SKFOF - Sika: A Brighter Outlook As MBCC Acquisition Draws To A Close

Summary

- Sika takes another step toward closing the MBCC acquisition.

- With valuations de-rated across the industry, the focus on inorganic growth makes sense.

- While 2023 could be a challenging year on the macro front, I think Sika has enough pricing power and secular tailwinds to outperform.

The investment case for Sika AG ( SXYAY ), a Swiss specialty chemicals company with operations spanning construction and industry, remains intact. Despite the stock price decline in 2022, Sika's pricing power continues to shine through due to a robust business model and product lineup built over the years. With few of its peers able to match this pricing power, I see Sika outperforming on earnings and potentially even gaining share amid a more challenging macro environment this year.

With the MBCC acquisition also clearing the UK regulator in recent weeks, the company is on track to unlock synergies from a highly complementary and EPS accretive integration. Going forward, news flow on the MBCC acquisition close offers a near-term upside catalyst. Over the mid to long term, further progress on its decarbonization efforts offers additional valuation support from increased ESG flows.

CMA's Approval Marks Another Step Towards Completing the MBCC Acquisition

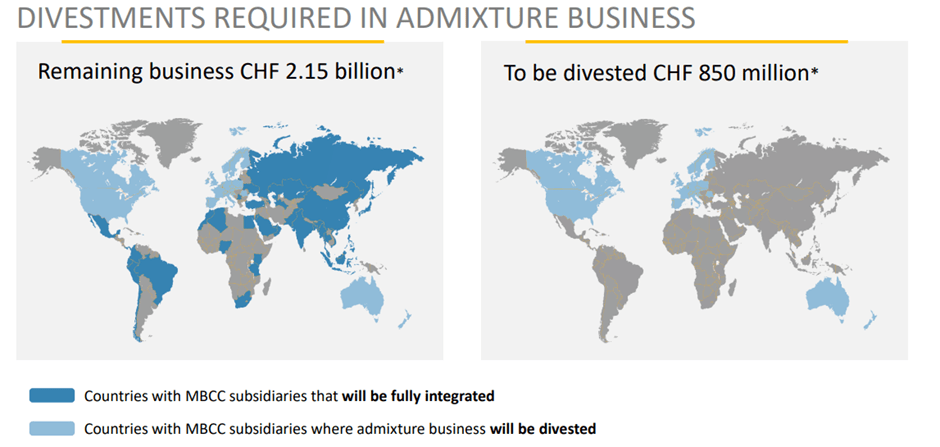

The UK's antitrust regulator, the Competition and Markets Authority ((CMA)) officially released its final report on the MBCC transaction, also approving the 'fast-track remedy' well ahead of the late January 2023 deadline. Recall that as part of its acquisition, Sika had proposed to divest MBCC's admixtures unit (~CHF0.9bn in FY21 sales) to a single buyer. The CMA report validates this proposal and prior commentary that there was a suitable purchaser in place, paving the way for the divestiture to be completed ahead of schedule.

While the divestment will result in Sika losing a sizeable chunk of the MBCC revenue base, pro-forma sales from MBCC of ~CHF2.2bn should still yield significant scale benefits. Thus, Sika's targeted run-rate synergies of CHF160-180m by FY25/FY26 remain intact, along with the 2.5x leverage target in FY23. Assuming no further roadblocks, the transaction should close in H1 2023 at the latest.

{kind=link}

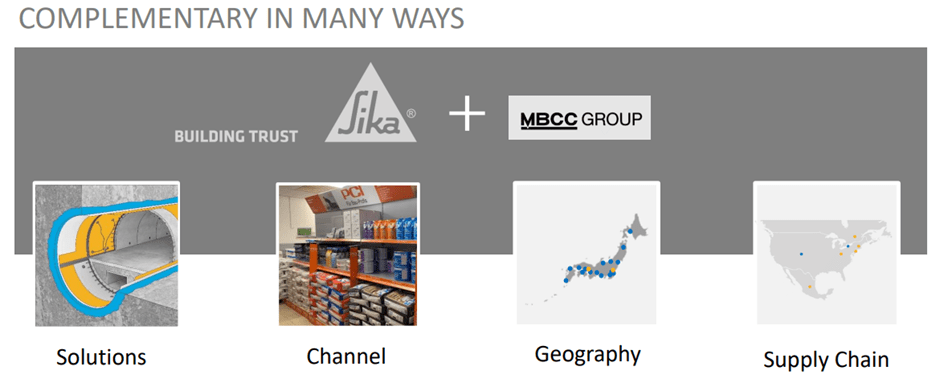

MBCC Acquisition Paves the Way for More Inorganic Growth

Importantly, the earlier-than-expected CMA approval significantly lowers the potential antitrust hurdles, representing a key step towards getting the acquisition closed by the H1 2023 target. From a strategic perspective, the MBCC acquisition fits nicely within the broader Sika M&A framework, supporting the case for an EPS accretive outcome. Of note, MBCC's product offering complements most of Sika's core technologies and end markets, while the overlap of production and distribution footprints also presents significant scale benefits post-integration. Thus, the closing of this transaction is a key near-term upside catalyst for the stock; over the mid to long-term, good execution on synergy realization should unlock incremental upside to the earnings growth algorithm as well.

{kind=link}

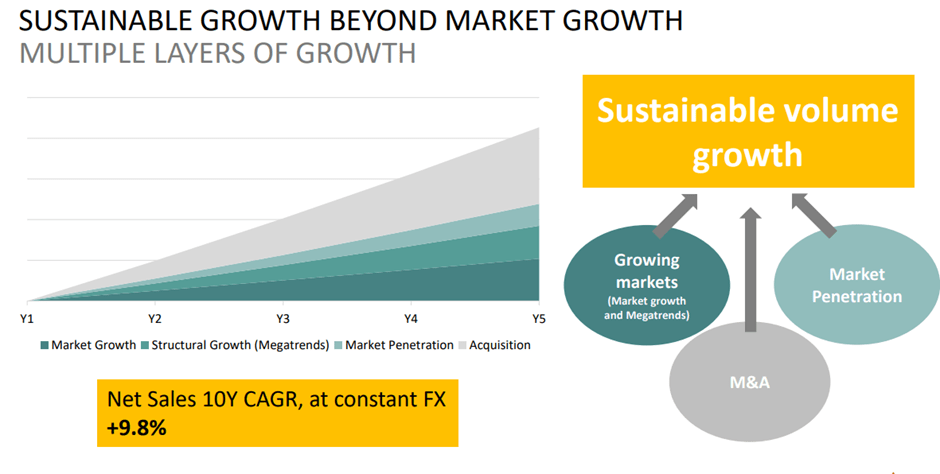

Going forward, expect a further extension of Sika's M&A strategy, having already acquired two companies in North America last year. The key difference lies in the size of future acquisitions – backed by a strong balance sheet and given the current low valuation backdrop, management's renewed focus on acquiring assets with >CHF1bn of sales could pay off. Thus far, it's hard to fault Sika's track record of combining organic and inorganic growth - over the last decade, sales growth has outpaced the industry at ~10% FX-neutral per year. So with management confident in extending the runway using this playbook, I feel comfortable underwriting more outperformance ahead.

{kind=link}

Leaning on Industry Tailwinds and Pricing Power to Protect Margins

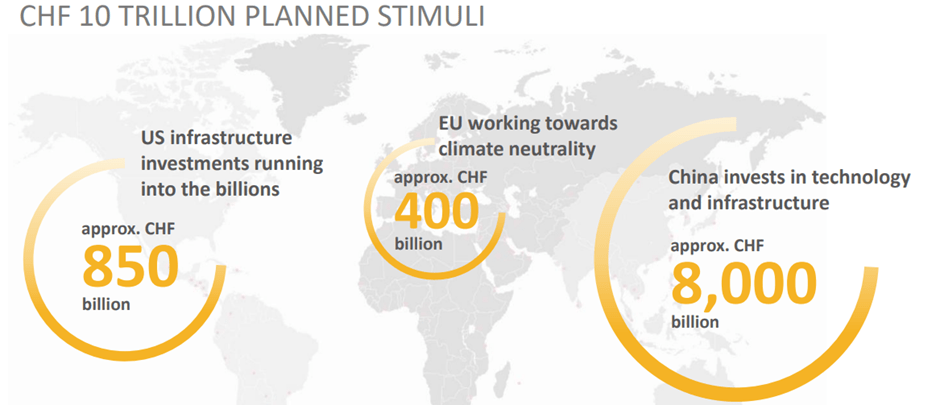

Despite weakening housing demand in the US, Sika noted it continues to see solid volumes in Q3. While housing will likely trend lower in 2023, Sika's robust pipeline of projects should still be supportive of positive volume growth, particularly with the 'Infrastructure Investment and Jobs Act' ramping up in the US. For context, the stimulus package calls for reauthorized surface transportation programs for five years and >$100bn of additional funding. Given the size of the package and the prospect of more stimulus ahead across the US (est ~CHR850bn), China (est ~CHF8tn), and the EU (est ~EUR400bn), Sika is well-positioned to benefit as more funding flows through.

{kind=link}

In the meantime, investor concerns are likely focused on the ongoing input cost inflation and the impact on Sika's profitability. While this has led to lower margins for its peers, Sika has bucked the trend; its pricing power has allowed it to raise prices by +15% last year and schedule further hikes for early 2023 as well. With raw materials price inflation also showing signs of easing amid plateauing commodity prices, I expect a gross margin inflection sooner rather than later from the FY22 trough. Over the mid to long term, Sika's digitization efforts via automation and process control should unlock incremental operational efficiencies, supporting the 15-18% margin guidance. Note that this guidance includes a base case MBCC integration scenario; given Sika's integration track record, for instance, in extracting ~CHF100m of synergies from Parex post-acquisition, there remains ample room for earnings upside, in my view.

A Brighter Outlook as MBCC Acquisition Draws to a Close

The near-term macro headwinds are material, but the investment case for Sika remains intact, in my view. As demonstrated in recent quarters, Sika has continued to maintain enough pricing power to protect margins, supported by a robust business model that should allow for a high-single-digit % sales growth algorithm through the cycles.

The acquisition of MBCC is also nearing its close, and given the complementary product lineup and production/distribution footprints, an EPS accretive outcome looks to be on the cards. Going forward, developments on the MBCC acquisition close offer a positive near-term catalyst, while positive ESG progress could provide valuation support through a potentially turbulent next few months.

For further details see:

Sika: A Brighter Outlook As MBCC Acquisition Draws To A Close