SILC - Silicom: A Value Bargain With Growth Potential

2023-11-21 05:02:44 ET

Summary

- Silicom is trading at a steep discount to its cash and inventory value, making it a bargain at current prices.

- The company is projecting a roughly break-even year in 2024 but has plenty of cash to ride it out.

- SILC expects to bounce back in 2025 and resume double-digit growth.

- Silicom is positioned in an industry that is expected to grow through at least 2030, so there is plenty of opportunity ahead.

Investment Thesis

Silicom Ltd. ( SILC ) is a free business, if you believe in it. The company is bracing for a bad year in 2024, hoping to break even or crank out a small profit, but warning that they could take a loss for the first time in 18 years. Then in 2025, they say they'll bounce back and resume double digit growth.

Despite that, the business is trading at a steep discount to its 52-week high of $50 per share. In fact, it's trading at a steep discount to its tangible book value of $22.73 per share and its cash and inventory value of $19.25 per share. According to Silicom's third quarter earnings call , where they stated that the cash position had increased to $67 million since the end of the third quarter while confirming the inventory stood at $63 million. Dividing that $130 million by 6,753,000 weighted shares (per the Q3 earnings report) gives us that $19.25 figure. At the time of this writing, SILC can be had for just $15.40 per share.

So if SILC's long-term assessment is accurate, you can buy dollars at a discount and get a free business to boot. You just have to be willing to be patient. Is Silicom a risk worth taking? From a value investor's perspective, it's about as good as it gets. Let's break it down.

About Silicom Ltd.

SILC makes high-performance networking and data infrastructure products, such as server adapters, smart cards, and edge products. Basically, they make customized solutions to improve performance and efficiency in telco and mobile deployments infrastructure, cloud and data centers, edge networking, and cyber security.

They primarily work with current and potential clients to compete for design wins based on the particular specifications and needs of their customers, then contract future business when they're awarded a win.

Silicom Ltd. Presentation, Q3 2023

On a trailing twelve-month basis as of their third-quarter earnings report, Silicom derives around half of its revenue from the platforms and infrastructure segment, just under a quarter from cyber security, and a little under 20% from network appliances.

Silicom is headquartered in Kfar Sava, Israel, with offices in Paramus, New Jersey, and Soborg, Denmark. Their manufacturing plant and storage space are located in Yokne'am, Israel and their secondary storage space is located in Migdal Ha'emek, Israel. These locations are 15 to 20 miles from Haifa. Their executive offices are about 15 miles from Tel Aviv.

SILC Value Fundamentals

There are a few key areas I look at as a value investor, and SILC is strong in most of them. If they can bounce back to double-digit growth, they would become a 10/10 on my screener at these prices. But for now, they're a 7/10, which is my standard threshold to buy.

Margin of Safety

The first thing I look to do as a value investor is protect myself from significant downside risk. I feel extremely good about SILC in this regard. With a tangible book value of $22.74 per share, and a net current asset value of $13.96 per share, there just doesn't seem to be much downside here unless the company is deluding itself and investors over its ability to scratch out a break even, or close to it, 2024.

Even if the company were to remain break even, it could be an acquisition target, as simply liquidating its cash and inventory would return more to investors than the current market price.

Price

In an absolute sense, the price is fantastic. It's cheap relative to its book value, it's cheap relative to its trailing earnings, and it's cheap relative to its 2025 and beyond earnings. If we're willing to look past a rough year in 2024, and as long-term investors that's not a problem, this is a bargain.

Relative to its typical range of price-earnings ratios, Silicom is also trading at a huge discount. This means that once the company returns to its baseline revenue and resumes double-digit growth, the market will likely be willing to pay a multiple somewhere in the 15x to 25x range based on how it has historically valued the company, and current investors can get it on sale for 7x to 10x.

Earning Power

This is the area that's most concerning, especially for investors who are looking for big growth upside. Obviously, 2024 will be challenging for Silicom, and there will be more detail on that below. But they've also had choppy earnings for quite some time now, after strong growth through 2014.

Given that we went through a pandemic in there, it's easy to form a narrative that the trendline was still quite positive through 2018, and with a lot of supply chain disruption, you need to evaluate the business from 2020 through present based on their average earnings and revenue and not judge them on the annual numbers.

That's a reasonable view, but so is the case that from 2014 to 2019 their earnings were choppy, and that may be kind of the peak for SILC. It's possible that something in the neighborhood of a range of $1.50 to $2.50 per share, and not a lot of further growth, is the future for SILC. I'm not here to make a strong argument either way, because while I'd obviously prefer the growth narrative, I'm perfectly happy to buy a business cranking out $1.50 to $2.50 per share in the $15 to $16 per share range when the cash and inventory on hand is worth more than $19 per share, and they've been profitable 18 years in a row.

Return of Capital

While SILC no longer pays a dividend, they have been buying back shares, and the buyback yield is likely to be in the neighborhood of 8% over the next six months. That's more than enough to make me happy.

They repurchased $4.8 million worth of shares in Q2 and Q3, which leaves $10.2 million under their authorization for Q4 2023 and Q1 2024. Their CFO Eran Gilad said on the Q3 earnings call that they plan to continue repurchasing shares at a pace of around $15 million per year.

During the third quarter, Silicom purchased approximately 144,000 shares at a cost of $3.9 million under the 15 million share repurchase plan we announced earlier this year. In total, Silicom has purchased an aggregate $48 million in share buybacks in recent years. As mentioned by Liron, based on our strong balance sheet and improved cash position, we intend to continue repurchasing our shares at full pace."

SILC's commitment to returning capital to investors seems strong, and if they end up stagnating in terms of growth, I'm content to own a business with a strong balance sheet that returns capital with yields that high.

Financial Soundness

This category is particularly important for a business heading into a tough year. Silicom has no debt and a current ratio of more than 8.8. They have always run the business somewhat cautiously, keeping the current ratio between 4 and 6 most of the time.

With supply chain issues during the pandemic, SILC invested to build up inventory so that its customers could do the same, and knowing they were heading into a rough stretch, they've now also built up their cash position. With $67 million in cash as of the most recent earnings call, Silicom is confident enough in their ability to ride this out that they're not suspending buybacks.

Risks and Headwinds

Lack of Visibility and Potential Losses in 2024

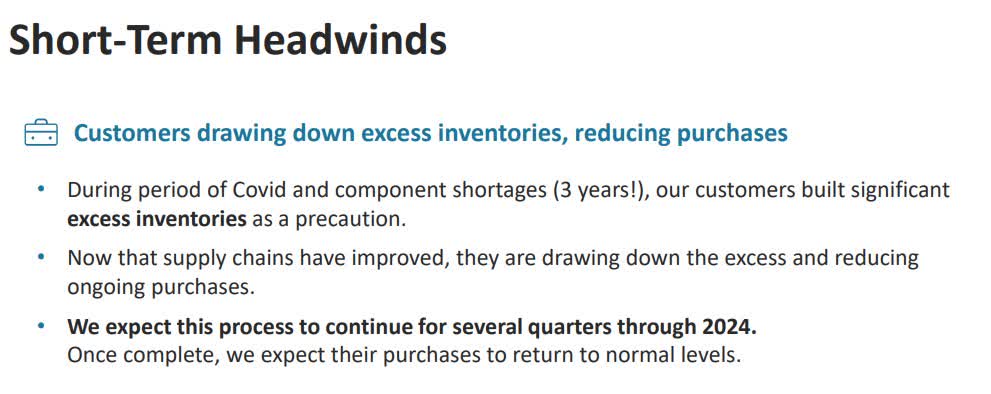

The primary reason that SILC is such a bargain right now is that 2024 is going to be bad, and they aren't giving detailed guidance on how poorly it will go. This is because their customers have built up inventory due to supply chain risks, and now that things have normalized, they can work through the inventory instead of immediately placing more orders. Here's CEO Liron Eizenman discussing it on the Q3 earnings call .

Similarly, over the past two years, our customers ordered a high level of our products for months, so they can manufacture products for their customers in turn. And this ordering, a good portion for inventory, drove above average demand and a high backlog for our products in both 2021 and 2022. However, the second half of 2023 has seen a reversal in this trend. The supply chain's tightness has abated and customers which has built-up significant inventory are now drawing on their existing stock of our products where possible, and currently do not need to order significant quantities for months."

Eizenman also spoke at length about the lack of visibility towards 2024. They don't know when this dynamic will subside for them, and they won't give any detailed guidance on 2024 revenues yet. They believe that on top of the stockpiles of inventory their customers built up, a murky macroeconomic picture is leading to some delays in orders.

What Silicom Will Project

Eizenman wouldn't project 2024 revenues but did say on the Q3 call that they believe they can break even or come close to it in 2024 without sacrificing future growth potential.

I would say on an annual basis we still plan to be I'd say break even or profitable, right. That's our goal on an annual basis and it does not mean that we will do everything we need to do in order to be there, because our plan based on the analysis we've done is that we can continue and develop the product that we need and continue to do everything that we need to do in order to grow the company in 2025 and beyond, and we don't want to sacrifice that. That's extremely important for us, but we took steps, we took a lot of steps in order to manage our cost to make sure that even at the estimated 2024 numbers or the plans that we have in mind we will be -- it will be on an annual basis, be break even or profitable."

So they're basically saying they'll be roughly break-even in 2024. In their Q3 earnings presentation document, they say that they expect customers to return to normal purchase levels in 2025.

Silicom Ltd. 2023 Q3 Presentation

{kind=link}

Analysts on the call were frustrated by the lack of specifics with regard to 2024, but I believe the two key factors that long-term investors need to consider are how much SILC will lose (if anything) in 2024 and where they expect to start from in 2025 when resuming double-digit growth. I really don't care what their revenue figure is in 2024, as long as their prediction that they'll be roughly break-even pans out. I care about the revenue in 2025 and beyond because that's what the resumption of double-digit growth is working on.

While they aren't giving guidance, I think they have provided enough information to extrapolate the numbers we need. Based on the Q3 call, Silicom isn't ruling out turning a small profit in 2024, but they would be happy to break even and admitted that quarterly losses are possible. It seems safe to say that they aren't going to significantly weaken their balance sheet riding it out, which is good enough for me. In the grand scheme of things, a small profit or a small loss in 2024 doesn't fundamentally change this investment thesis.

They expect to return to normal levels in 2025, but the question after a few years of supply chain chaos is, what constitutes normal? We can't use 2022, since that's when orders were higher and customers built up this excess inventory. If we look at income statements pre-pandemic, SILC averaged $116 million in annual revenue and $1.97 in annual earnings per share over a four-year stretch from 2016 through 2019. That seems like the lowest range we could consider "normal."

On the Q2 2023 call at July-end, Eizenman was pressed on what the baseline of revenue would be once things normalized. An analyst asked if $35 million-plus was reasonable for quarterly revenues. Eizenman agreed with that figure.

Maybe, I think it's reasonable to say this number. I think overall, when we're looking -- trying to analyze the situation, obviously, it's not only inventories. I mentioned before also the economic, let's say, concerns, et cetera, that are also in the mix. It's a little bit hard to distinguish between the two.

But again, when we analyzed the data, we looked at least $10 million-plus that were pushed out from this quarter per our expectations that customers would put. So, $35 million, maybe a little more could be as well, but it's very hard to say an exact number given that it's a mix of reasons here."

So that would put the annual figure at $140 million of revenue. On the most recent call, Eizenman said gross margins could come down to the 31% to 33% range, which would mean a baseline of gross profits around $44.8 million. That's higher than the 2016-2019 average of around $41.5 million, and in line with the 2021 figure of $44.4 million. In 2021, the company generated earnings per share of $1.51. So it feels like a good estimate for 2025 is approximately $140 million of revenue, $45 million of gross profits, and $1.50 to $2.00 in earnings per share.

Based on the above, it feels like the gloomiest estimate would be a 31% margin on revenue of around $116 million, which would yield gross profits of around $36 million. That matches the 2019 figure, when the company earned $1.35 per share. This still seems fine, given the current price.

Changing Decision Makers in Industry

The other risk-factor that should be weighed is that, due to strategic reviews of operating processes throughout the industry in light of the supply chain disruption over the last few years, the decision-maker on which server adapter vendor to use could change.

A result of that may be a decision to change their decision-making processes and integration practices. With that, the selection of this specific server adapter vendor, which will be used for building their systems may be moved from the company to its integrator. While this may present an opportunity for us with companies, which currently do not use our server adapters, it may present a challenge with existing customers that we will face once such customer will exhaust the excess inventory it currently has."

This presents both a risk and an opportunity - Silicom could lose business if some clients push the decision off to the integrator, but competitors could also lose business this way and Silicom could acquire new business. This presents volatility, but it's not necessarily all negative.

Either way, it's not going to impact a significant portion of their revenue. On the earnings call , Eizenman estimated it at about $5 million of annual revenue that is at-risk and emphasized that they don't expect to lose all of it.

Concentrated Business with Top Customers

One of the other risks, that many micro caps face, is that around 35% of their revenue on a trailing 12-month basis is concentrated in their top three customers, according to their CFO Eran Gilad on the Q3 call. While this may not be ideal, it's part of the game with smaller companies, and as a result, investors can generate stronger returns. It's a risk I'm comfortable taking over my lifetime as an investor, with the expectation that stronger overall returns will more than offset those times the downside risk is realized.

I'm particularly happy to take on this risk when I'm getting such a bargain - remember, we're getting $19.25 of cash and inventory for $15.40 at the time of this writing.

Potential SILC Growth Catalysts

Silicom is not without potential growth catalysts, and if they are able to execute one or more of them, investors could end up with enormous returns at current prices. The company has been adamant that it can resume double-digit growth from 2025 forward, with Eizenman stating it twice on the third quarter earnings call .

Looking further to next year, giving our very limited visibility and the factors I just discussed, we expect 2024 to be a challenging year. However, we strongly believe that we will return to double-digit growth in 2025.

In the second reference, he cited their backlog of design wins as providing evidence of enough future business to power such growth at SILC.

Our aim is to return to double-digit revenue growth and recovery in 2025, underpinned by a strong and continually growing list of design wins, many of which are with some of the world's leading players in telco and networking space.

Obviously, businesses tend to be bullish about their own prospects, but Silicom does have a strong track record of issuing accurate guidance, with 22 consecutive quarters without an earnings miss. They also remained particularly cautious in their statements about 2024 in the face of criticism and pushback on that recent earnings call, which in my eyes lends more credibility to the projections they're willing to make. They're also serving markets that are projected to grow rapidly over the next decade, such as edge networking, which creates plenty of opportunities to hit their target.

Growth in Edge Networking

The fact that Silicom is projecting a return to double digit growth in 2025 and beyond makes sense given the trends in networking. As another analyst pointed out in an article in February , the global edge computing market is expected to grow at a CAGR of 32.3% from 2023 to 2030. While this does pull down their overall profit margins (this segment has lower margins than their others), that's a tradeoff that seems worthwhile if that segment of the business is growing its revenue at anywhere near 32% per year. This is an area that Silicom is focusing on, according to Eizenman.

In parallel, we intend to increase our focus on the sectors that have allowed us to grow so well in the recent times, and those that we believe will remain primary growth drivers for us into 2025 and beyond. Server adapters, including specific FPGA-based and hardware acceleration smart NICs and Edge Systems."

Cyber Security Increasingly Critical

SILC also provides cyber security solutions, and it seems like every week or two a major corporation is in the news due to being hacked. With ransom attacks increasingly common, and some major corporations taking significant hits , it stands to reason that increasing amounts of money will be spent on cyber security.

SILC has had recent design wins in this area and continues to pursue more. On the 2023 Q2 earnings call , Eizenman highlighted that win.

In April, a Tier 1 U.S.-based cybersecurity vendor awarded us with two NIC design wins: one for an advanced encryption offload acceleration card and the other for an FPGA-based market. Both will be incorporated into two customers' next-generation solutions, which are sold to some of the world's largest, most technologically advanced companies to secure and optimize their networks and applications in the cloud, on-premise over the edge."

Continuing Share Buybacks at Bargain Prices

The fact that SILC is in such a strong financial position is allowing them to continue to repurchase shares into 2024, despite the headwinds the company is facing. Shareholders should be thrilled with this, not only because it will provide price support in the short-term, but because of the reduced share count in the future as the company resumes growth.

I'm not a fan of indiscriminate buybacks, and often in tech we see companies buying back shares at price levels that perhaps aren't supported. But when a company is trading for less than the sum of its cash and inventory, I want to see management buying back shares hand over fist. With shares at $15.40 and cash and inventory at $19.25, that's an immediate 25% return on capital. That's a huge win. Likewise, assuming management executes its plan and returns to baseline revenue and double-digit growth in 2025, all of those shares bought back in the $15 to $16 range are going to look like an absolute steal.

SILC Could Be an Acquisition Target

Even if Silicom does not execute its plan to perfection, buying in at such a discount means that investors could show a significant profit if SILC becomes an acquisition target. Major companies have shown a recent appetite for this type of consolidation, with NVIDIA buying Mellanox , a Silicom competitor, for $7 billion. That deal closed at $125 per share, which represented 34.5 times their final trailing earnings and 4.2 times their final book value. Needless to say, an acquisition at multiples anywhere near those levels would provide a tremendous return to Silicom investors.

SILC Price Target and Valuation

I'm not particularly concerned with nailing an exact price target when buying a stock. Rather, I look to identify a broad range and enter a position well below that range. In this case, I'm looking to project Silicom's fair value in 2025 once it returns to profitability and growth. I showed above that SILC has traded at a price-to-book ratio between 1.6 and 2.4 quite often over the last five years. It has also traded at price-to-earnings ratio between 20 and 25 quite often and for extended periods of time.

SILC currently has a book value of about $27.66 per share, so its typical range would be $44 to $66 per share. I demonstrated a reasonable earnings projection of $1.50 to $2 per share in 2025, which would give us a range of $30 to $50 at multiples it has frequently achieved in the past. If it hits those levels, I would re-evaluate based on its fundamentals and growth trajectory at that time, but a very broad range of $30 to $66 per share seems reasonable. I would say the lower end looks attractive in the near term, whereas I'd be more inclined to hold on for the high end (or beyond) if the company has already returned to baseline profitability when those values are reached.

Conclusion

One of my core tenets as an investor is patience. I'm looking to maximize my long-term returns, and I have no qualms about riding out short-term turbulence. This is likely at least a two-year play (and if growth is impressive, it could be a lot more than that), but it should show impressive returns. At the low end of my target range ($30), an investor buying at $15.40 would see annualized returns of nearly 40% across two years. At the high end ($66), that would translate to more than 105% in annualized gains. Needless to say, those numbers are far superior to average market returns. As a result, I consider SILC to be a strong buy at current prices.

For further details see:

Silicom: A Value Bargain With Growth Potential