SXYAY - Sika: Not As Great As Some Believe But Quality And A 'Buy'

2023-08-03 10:54:24 ET

Summary

- Sika AG is a multinational specialty chemical company with over 110 years of history and operations in over 100 countries.

- The company is known for its stability and high-quality products, but its stock is trading at a premium compared to other chemical businesses.

- Sika benefits from global megatrends, such as the repair and refurbishment of older buildings and expansion into emerging markets like Southeast Asia.

Dear readers/followers,

For my article this week, I'm looking at Sika AG ( SXYAY ), a company that seems to be on some analysts' radar for the solid profitability of their operations. This is great news - because as you know, I too am looking at above-average profitability and strength in the companies I review and invest in. Sika has been on my radar for some time, as it happens.

However, I've never gone ahead and actually pulled the trigger on the company.

Why is that?

That's what I'll attempt to explain to you in this article. While the company is extremely qualitative and has a long-term convincing upside, it comes with a number of caveats that you should know prior to investing.

While the company is certainly attractive here, the simple fact is that I view other companies as substantially better investments at this particular time.

Let's look at this company and see what it does.

What is Sika AG?

Sika is Swiss, Sika is large, and Sika has been around for over 110 years. The company is a multinational specialty chemical/basic material company supplying infrastructure/construction and automotive/vehicle industries. The headquarters are in Baar, Switzerland. It's active in over 100 nations and has over 10B CHF in annual revenues.

The company is among the best-rated chemical businesses with an A-rating. It's also one of the lowest-yielding, at less than 1.2% dividend yield. However, it's also one of the most stable chemical businesses in the world, and it seems to go completely against the notion that "Chemical businesses are volatile".

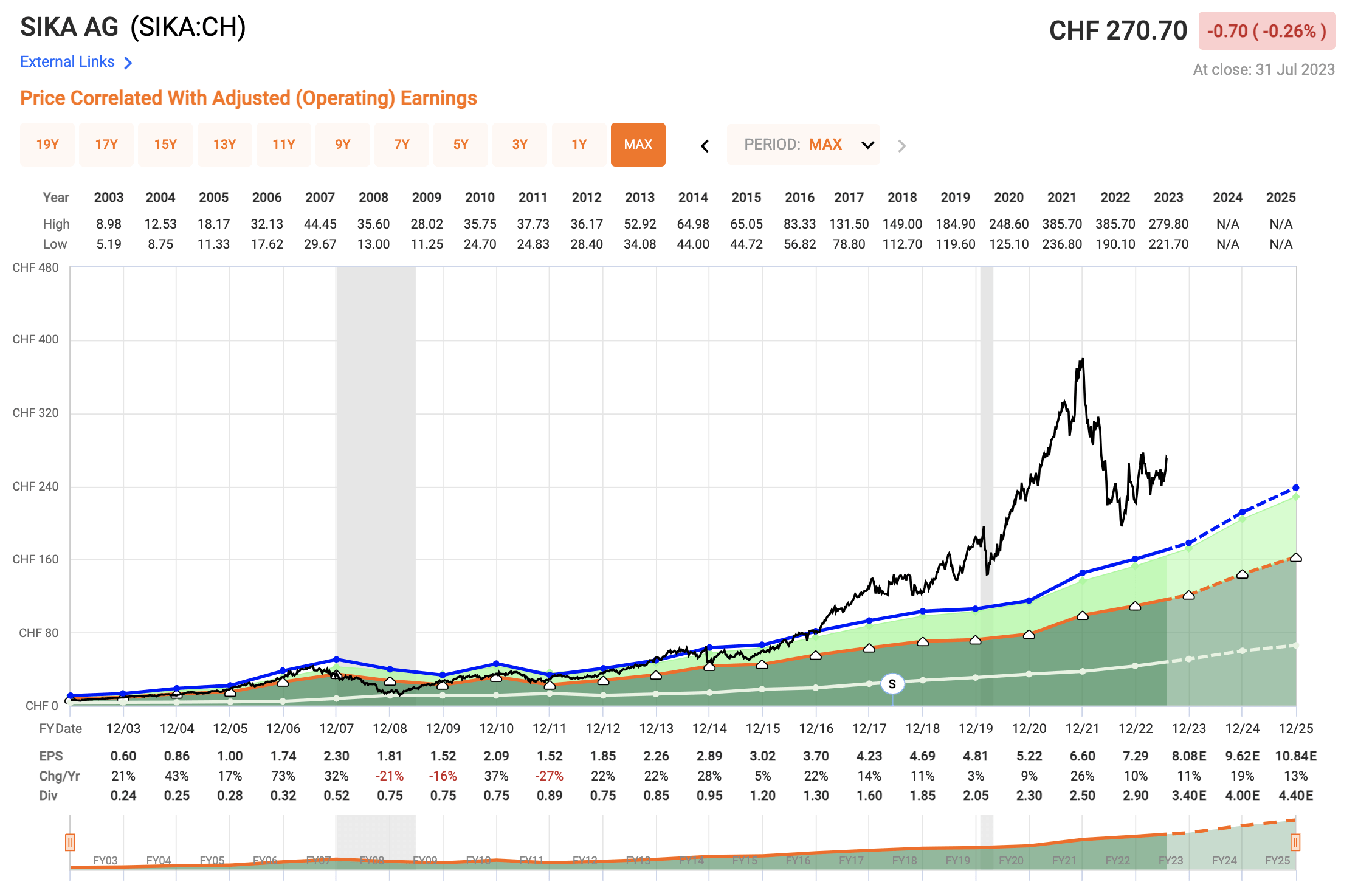

Sika earnings/valuation (F.A.S.T graphs)

{kind=link}

This chart illustrates extremely well both the advantages and the challenges of Sika. The stock is essentially telling the market that "Nope, despite my operating areas, I'm not going to be at all volatile, but you'll have to pay through the nose to get me".

The premium of almost 35x is almost 3x the valuation of a much higher-yielding, potentially qualitative chemical business elsewhere. What fascinated me when looking at Sika in the first place was how the company had/has managed this sort of operational stability despite being exposed to such volatile sectors.

While I don't have a perfect, explain-it-all-answer, I believe it lies close to the notion of product quality. The company's portfolio includes world leading bonding, sealing, damping, reinforcing, and protection brands, including things like Sikaflex, SikaTack, Sika ViscoCrete, SikaBond, Sikafloor, Sika CarboDur Sikagard, Sika MaxTack, Sikaplan, Sikament, and Sikadur. While I would say that my thumb is in the middle of my hand (a literal swedish translation of not being very much of a "handyman"), I've heard of and used Sika products. I would say the combination of reno/service markets makes up for the volatility in the otherwise volatile end markets the company is in.

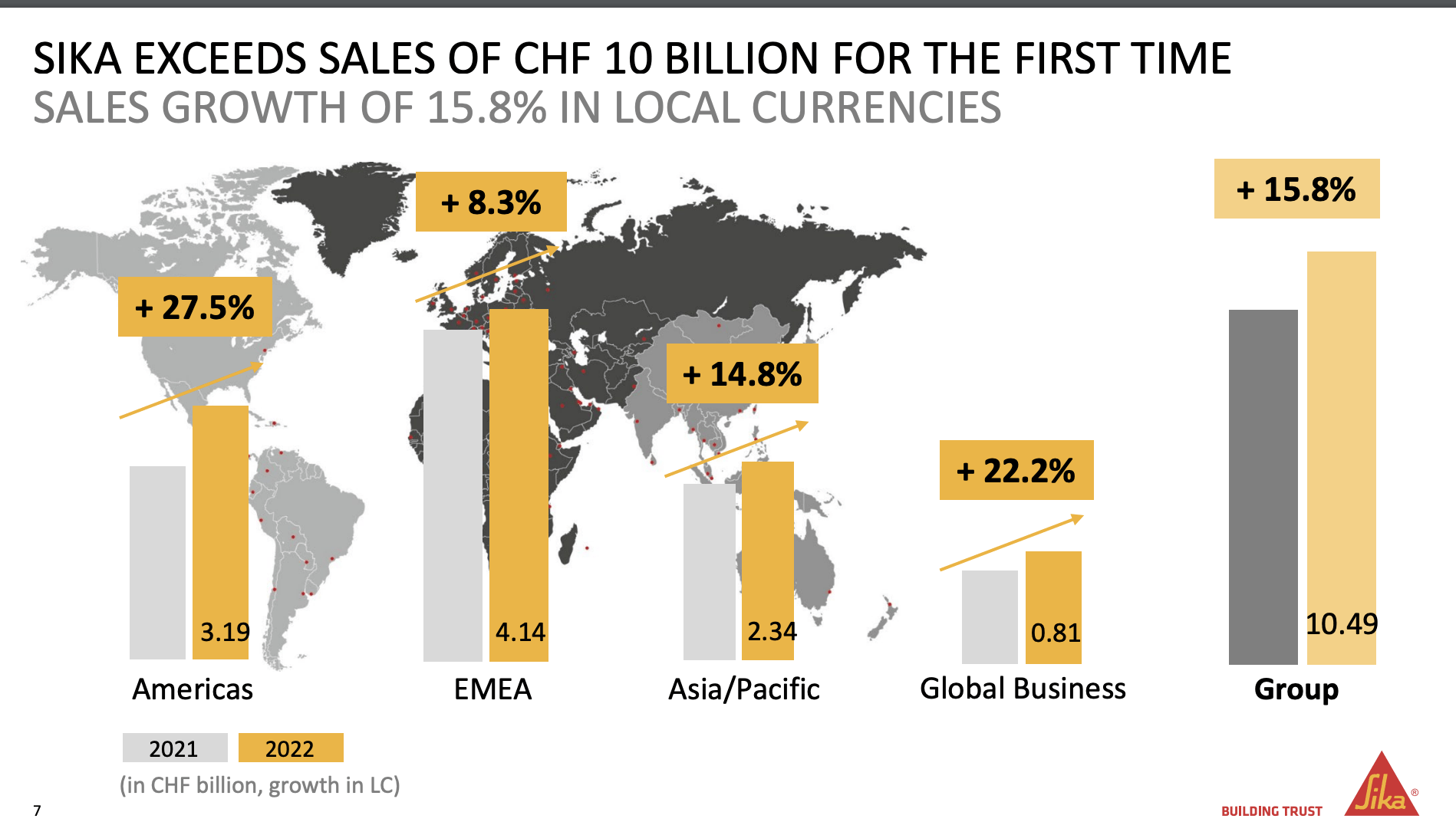

The company's sales growth confirms this overall picture.

{kind=link}

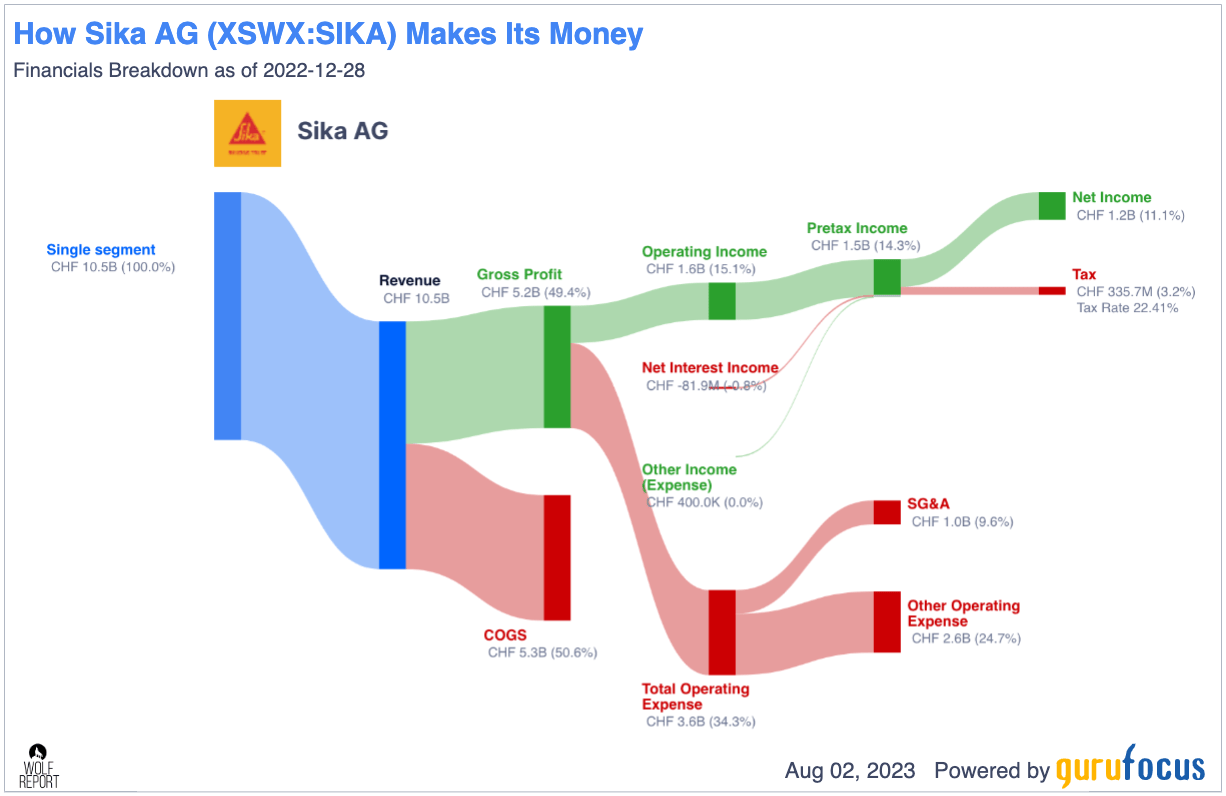

Net sales have grown steadily since 2017, the same with EBIT and EBIT margins. The company now manages a pre-tax margin of 15% and a net margin of over 10%. With a GM of almost 50%, the company is, on an implied basis, a very well-run industrial/chemical player with comparatively low COGS of below 51%, and SG&A of below 10%.

{kind=link}

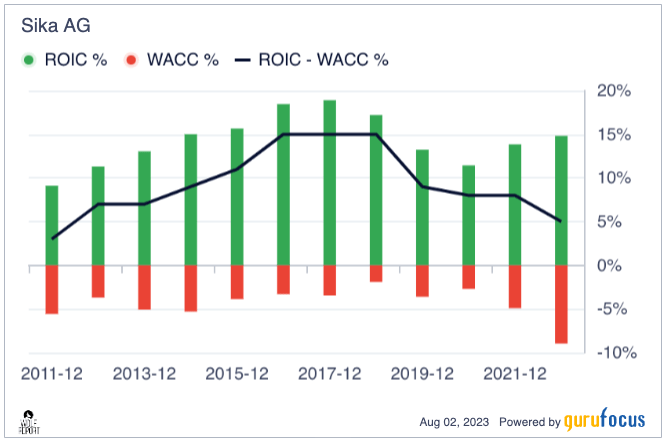

This is a very well-run company with low debt - Long-term debt is at less than 41%, and the market cap here is currently over 41B CHF despite the company correcting from what I can only describe as fantasy-type valuations. Recent investments have pushed the company's typically cash-heavy operations to where they have more debt on the books than usual, but not to any worrying degree, especially post-2022A results. The company's ROIC relative to its WACC is extremely good, even if in slight decline over the past few years as the costs of debt and capital have increased (and the company has issued a fair number of shares).

{kind=link}

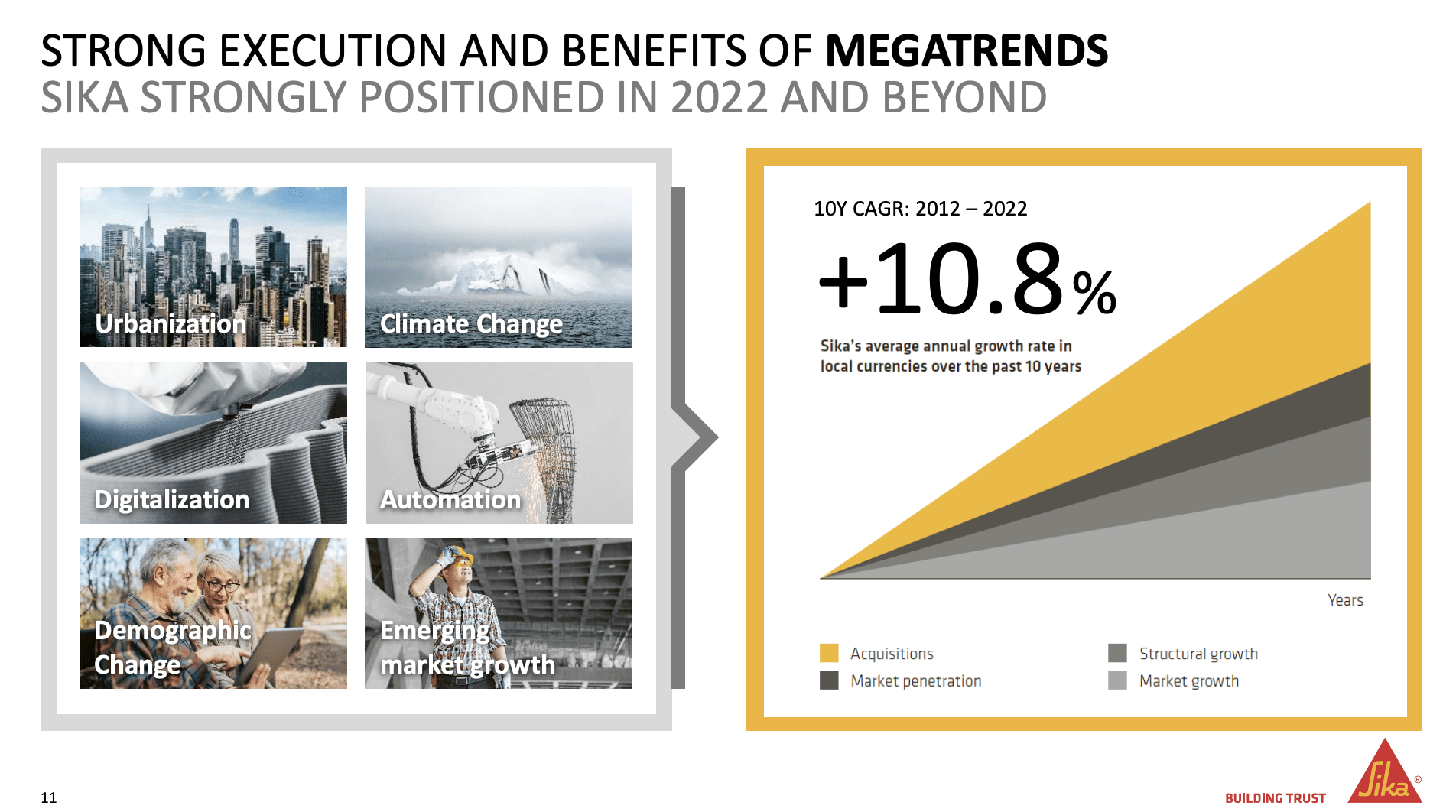

The latest full-year results detail extremely strong trends, but also reasons for why the underlying growth is not only likely to continue but to even grow larger. Much like other companies that benefit from the overall global megatrends, Sika AG is a net beneficiary of some of the overall global trends going forward.

{kind=link}

Sika has a relatively interesting exposure to the repair and refurbishment of older buildings in urban areas. Its products are used for upcycling, where most infrastructure companies won't see new sales due to 95% of existing core materials being preserved - but Sika specifically are seeing advantages because its products are being used for renovation. The company is also very active in new emerging markets, such as Southeast Asia, and is already in place with multiple new factories and assets, selling Sika products and expecting a market value of over 500B CHF in the next few years in terms of investment volume. That's why the area already has 8 national subsidiaries and 20 production plants in nations like Thailand, Cambodia, Vietnam, Malaysia, Myanmar, Indonesia, and other areas.

{kind=link}

Sika is growing both organically and inorganically. The recent successful M&A with the MBCC Group adds both solutions, US-based supply chains and interesting geography to the company's portfolio. MBCC generates over 2B CHF worth of sales, and synergies are expected to reduce costs by over 160M CHF by 2026. Integration is already ongoing, and the company fully expects to break the 12B CHF sales barrier by 2023E.

Continued earnings growth on an adjusted basis is around 6-8% expected in local currencies, though this is ex-MBCC M&A. On a high level, the company has a very interesting and well-diversified sales mix, around 39.5% EMEA, 30% Americas and 22.3% APAC, set to grow.

Insider buying/selling is very rare - hasn't happened for years. No significant institutional investors are buying shares here except a few funds.

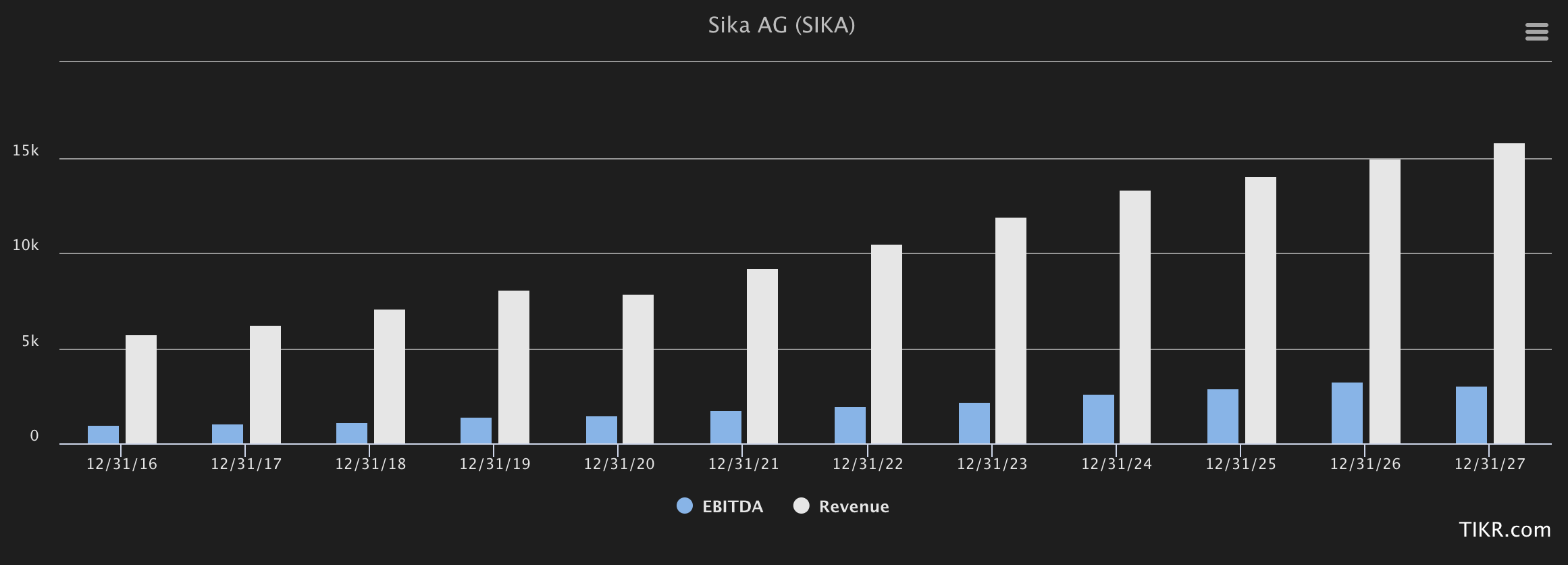

The biggest challenge, if you want to invest in Sika AG, is that you have to reconcile the company's high valuation with your expectations. Sika is, without a doubt, expected to grow. Here are the company's current revenue and EBITDA expectations on a forward basis. I also view these growth estimates as realistic - or at least, I can't find any clear flaw with the underlying assumptions beyond the typical argument of "APAC/Southeast Asia is volatile". Yes, it's volatile. But if you have the right sort of assumptions and expectations and are willing to hold the company for some time, then you should see earnings materialize.

Sika Revenue/EBITDA (TIkr.com)

{kind=link}

The same is true for many of the Scandinavian companies that I write about in the industrial sector.

But still - it's a specialty chemicals company trading over 30x P/E. On 5-year basis the average P/E-ratio is as high as 44x P/E and above.

I want to clearly state to you that no company with 13-15% estimated EPS growth is worth this premium in my eyes. We have an EPS yield of less than 2.9%, and a dividend yield of 1.18%.

In the case of market underperformance or reversal to standard valuation patterns, you're almost guaranteeing yourself sub-par returns here.

At least if we look at valuation the following way.

Sika AG - So much to like, but valuation throws us a curve ball

So - yeah. Valuation is really throwing us a curve ball here. Investing in an industrial specialty chemicals at almost 35x P/E, even with this sort of upside comes at a comparatively high risk - namely the risk of underperformance.

Underperformance for Sika is fairly easy. In fact, all it would take for Sika to underperform based on current EPS estimates is if the company was trading at a forward of 30x instead of 35x. In this case, your annual RoR would be around 7-8% annually. Even a 32.5x would barely bring about double digits.

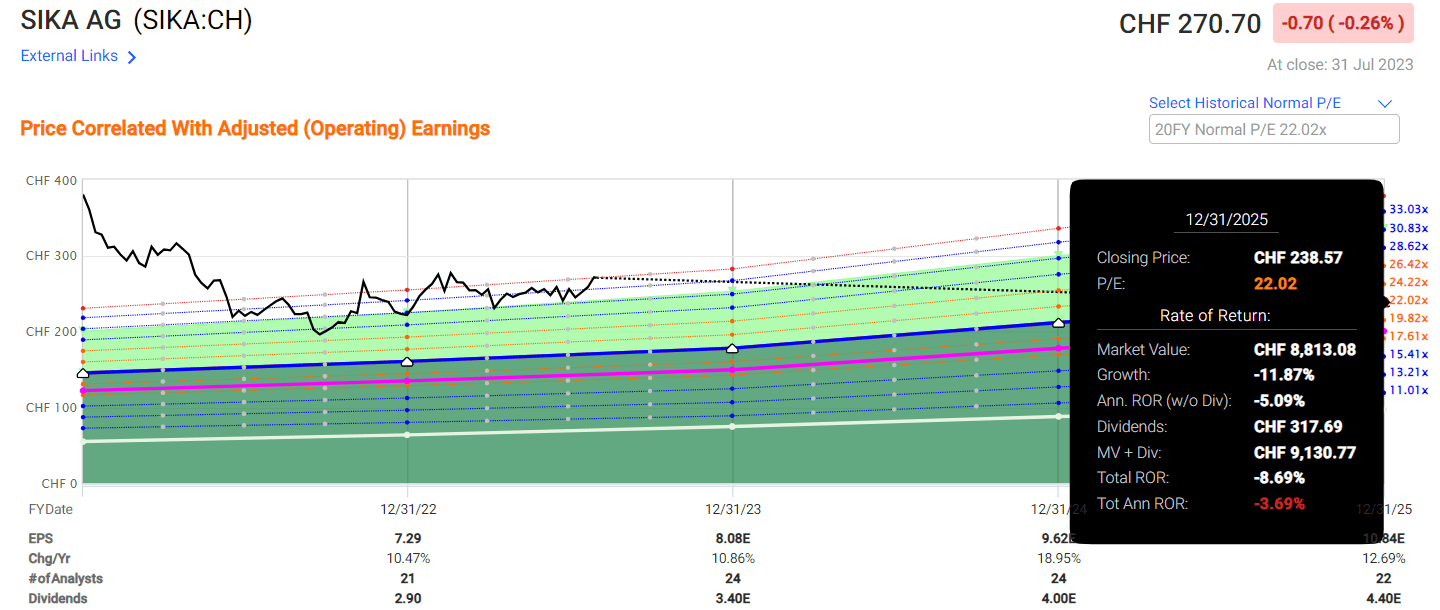

We've been in an environment where growth has been priced at a high premium, with very little regard for yield. This is still reminiscent in Sika, despite some of the normalization we've been able to see. However, to illustrate to you just how quickly things could normalize, I want you to take a look at the 20-year average P/E.

Sika Upside 20-year premium (F.A.S.T graphs)

{kind=link}

Do I actually think it is likely that we'll see this sort of valuation? No, that would be too contrary to the company's growth trajectory. I don't actually think that this would be likely.

However, what I want to illustrate here is the degree of premium the market is assigning to the company, and what you accept if you invest here. It's after all, about what sort of degree of premiumization and valuation you accept.

In this case, while we've seen a decline in Sika, I don't believe the case is a "simply bullish" as some would have them presented to you.

I can see an upside here. The company is a great business, great profitability, great prospects. At a 33-35x P/E, which we have today and which bulls would have you forecast at, you're getting around 15-16% per year, but most of that is earnings growth and premium - almost all of that earnings growth and retained premium.

S&P Global has a comprehensive coverage of the company, 21 analysts covering Sika at PT's of 228 CHF on the low side and 360 CHF on the high side, averaging out at a price target of 300 CHF, implying an even higher upside here.

I find assigning a justifiable valuation here difficult. Analyst accuracy isn't as high as the results would imply. FactSet only hits the mark 58% of the time with a 10% margin of error. I would put Sika at a forward P/E of about 30x, implying an upside of around 9.9% annually long-term. Not enough to interest me regardless of what else is available on the market, but it might be enough of a market beat to interest you - and it's enough for me to consider the company a "BUY" here - as long as you understand the limitations of what you're buying, and the potential downside.

if you do, then here is my initiatory thesis for you when it comes to the Sika AG.'

Thesis

- Sika AG is a world-leading specialty chemicals business with market-leading and superb brands. It has solid management, solid growth, solid profitability, solid fundamentals and credit rating.

- The lack the company has when it comes to looking at as an investment are primarily two. First off, the company's dividend yield is sub-par, and unlikely to change. Secondly, the company's valuation is almost triple that of other chemical investments - and this is up to you whether this is something you want to go into.

- Provided you accept a very high premium, and you're fine with the low dividend yield, then this is an investment for you.

- I do consider it a "BUY" - but my PT goes only to 300 CHF - and this is on a forward basis - so the upside is slim here, as I see it.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

This means that the company fulfills all but one of my criteria, making it relatively clear why I view it as a "BUY" here - provided that the premiumization is something you can get on board with.

For further details see:

Sika: Not As Great As Some Believe, But Quality And A 'Buy'