UHAL - Silver Beech Capital LP Q1 2023 Quarterly Letter

2023-05-02 03:00:00 ET

Summary

- Silver Beech is a value-oriented, fundamentals-driven investment firm that targets high-quality but misunderstood North American businesses and deep value opportunities.

- Recent fear in the banking system had a short-term negative impact on Silver Beech’s Q1 2023 performance.

- It is possible other banks could fail or be permanently impaired, especially those with banking models and clients similar to those of SVB and Signature.

Dear Fellow Investors and Friends,

We write Silver Beech Capital, LP's ("the Fund" or "Silver Beech") inaugural quarterly letter with genuine pleasure. Our January letter celebrated Silver Beech's launch and described our investment strategy, objectives, core values, and partnership culture. In this quarterly letter and those to come, we will provide updates on Silver Beech's performance, holdings, and operations.

For this quarter, we have written about four of the Fund's larger holdings: ECN Capital ( ECNCF ), U-Haul ( UHAL ), Ally Financial ( ALLY ), and First Citizens Bank ( FSDK ). We also explain why we exited a position in Green Brick Partners ( GRBK ).

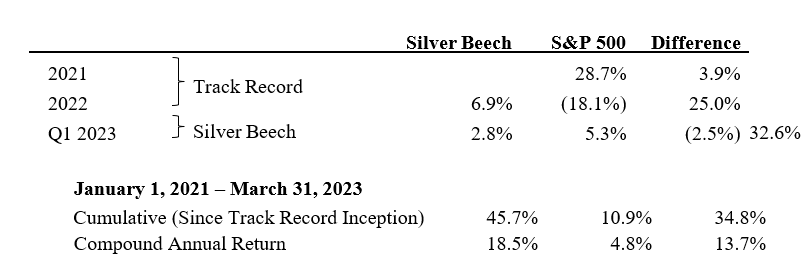

The estimated first quarter of 2023 and historical net performance for Silver Beech is presented below.

Performance Summary:

{kind=link}

Returns presented above for Silver Beech are net of 1% management fee and 20% incentive fee above a 6% hard hurdle since inception (January 11, 2023). Each Investor's actual performance will vary depending on the timing of their contribution(s) and fees. Returns for the S&P 500 include dividend reinvestment. S&P 500's Q1 2023 returns begin January 11 to match Silver Beech's inception. Please see additional disclosure.

Recent fear in the banking system had a short-term negative impact on Silver Beech's Q1 2023 performance. Silver Beech has holdings in resilient banks (Citigroup ( C ), Ally Financial, and First Citizens Bank) at compelling valuations that offer a substantial margin of safety and which were fundamentally unaffected by recent banking events. As a result, we are very optimistic about the Fund's go-forward performance and note that the Fund's banking positions recovered shortly after quarter-end.

In March, Silicon Valley Bank ("SVB") (SIVBQ) failed due to a venture capital-led bank run, and two days later, Signature Bank (SBNY) ("Signature") was closed by the FDIC. We would typically refrain from commenting on companies not held by the Fund, however, given Silver Beech's bank holdings, we have decided to share our views on recent events in the banking system.

Over 10,000 banks have failed in the United States since the Civil War. A bank's failure does not necessarily indicate an oncoming banking crisis. Below, we briefly explain why we think SVB and Signature failed and why their failures are contained and not emblematic of a "banking crisis."

In the bull market of 2020 and 2021, SVB and Signature feasted on the cheap deposits of their customers. They also neglected a core principle of prudent banking: asset-liability duration matching. SVB and Signature overestimated the stickiness of their deposits and did not maintain appropriate liquidity positions. In March, both banks had to rapidly sell assets at losses when customers withdrew their deposits, leading to further depositor concern and withdrawals, and ultimately a bank run.

Within the banking system, SVB and Signature were outliers. For example, in October 2020, JPMorgan Chase's respected CEO Jamie Dimon emphasized the importance of duration matching and preparing for interest rate rises: "we're not going to invest in stuff making 50, 60 or 70 basis points so we get a teeny little bit more net interest income." On an earnings call a few days later, SVB's CFO said, "our treasurer goes home tired every single day... the bucket continues to be refilled with additional liquidity and we plan on continuing to deploy it." Indeed, while JPMorgan Chase ended 2020 with a disciplined capital position but a modest 11% return on equity, SVB posted a superior 17% return on equity. Like Mr. Dimon and most bank CEOs, we believe banks should be managed for solvency at the expense of short-term profitability. SVB and Signature appear to have prioritized short-term profits; they were the proverbial hogs in the adage "pigs get fat, hogs get slaughtered." SVB took a particularly cavalier approach to risk management: in 2022, SVB operated without a Chief Risk Officer for 8 months, even as its deposit base shrank 8.5% year-over-year.

It is possible other banks could fail or be permanently impaired, especially those with banking models and clients similar to those of SVB and Signature. But after careful study of national banking and credit data, we have found little evidence of meaningful deposit runs or emergency borrowings at other banks outside of this select group (despite breathless headlines). We have concluded that in the near term, fear in the banking system could tighten financing into the real economy (which might simply mitigate the need for the Federal Reserve to do the tightening itself through more rate hikes), but there is no "banking crisis."

Portfolio Update

ECN Capital Corp. (TSX: "ECN")

ECN Capital Corp. ("ECN") is a small-capitalization specialty finance holding company that originates, manages, and advises credit portfolios within three distinct platforms: (1) Triad, a scaled consumer lender in the manufactured housing ("MH") market; (2) SourceOne & Intercoastal, consumer lenders in the recreational vehicle ("RV") and marine markets; and (3), RedOak, an inventory finance lender, primarily for dealers that offer consumer access to Triad, SourceOne, and Intercoastal's credit products. All three platforms are asset-light businesses with significant long-term growth potential. Despite being listed on the Toronto stock exchange, ECN operates exclusively in the United States. We believe ECN's intrinsic value is more than 70% greater than its March 31 share price.

ECN sits at the nexus of credit relationships between funding partners (banks, insurance companies, etc., who fund the credit on their balance sheets), dealers (who sell products like MHs, RVs, or boats in physical or online stores), and consumers (who purchase the MH, RV, or boat, financed by credit originated by an ECN platform). ECN and its counterparties are regulated by many different entities. We believe this operating complexity and regulatory compliance require specialized knowledge that creates an important economic moat.

In this letter, we focus on ECN's crown jewel, Triad, which accounted for over 90% of adjusted

EBITDA in the final quarter of 2022. We estimate that Triad will account for ~75% of adjusted EBITDA in 2023. We wouldn't usually analyze companies using adjusted EBITDA but do so here considering ECN's de minimis economic depreciation, and to compare cash flows through time unburdened by interest expense (each platform utilizes different amounts of leverage depending on platform maturity and product), tax treatment, and corporate G&A expense.

ECN acquired Triad in December 2017. Triad grew originations from $525 million of MH loans in 2018 to $1.4 billion in 2022; 2.6x origination growth in four years, or a 27% compound annual growth rate ("CAGR"). We estimate the manufactured housing market grew sales volume at a 21% CAGR over the same period, meaning Triad took market share. Over the same period, Triad expanded its EBITDA from $22 million (a 44% margin) in 2018 to $91 million (a 54% margin) in 2022. This EBITDA expansion of 4.2x in four years indicates Triad's market share gains were highly profitable.

Triad's credit products are also profitable for funding partners. Our industry knowledge of leveraged loans and real estate informs our view that MH consumer credit ranks as one of the most attractive credit products for investors today. MH loans typically price ~250 basis points above traditional 30-year mortgage rates despite shorter duration. We believe the continued attractiveness of MH credit pricing is driven by (i) difficulty for entrants to deploy substantial capital into a smaller market versus traditional 30-year mortgages; and (ii), less competition due to manufactured housing's oligopolistic market structure (Berkshire Hathaway's ( BRK.B ) ( BRK.A ) wholly-owned MH lenders 21st Mortgage and Vanderbilt have about 50% market share).

In addition to economic moats, strong continued growth, and attractive credit products that have driven the company's strong returns on capital, we believe ECN is an attractive investment because:

- Management Track Record: We have confidence in management because they have a strong track record of performing for shareholders. Since ECN's inception in September 2016, ECN shareholders have earned a ~23% total return CAGR (versus ~12% total return CAGR for the S&P 500). ECN's CEO, Steve Hudson, owns ~6% of the company's outstanding shares.

- Attractive Valuation: What valuation is appropriate for a high-growth, asset-light business with 50%+ adjusted EBITDA margins operating in an oligopolistic market with a strong management team? Taking ECN's lowest EPS guidance estimate for 2023, as of March 31, ECN trades at 12x estimated earnings, whereas the S&P 500 trades at 20x estimated earnings. We believe ECN's intrinsic value is at least 70% greater than its share price.

- Near-Term Strategic Review Process: On March 7, ECN announced a "review of strategic alternatives to maximize shareholder value" due "to interest that has been received." We would be thrilled if ECN was able to maximize value in this near-term process, however, we are also happy to own ECN for the long term based on our articulated view of the company's profitable growth and strong management.

U-Haul Holding Company (NYSE: "UHAL"; "UHAL-B")

U-Haul Holding Company ("U-Haul") is North America's largest do-it-yourself moving company, one of the largest owners of self-storage real estate in the United States, and a high-quality business that has grown its market-leading position for decades by putting customers first. U-Haul is one of North America's most recognizable brands and can be thought of as a royalty on consumer moving. All else equal, we prefer to invest with owner-operators as their economic incentives are aligned with shareholders. The Shoen family controls U-Haul with about 50% of the voting common stock. Joe Shoen is U-Haul's CEO. Joe's father, Leonard Shoen, founded U-Haul in 1945. We believe U-Haul's intrinsic value is more than 40% greater than its March 31 share price.

U-Haul's consumer moving products include truck, van, cargo trailer, moving box, self-storage real estate rentals, moving insurance, packing supplies, trailer accessories, and an online marketplace for moving labor. U-Haul also sells WebSelfStorage, a web-based platform for self-storage facility management that connects users to U-Haul's network of 5,000+ owned, operated, or affiliated self-storage facilities. Our channel checks and scuttlebutt research inform our view that U-Haul's moving products and services are second to none in customer experience and value proposition.

U-Haul holds an unassailable market position in a mature but growing industry, where the company's vast distribution network and preference to pass lower costs to customers act as strong economic moats. U-Haul's products can be accessed at over 23,000 locations (2,000 U-Haul owned / 21,000 independent dealer locations). Recognizing the power of its distribution network, U-Haul began offering propane tank refills at its stores in 1984. In just three years, by 1987, U-Haul was the largest propane retailer in the United States! Further, U-Haul's customer-focused approach drives loyalty and market share gains, sustaining a virtuous circle of lower prices and increased market share. It would be expensive, difficult, and require decades of commercial discipline for any competitor to challenge U-Haul's market position.

In April 2022, U-Haul's Board of Directors formed a special committee to enhance "the marketability and liquidity of the Company's stock." The committee acted quickly. In October 2022, the company changed the name of its parent company from "Amerco" to "U-Haul Holding Company", did a 10-for1 stock split with nine shares of non-voting common stock and one share of voting stock distributed to existing stockholders, and announced a dividend on the new non-voting stock. U-Haul's decisive actions piqued our interest and helped convince us that U-Haul was committed to creating shareholder value by helping public markets recognize the company's intrinsic value.

We believe U-Haul's shares are undervalued. Our variant view is driven by:

- Undervalued Asset (Self-Storage Real Estate Portfolio) : U-Haul owns a 55 million square feet self-storage real estate portfolio. We conservatively value this real estate at $10 billion [1] , roughly equal to U-Haul's current market capitalization. Valuing the real estate at $10 billion implies investors get the rest of U-Haul's impressive business (trucks, equipment, brand/customer goodwill) for less than 5x after-tax operating earnings.

- Understated Earnings Power : GAAP accounting understates U-Haul's earnings power. GAAP depreciates U-Haul's self-storage real estate too aggressively, resulting in GAAP earnings that are 10%+ lower than true earnings power. GAAP approximates maintenance capital expense to depreciate U-Haul's trucks and equipment, but it is not an appropriate estimate for real estate.

- Strong Returns on Capital : U-Haul generates sustainable 11%+ after-tax returns on capital despite the capital-intensive and commodity nature of its business. This is important because the company is currently investing all operating cash flow into growing its self-storage real estate portfolio, and its truck and equipment fleet.

- Attractive Valuation : As of March 31, U-Haul traded at 11x trailing GAAP earnings and 6x trailing EBITDA, a low valuation for a business of this quality and durability, and a substantial discount to the sum of its parts. We believe U-Haul's intrinsic value is at least 40% greater than its share price and is compounding at 10% annually driven by profitable growth.

Ally Financial (NYSE: "ALLY")

Ally Financial ("Ally") is the largest all-digital bank in the United States, the 22nd largest bank by total assets ($192 billion), the nation's leading prime auto lender (with 6.5 million consumer customers), and leading auto floorplan lender (with over 23,000 dealer relationships). Most of Ally's assets are auto loans and finance receivables, but Ally also offers consumer protection insurance through its dealer channels and operates small corporate and mortgage lending businesses. Notably, Ally also offers some of the industry's most competitive deposit products: Ally was awarded "Best Checking Account", "Best Saving Account", and overall "Best Online Bank" by third-party reviews and was the first large bank to eliminate overdraft fees. We believe Ally's intrinsic value is more than 40% greater than its March 31 share price.

Ally evolved from the auto finance unit of GMAC, emerged from GMAC's restructuring as a bank holding company, and rebranded, before going public in 2014. Since then, Ally has transformed itself from a wholesale-funded, captive finance company into a full-service retail-funded automotive finance and insurance provider by steadily gaining retail deposit market share. Today, Ally's balance sheet is 85% funded (versus 43% funded in 2014) by $152 billion of deposits (versus $58 billion in 2014) across 4.4 million depositors (versus 900k depositors in 2014). Over 90% of Ally's deposits are FDIC-insured, more than any other $100+ billion-asset bank in the United States. Ally's massive insured deposit base is stickier and more resilient to depositor fear of a bank run than other regional banks.

Ally's funding transformation has driven structural improvement in net interest margins ("NIMs") from the mid-2%s to mid-3%s. Although recent interest rate increases will pressure Ally's NIMs in the short term as deposit rates rise faster than can be passed through to loans, Ally's moderate-duration assets will capture recent rate rises and should drive strong NIMs of 3.5-4.0% by 2024, and ultimately returns on equity of 12%+.

Recently, market participants have become concerned by broadly rising auto loan charge-offs and delinquencies. There are also concerns that used car prices (used cars are collateral for many of Ally's loans) have declined from COVID's supply-constrained highs. However, despite this negative macro sentiment, our analysis of Ally's balance sheet position is favorable, where 90% of Ally's auto loan book is "prime credit" (FICO score over 620). And although Ally "over-earned" in 2021 and 2022 when credit losses did not materialize, Ally has earnings power to offset credit losses in 2023 and 2024 should they exceed existing loss reserves.

Moreover, Ally's balance sheet already reflects a 30% decline in used car prices between 2021 and 2023 as its base case underwriting assumption. Ally has reserved ~3.6% of its auto loans for losses. We do not believe Ally's credit losses will exceed those already underwritten. To help contextualize the conservatism of Ally's ~3.6% auto credit loss reserve, we note that during the Global Financial Crisis ("GFC") of 2007 and 2008, GMAC auto finance credit losses peaked in 2009 at ~2.3%.

We believe Ally is an attractive investment today because:

- Resilient Deposit Base & Assets: Ally's deposits are large, diverse, and insured. Ally has moderate duration assets and no hold-to-maturity book. Ally's balance sheet is resilient against banking sector concerns over asset-liability duration matching.

- Auto Credit Losses Already Provisioned: Ally has appropriately reserved its balance sheet for potential losses. Moreover, Ally's earnings power can offset excess credit losses (which we don't believe will significantly materialize).

- Attractive Valuation: At $25.49 per share as of March 31, Ally trades at ~85% tangible book value and a mid-single digit price-to-earnings ratio on trough 2023 earnings. We believe returns on equity of 12%+ remain achievable for Ally, implying intrinsic value above $36 per share and offering 40% upside from March 31 price levels.

First Citizens Bancshares, Inc. (NASDAQ: "FCNCA")

First Citizens Bancshares, Inc. ("First Citizens") is a 130-year-old, Raleigh, NC-based, large regional bank operated by the aptly named Holding family. Robert Powell Holding, who joined the bank as an assistant cashier in 1918, became president in 1935. Frank Holding Jr., Robert's grandson, has been Chairman and CEO since 2008 (preceded by his father, who held the role for over 50 years). Frank and his family own over 20% of First Citizens stock and have nearly 50% of the voting power.

We have tracked First Citizens for several years. Frank is a world-class banker who deeply understands the rewards of operating within limits during periods of excess, or in his own words, "taking the road less traveled." First Citizens reaped the fruits of Frank's discipline after the GFC. First Citizens entered the GFC with a strong capital position and high-quality book of assets and took no Troubled Asset Relief Program funds. Frank then led First Citizens to acquire 20 banks in the aftermath of the crisis (six failed banks almost immediately after the GFC and several failed banks thereafter). Frank has consistently expanded the First Citizens franchise in a cost-effective manner by acquiring failed banks.

We purchased shares of First Citizens after First Citizens acquired certain assets and liabilities of the failed Silicon Valley Bank ("SVB"), including 17 SVB branches and the SVB franchise, from the FDIC. Although public markets immediately recognized the acquisition's accretion to First Citizens' underlying value (shares rose over 50% on the day of the deal's announcement), we think First Citizens is in an even superior capital position than the public market has recognized.

First Citizens acquired $110 billion of SVB's assets ($35 billion cash, $72 billion loans, and $3 billion of other assets). The acquired assets were funded by $94 billion of liabilities ($56 billion of deposits, $3 billion in other liabilities, and a 5-year $35 billion loan from the FDIC with a 3.5% interest rate). The $16 billion plug between SVB's assets and liabilities equals the discount that First Citizens received from the FDIC. We would argue this is one of the most profitable and asymmetric bank deals of the modern era.

First Citizens ended 2022 with $8.8 billion of common equity. Clearly, the $16 billion discount for SVB created substantial accretion to First Citizens' common equity. The acquired SVB loans are primarily short-duration capital call lines with near-zero loss history, not riskier venture loans that SVB was infamous for when it was solvent. After acquiring SVB, First Citizens has substantial cash reserves, an FDIC back-stop, and credit loss-sharing on SVB assets. Based on our valuation analysis, which includes First Citizens incurring a "bargain gain" tax and burdening SVB loans with conservative loss estimates, we believe the SVB acquisition accreted over $8 billion to First Citizen's common equity. First Citizens also benefits from downside protection and loss-sharing provided by the FDIC.

If our valuation analysis is correct, and First Citizen's common equity rose by more than $8 billion, or nearly 100% of First Citizens' pre-transaction common equity, then the shares are materially undervalued. We look forward to investing alongside CEO Frank Holding and we have confidence he will continue to create value for shareholders.

Exited Position - Green Brick Partners (NYSE: "GRBK")

Green Brick Partners is a small-capitalization homebuilder with a leading market position in Dallas-Fort Worth, TX, and Atlanta, GA. We like Green Brick for its conservative land underwriting strategy and focus on high-growth markets, pristine balance sheet, attention to capital allocation, and management's shareholder alignment. These are rare features in the boom-bust world of homebuilding. Indeed, despite its smaller size and low debt level, Green Brick earned among the highest gross margins and returns on equity among homebuilders in 2021 and 2022.

We are long-term investors and expect that orientation to be reflected in our investment holding period. The first quarter offered a rare exception to the rule: we fully exited our holding in Green Brick after seeing our investment thesis play out in less than one month. We exited our position as we believe the company's current valuation offers less margin of safety compared to the Fund's portfolio and other opportunities. We continue to monitor Green Brick on our watchlist. We think the company is well-run and will benefit from the structural underbuilding of for-sale residential homes that have occurred since the GFC.

Conclusion

We welcome new investors that have committed to joining the investment partnership. Thank you for the trust that you have placed in us. We also greatly appreciate your referrals and capital introductions. We look forward to providing you with the next update for the second quarter of 2023. Please do not hesitate to contact us.

Silver Beech Capital, LP - Fund Summary as of March 31st, 2023

| Holdings: |

| Name |

| Ticker |

| Sector |

| Description |

| Ally Financial |

| ALLY |

| Credit Services |

| Digital financial services company that provides banking, auto finance and insurance services, credit cards, and advisory services to consumers. |

| Builders FirstSource |

| BLDR |

| Building Products & Equipment |

| Largest U.S. supplier and leading manufacturer of building materials, manufactured components, and construction services to professional builders. |

| Citigroup |

| C |

| Banks (Diversified) |

| Global diversified financial services company that primarily provides consumers and institutions with banking, advisory, trading, and treasury services. |

| ECN Capital |

| ECN |

| Credit Services |

| Asset-light holding company that originates, manages, and advises on consumer and inventory finance credit portfolios for its funding partners. |

| First Citizens |

| FCNCA |

| Banks (Regional) |

| Regional bank based in Raleigh, NC that primarily provides banking, lending, and advisory services to consumers and small & middle-market companies. |

| Microsoft |

| MSFT |

| Software (Infrastructure) |

| Leading global developer and provider of software, technology services, devices, and solutions. Products include Microsoft 365, Teams, LinkedIn, and Azure. |

| U-Haul |

| UHAL |

| Rental & Leasing Services |

| Largest DIY moving and storage company in North America. Specialized rental products include trucks, trailers, self-storage real estate, and portable storage. |

| Winnebago |

| WGO |

| Recreational Vehicles |

| North American manufacturer of RVs and marine powerboats under the Winnebago, Grand Design, Chris-Craft, Newmar, and Barletta brands. |

| Fund Composition by Market Capitalization: |

| Weight |

| Large Cap (greater than $5 billion) |

| 72.2% |

| Mid Cap (greater than $1 billion) |

| 12.0% |

| Small Cap (less than $1 billion) |

| 15.6% |

| Cash |

| 0.1% |

| Total |

| 100.0% |

{kind=link}

Returns presented above for Silver Beech are net of 1% management fee and 20% incentive fee above a 6% hard hurdle since inception (January 11, 2023). Each Investor's actual performance will vary depending on the timing of their contribution( s) and fees. Returns for the S&P 500 include dividend reinvestment. S&P 500's January 2023 returns begin January 11 to match Silver Beech's inception. Please see additional disclosure.

IMPORTANT DISCLOSURES

Silver Beech Capital Management, LLC ("Silver Beech") is a New York limited liability company that serves as the investment manager to Silver Beech Capital, LP (the "Fund"), a Delaware limited partnership. The principals of Silver Beech are James Hollier, who serves as the portfolio manager and managing partner of the Fund, and James Kovacs, who serves as the managing partner of the Fund.

All performance results presented herein refers to the performance of an unrestricted investor in the Fund since its inception. Net performance is presented net of the highest performance allocation in effect at the time (20%) above a 6% hurdle rate, the highest actual management fees (1.0%) charged at the time, and net of other expenses, and includes the reinvestment of all dividends, interest, and capital gains. Performance for investors who subscribed on different dates, or who pay different fees would necessarily be different from the performance presented herein. The rate of return is calculated on a "time-weighted" rate of return basis, which minimizes the effect of cash flows on the investment performance of the Fund. All monthly performance data presented herein reflects unaudited data unless otherwise specified, and as such its accuracy cannot be guaranteed. Cumulative returns for the "January 1, 2021 - March 31, 2023" period include the audited returns of Silver Beech's portfolio manager prior to Fund launch. Past performance is not necessarily indicative of future results. All securities transactions involve substantial risk of loss.

The material presented is compiled from sources thought to be reliable, including in certain instances, from outside sources, but accuracy and completeness cannot be guaranteed. Any opinions expressed herein reflect the judgment of Silver Beech and are subject to change.

The information in this letter is for discussion purposes only. Nothing contained herein should be construed as an offer to sell, or a solicitation of an offer to buy or sell any security or investment strategy or a recommendation as to the advisability of investing in, purchasing or selling any security or investment strategy, which may only be made in the Fund's confidential offering memorandum and operative documents (collectively, the "Offering Documents").

Before making an investment decision with respect to the Fund, prospective investors are advised to read the Offering Documents carefully, which contain important information, including a description of the Fund's risks, investment program, fees, expenses, redemption and withdrawal limitations, standard of care and exculpation, etc. Prospective investors should also consult with their tax and financial advisors as well as legal counsel. The Offering Documents are the sole documents on which a potential investor is entitled to rely in evaluating an investment in the Fund. The information in this letter does not take into account the particular investment objectives, restrictions, or financial, legal or tax situation of any specific prospective investor, and an investment in the Fund may not be suitable for many prospective investors. This letter is not intended to be, nor should it be construed or used as, investment, tax, or legal advice.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

[1] Valuing U-Haul's 55 million square feet self-storage portfolio at $10 billion equates to $182 per square foot. This is lower than U-Haul's self-storage peers which trade in public and private markets for more than $250 per square foot.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Silver Beech Capital, LP Q1 2023 Quarterly Letter