SAMG - Silvercrest: Undervalued Following Good Q2 Results And Bullish Analyst Forecasts

2023-08-29 12:48:57 ET

Summary

- Silvercrest has demonstrated positive growth in their financial fundamentals, and the market consensus is forecasting Net Income and EPS to increase further.

- The stock price is undervalued relative to peers, and is well supported by key institutional shareholders such as BlackRock.

- Sell-side analysts have issued a "BUY" rating on the stock, with a consensus 12-month target price implying a 26.5% return potential.

Investment Thesis

Silvercrest Asset Management ( SAMG ) has released positive financial results in H1 23, as Net Income and EPS have grown substantially, and are forecasted to increase further for the rest of the financial year. Despite the improving fundamentals, the stock price is up only 2.5% year-to-date and looks undervalued relative to peers. As a result, I believe the stock is due an upward move to higher levels.

Company Summary

Silvercrest is a wealth management firm based in New York, providing financial advisory and related family office services to high net worth individuals (HNWI) and institutional investors. As of the Q2 23 results, the firm's Total AUM increased by $3.2 billion or 11.2% on a year-on-year basis, from $28.7 to $31.9 billion, driven by both a market appreciation of assets under management after better performance across equity markets this year, as well as new net client inflows.

SAMG's management have driven the growth of the firm and AUM by offering a diversified suite of product offerings, ranging from value, growth, and international investment strategies. In addition to its equity strategies, SAMG has also been building out new product lines such as the Outsourced Chief Investment Office , specifically catering to more institutional players such as endowments, foundations, and family offices. This is an exciting product line that will help diversify the company's revenues away from just the HNWI space. The OCIO model aims to take the workload away from smaller family offices that do not have the ability or resources to manage advanced portfolios in-house.

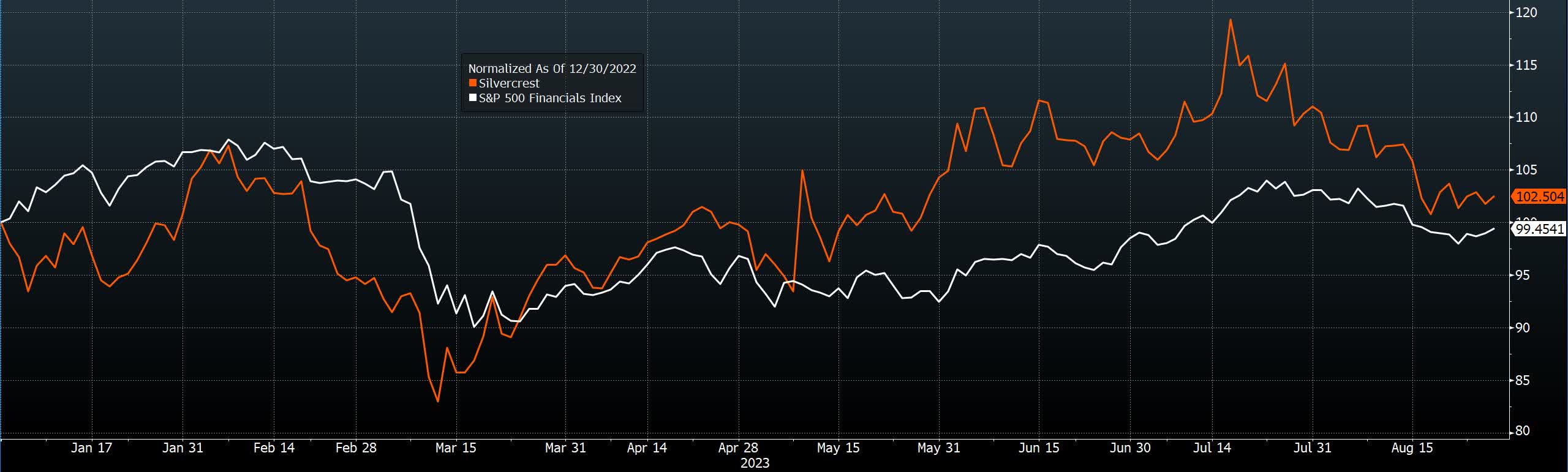

Normalized Chart - SAMG, S&P 500 Financials Index (Bloomberg)

{kind=link}

Despite the positive developments and management strategy execution on multiple product fronts, the share price has struggled to outperform, as SAMG is currently up only 2.5% year-to-date. Nevertheless, it is worth noting that despite the financial sector turbulence earlier this year, SAMG has managed to remain in the green. I believe in the coming periods, the stock should better reflect a combination of bullish factors - improved financials, undervaluation relative to peers, and positive sell-side and buy-side sentiment discussed further below.

Positive Financial Results

Last month, SAMG released their Q2 23 results and they showed positive developments. Whilst Revenue was generally flat vs. the previous quarter, Net Income increased to $3.2 million, up ~68% on a year-on-year basis, whilst also seeing margin % increasing. EPS also increased to $0.34 per share, up from $0.30 in Q1 23, and significantly higher than the $0.19 released in Q2 22.

Looking forward, the analyst consensus for the rest of the year looks to continue the positive upward trend in results. Net Income is forecasted to hit $5.6 million in Q4 23, with EPS also increasing once again up to $0.39 per share.

{kind=link}

One can argue that both the recent and forward-looking fundamental are currently not being reflected in the stock price's performance so far this year. I believe this divergence between positive financials and lackluster share performance can only continue for so long, and I expect the stock to break ground and trade higher in the coming periods.

Growing Dividend History

From a dividends perspective, SAMG also demonstrates solid income benefits for shareholders. As per the below Dividend Summary on Bloomberg, SAMG has shown a consistent and growing dividend policy. The stock has a 1 year dividend growth of nearly 6%, with the most recent quarterly dividend increasing to $0.19 per share. The annualized dividend yield is attractive at 3.98%, higher than its peer group. This positive income angle adds to the undervaluation view, and could possibly see SAMG contributing a significant total return to your portfolio in my view.

{kind=link}

Bullish Analyst Recommendations

I always look to affirm my thesis by looking at the analyst recommendations in order to gauge the sentiment of the sell-side community. Whilst SAMG has relatively low coverage by analysts, there is a clear positive consensus around the stock. 100% of surveyed equity research analysts have issued a "BUY" rating on the stock, and the consensus 12 month target price is $24.17, which implies a possible 26.5% return potential based on the current price.

{kind=link}

Undervalued Relative To Peers

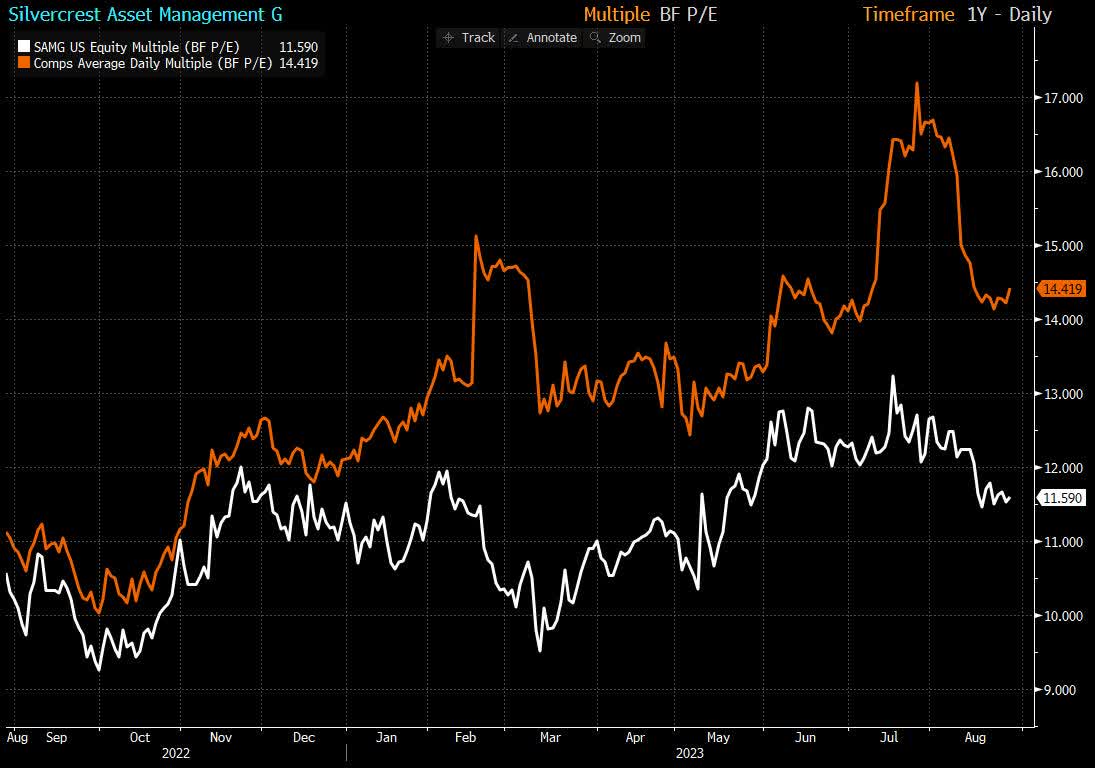

Referring to Bloomberg's Relative Valuation screen, SAMG looks to be significantly undervalued to its US Wealth Management peer group, trading at a discount in terms of Price-to-Earnings Ratio.

The Blended Forward P/E Ratio, which uses a time weighted average of fiscal year 1 and fiscal year 2 forward estimates, has seen a growing spread between SAMG and peers, despite a much closer correlation in 2022. If this divergence reverses, we should see a positive scenario in SAMG's stock appreciating.

{kind=link}

The stock's Bloomberg Adjusted EPS estimate for FY 2023 is 1.77, which if we apply to the comps average blended forward P/E Ratio of 14.42, we can calculate a target price of ~$25 for SAMG. This represents a significant potential uplift, and is also in-line with the analyst consensus 12 month target price of ~$24 illustrated earlier.

SAMG P/E Valuation (Bloomberg)

Notable Shareholder Increases

Looking at the Top 10 Shareholder base and the recent quarterly reporting of their positions, we can see a positive outlook that affirms my bullish thesis. Whilst some of the smaller shareholders on the list may have decreased their positions to an extent, we see significant increases in the stakes of the top shareholders, such as Long Path Partners, BlackRock, and Vanguard. BlackRock increased their position 6x in the last year, amassing ~6% of the shares outstanding, whilst Vanguard has increased their stake by 10% over the period, holding ~5% of the shares. These purchases in recent quarters by some of these key institutional players imply that they could potentially see good value in the stock and have a bullish outlook.

{kind=link}

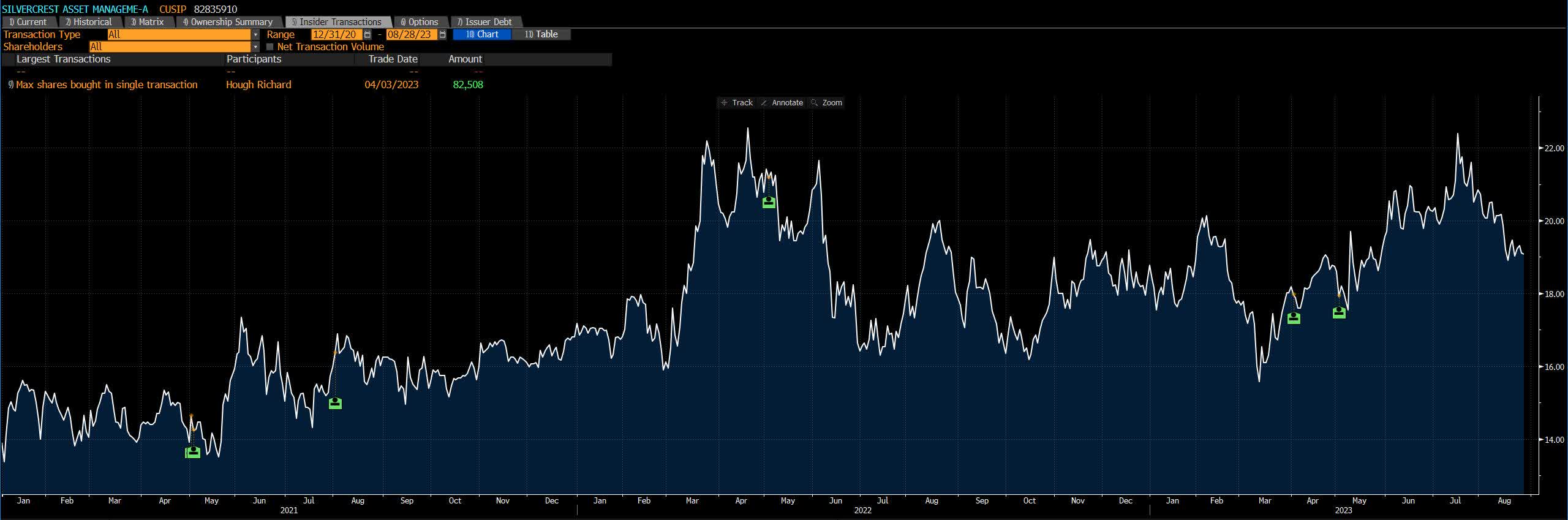

A similar pattern can also be seen in the transactions of the Management Insiders, as the executive team have been purchasing shares in the last couple of years, with no sell transactions. This indicates that the management team have skin in the game and implies they might see the recent price levels as good value relative to the long-term prospects for SAMG, which corresponds well with the thesis.

{kind=link}

Risks

It is worth highlighting a couple of risks that could lead to the thesis underperforming. On a macro level, if there were a sustained period of economic and financial distress, this would have a negative impact on equity markets valuations and possibly lead to underperformance in the strategies managed by SAMG. In turn, sustained underperformance could lead to net outflows in terms of their AUM and harm the management and advisory fees that feed into SAMG's top line, as investors look to shift their assets elsewhere. Tough economic circumstances could also lead to both HNWI and institutional investors needing to redeem and liquidate their investments for other general reasons, further compounding the outflow risk. So far, the US economy has managed to remain impressively resilient following the aggressive monetary tightening policy implemented by the Federal Reserve, but this policy often has a significant time lag before it is felt throughout the underlying economy, so time will tell.

Secondly, we are in an age of growing financial literacy and inclusion, as there is a wealth of valuable and affordable financial advice, products, and services that the average investor can now access. This is a long-term trend that may require active wealth managers to continuously prove their worth in outperforming their relative benchmarks in order to justify their fees. If not, existing and prospective clients may turn to lower cost and/or passive investment solutions such as Exchange Traded Funds.

In Conclusion

Silvercrest has done an impressive job of growing their business, both in terms of expanding the range of products to cater for the HNWI and institutional client bases, and also in growing their AUM during a tough financial environment. These positive developments are clear to see in the financial results in the first half of this year, and are expected to continue in the second half as per the analyst consensus. At the same time, I take comfort in the shareholder buying sentiment of the key institutional and management shareholders, and I believe the stock's current undervaluation relative to peers make this an attractive long-term value play, whilst also benefitting from a solid dividend yield in the meantime.

For further details see:

Silvercrest: Undervalued Following Good Q2 Results And Bullish Analyst Forecasts