SILK - Silk Road Medical: Unsure On Economics Given List Of Probabilities (Rating Downgrade)

2023-08-10 03:50:45 ET

Summary

- Silk Road Medical's Q2 FY'23 numbers show reasonable performance, but the stock has slipped over 60% since December.

- The outlook for the company is mixed, with potential capital budgeting constraints and exogenous risks from the marketplace.

- The company specializes in mitigating the risk of stroke, and its revenue comes from the sale of its TCAR products.

- Net-net, reiterate hold.

Investment briefing

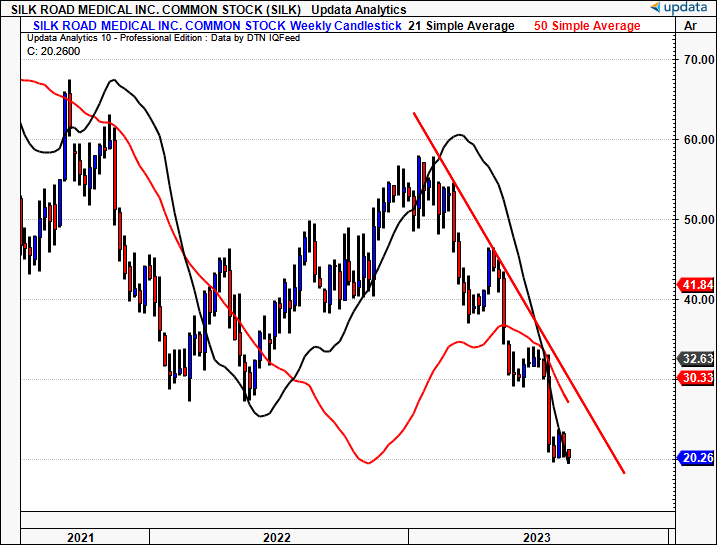

Silk Road Medical, Inc. ( SILK ) posted Q2 FY'23 numbers last week with a reasonable performance throughout the P&L and cash flow statement and balance sheet strength. Despite this, the outlook is mixed on the firm as an investment-grade company. Since my last publication in December, the stock has slipped >60% to the downside, begging the question: Is it cheap, or is it low value?

Based on findings discussed here, the scope of potential outcomes for SILK going forward is vast in my opinion. This doesn't add a layer of confidence to investor returns moving forward. Here I'll run through my revised hold thesis after the deep dive revealed potential capital budgeting constraints amid other exogenous risks from the broad marketplace. Net-net, reiterate hold.

Figure 1. SILK price evolution, rapid selloff across FY'23

{kind=link}

Critical facts forming revised hold thesis

Here I'll run through all of the critical investment facts forming the SILK investment debate.

1. Revenue model and core offerings

SILK specializes in mitigating the risk of stroke and its lasting effects on patients. If you didn't know, a stroke is caused by either a bleed or blockage in one of the arteries supplying the brain, therefore starving it of essential oxygen, thus resulting in death of the cerebral tissue. In medical terms, it is dubbed a c erebrovascular incident, or "CVI".

Like many in the field, the company develops minimally-invasive interventions to address one primary contributor to stroke—carotid artery disease ("CAD"). SILK has pioneered a relatively new approach for managing CAD, known as transcarotid artery revascularization ("TCAR"). Currently, ~70-75% of all CAD treatments are performed using the carotid endarterectomy—that's been around for >70 years, and SILK's main competing procedure. Thus, it aims to establish a new treatment paradigm through its TCAR offering.

The company books revenues entirely from the sale of its TCAR products. These are fed into hospitals and medical centres in the U.S. (no international market just yet). The route to market is through direct sales representatives selling to these institutions. More explicitly:

- SILK's portfolio of TCAR products is purchased individually, with the majority of revenue derived from sales of the ENROUTE neuroprotection system ("NPS") and the ENROUTE stent. Both are used as part of the TCAR procedure.

- Both products are designed to mitigate the risk of knocking off 'plaques' in the carotid artery that can result in the stroke occurring.

I'd also point out that the ENROUTE NPS is contraindicated in several categories of patients. For one, those who aren't candidates for antiplatelet and/or anticoagulation therapy. Typically these are patients with uncorrected bleeding disorders. Hence, the treatment market is potentially limited by this subset of the populous in my view.

2. Recent developments—CMS revised coverage

The elephant in the room here is CMS's decision to cover a broader array of carotid artery stenting ("CAS") in July. This brought SILK's TCAR procedure in line with competing treatments percutaneous transluminal angioplasty ("PTA") and transfemoral carotid artery stenting ("TFCAS"). A final decision of the new rule will be made on October 9th this year.

Understanding the basis of CMS's decision is essential here. It is to broaden the patient access to minimally invasive CAD treatments, and then let the clinical data of each do the rest of the talking to respective referrers/surgeons. In other words, it is putting the patient first. SILK also went as far to say that it will ensure "physicians are held accountable for their outcomes". Net-net, the facts are that:

- Patients may potentially have more access to a generic set of CAD treatments;

- Thereby opening up the gates to patients of a wider socioeconomic and health status (the 'beneficiaries');

- Resulting in a potentially wider addressable market.

Whether or not this wider market applies to SILK is another question. The company seems to think it does. It believes 1) the CMS decision allows for more minimally invasive options, 2) that TCAR is the "gold standard" of these options for CAD, and, therefore, 3) that the decision is actually a tailwind for TCAR procedure growth.

Consequently, it sees CMS' decision as a "rising tide that lifts all boats", so to speak.

The flip side is that greater access to competing procedures could cannibalize TCAR procedural growth. JP Morgan analysts felt this way with a 44% reduction in its price targets to $28/share, citing this reason for the change. Critically, it sees a risk to the company meeting its FY'24 numbers from this. The CMS update on October 9th is therefore critical in gauging SILK's outlook moving forward.

3. Quarterly numbers—financials ratcheting higher, economic drivers are not

Leaving the opinions aside for one second and focusing on the numbers vs. narrative reveals a balanced view of the company in my estimation.

Q2 top-line breakdown

For one, Q2 procedural volumes have compounded at ~34% since 2019, reflected in a 32% compounding growth in quarterly turnover [note: this looks at Q2 for each year from 2019—'23]. It booked $45.3mm in sales last period, up 37% YoY. Procedures were also up ~37% to 6,450 for the quarter.

The revenue per procedure (listed in Figure 2 as "ASP") has held relatively flat on this growth, coming in from $7,450 to ~$7,023 in the quarter. Note, the company's revenue per procedure closely resembles its average selling price ("ASP"), yet typically won't match, given the small breadth between purchases and utilizations.

Nevertheless, more than 3.2x growth in Q2 procedures and $30.4mm additional quarterly revenues in 4 years aren't bad numbers in my opinion.

Figure 2.

Note: Revenue/procedure and ASP are used interchangeably in this instance. (Data: Author, SILK SEC Filings)

To grow procedures and ultimately turnover SILK's salesforce must remain incredibly busy. That involves growing the rep headcount and covering more territories. From 2021—'22 is grew the number of territories from 58 to 70, and ended Q2 with 80 territories. It looks to add another 2—3 territories by yearend based on language on the call. The benefits of adding territories are fairly clear, but it also concentrates its salesforce into more discernible areas, hopefully driving revenue from each.

Gross economic value-added

Historically speaking, since 2020 SILK has been efficient in maintaining an average gross margin of ~73% (using TTM values). It was 71% in Q2, thus slightly below average. Still, gross profit has grown substantially along with the sales growth outlined earlier. This is indeed noted.

Figure 3.

Data: Author, SILK SEC Filings

But a more informed and detailed appraisal of the company's gross profitability is needed. Investors are interested in what the assets and/or capital tied up in the company gets them on a rolling basis. My thoughts on SILK's performance here are mixed.

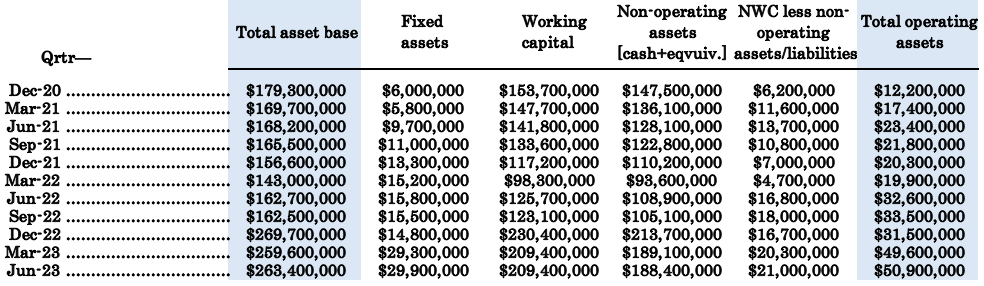

On the one hand, the company exhibited asset growth of $84.1mm over the testing period in Figure 4 to $263.4mm. Correspondingly, the gross return on capital (gross profit scaled by total assets) has pushed from $0.30 to $0.44 for every $1 in assets [Figure 5]. On face value, you'd call this a success, and evidence of a company creating value for its shareholders at the gross level.

The issue I have here is that over time, the overwhelming majority of SILK's assets have been tied up in working capital—specifically, in cash + marketable securities. These aren't even operating assets, despite the optionality each item provides when cash is needed to deploy.

You can see in Figure 4 the mix of fixed assets to working capital SILK booked each quarter from yearend FY'20. Furthermore, you can also observe the working capital less cash + marketable securities, and what I'd dub as 'operating assets' in the final column. In Q2 FY'23 for example, the difference in total assets to operating assets was $263.4mm to $50.9mm. Otherwise, $188.4mm tied up in cash et al.

Figure 4.

Data: Author, SILK SEC Filings

{kind=link}

This opens up an interesting debate. In one view with SILK you've got a capital-light compounder, generating growth in gross income off a relatively thin operating asset base. In fact, the gross capital return off its operating assets is seen in Figure 5, using rolling TTM values. Effectively, it saw ~$2.30 for every $1 in operating assets last period, slightly down from $2.56 the year prior. This is quite a number, and does suggest SILK can generate sales and gross profits with low capital intensity. Keep in mind, these are not earnings, and thus don't necessarily create shareholder value.

In another view, the question is posed: why all the surplus cash? 71.5% of total assets in Q2 to be exact, with just 28.5% invested as capital that produces business returns.

Companies are tasked with creating value for their shareholders as a secondary function to their existence in my opinion (the first would be to solve problems/provide needs). They do this by reinvesting excess cash into opportunities to grow the business. There are many ways to achieve this. But it all hinges on 1) having the surplus cash flow to reinvest, and 2) equally, the opportunities to deploy growth capital in the first place.

Without point (2), there won't be much capital appreciation for shareholders, not for SILK anyway. If you take the company's ability to generate gross economic value for its owners—i.e., you, the shareholders—as a function of the gross return on capital, and the amount it reinvests at this return, SILK hasn't added much value over the last 3-years in my opinion. It may be buffering for a period of foreseeable losses into the next few years, but still, it is holding too much cash to suggest there are multiple opportunities for it to build more inventory, and then sell this to its customers, based on market demand.

I've calculated the opportunity cost to gross capital returns in Figure 5 simply as the gross return on operating assets less those scaled by total assets. From 2020 to date, the opportunity cost of holding cash vs. deploying it into the business has reduced from $4.12 to $1.86. The decline makes perfect sense, given the higher cost of capital, and the higher returns (interest) achieved on cash + marketable securities like UST's and Treasury bills since 2022.

Nevertheless, the tension points remain—why isn't SILK redeploying its cash into the business, and what does this mean? My estimations are that it either has no major opportunities to do so, or, more likely, the demand for its core offering isn't there (yet) to drive inventory purchases and production capacity. This speaks to the productivity of its sales force, the market's utilisation of the conventional standard of care, and what SILK plans to do about each of these points.

These, to me, are risks that simply cannot be overlooked.

Figure 5.

Data: Author, SILK SEC Filings

4. Guidance ranges point to similar expansion rate

Management has made it clear that it aims to penetrate the CAD market by taking on the current standard of care. Looking at this in closer detail, it notes that ~75%—80% of the market's procedure volume is still made up of cardiac endarterectomy ("CE"), TCAR's major competing procedure, so to speak. You should know that CE has a tremendously low periprocedural stroke rate, making it the procedure of choice for many. It has also been around for ~70 years, as mentioned earlier.

If TCAR can't beat CE on safety or efficacy data, then it boils down to procedural volumes. SILK is effectively trying to steal market share from these providers. Such a bold move will require a mammoth effort from its sales team and from the procedure's efficacy.

To that effect:

- Management project $184mm in revenues this year at the upper end, calling for ~33% YoY growth. This guidance is raised by the amount of the Q2 earnings beat.

- To get there, it looks to 25,000 total procedures for the year, on a c.$7,000 revenue/procedure.

- It also eyed 170,000 aggregate CAD treatments performed in the U.S. last year, thus, SILK would have 15% of the CAD treatment market if it hits 25,000 procedures on this total.

The CMS decision outlined earlier no doubt has some impact on SILK's growth prospects in my view. You can't deny that more competition will in some way shake things up. Whether this is for the positive or the negative is the unanswered question right now.

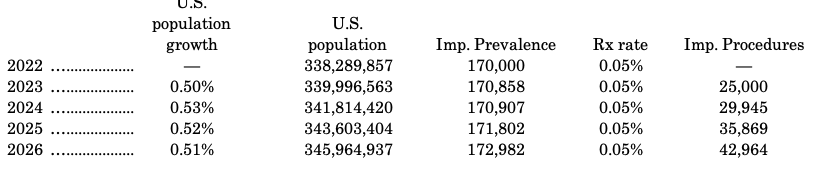

Some basic assumptions moving forward provide a reasonable picture to work from. U.S. population growth is estimated at ~50bps per year into FY'26, potentially reaching 345.9mm by then. At present, it is 338.3mm. Thus, the implied prevalence of 170,000 CAD treatments is an implied treatment rate of ~0.05%. Anchoring these assumptions into FY'26 we get an implied treatment prevalence of 172,982 CAD treatments performed by all purveyors in the U.S.

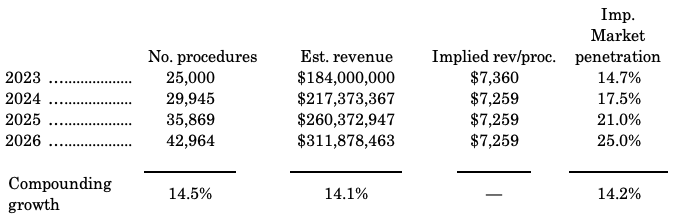

I've run the scenario where SILK doesn't lose meaningful market share from the competing surgeries discussed. I've also assumed an implied revenue/per procedure of $7,259 per year, the quarterly average from FY'19—Q2 FY'23. Keep in mind this is a basic calculus to observe the company's directory and I'm hoping to be ~80% of the way there with my assumptions, but I'm very cognizant of the exogenous risks at play.

With these numbers, the implied model spat out $217.4mm in turnover next year, stretching to $260.4mm the year after. This correlates to 21% market penetration from 35,870 procedures. For FY'26, ~43,000 procedures on $311mm in revenue. Otherwise, 14% compounding growth to each from this year into FY'26.

Figure 6. Implied estimates from market modelling

Note: Several assumptions are anchored to form these outputs. Changes to the implied revenue/procedure and prevalence numbers are the main variables that would change this outlook. (Data: Author)

{kind=link}

Figure 7. Implied estimates from market modelling

Note: Several assumptions are anchored to form these outputs. Changes to the implied revenue/procedure and prevalence numbers are the main variables that would change this outlook. (Data: Author)

{kind=link}

Valuation and conclusion

Investors are attempting to unload SILK stock at >5x book value as I write. Keep in mind, most of that net asset value is comprised of cash, something you'd strip out when purchasing an entire company, and a non-operating asset as we've seen. I can't advocate to pay this. Not with what's been discussed on the company's capital budgeting, and the exogenous threats to its revenue growth via the CMS decision.

Say you're valuing SILK as a function of sales—you're still paying >4x forward. At 4.2x FY'23 sales, factoring in the sales growth of FY'23 and FY'24, I'm getting a 'price-sales-growth' ratio of 10.18x at the current market cap of $778mm [ (778/184)/0.42 = 10.18]. To me, this is wildly overvalued, even though it is a less-common metric. In any sense, SILK is not selling cheaply in my opinion. And I'm not prepared to pay a premium at this stage.

Figure 8.

Data: Seeking Alpha

In short, when thinking in combinations and permutations, there are a number of potential scenarios for SILK moving forward. In my tenets of first principles investing, I prefer companies where the probabilities are more binary—they are either growing, or, they are growing rapidly. This isn't the case here. Procedural volumes and sales have been turning over at higher rates, for sure. But the overwhelming amount of cash yet to be redeployed tells a different story. If you read between the lines, it makes one question why the capital hasn't been put to work.

For further details see:

Silk Road Medical: Unsure On Economics Given List Of Probabilities (Rating Downgrade)