SMWB - Similarweb: A Cheap SaaS Play

Summary

- Similarweb has plummeted nearly 70% since going public in 2021.

- The analytics company has solid fundamentals with a large and growing addressable market.

- Its latest Q4 earnings showed strong top line growth and improved profitability.

- The current valuation appears to be cheap as multiples are way below software peers.

- I rate the company as a buy.

Investment Thesis

Similarweb ( SMWB ) went public back in 2021 but shares have been dropping non-stop due to rising rates, elevated inflation, and a lack of appetite for growth companies. It is now trading at just $6.59, down nearly 70% below its IPO price.

However, unlike the share price, the company’s fundamentals remain solid. It has a compelling platform with a huge addressable market. It continues to report strong growth with revenue up 28% and also significantly narrowed its loss from the prior year. After the huge drop, the current valuation seems attractive as multiples are meaningfully below SaaS (software as a service) peers. I believe the current price level offers decent upside potential therefore I rate SMWB stock as a buy.

Huge Opportunities

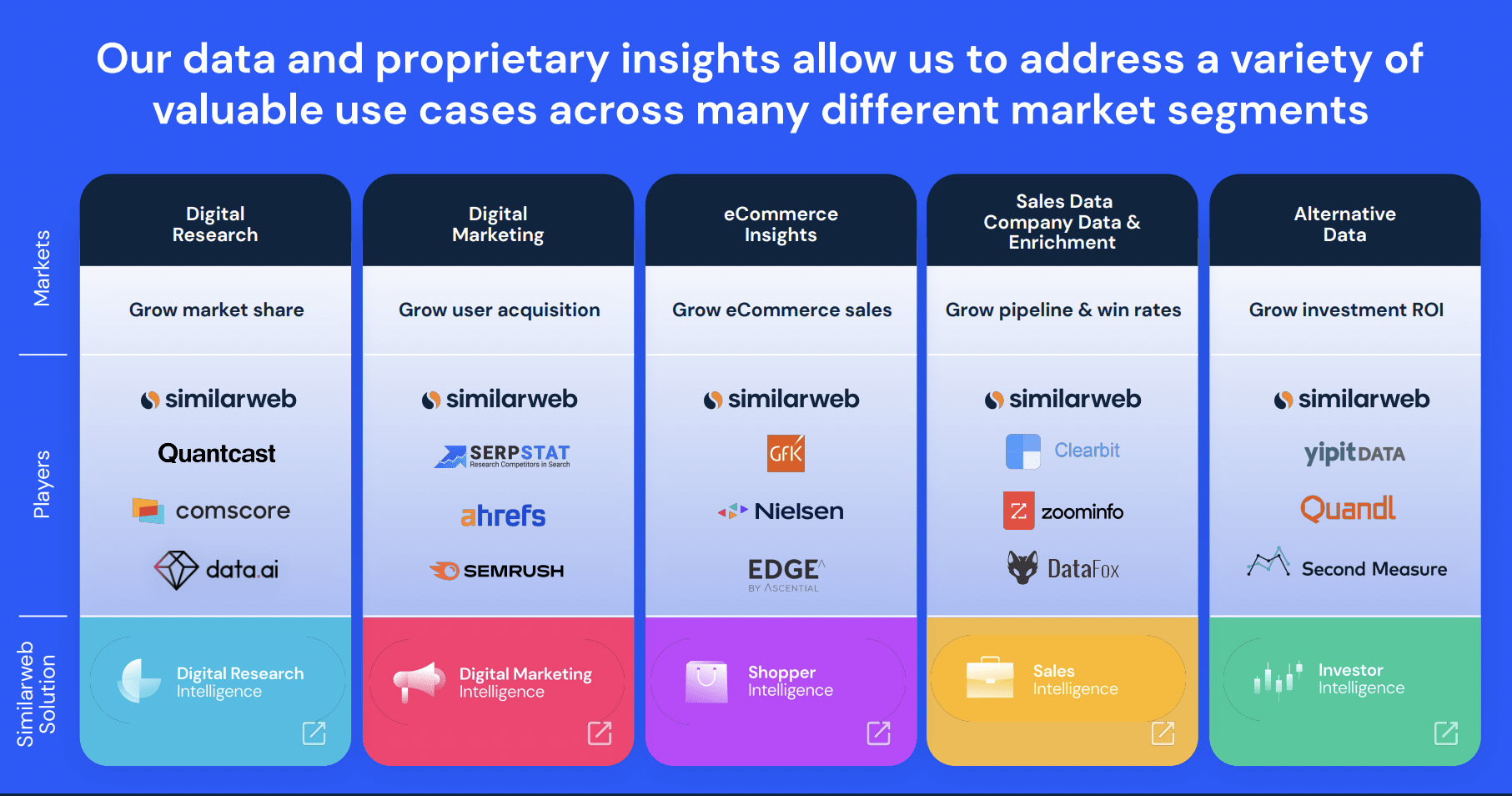

Similarweb is a US-based digital analytics company founded in 2009. The company’s intelligence platform offers data and insights to help customers with research, marketing, sales, etc.

It provides different solutions for market analysis, benchmarking, keyword research, competitive analysis, and more. The company analyzes 100+ million websites and 4.7+ million apps from multiple sources and converts them into unique insights through AI and machine learning. This ensures all its insights are top-notch and up-to-date. Its existing customers include blue-chip companies such as Google ( GOOG ) (GOOGL), Walmart ( WMT ), Pepsi ( PEP ), and others.

{kind=link}

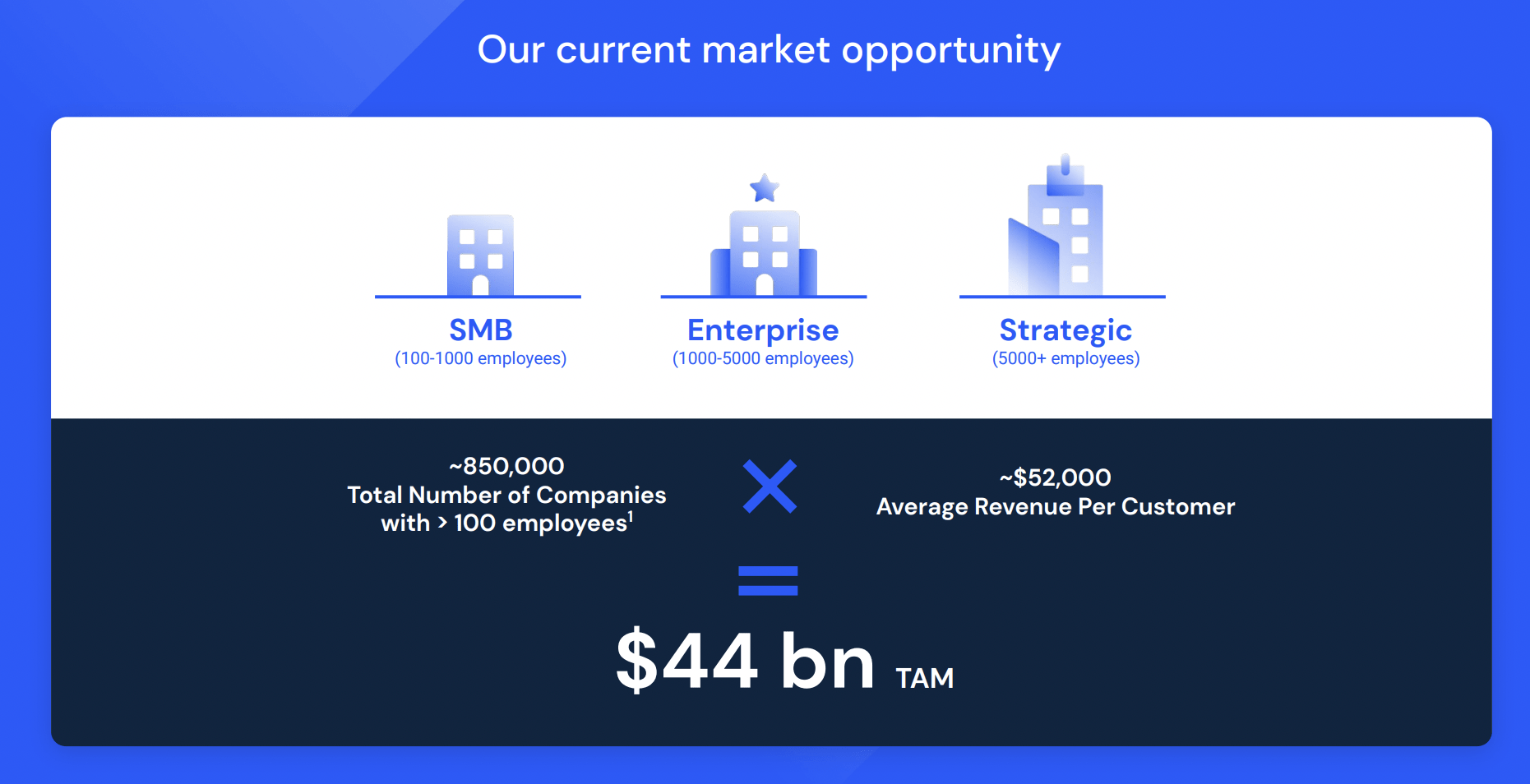

Similarweb has huge market opportunities. The company estimates its current TAM (total addressable market) to be $44 billion. The TAM should grow over time as it is launching products for new use cases such as investing and e-commerce.

For instance, the new investor intelligence solution can expand its TAM by $4.4 billion. The company’s products are seeing strong demand as customers want better visibility of the market landscape in order to make better decisions. A lot of the existing tools allow companies to analyze their own performance but not competitors or partners. Similarweb is able to reach that blind spot which significantly broadens the customer’s visibility. The need for more comprehensive insights should continue to be a solid tailwind moving forward.

Andrew Smith, manager of MGM Resorts, on Similarweb :

The reason that we use Similarweb is because it gives us something we don’t have. With Google Analytics or PowerBI, we know what’s happening with us. It’s what’s happening with our competitors, our affiliates, our partners, that’s what we need to know. And there’s nothing like that. For MGM Resorts, if we were to lose Similarweb we would lose the ability to know what our partners, what our competitors, and what the industry was doing.

{kind=link}

Q4 Earnings

Similarweb just reported its fourth-quarter earnings and the results are solid considering the macro backdrop.

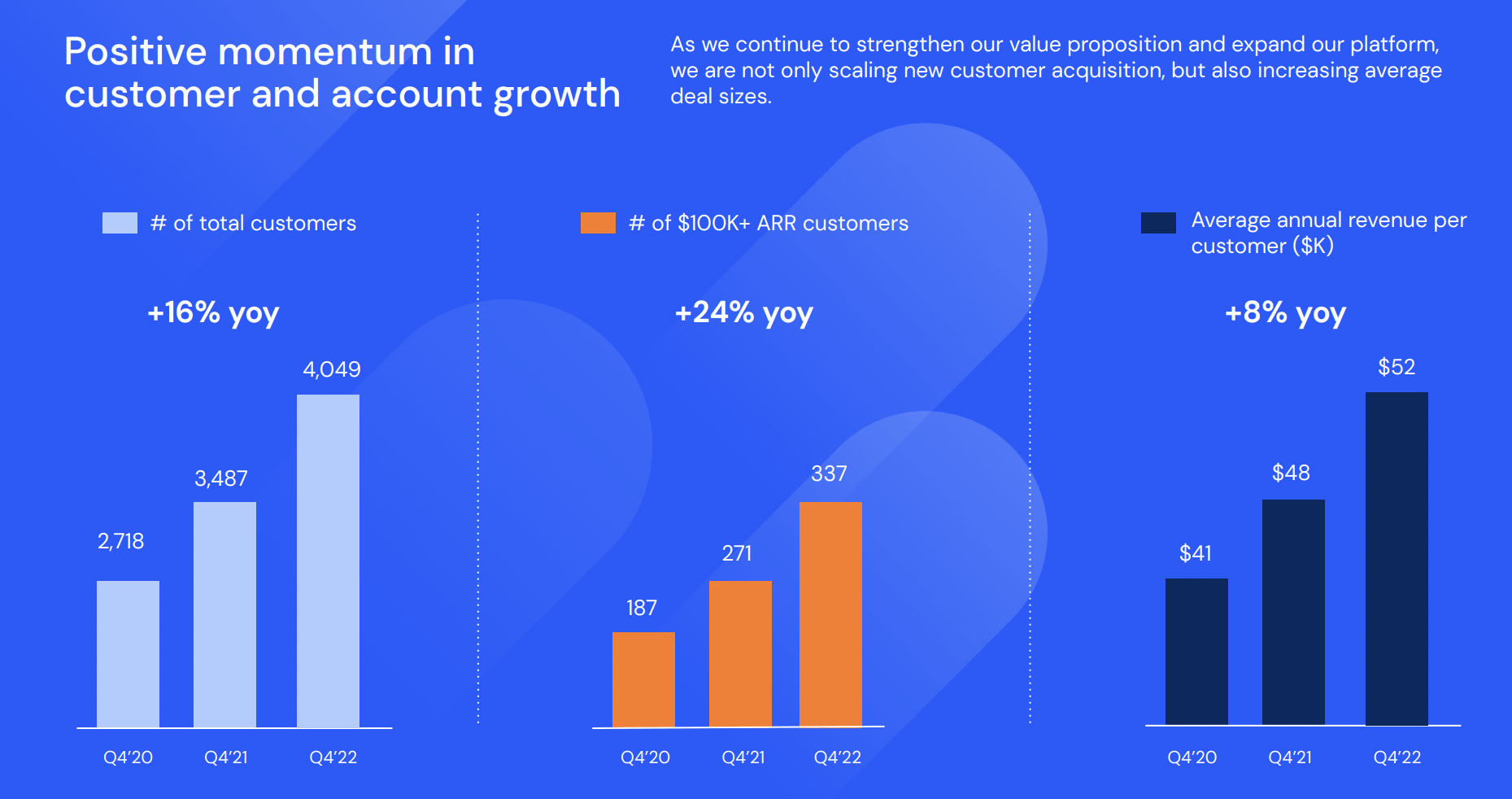

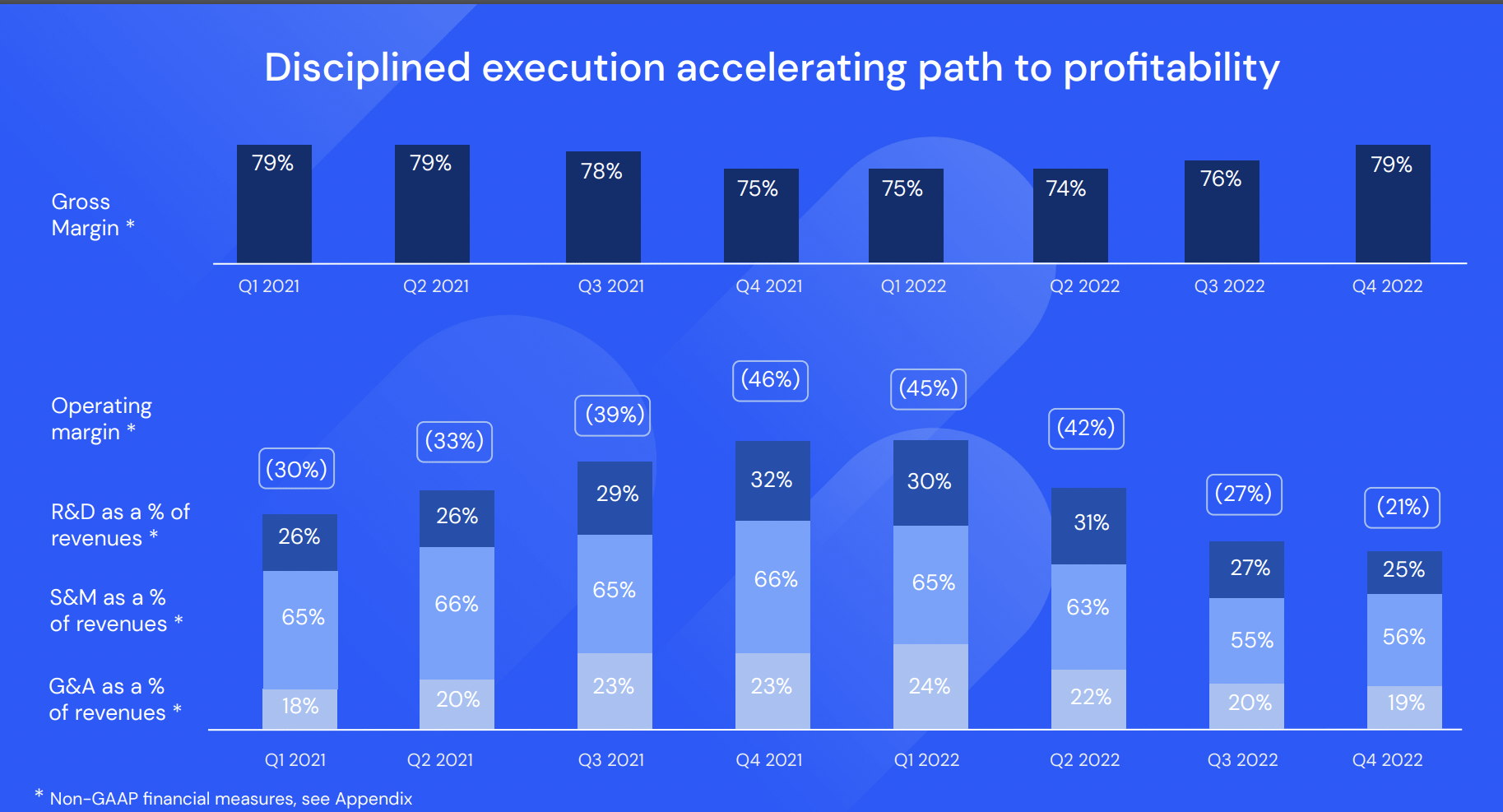

The company reported revenue of $51.3 million, up 28% YoY (year over year) compared to $40.2 million. The growth is driven by the increase in the number of customers with ARR (annual recurring revenue) of $100,000 or above, which grew 24% to 337. It is also seeing strong expansion opportunities within the group. The dollar-based net retention rate for the group was 120%. The total number of all customers increased 16% YoY to 4,049 and the overall dollar-based net retention rate was 109%. The relative softness is due to the weakness in SMBs as they are more exposed to macro headwinds. Thanks to cost optimization, costs of sales grew at a slower pace than revenue. This resulted in gross profit increasing 31.9% from $29.5 million to $38.9 million and gross profit margins expanding 250 basis points from 73.3% to 75.8%.

{kind=link}

The bottom line was still negative but narrowed substantially which is very positive. The company managed to be very disciplined in spending and continued to show operating leverage. Despite revenue growing 28%, operating expenses only increased 2% YoY from $52.4 million to $53.5 million. S&M (sales and marketing) expenses increased 7.5% YoY but got offset by the decline in R&D (research and development) and G&A (general and administrative) expenses, which were down 2.1% and 6.9% respectively. This resulted in an operating loss of $(14.6) million compared to $(22.9) million, representing a significant improvement of 36.2% YoY.

Guidance for FY23 seems pretty weak as revenue growth is only forecasted to be roughly 15%. However, this is mainly due to the company shifting its focus to profitability. It expects non-GAAP operating loss to further improve and generate positive cash flow by the fourth quarter, which is huge in my opinion.

Jason Schwartz, CFO, on guidance for FY23:

“We intend to achieve sustained positive free cash flow quarterly by the fourth quarter of 2023. We have aligned our strategic objectives on balancing our revenue growth with accelerating our profitability. We continue to focus on disciplined execution in this challenging environment, which will be critical to accomplishing our objectives in 2023.”

{kind=link}

Investors' Takeaway

Overall, I think this quarter’s results are pretty decent. Top-line growth continues to be strong thanks to the strength in larger customers. The bottom line also improved substantially thanks to better cost and expense management. The guide for growth was soft but prioritizing profitability in the current environment is more important in my opinion. As the macro environment rebounds later on, customer spending should also increase which will re-accelerate growth. After the massive drop, the company is trading at a P/S ratio of just 2x which is very cheap for a SaaS business with huge market opportunities. For instance, ( WCLD ), an ETF comprised of multiple SaaS companies such as Shopify ( SHOP ) and monday.com ( MNDY ), is trading at a P/S ratio of 5.2x. Similarweb is so discounted that even if growth rates were to slow to mid-teens, there would still be meaningful upside potential. Therefore, I rate the company as a buy.

For further details see:

Similarweb: A Cheap SaaS Play