SMWB - Similarweb: Too Cheap To Ignore But Too Many Questions

2023-09-12 14:44:24 ET

Summary

- Similarweb's stock is attractively valued at around 2.0 price/sales, but lingering questions about AI capabilities, 2024 guidance, and conversion of free users, leave the stock on hold.

- Similarweb reduced its revenue guidance for the year and has declining net revenue retention which could lead to lower 2024 revenues.

- Fortunately, a growing user base, strong gross margins, and a projection for positive free cash flow keep positive prospects for the stock.

- The waning metrics for a close competitor provide potential thresholds that define a path away from Similarweb becoming another cautionary tale.

Similarweb Ltd. ( SMWB ) offers a digital marketing and research platform that provides competitive intelligence on website and app traffic. SMWB went IPO right around the peak of the pandemic-era mania for tech and all things digital. Accordingly, the stock has fared poorly since its IPO. Today, at around 2.0 price/sales, the stock is too cheap to ignore. However, this rock bottom valuation occurs within the context of a macroeconomic environment where, as the company acknowledged in its Q2 2023 earnings conference call , companies are rationalizing spend on software. I had a lot of questions going into a read of the earnings results, and I still have outstanding questions. On balance, I am on hold with SMWB until I get more clarity on at least a few areas.

Does Reduced Guidance Portend Looming Weakness?

Similarweb reduced its revenue guidance for the year from a range of $221M to $222M (a 15% year-over-year growth rate at the midpoint) down to a range of $216M to $218M (a 12% year-over-year growth rate at the midpoint). This small reduction did not come with a clear driver, but it seems the company expects a small erosion in pricing power or perhaps longer sales cycle have shifted a small amount of revenue into next year. In response to an analyst question about recent pricing and packaging questions, Similarweb only said customer feedback has been “good” (do customers ever like new pricing models that cost them more money?). Either way, the user base metrics look solid enough to overlook the small reduction in revenue guidance, especially since the company is sticking to its projection of positive free cash flow by Q4.

The company reported a year-over-year growth in its customer base of 12%. The average spend of these 4,300 customers is $51K annually, flat with Q2 of 2022. Yet, the overall dollar-based net retention rate (NRR) dropped year-over-year from 115% to 101%. A continued downtrend in NRR may lead to slower revenue growth in 2024. On the positive side, Similarweb has a 98% logo retention rate for its $100K+ customers. Similarweb expects to issue 2024 guidance in Q4.

Other notable guidance for the year: non-GAAP operating loss in the range of $16M to $17M. The improvement in the operating loss will deliver a greater than 4.5 percentage point improvement in non-GAAP operating loss margin from the first half of the year. This margin should be 5.4% in the second half of the year.

Can Similarweb Convert Free Users?

Similarweb reported that 25M users accessed its free tool in Q2. The company expects a total of 100M users for the year. This number sounds amazing except that there is clearly a minimal conversion rate of users going from free to paid subscribers. When asked directly about conversion expectations, management did not provide any information except to say “we understand this is a very strong engine to build pipeline on top of that, especially as you grow that — you have such a strong brand. And for big — I think, that we have big audience out of those 25 million people that register to try the paid version that you get a free trial.” Management did not provide numbers on free trials or conversion rates from free trials.

Having said that, clearly, if Similarweb figures out how to generate material conversion rates, the upside to the business would be tremendous. For now, it seems that the vast majority of free users are content with the “good enough” offering.

Will AI-Powered Features Boost Subscriptions?

Per Similarweb, SimilarAsk is “the first digital intelligent AI system designed to answer real questions that users type in free text without having to know how to navigate our platform.” This feature sounds promising as a way of using natural language to sift through a myriad of data segmentation and dashboard possibilities. In particular, analysts are typically tasked with identifying the drivers of material changes in data trends. Instead of clicking through and configuring dashboards, downloading data, attempting a bunch of correlations, and then constructing a narrative that explains the observations, an analyst can start with an AI engine that tries to track down these connections. Similarweb calls this solving the “holy grail of data to insight and insight to action.”

Yet, when describing how the AI works, management indicated that SimilarAsk can “go to the open web and try to explain why a certain website has a spike in traffic why it was jumping. So we can go and understand what happened in the same day by looking on the data that’s available online.” Such powerful reach would require massive amounts of computing power. This ability is not just about powering through an index and identifying appropriate key words. A platform would need to assemble a large sample of potentially related data across the entire internet and next make relevant inferences. Thus, Similarweb ’s claims sound astonishing. I need to see to believe.

The SimilarAsk press release from last month does not discuss these kinds of capabilities. Instead, it describes what I would expect: a fast and efficient way to navigate Similarweb’s dashboards and analytics.

SimilarAsk is in beta and being used by Similarweb’s early adopters.

Are Similarweb’s Economics Substantially Better Than comScore’s?

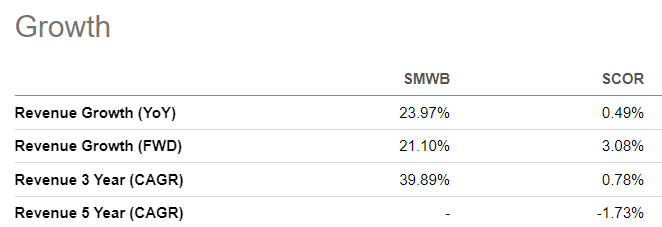

Partially thanks to some management missteps years ago, close competitor comScore, Inc. ( SCOR ) has been in a tailspin. SCOR hit an all-time high in 2015 and currently trades at an all-time low and below $1. I reviewed a few key metrics to compare SCOR vs SMWB and, like a digital analyst, looked for any warning signs that Similarweb could go eventually go the way of comScore. Some of SCOR’s key financials actually look better than SMWB’s. Revenue growth is a key differentiator: SWMB still has it, SCOR has little to none. For now, SCOR is still the bigger business in terms of revenue with $376.26M in the trailing twelve months ((TTM)) vs $207.80M for SMWB.

SWMB is still growing while SCOR's growth days are pretty much over. (Seeking Alpha)

{kind=link}

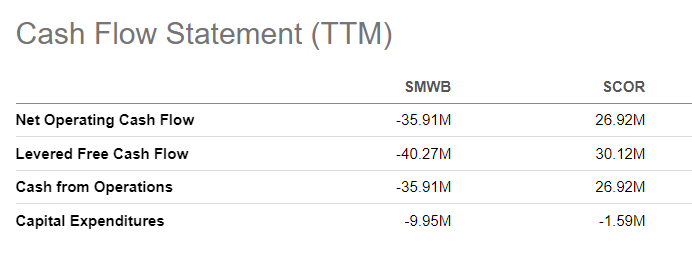

SCOR’s cash flow remains positive. SMWB is playing catch-up on this metric.

Despite a lack of growth, SCOR is holding onto positive cash flow while SMWB is yet to mature into a positive cash flow company. (Tradingview.com)

{kind=link}

The following charts are even more telling about the mixed picture.

SCOR had a business that was barely profitable when it was in the green. On a net income and diluted EPS basis, SCOR struggled until diving irrecoverably into the red starting around 2009. So far, SMWB is facing its own struggles to achieve profitability.

It is not yet clear whether SWMB can perform better than SCOR on net income. (Tradingview.com)

{kind=link}

Until very recently, SMWB under-performed SCOR on a (diluted) EPS basis. (Seeking Alpha)

{kind=link}

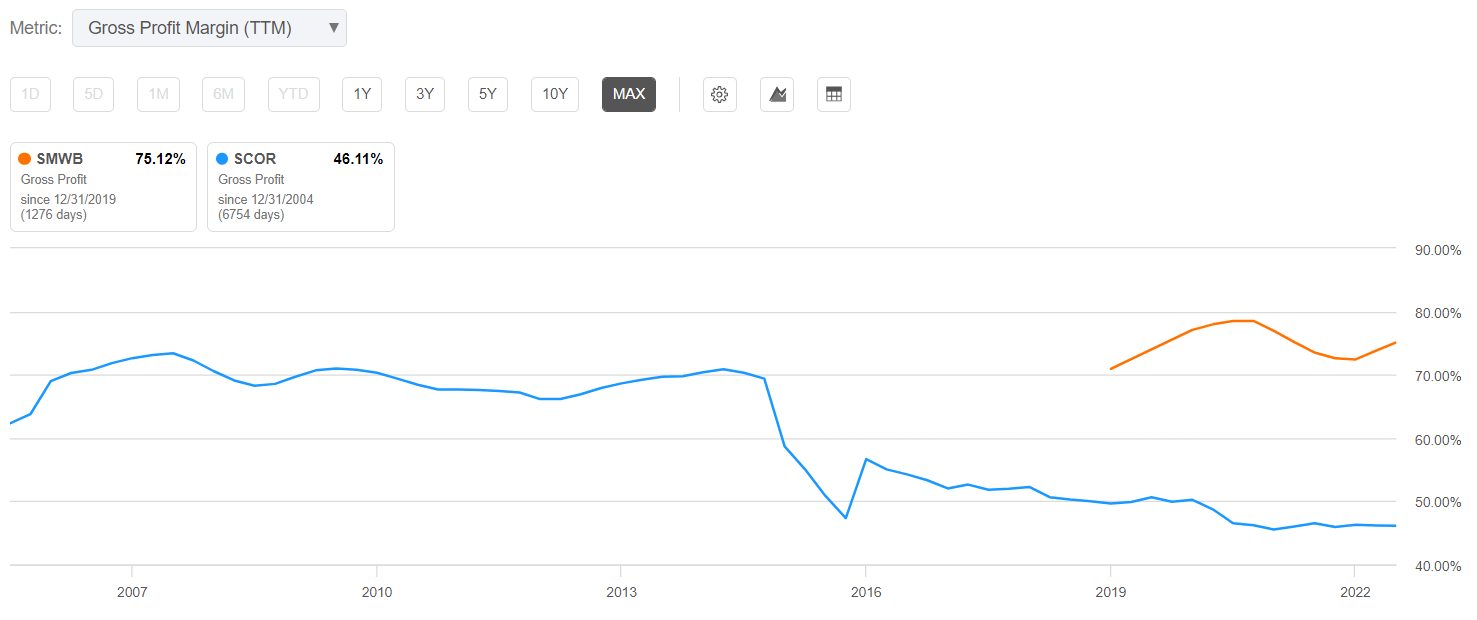

Fortunately, gross margins are a key differentiator for SMWB. SMWB has much better gross margins than SCOR ever had.

SWMB far outperforms SCOR on a gross margin basis. (Tradingview.com)

{kind=link}

Thus, getting to positive free cash flow is a major and necessary milestone for SMWB to demonstrate it can grow into a profitable business model in due time.

Finally, from a valuation perspective, SMWB is at an important juncture of sentiment. SCOR consistently bounced off the 2.0 price/sales level until valuations came tumbling down in late 2018. SMWB has bottomed out at 2.0 for nearly a year. A sustained decline below the 2.0 level could be a major red flag for investor expectations of Similarweb’s prospects.

A price/sales ratio of 2.0 seems to be a key threshold of investor sentiment for both SCOR and SMWB. (Seeking Alpha)

{kind=link}

The Trade

SMWB is a tempting buy since the stock combines revenue growth, strong gross margins, and a low valuation. However, until the company demonstrates a profitable business model, it is hard for me to pull the trigger. As a result, I will just watch the stock in case it breaks out above the current trading range ahead of the company’s announcement on 2024 guidance.

After a roller coaster of price action starting with the November lows, SMWB is up just 5% this year. (Tradingview.com)

{kind=link}

Be careful out there!

For further details see:

Similarweb: Too Cheap To Ignore, But Too Many Questions