SXYAY - Sika: Upside After Buying The Dip

2023-12-19 06:17:06 ET

Summary

- Sika AG, a multinational specialty chemical company, has seen significant growth in sales and margins in 2023.

- The company is expanding across various markets and leveraging global megatrends for future growth.

- Despite its high valuation, Sika AG remains a solid investment option with strong fundamentals and market leadership.

Dear readers/followers,

I wrote an article on Sika AG ( SXYAY ) ( SKFOF ) not that long ago. Pretty soon after that article, the company dropped to levels I would not only consider attractive, but almost cheap for Sika.

So I bought it. If you read the piece which I wrote here then I would point you to the thesis - not the greatest price, but quality. But now I managed to "BUY" Sika for a great price, and given the massive reversal we've seen since that drawdown, I'm up significantly.

Sika AG, to remind you, is a multinational specialty chemical company with over 110 years of history and operations in over 100 countries. The company is known for its stability and high-quality products that are being used not only in new construction but significantly in reno/refurbishing as well. This stock typically trades at a significant premium to other cyclical chemical companies, but there are reasons for this.

Sika not only benefits from global megatrends, such as the repair and refurbishment of older buildings and expansion into emerging markets like Southeast Asia, but it also has the history and the quality to back all of these things up.

In this article, I'll look at 3Q23, and estimate where we go for the next year.

Sika AG - A lot to like about quality chemicals

Sika is a huge Swiss, 110-year-old business with verticals and products in specialty chemicals. The headquarters are in Baar, Switzerland. It's active in over 100 nations and has over 10B CHF in annual revenues.

The company is among the best-rated chemical businesses with an A rating. It's also one of the lowest-yielding, at less than 1.2% dividend yield. However, it's also one of the most stable chemical businesses in the world, and it seems to go completely against the notion that "Chemical businesses are volatile".

So, a lot of contrarian things to Sika. The yield prevents most investors who follow my article from going all that deeply - but the fundamental trends are the upside and the biggest argument for investing here that we're seeing. Even if the company has what I would consider a very limited yield, especially in this operating environment, we're still seeing good top-line growth.

How so?

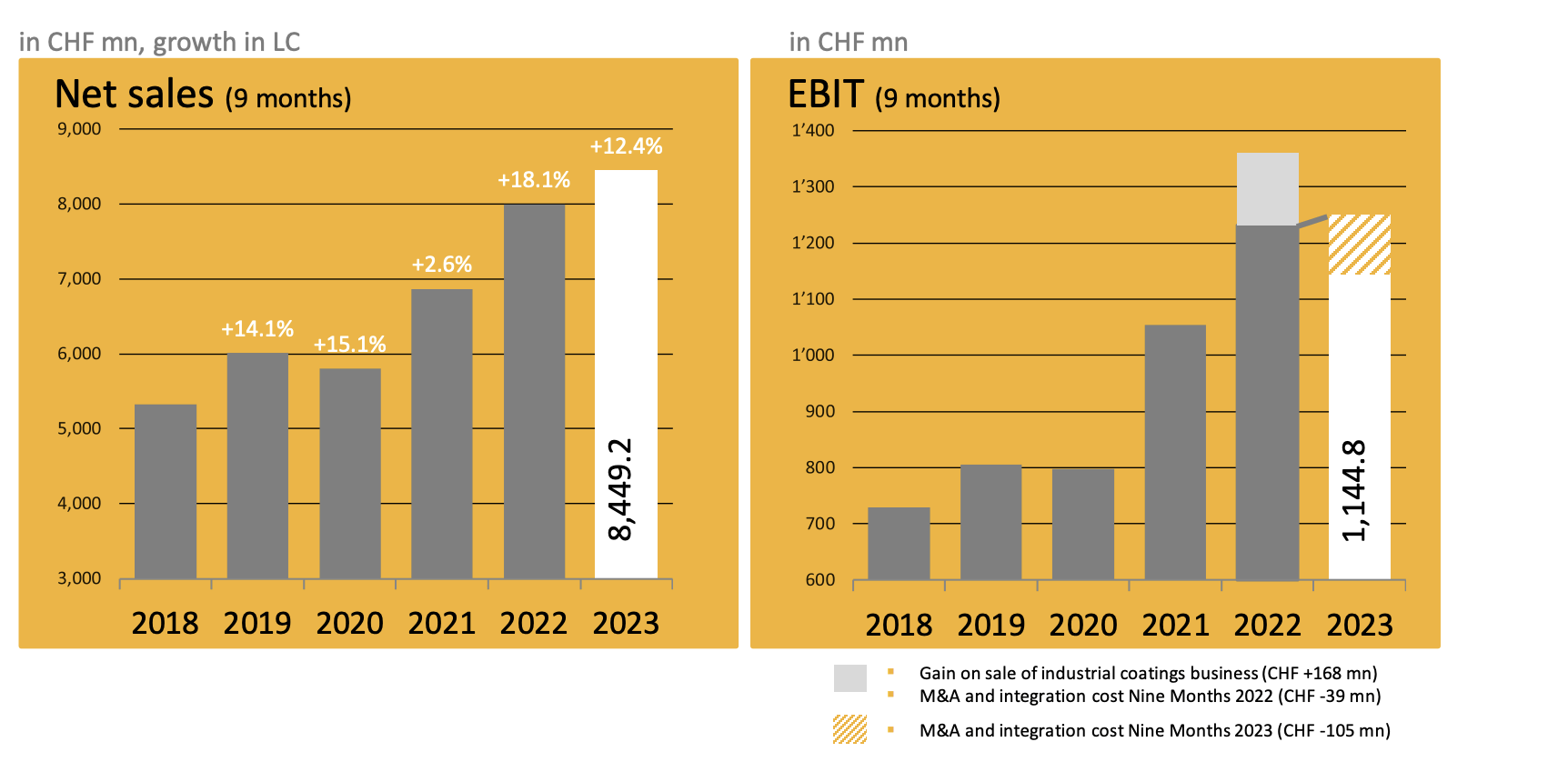

Well, for 9M23 the company recorded 12.4% local currency sales growth, and record sales numbers, totaling almost 8.5B CHF. The company also saw material margin expansion to 53.1%, up almost 400 bps.

The company increased EBIT margin, higher EBIT, and higher operating free cash flow - almost double that of YoY. So the downward trend we saw in 2-3Q isn't really something I considered justified.

That's why I added more Sika AG to my portfolio - although not to any major 1-2% exposure, sadly. I usually expand my positions slowly, which means that sometimes the suddenness of reversals catches me off guard and causes me to "miss" opportunities. Other times, it enables me to really establish a 1-2% position at a very attractive sort of valuation and yield.

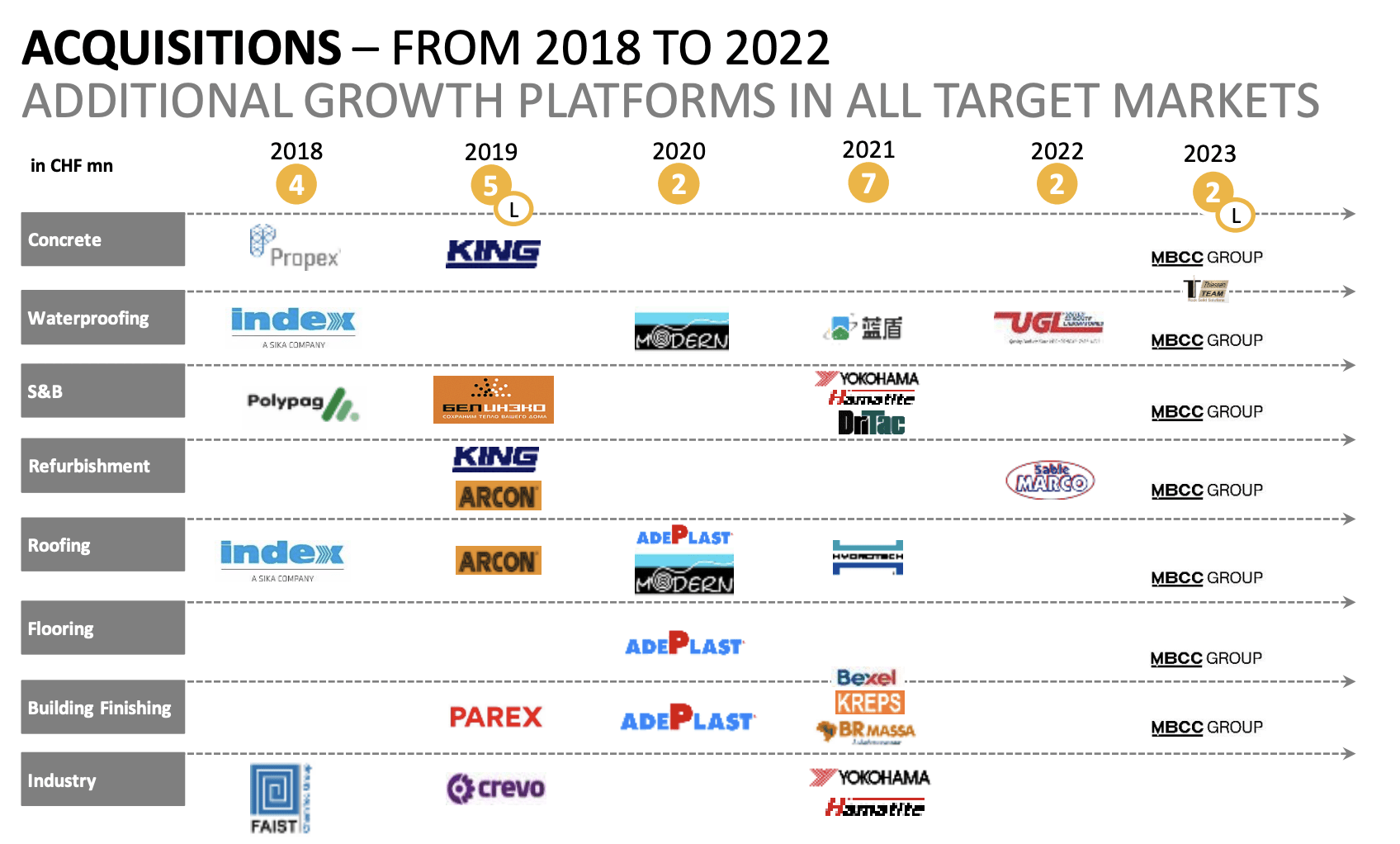

The company has multiple operational upsides and good results for this year. This includes the opening of a new mortar and admixture plant in India, an M&A of the Thiessen Team in the US, a new macro fiber line in the US, and an M&A of Chema, mortar from Peru. In short, the company is expanding across the board and moving to realize synergy potentials in the hundreds of millions of Swiss Francs. The company is playing the inorganic growth game as things currently stand, and unlike many companies in this game, Sika AG has a history of actually making these trends work .'

The improved margins and results are proof of this - as is the improved growth model the company follows.

{kind=link}

The company has, in fact, proved over time that it can deliver topline growth and profit over the last 4-5 years, not only double-digit improvements in net sales but in EBITDA and EBIT as well. It goes again for the point that you pay for quality. Sometimes cheaper operators with less quality are available at good prices, but I can certainly understand those who would rather pay more for a quality operator instead.

The company is following the nuts and bolts of its 2028E strategy. This involves switching the FCF proxy EBITDA as the main KPI, focused initiatives to drive specific market penetration pushes, the expected net zero pathway that most companies in this environment seem to adopt, and moving to become a market leader in certain new segments, such as the automotive industry.

{kind=link}

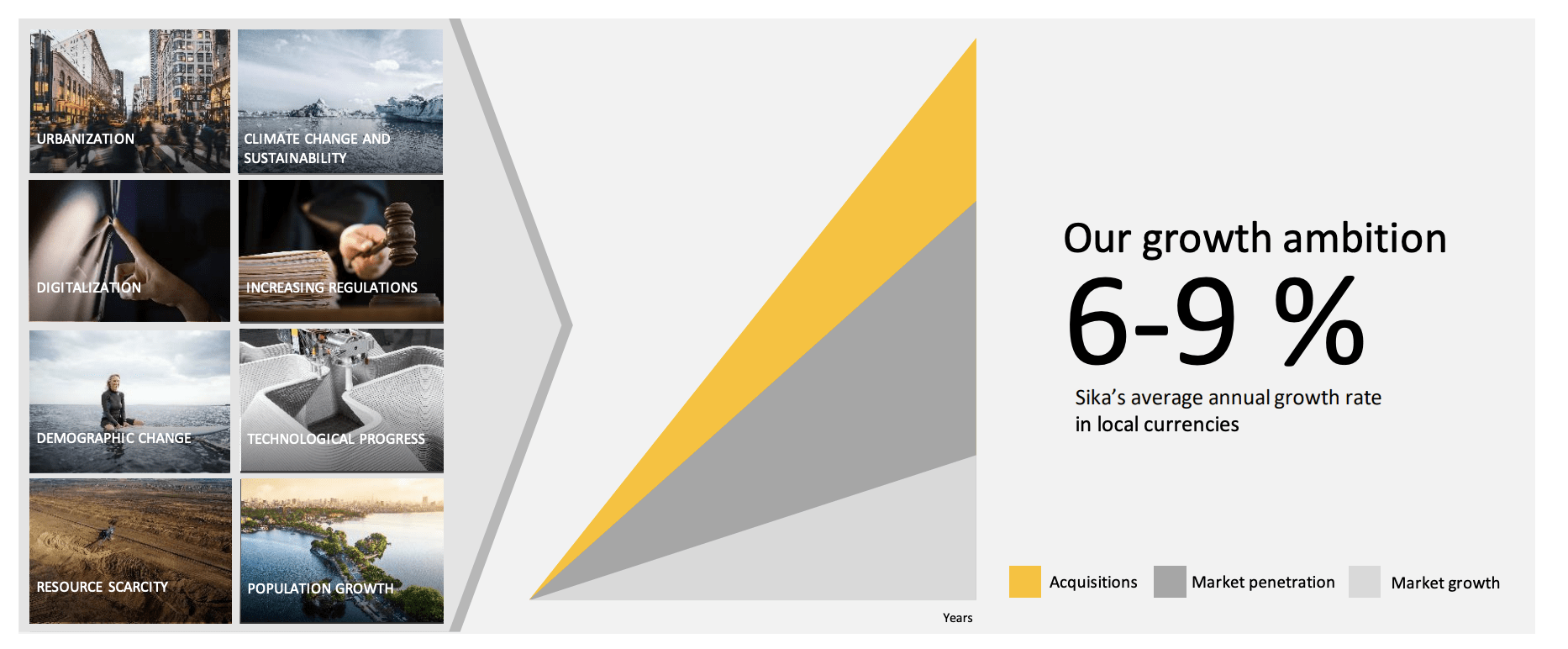

The company also fully expects the above-average growth to continue, with megatrends as the main driver for these improvements. These megatrends include population growth, urbanization, significant demographic change, ongoing resource scarcity and climate change, increasing regulation that will make things harder for the smaller player, ongoing technological processes, digitalization, and other factors. All of these things will enable a specific increase in market penetration which is expected to drive these changes and profitability metrics higher.

Currently, Sika has around 11% of the market in construction chemicals. That's 10-11B CHF out of a TAM of around 110 B. Despite massive M&A activity, the market remains a very fragmented landscape and one where Sika AG is the undisputed market leader at this time. It has 11%, its top 30 competitors have 55% of the market share together with no one higher than 4.5% aside from Sika.

This is what the company will leverage on a forward basis, with an ongoing growth ambition in LC of 6-9% per year.

{kind=link}

How?

Through strong cross-selling and a multi-channel approach, focus on growing geographies in high-potential markets. I interpret this as increased volatility and risk as well - but when it comes to Sika, I believe the risk to be on a controllable level given the company's very solid history of making lemonade out of lemons - when it comes to acquisitions. We have decades here in terms of history, and the past 4 years have really shown us just what Sika "can do".

{kind=link}

We have expectations for 2023 and beyond. For 2023, the company forecasts top-line increases of 15% in local currencies, excluding MBCC, with a confirmation of a very large EBIT increase, even excluding MBCC. The company's operating FCF is expected to be over 10% of net sales, another very solid trend.

In short, Sika is thriving despite being a cyclical business - and here is how I expect the company to look in terms of Risks and upside in the near term.

Risks & Upsides with Sika AG

Risks to Sika AG are not mainly operational. I view the company as "too good" at what it does to see a significant downturn from a failed M&A or some sort of operationally specific trend. A good comparison is someone telling me they're afraid that my investment strategy could result in material deterioration and significant loss of capital to where my own economy would be in danger.

My response would be that my highest acceptable position allocation is 2-4%, and my portfolio yield is always higher than my highest portfolio allocation. Because of that, even a material decline in a specific position has only limited effects on my overall fortune.

Sika is similar. It moves with care and despite its cyclical sector, company leadership and quality are the main upside here, not yield. If you're interested in investing in an overall mega-sector-dependant company, I would say that Sika AG is a good bet.

Let's look at company valuation.

Sika AG - Plenty of upside if you're willing to premiumize.

When the company dropped down to below 220 CHF, I was on it like a kid on a Twinkie. I expanded to 0.15% of my portfolio. This might not sound like much, but it's a large move for me given my overall portfolio size at this point - and how I typically go about expanding in a company.

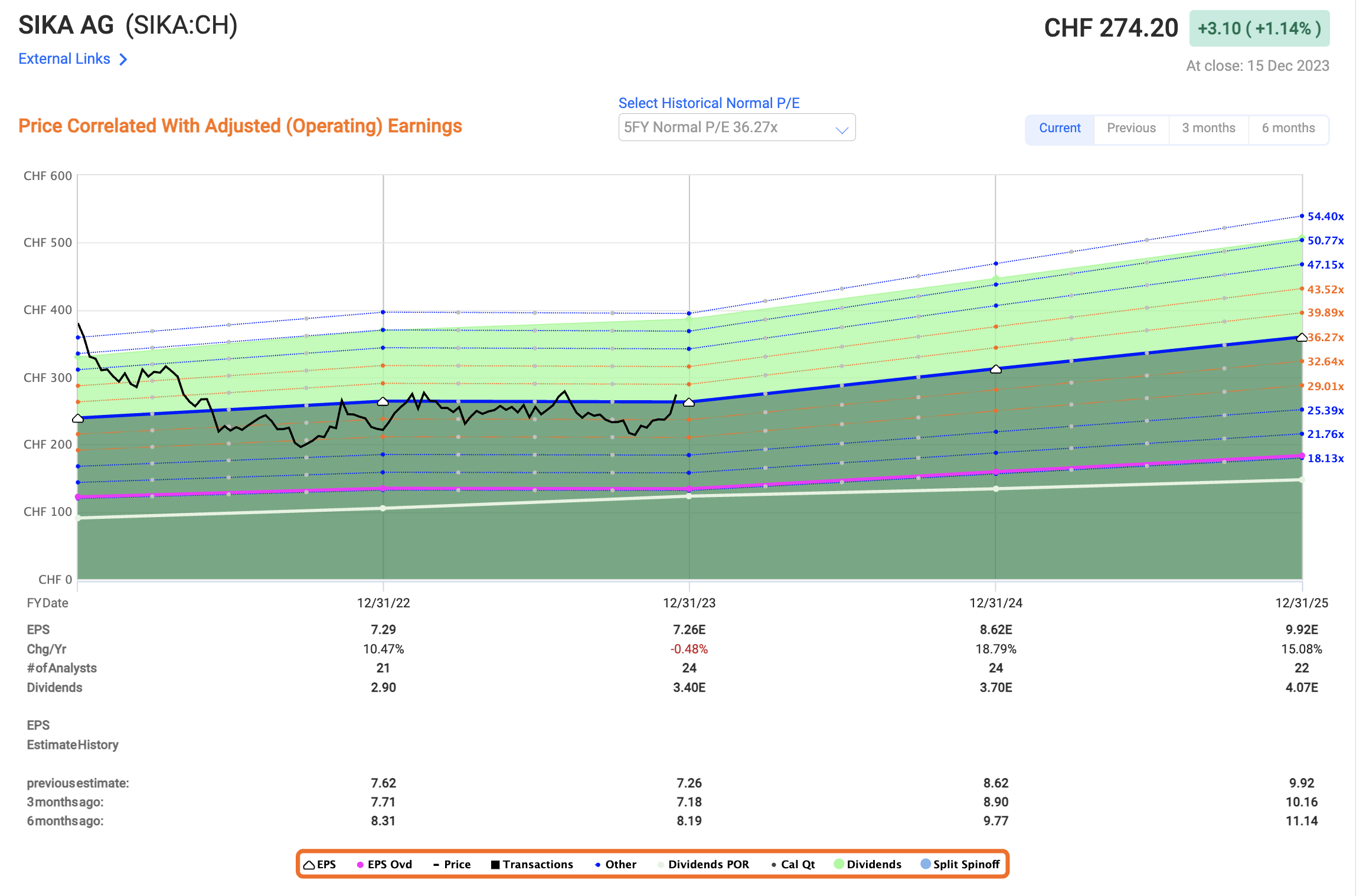

Unfortunately, Sika reverted far quicker than I could have expected and now trades even above what I saw when I wrote my first piece on the company. The current normalized P/E is above 37.5x.

And in this environment, yes, even with growth, that's a bit of a problem for me. I would like cheaper, the problem is that Sika rarely goes cheaper for long.

The best way to play Sika, I believe, is to take advantage of the short bursts in downward valuation that take place with frequency. If you take a look at the valuation relative to P/E you'll see this is exactly what happens.

{kind=link}

And before you get all excited about the upside you see here, remember that this upside is based on a 36x normalized 5-year average. This company actually misses negatively 25% of the time even with a 10-20% margin of error, so there's the potential for downturns here.

Let's say we use the 20-year valuation trends. That's 22x P/E. To a 22x P/E in 2025E, there's a negative annual RoR potential of almost 9%. Between a heavy short-term premiumization and the current interest rate and macro environment, I continue to be unwilling to be overly exuberant at this valuation.

I remain at a "BUY" stance - no doubt about that. But I will not go heavily beyond "BUY" with my previous PT, which for the long term still comes to 300 CHF. To give you an example, a 2025E P/E of 36x implies with the current growth rate a share price of almost 360 CHF. I believe this to be too much.

At 275 CHF, the company is a "BUY" - but not one I will go out of my way to buy at a 1.17% yield. But if we see a drawdown to below 230 CHF, then I'll be more on the prowl and add more shares here.

I have no issue with a 2-3% Sika AG allocation, provided I get that allocation at the right cost basis.

Here is my updated thesis for Sika.

Thesis

- Sika AG is a world-leading specialty chemicals business with market-leading and superb brands. It has solid management, solid growth, solid profitability, solid fundamentals, and credit rating.

- The lack the company has when it comes to looking at as an investment is primarily two. First off, the company's dividend yield is sub-par and unlikely to change. Secondly, the company's valuation is almost triple that of other chemical investments - and this is up to you whether this is something you want to go into.

- Provided you accept a very high premium, and you're fine with the low dividend yield, then this is an investment for you.

- I do consider it a "BUY" - but my PT goes only to 300 CHF - and this is on a forward basis - so the upside is slim here, as I see it. The same remains for my thesis as of December of 2023.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansions/reversions.

This means that the company fulfills all but one of my criteria, making it relatively clear why I view it as a "BUY" here - provided that the premiumization is something you can get on board with.

This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Sika: Upside After Buying The Dip