CHK - SilverBow Resources: Is The Deal Worth The Debt?

2023-12-06 15:12:39 ET

Summary

- SilverBow Resources, Inc. acquires Chesapeake Energy's South Texas operations.

- The deal is mostly debt for SilverBow Resources, raising concerns about the company's amount of debt even though the leverage is within reason.

- Management plans to hedge production for three years to mitigate price fluctuations and ensure a minimum cash flow.

- The sale to SilverBow from Chesapeake is relatively cheap. However, the acquisition is relatively large for the size of the company. Large acquisitions tend to fail more often.

- Transitioning to more liquids production from natural gas production will increase company profitability.

SilverBow Resources, Inc. ( SBOW ) got exceptional terms by purchasing Chesapeake Energy's ( CHK ) South Texas (Eagle Ford) operations. Chesapeake has spent roughly a year trying to sell. Management has spent time talking up the Austin Chalk, which is the primary focus of the assets at the current time. But the Eagle Ford often has a few more intervals that are highly likely to provide considerable upside potential that is not on the reserve report used by the parties to negotiate a price. The worry here is that the deal is nearly all debt for a relatively small company like SilverBow Resources.

The Deal Details

SilverBow management claims that the ratio of the selling price to EBITDA is around 2.3, with negotiations taking place after SilverBow management waited for prices to decline and stabilize at lower levels from fiscal second quarter 2022. Commodity prices have since strengthened since the deal was announced.

The worry about the debt is not the debt ratio, because that ratio appears reasonable. It is the amount of debt to equity because that is another measurement of risk. The question would be: is there enough stock offerings or part of the deals to keep risk reasonable? So, the risk is a little different in that the amount of debt is aggressive compared to the amount of equity. As the company earns money, that measure will fix itself. Hopefully the company does not go into the next cyclical downturn with perceived extra risk.

Management does have to hedge and intends to hedge 3 years out. There will likely be roughly 20% of production that is exposed to market prices. This will decrease the risk of price fluctuations that could hurt the initial returns on the deal.

Any leveraged deals, especially 100% cash deals, need to deleverage fast in this industry. Having that hedge will likely assure that the deleverage will happen no matter the industry conditions.

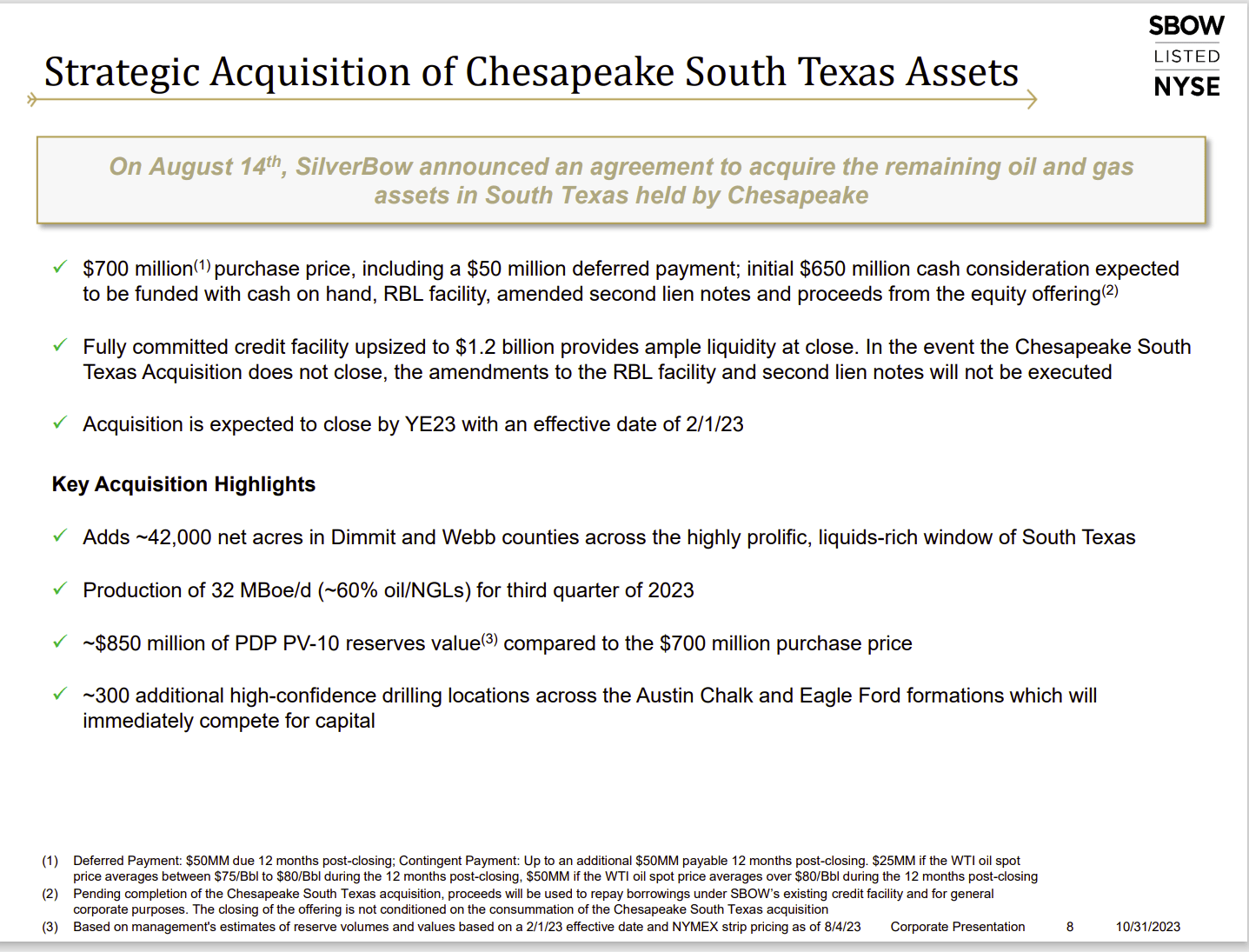

SilverBow Resources Summary Of Chesapeake South Texas Acreage Acquisition (SilverBow Resources Corporate Presentation November 2023)

{kind=link}

But the big deal for what was a natural gas producer is the transition towards more liquids production by purchasing probably one of the premier positions in the Eagle Ford that also had contiguous acreage that the company has long lacked.

This Eagle Ford acreage will not only compete for capital. But it may be the most profitable acreage in the company portfolio. The acreage location is just that good. For this management, the South Texas location is relatively "pure gold," whereas for Chesapeake it was a noncore asset. This company was lucky to be able to get a chance to purchase acreage like this. (For Chesapeake, this outcome could indicate a sales marketing error of some sort.)

There is every chance that SilverBow will spend a fair amount of time increasing profitability of this acreage. It will likely have some material improvements to report to shareholders fairly quickly.

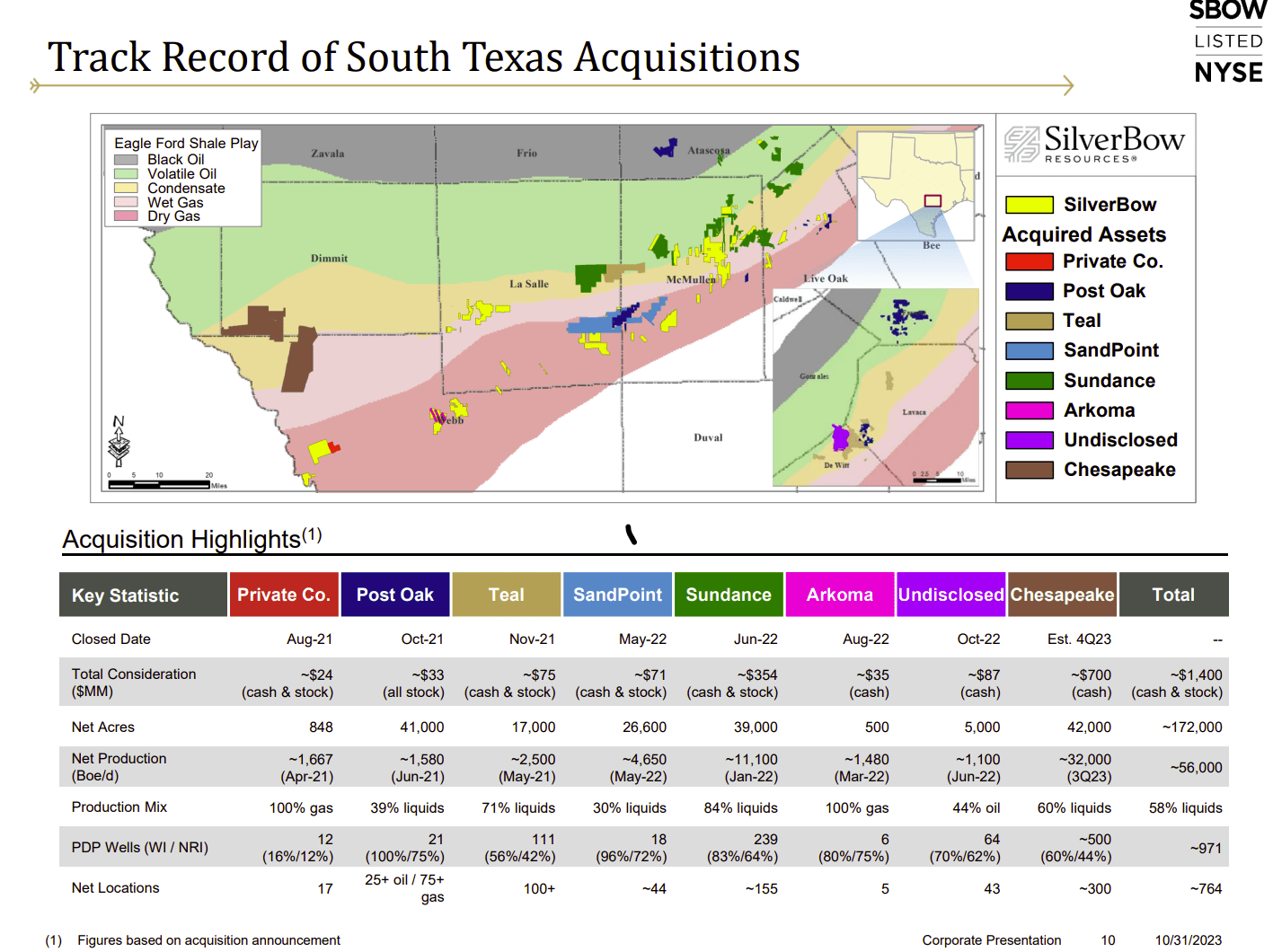

Deals So Far

This deal is easily the largest the company has done to transition from natural gas production to far more liquids production.

SilverBow Resources History Of Acquisitions Since Emerging From Bankruptcy (SilverBow Resources Corporate Presentation November 2023)

{kind=link}

The company has made a significant transition to a far more profitable production mix. Management noted that free cash flow is expected to be in the $20 million to $40 million range for the current fiscal year. Cash flow from operating activities at the 9-month period is about $300 million.

Now once the deal closes, management is going to have to juggle capital requirements with the debt repayment. Given the current free cash flow, management will have to increase that considerably to handle the debt load after the deal closes. A lack of deals and one-time expenses alone should allow free cash flow to increase considerably.

For investors, note that the larger deals prior to this one were generally cash and stock. There is a good chance management should have made plans for several secondary offerin gs to keep the risk level down. There was an offering in September where the company sold roughly 3 million shares. Whether this is sufficient remains to be seen.

Given all the acquisition activity, that is quite possible there will be a lot more free cash flow next year than there is currently. However, large acquisitions like the current one, often have optimization requirements comparable to the size of the acquisition. That could provide a risk factor for the reported outcomes in the next fiscal year.

Offsetting that risk is the material increase in natural gas exporting abilities that will likely strengthen natural gas selling prices over the next couple of years (and probably further out as well).

To get where this company needs to go, management will have to have some very tight controls and be extremely efficient with what it has.

There is also the possibility that management can drill more oil-based production to immediately increase profits and cash flow until natural gas prices strengthen.

Market Worries

SilverBow Resources is a company that filed bankruptcy as Swift Energy back in 2015 after oil prices crashed. Any company that files bankruptcy is likely considered to have a higher chance of filing bankruptcy a second time. Taking on a lot of debt, even if the debt ratio remains within acceptable limits, does little to ease those fears.

In this case, there is a promise by management to pay down the debt or otherwise get the debt ratio to 1.0. But the rapid growth of the company can have its own risks as well. If the whole "new" company does not operate well because some or all of the acquisitions do not meet expectations, there could be some repercussions that affect common shareholders. All the debt has a higher claim to the assets than the common shares.

Similarly, some of the debt issued will be secured. This is another indication that the debt market believes that risks are higher than normal.

Large acquisitions traditionally have a higher failure rate than small acquisitions. This is generally due to the logistics and other challenges facing the acquiring company. When that same large acquisition is made with debt, then Mr. Market has the equivalent of a heart-attack over the potential risk.

Management did back off by selling some stock which will help. The proceeds were in the neighborhood of $100 million in the third quarter as shown on the cash flow statement. Any equity sales for any reason helps the leverage fears. But more equity sales may be required to satisfy the market in the near future. Otherwise, the stock price could languish despite profitability progress until a sufficient amount of debt is repaid.

Key Ideas

Management has done well to grow the company by acquiring more profitable production of liquids. Management has also done well to keep the debt ratio near acceptable levels. The SilverBow Resources, Inc. three-year hedging program will assure a cash flow while somewhat limiting exposure to high prices during the hedging period.

But too many acquisitions in the eyes of the market at a pace deemed by the market as too fast or too large can depress the stock price for a period of time.

Investors who do not mind the risk can consider reading up on this company to possibly invest in the shares. All the recent deals need time to assimilate and optimize (especially the latest deal that has yet to close).

It is particularly important that a company with a bankruptcy already on the record demonstrate that the fast growth can be handled now no matter the management experience. That likely means there is plenty of time for researchers to research the company.

SilverBow Resources, Inc. can be considered a very speculative strong buy given the issues presented above. It would be an advanced situation for those investors with a lot of discipline and experience handling a situation like this. Management appears to be making the right moves. The risk is in accomplishing the goals with all that new acreage (and probably personnel) as well as repaying debt as planned. Most likely, as the plan executes as management is guiding, the risk would come down to more acceptable levels. But that is far from assured.

Many would likely want to watch from the sidelines until there is proof that management is executing as planned and will be able to execute as planned.

For further details see:

SilverBow Resources: Is The Deal Worth The Debt?