SAMG - Silvercrest Asset Management: Very Strong Candidate For Long-Term Investment

2023-03-11 03:35:06 ET

Summary

- Great profitability metrics show potential. I wanted to shed some light on an unknown stock so people can add it to their watchlists.

- A slight decline in revenues due to the hard environment in 2022, however, the results were not the worst.

- With no clear trajectory of revenue increases, I decided to do a stress test for declining revenues in '23 and '24.

- Even with conservative assumptions, the company manages to generate great FCF and a DCF and a dividend model suggest undervaluation.

Investment Thesis

Outstanding balance sheet and FY2022 results showing not the worst performance in a very tough time for the whole world, coupled with a high retention rate, solid track record, and historically low P/E ratio caught my attention to look into in more detail into Silvercrest Asset Management Group (SAMG). With high FCF generation, I wanted to see how the asset manager may perform in the future with further declines in revenues over the next 12-24 months. In my valuation model, I have a slight decline in revenues for the next two years and only a conservative bounce back in the later years to be more conservative. Even with these conservative assumptions in place, the asset manager is still a buy, however, with more pain ahead in the global markets, I wouldn't be surprised if the stock price will drop along with the markets in the next couple of months.

Briefly on the Company and FY2022 Results

Silvercrest Asset Management Group is a wealth management firm that provides financial planning, investment management, and family office services primarily to ultra-wealthy individuals and families, as well as certain institutional investors. They currently have 8 locations across the country.

The firm saw a decrease in AUM y-o-y due to the year 2022 being very tough for the markets, and only easing slightly in the last quarter. Discretionary AUM, which primarily drives revenues has declined a whopping 16.7%, however, that translated to a full-year revenue decrease of around 6%.

This in my opinion wasn't that bad of a year for the company, especially since their ability to retain clients is very impressive, which stands at over 98%.

The Future Outlook for the Manager

Over 95% of total revenues come from Management and advisory fees segment which depends on AUM. The more assets appreciate and the more clients the firm can get on board, the more revenue it can generate. It looks like it may be another tough year for the global markets, with a lot of talk of the Fed becoming more aggressive again in raising interest rates. Now a lot of people believe that the fed will raise interest rates by another 50 basis points instead of 25 because inflation is not coming down meaningfully enough and the economy is the strongest in decades.

How will this affect the firm? It is hard to tell but clearly if we are going to see further deterioration in the global markets, so will the firm's revenues. Looking at historical figures, the firm has been doing quite well during the tough times and in the last 10 years they managed to grow at 9% per annum, with only the first decrease in revenues in FY2022. The skill of obtaining new clients and increasing AUM has been admirable. Since the firm's inception, it managed to grow its AUM at a very strong pace, 28% CAGR.

The company currently has 7 office locations, mostly on the east coast. There could be more opportunities for the company to grow by opening up more office locations or acquiring other firms like the recent acquisition of Cortina Asset Management up in Wisconsin. The management wants to keep growing organically by retaining clients and acquiring new clients instead of acquiring companies for now it seems. It has been working for them in the past, I don't see why it wouldn't work in the future also. They seem to have quite a professional team of wealth managers that can retain good relationships with their current clients, which leads them to gain trust and in turn receive referrals for new clients. I worked for an asset management firm, and it is definitely easier to sign up a new client through referrals than through cold calling.

With that said the way I see it, there aren't many developments in the future that could potentially propel their revenues, besides keeping what they have been doing and acquiring/opening new offices to expand their reach, however, I cannot put viable growth assumptions on these speculations, so my best bet is to look at how the company performed in the past and apply some conservative growth figures to my model. But before I do that let's have a look at the books.

Financials

The company has a very healthy amount of cash on hand. They could be earning some interest on it, but they chose to have it ready in case they see any acquisitions that they would want to jump on. They can easily cover all their short-term obligation with cash on hand. The company has no long-term debt, just some short-term debt which is easily coverable with cash.

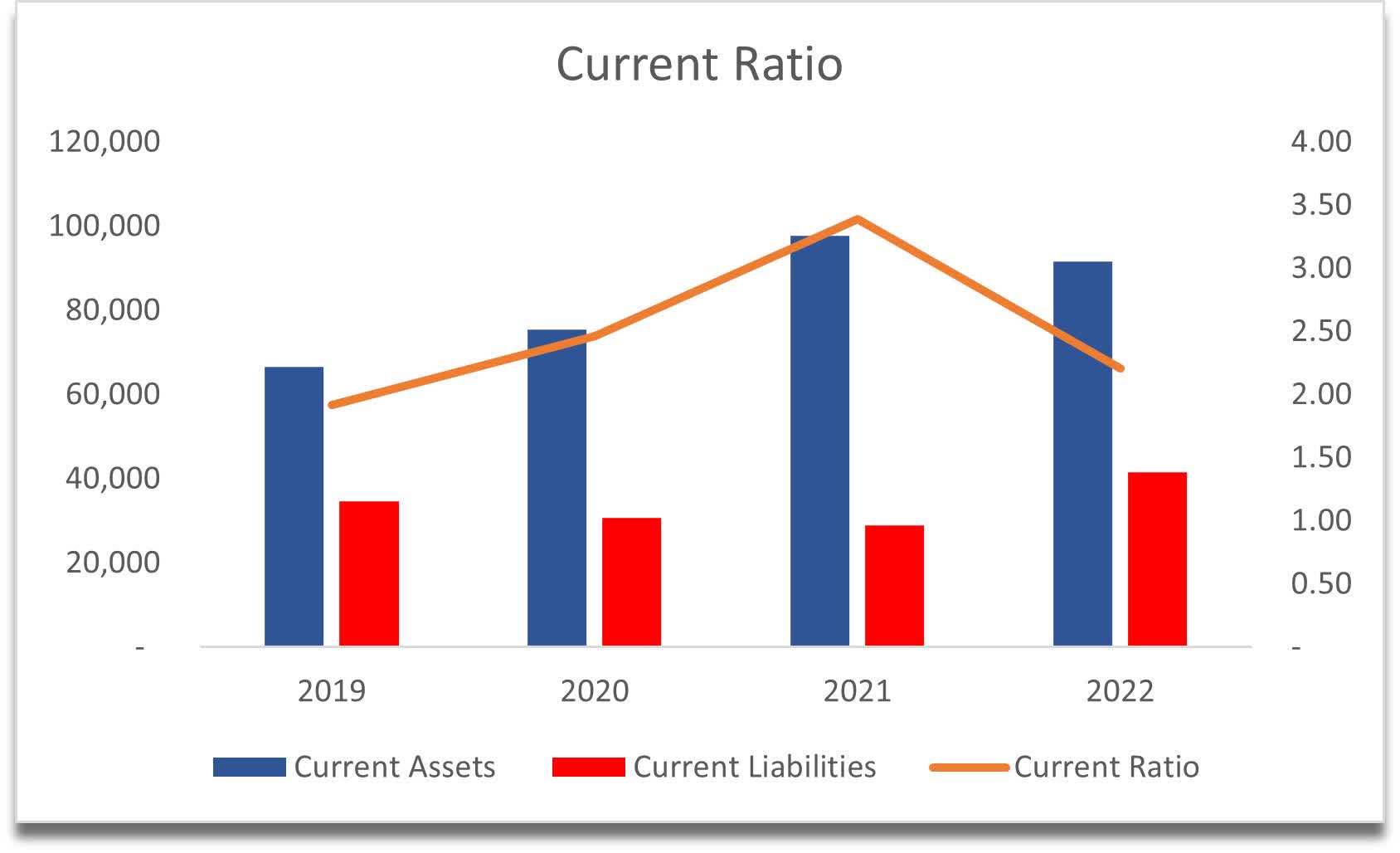

Speaking of liquidity, the company also has a very healthy current ratio.

{kind=link}

The profitability ratios were the reason I wanted to cover the stock because while I was searching for a more unknown company to shed some light on that there could be some hidden gems out there, my stock screener displayed decent ratios for SAMG.

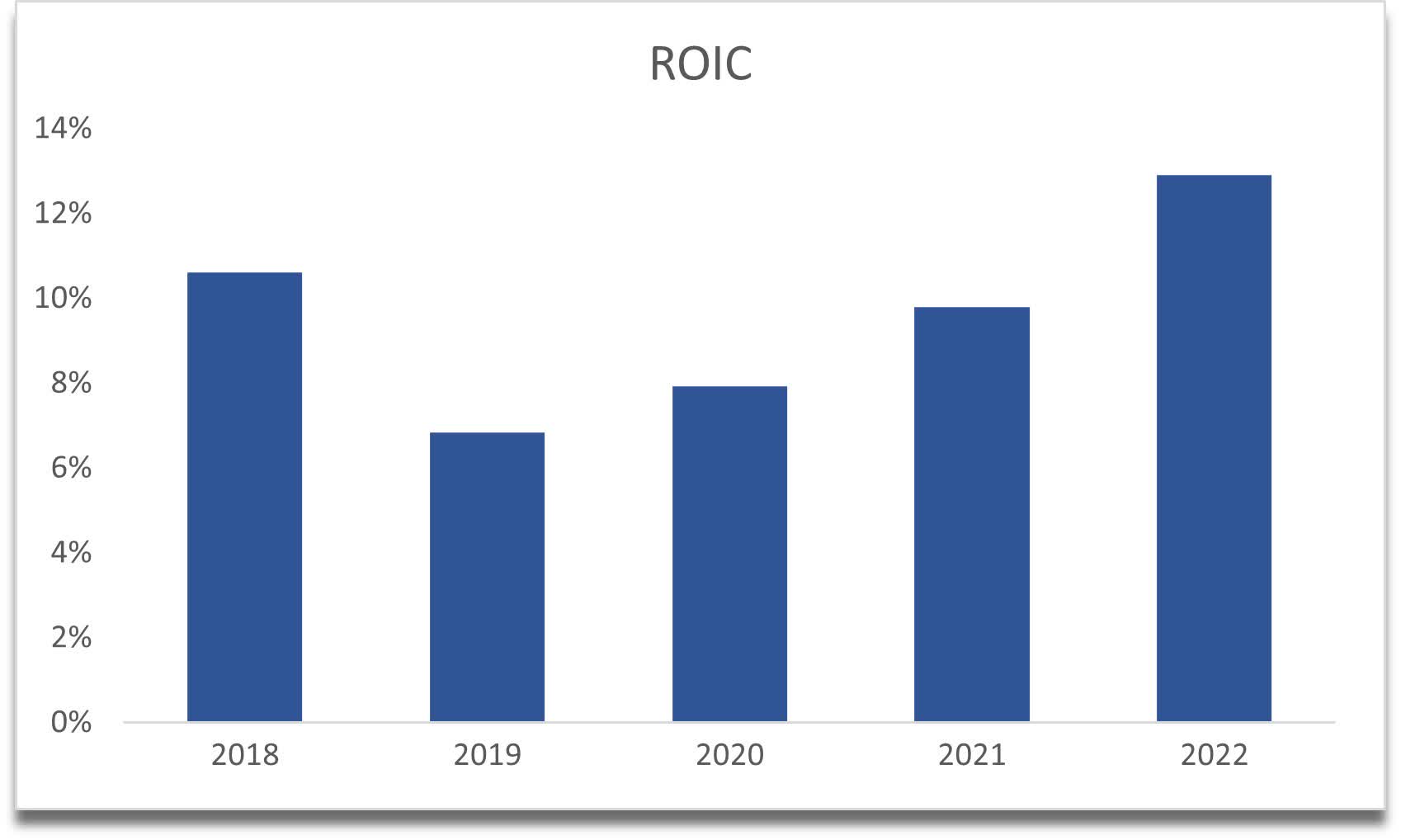

Return on invested capital is well above my minimum and from the graph below you can see that it is on the rise still, however, we may see a dip if we do experience a further downturn in the global markets while the fed continues the tightening.

{kind=link}

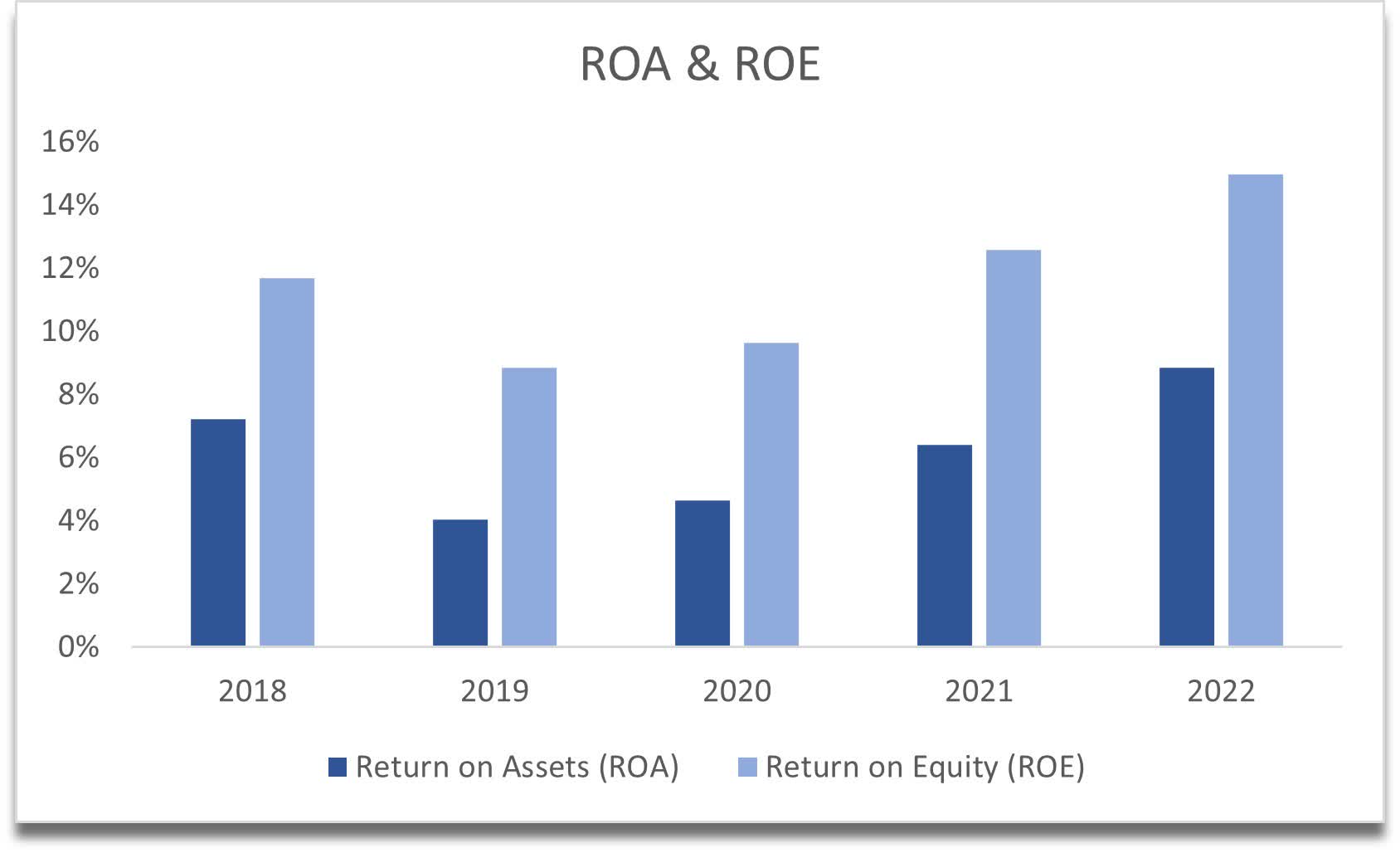

We can see the same trend in return on assets and return on equity. Very healthy returns on those too, which tells me the management is a value creator and knows how to run a company efficiently.

{kind=link}

Overall, the company is very efficient in how it is using the capital it has, and if this continues the company will reward its shareholders in the long run, which will depend on the wealth managers' ability to retain clients, gain new clients, and keep increasing AUM as they have in the past.

DCF Valuation

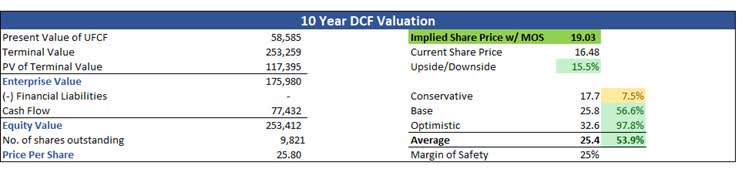

This time around, it was harder to come up with some reasonable assumptions on growth. I decided to do a stress test on the company instead. I modeled three scenarios, a base case, a conservative case, and an optimistic case. All three scenarios have a recession built in for the first 2 years, where the revenues go down by 10% in '23 and '24, flat in '25, +10% in'26 and then average growth of 5% for the remainder of the model in the base case scenario.

For the conservative case, I had 2% less each year and for the optimistic case, I added 2% to the base case, so this will give me a range of possible outcomes. To be even more conservative, I like to add a 25% margin of safety on top of the assumptions at the end, with that said, the model suggests the company is slightly undervalued, with intrinsic value sitting at $19.03, suggesting a 15% upside from the current share price.

{kind=link}

Dividend Valuation

I wanted to get more insight into how much the company might be worth, and I noticed it is paying a dividend. A very predictable dividend, increasing by a penny every year, so I modeled the same for my calculations. The payout ratio is sitting at around 36% so they have no problem covering it. In my opinion, the dividend growth rate of 5% can be achievable in the long run and with that in mind, the dividend discount model with a 25% margin of safety added also gives me a very similar intrinsic value calculation of $18.98 a share, which indicates the company is undervalued.

Conclusion

It was not the easiest to find some solid growth prospects for the company other than going by historical growth, so going by the worst-case outcome in a form of a stress test seemed reasonable to see how well the company can withstand harsh environments that we may plunge into in the next 12-24 months. It seems that even with such conservative assumptions in place, the company is operating exceptionally and if the management maintains it, the company can be a very good long-term hold for new and current investors alike.

The risks of opening a position right now are quite big, considering that the fed is still tightening the economy. I shall monitor the situation over the next couple of months, and in the meanwhile, I am not opposed to opening a small position and averaging down further if the markets do end up going lower in the future. It is hard to go wrong when it comes to investing in a company that has an outstanding balance sheet with no liquidity problems in sight and great cash flow generation.

The big question is, will the investors see value in the long run, or will the share price go nowhere and never reach the potential that it can? The only thing to do is to wait and reassess the situation every year, to see if the thesis has changed from any new revelations that the company might announce, but right now the company looks like a good bet for the future.

For further details see:

Silvercrest Asset Management: Very Strong Candidate For Long-Term Investment