SVM - Silvercorp Metals: Misunderstood And Growing Fast

2024-01-04 03:56:33 ET

Summary

- Silvercorp Metals Inc. is trading at a very cheap valuation compared to its peers, despite having a much stronger track record of profitability.

- The company owns 27% of New Pacific Metals, an exciting and undervalued silver explorer and developer.

- Silvercorp is set to grow production from its flagship Ying Mine project by over 20% by FY 2026 via optimization and exploration activities.

- The acquisition of OreCorp is potentially transformative: it is highly accretive on a NAV base, and it provides geographical and metal diversification.

- I expect a substantial re-rate over the next 2-3 years.

Silvercorp Metals Inc. ( SVM , SVM:CA ) is a Canadian mining company with predominantly silver assets located in China (in the Ying and GC mining districts). About 60% of its revenues come from silver, 34% from base metals (lead, zinc), and the rest from gold.

The company is trading at a very cheap valuation. In general, silver miners have performed poorly as of late. This is a consequence of their dramatically compressing margins, as production costs have risen due to inflationary pressures, while the silver price has declined more than 15% from its recent highs because of tightening monetary conditions. Even so, Silvercorp has been particularly affected: its stock price has underperformed the index and many of its most direct peers. The company is currently trading at an EV/EBITDA multiple of just 3.5x (compared to a peer average of around 16x), a P/Adj. Earnings of 13.9x (compared to a peer average of over 90x), and a P/OCF of 5.6x (compared to a peer average of over 32x). This is perplexing because, as the multiples above imply, in reality, Silvercorp is a superior company relative to many of its peers.

Silvercorp has always had a strong focus on profitability. In fact, I consider Silvercorp one of the few investable companies with a focus on silver. Most silver miners have a track record of very poor returns. On the other hand, Silvercorp has consistently been able to earn a return on equity greater than many of its peers, thanks to its superior margins. While many silver miners struggle to consistently generate free cash flow, Silvercorp has largely been cash flow positive, even when the silver price has suffered. It has been able to grow production and replace reserves while simultaneously paying out a dividend. It has achieved this mostly from its internally generated cash flow: not only does the company have no debt, but it has also accumulated a significant cash position of $189 million, which is equivalent to around 42% of its entire market capitalization.

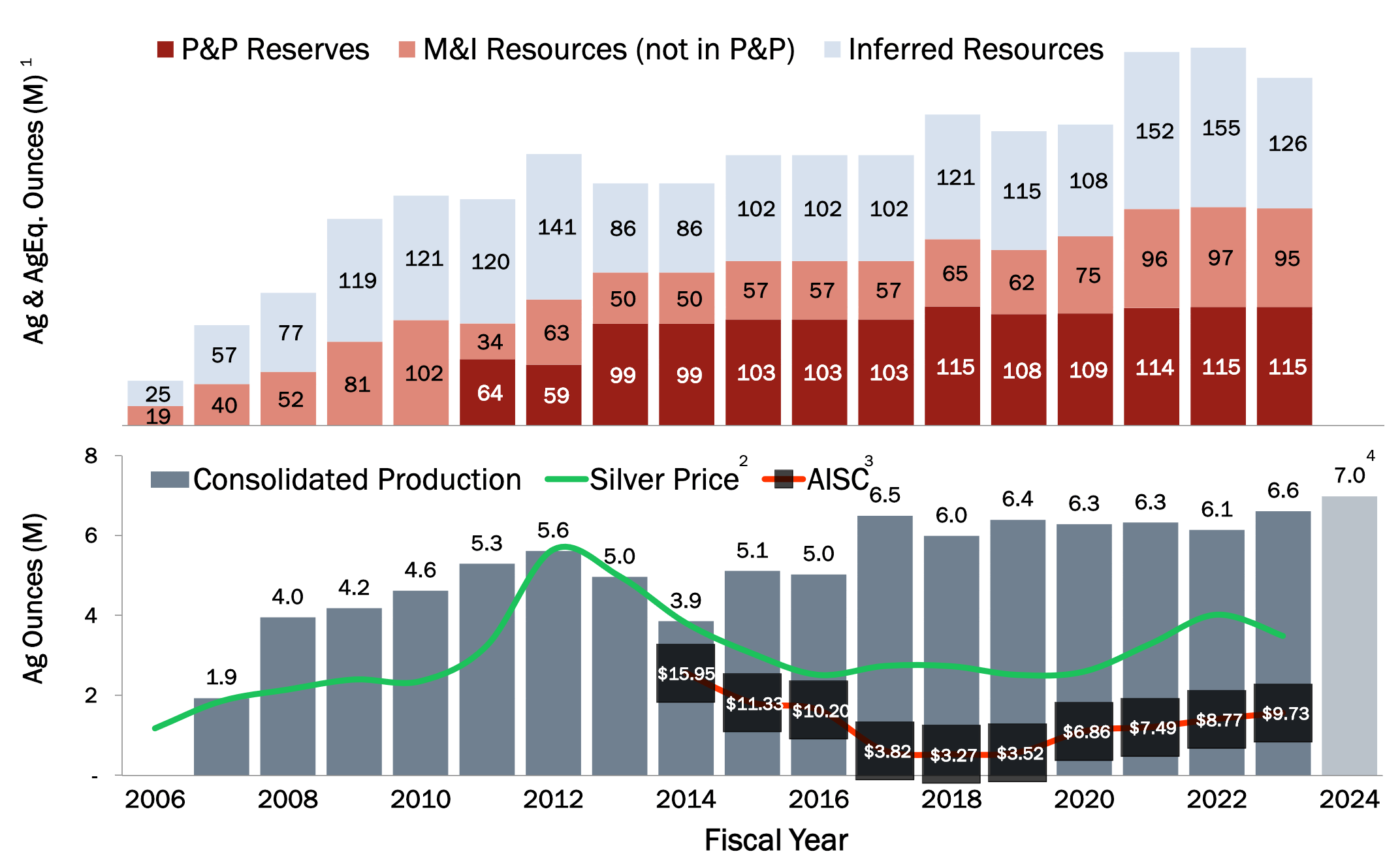

Silvercorp has historically been able to replace reserves and expand production, while maintaining profitability (Company's Presentation)

{kind=link}

Another way to grasp just how cheap Silvercorp is, is through a sum-of-the-parts argument. Starting from its current market capitalization of $450 million, let's subtract $189 million in cash and cash equivalents. Then, let's subtract $125 million, which is the value of its equity investments (as of the beginning of December, including a 27.4% stake in New Pacific Metals). The implied EV of the mining assets is therefore only $135 million.

Over the last 12 months, which, as already mentioned, has been quite a difficult period for all silver miners, the company has still managed to generate almost $33 million in free cash flow. So, even using backward-looking and conservative numbers, the company is trading at a 4x EV/FCF multiple.

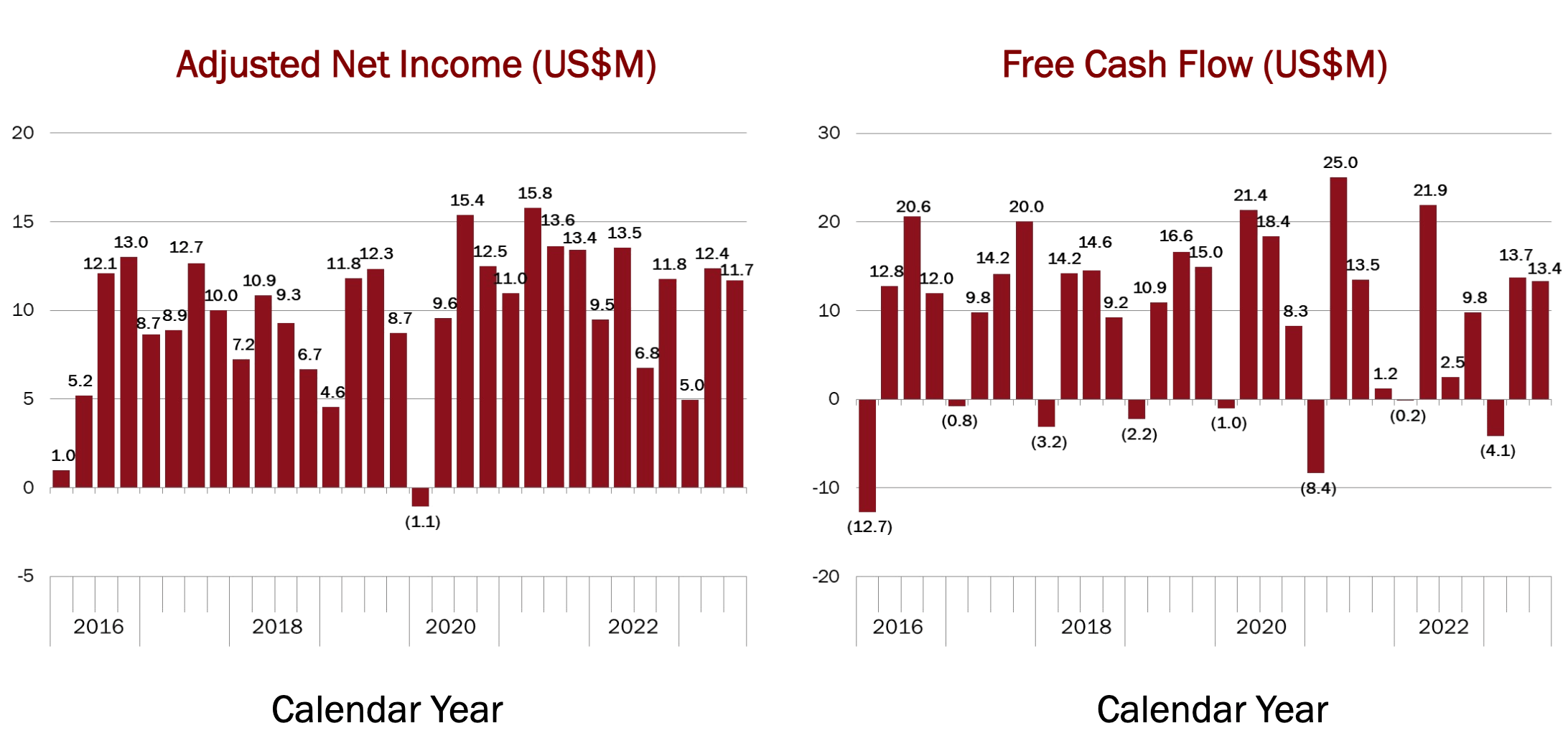

Silvercorp has a solid track record of free cash flow generation (Company's Presentation)

{kind=link}

It should be noted that the situation can only improve from here. For FY 2024, Silvercorp is guiding for a lower AISC of $11.5 per ounce (which puts it in the lowest quartile of silver miners by production costs). It is also expecting to grow its production, from 6.6 million ounces in FY 2023 to 7 million in FY 2024, to about 8 million by FY 2026. This growth is to be achieved via organic growth initiatives, financed through internally generated free cash flow, including different mine optimization efforts, a new tailings storage facility, and mill expansion at Ying Mine, development of the newly-licensed Kuanping silver-lead-zinc-gold project, and the restart of the BYP gold project (currently under care and maintenance).

Moreover, with more than half of its revenues coming from silver, the company is highly leveraged to the silver price. While it is hard to predict how silver will trade in 2024, I would wager that silver is going to trade higher from here. We are already seeing significant energy deflation, which should continue to slow down core inflation, allowing central banks, and the Fed in particular, to stop and reverse their tightening monetary policies. Meanwhile, the fundamental picture for silver remains very positive, with industrial demand projected to grow and the market in a significant supply deficit. From the current level, the downside appears to be limited. But if the silver price started moving up again, then the upside could be significant. Just to return to its all-time high, the stock price should grow by 250%.

What if silver were to continue to trade in a range over the next couple of years? I would argue that, even in this scenario, Silvercorp would prove to be a good investment. Even if silver were to stay where it is, Silvercorp is destined to re-rate sooner or later. This is because over a horizon of 2-3 years, Silvercorp is going to be a dramatically different company. Silvercorp is not just a cheap call option on silver prices.

First of all, as already mentioned, Silvercorp owns more than one-fourth of New Pacific Metals , which I believe is an exciting story in its own right. It is currently trading at a $320 million market capitalization, so Silvercorp’s stake is valued at about $90 million. However, the market is underestimating its potential. New Pacific’s flagship asset is the Silver Sand Project, the largest silver discovery in Bolivia and one of the biggest silver discoveries globally over the last decade. The Silver Sand Project is a large, near-surface pure silver deposit, which could produce over 170 million silver ounces over a 14-year mine life. The existing technical report, dating back to 2022, implies a total all-in sustaining cost of $10.42 per ounce, a pay-back period of 1.9 years, a post-tax IRR of 39%, and a post-tax NPV-5% of $726 million. The costs may turn out to be higher, but the report is assuming a conservative silver price of $22.5 per ounce. Based on NPV, Silvercorp’s stake in the Silver Sand Project would be worth more than $200 million. It should also be noted that, while the Silver Sand Project is its flagship project, New Pacific has two other projects (the Carangas and Silverstrike projects). Over the coming year, an important catalyst would be the completion of the pre-feasibility study, expected in H1 2024. The company is also working to complete an environmental impact assessment study, as well as working with COMIBOL (the Bolivian state mine company) to obtain approval of the signed Mining Production Contract for areas surrounding the project. New Pacific should, therefore, generate over the next few quarters a stream of positive updates, which could help a re-rate of Silvercorp itself.

In the second place, there are various organic growth efforts in the Ying Mine District. This remains the company’s flagship project. The current focus is on improving operational efficiency and productivity via various initiatives. One in particular is the new X-ray transmission ore sorting system, already tested at the GC Mine, to address the higher anticipated dilution associated with shrinkage mining. In addition, Silvercorp is investing in a new mill facility, which will bring processing capacity to over 4,000 tonnes per day, up 60% from the current 2,500 tonnes. This strategic investment aligns well with the projected increase in mine output, which could include the development of the satellite Kuanping project. Moreover, Silvercorp is on track to commission a new tailings storage facility in 2024, which, together with the recently built new paste backfill plant, will support production at Ying beyond 2034. Silvercorp is also investing heavily in exploration at Ying, with over 218 kilometers of drilling this fiscal year. Recent exploration has significantly improved the geological understanding of a series of gold structures discovered back in 2020. In fact, Silvercorp has already started gold production in one of its mines in the Ying mining district, by pouring its first doré bar last September. This is part of an effort to increase gold production, to capitalize on high gold prices and achieve better revenue diversification.

Finally, and most importantly, Silvercorp is looking for growth opportunities in the M&A sector. Thanks to its strong balance sheet and significant experience in developing complex assets, Silvercorp is perfectly suited for acquiring greenfield projects and bringing them into production. Because of the currently difficult financing environment for new developers, the company should finally find a way to put its cash to good use. In fact, in all likelihood, it has just found one.

In August 2023, Silvercorp announced the intention to acquire all outstanding shares of OreCorp, an Australian company that owns an 84% interest in the Nyanzaga gold project in Tanzania (the remaining 16% belongs to the government). The initial offer was for A$0.15 cash plus 0.0967 Silvercorp shares for each OreCorp share. The market didn’t like the announcement, and the share price declined immediately following it. But, given the quality of the project, the acquisition would have actually been extremely accretive on a NAV basis. This is testified by the fact that Perseus Mining tried to contest the acquisition by acquiring a 19% stake in OreCorp and declaring its intention to vote against Silvercorp’s proposal. Since the original deal required a 75% majority, Perseus would have been able to effectively block it. Silvercorp has since then increased the offer to A$0.19 cash plus 0.0967 Silvercorp shares. It has also entered into a new agreement with OreCorp, which only requires a 50.1% majority to pass. It seems very likely that the acquisition will go through this time. OreCorp's share is currently trading very closely to the acquisition price (around a 3% discount at the moment), so the market is also thinking the same.

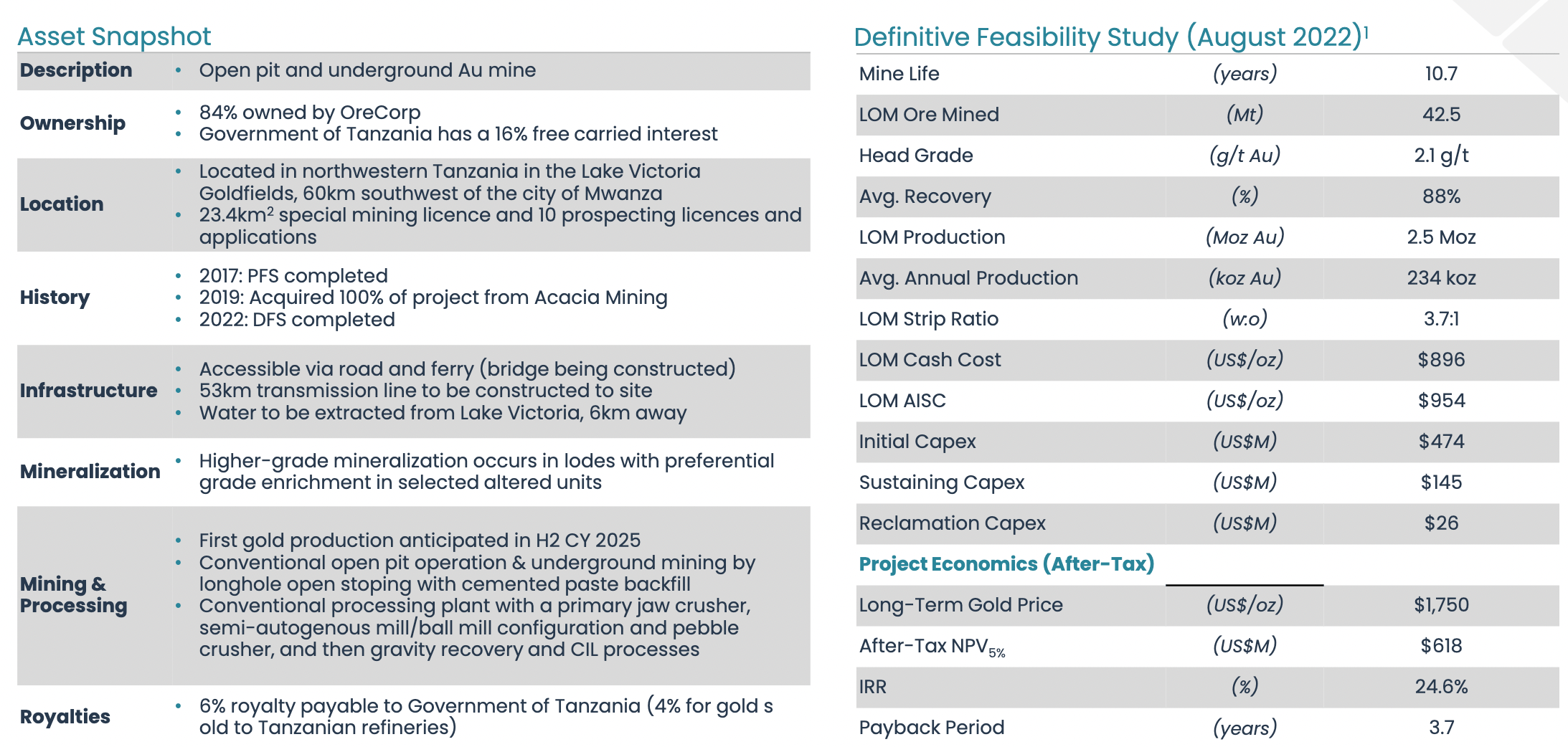

The acquisition of OreCorp offers several advantages. Firstly, it is fully permitted and close to production, with the potential to commence operations as early as H2 2025. The project's economics are robust, as indicated by the Definitive Feasibility Study released in August 2022. The anticipated mine life is 10.7 years, with an average annual gold production of 234 thousand ounces. The all-in sustaining cost (AISC) is expected to be around $950 per ounce, and the initial capital expenditure is estimated at $474 million. Assuming a conservative gold price of $1750 per ounce, the payback period would be 3.7 years, with an IRR of approximately 25% and an NPV-5% of around $618 million. Silvercorp is acquiring OreCorp for approximately $185 million. While the initial capital expenditure is substantial, Silvercorp intends to make optimizations and adjustments to the mine development plan. This includes deferring a portion of the initial capex until later stages, with internally generated cash flow used for payment.

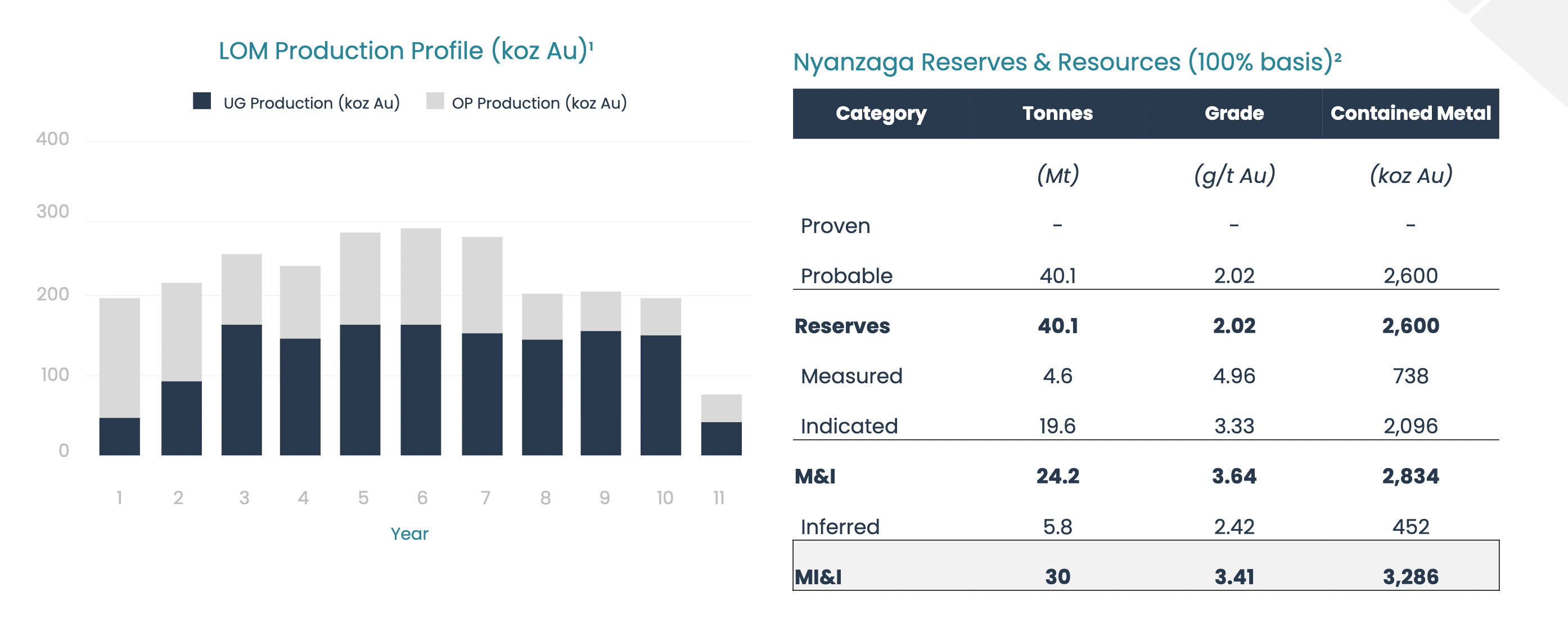

Production profile and Reserves & Resources for the Nyanzaga Project (Company's Presentation)

{kind=link}

{kind=link}

In summary, Silvercorp is currently undervalued due to its exposure to perceived risky jurisdictions (China and Bolivia) and negative sentiment in the silver sector. Nonetheless, Silvercorp represents an exciting growth story driven by both organic and inorganic initiatives, particularly through the acquisition of OreCorp. This acquisition not only provides Silvercorp with metal diversification but also expands its jurisdictional reach. Over the next 2-3 years, Silvercorp is poised to undergo significant transformation. If the company continues to deliver on its various growth initiatives, the market will not be able to continue ignoring it.

For further details see:

Silvercorp Metals: Misunderstood And Growing Fast