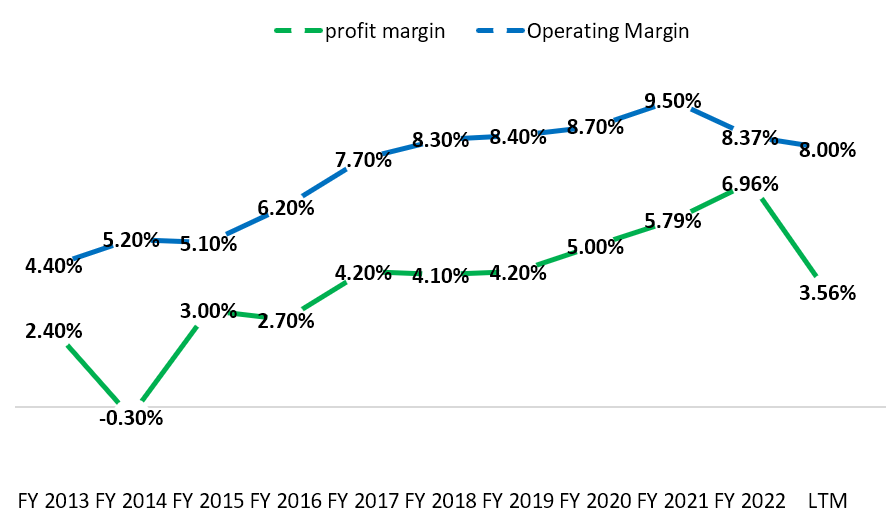

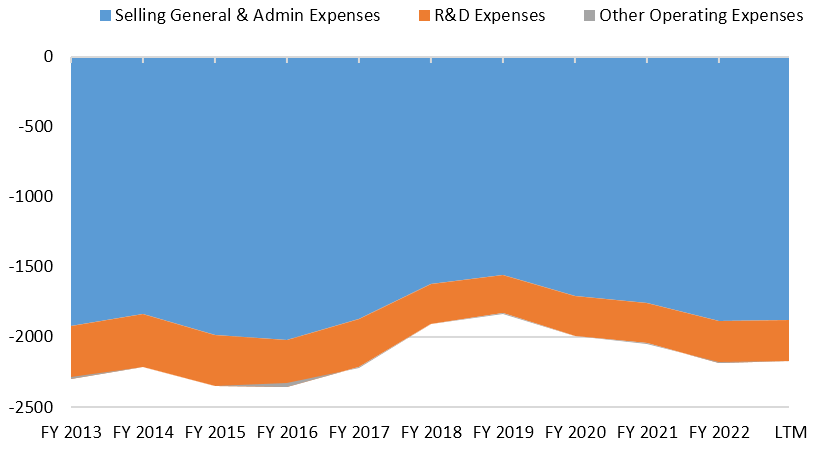

The company managed to keep its gross margin within 36-40% over ten years, which is impressive, given that equipment producers/manufacturers tend to lose here over time. What is truly impressive is that the operating margin was improved twice, from 4.5% to 9%. They slashed 290-350 million from Selling General & Admin. Expenses during 2017-2021 and also freed 50 million at R&D side.

Margins (TIkr.com, Author) Expenses structure (TIkr.com, Author)

{kind=link}

{kind=link}

CapEx, compared to gross profit, keeps a low profile, which is okay for the time being, however, they might increase it in the future to ramp up facilities, improve productivity, or just to stay relevant. Because CapEx below 100 million euros a year for a 7+ billion business is just too good to be true.

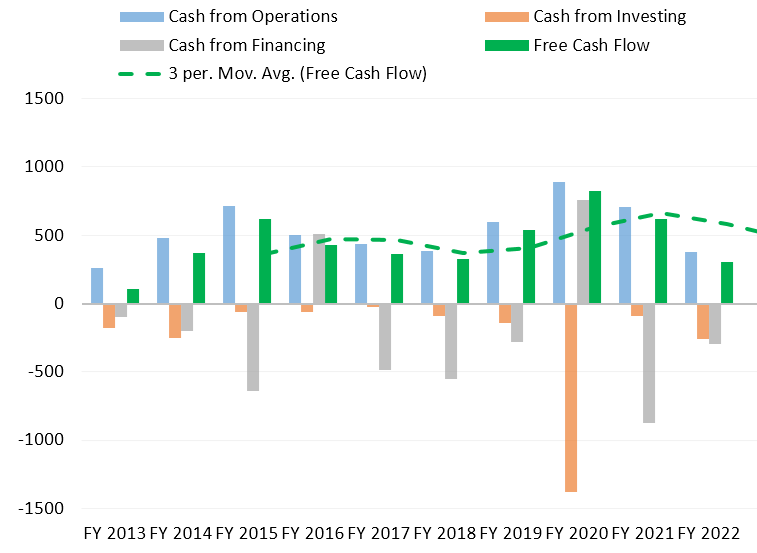

The business is generating stable positive cash flows, even at unstable and stumbling revenue dynamics, the historical average of the FCF-margin is 6.6%, and the CFO-margin's average is 7.8%. Three-year average FCF's CAGR rate was 12.7% in 2022 and 21% in 2021, which is quite remarkable; the business has succeeded in squeezing more juice for shareholders out of the same amount of fruits. Please, inspect the chart below.

{kind=link}

Let's Turn On More Lights

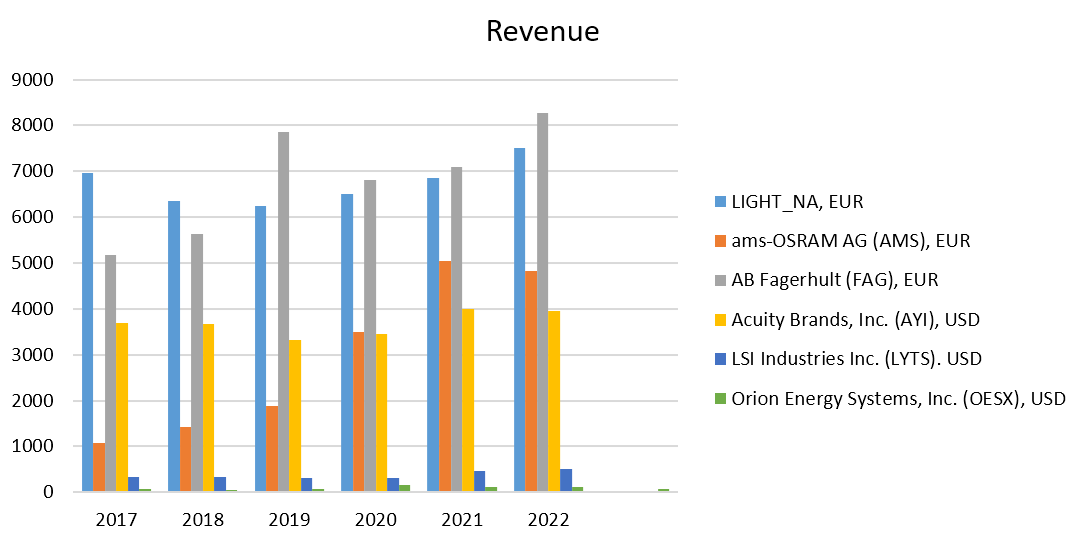

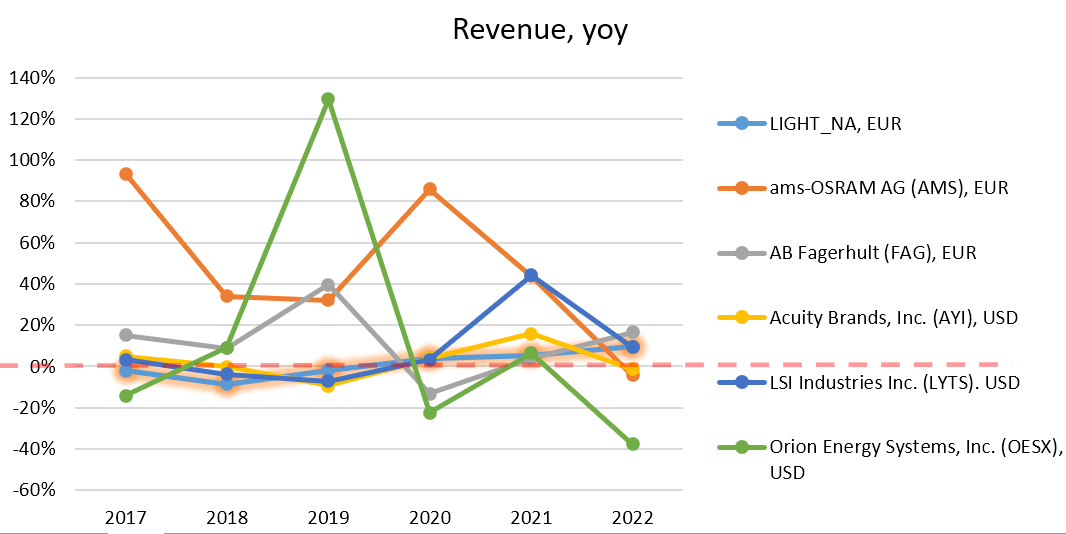

According to my data, Signify is the second largest player in the field, slightly after AB Fagerhult (FAG), whose revenue in 2022 was 8.29 billion EUR. However, for 2016-2022 AB Fagerhult grew double-digits, except for 2020 and 2019. In 2019, sales grew by 39%, presumably due to some M&A activities, which was not a product of organic growth. Debt to assets for FAG is 10+% higher than for LIGHT, but that's not that big of a difference.

Peers sales (Tikr.com, Author) Peers sales, YoY (Tikr.com, Author)

{kind=link}

{kind=link}

Signify NV and Acuity Brands, Inc. AYI are the two most profitable businesses with the highest operating margins. AYI's operating margin is at the top, averaging 4% higher than LIGHT's. At the per share data, Signify is a clear winner; its 3-year average EPS grew at a 5-y CAGR of 16.5%, way ahead of AYI with a 5.67% result. They are the only two who have a positive change in this period.

Peers diluted EPS (Tikr.com, Author)

{kind=link}

Investment thesis

Signify is a historical leader and pioneer in lighting solutions, formerly Philips Lighting. It develops and markets all sorts of lamps for indoor and outdoor lighting, no matter the scale of the project; its products illuminate cities, landmarks, and simple homes. It continues to innovate, offering lamps equipped with different contemporary functions and IOT. However, it lacks a growth driver despite several recent acquisitions. The company sales level topped the previous record of FY2015 just recently in FY2022, losing six years of history. Nevertheless, the company compensated it with better profits, significant growth in EPS, dividends, and a decrease in shares outstanding.

PE ratio and dividend yield (Tikr.com)

{kind=link}

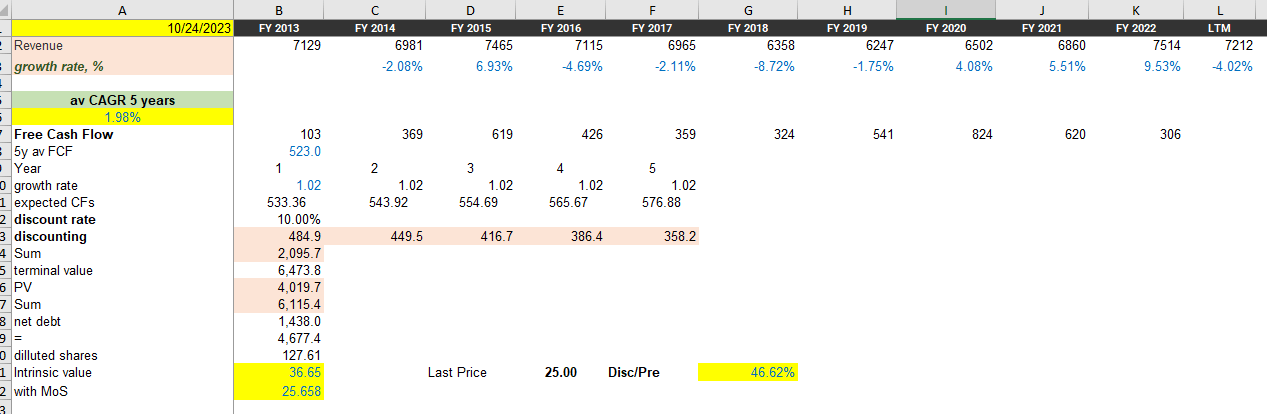

Valuation-wise, using my primitive DCF (5 years, 10% discount rate, EUR523m for the cash flow, 1% for Terminal value), we arrive at 36.6 EUR fair value, and with a 30% margin of safety (because I think a 10% discount rate is already too much), it would be reasonable to step in at 25 EUR per share. Currently, the price is between 24 and 25 EUR per share.

{kind=link}

Risk Factors

There is an obvious risk that the dynamics of Sales growth for the company won't recover in 2024. If that scenario materializes, the stock would easily crash another 30% down to 17-18 EUR per share,

The war in Europe and its burdens derailed and hurt one of Signify's primary market - Europe. And that could drag on for long.

In the long run, the acute price competition from Chinese companies occasionally takes away the bread & butter of all North American and European lighting solutions producers.

For further details see:

Signify: The Past And The Future Of Lighting, A Sound Portfolio Investment