SMWB - Similarweb: Undervalued With A $44 Billion Big Data TAM

Summary

- Similarweb is a data analytics provider which offers market, marketing, sales and even alternative investor data.

- The company reported strong financial results for the fourth quarter as it beat both revenue and earnings estimates.

- Its stock is undervalued intrinsically according to my model and forecasts and relative to historic multiples.

Similarweb ( SMWB ) is a market and competitor data intelligence provider, which is rated as a "leader" by G2. Surprisingly, the company has 4.5 stars out of 5, which is greater than ZoomInfo SalesOS which has 4.4 stars out of 5. To put how much of an achievement this is into perspective, ZoomInfo ( ZI ) is a ~$10 billion company (by market capitalisation) and Similarweb is a ~$500 million company. Now although the use cases are slightly different, the rating acts as a testament to the quality and value provided by Similarweb. Its customers already include over 4,000 iconic companies from Google , to Adobe, adidas, to CNN and even Walmart. Despite this, its stock price has been butchered by ~68% decline since its IPO in May 2021. However, in the fourth quarter of 2022, the company has reported strong financials, beating both revenue and earnings growth estimates. In this post, I'm going to break down its "big data" market opportunity, its fourth quarter financials, before revealing my valuation model for SMWB stock.

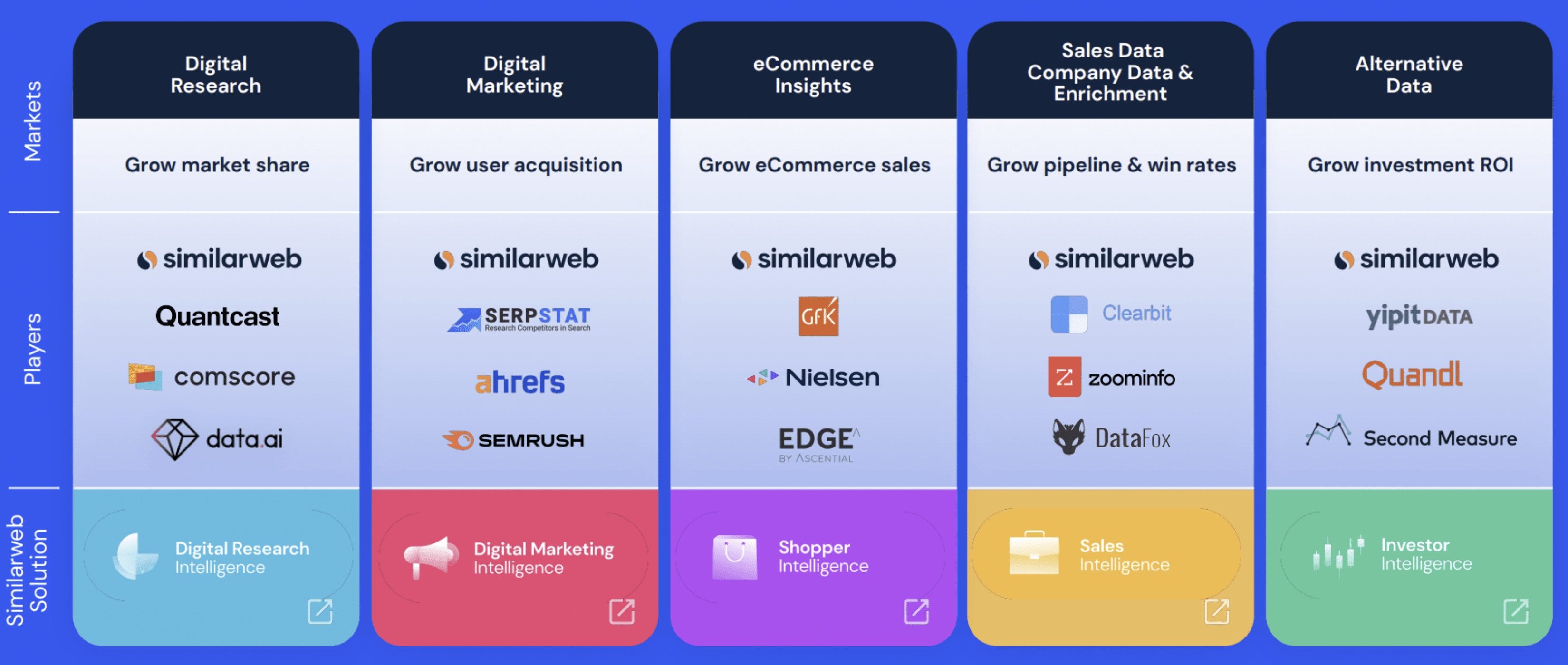

Big Data Business Model

Similarweb is basically a SaaS based data analytics provider, which initially gained traction as a Digital Marketing data or "intelligence" provider. As a former digital marketing agency owner, I found great value in using Similarweb to understand a variety of metrics for client competitors. This included website traffic estimates, keywords for Google search, referral websites, paid advertisements and more. Since then, the company has expanded its data offering to include Sales Intelligence, Shopper Intelligence and even Investor Intelligence.

{kind=link}

The Sales Intelligence data is pretty cool, in that a B2B company can identify prospects which are in their "sweet spot" as potential customers. This includes "firmographic" data such as company location, employee count etc. In addition, to revenue data and the direct contact details of "decision makers" for example, CEOs, CFOs etc. Now of course, Sales Intelligence data is a competitive market and I believe other companies such as ZoomInfo and LinkedIn sales navigator have a much stronger brand in this regard. Upon checking this, I was correct, as G2 reviews indicates ZoomInfo and LinkedIn as number one and number two, with Similarweb not even making the top 10. However, the company is slightly past the "contender" rating, which is a positive sign. Despite the competition, I believe Similarweb still has an opportunity to move across this market through a cross-selling strategy with its existing customers that use its marketing data. Also, as I mentioned in the introduction, Similarweb is a much smaller company than many of the big players, thus doesn't need to sign up many customers in this market to generate significant revenue. In other words, the business doesn't need to "own" this market, but simply gain traction.

I believe its Shopper Intelligence and Investor Intelligence data packages could also prove more lucrative initially, as they are in a much less competitive market and a much easier "add on" for a marketing or market research teams.

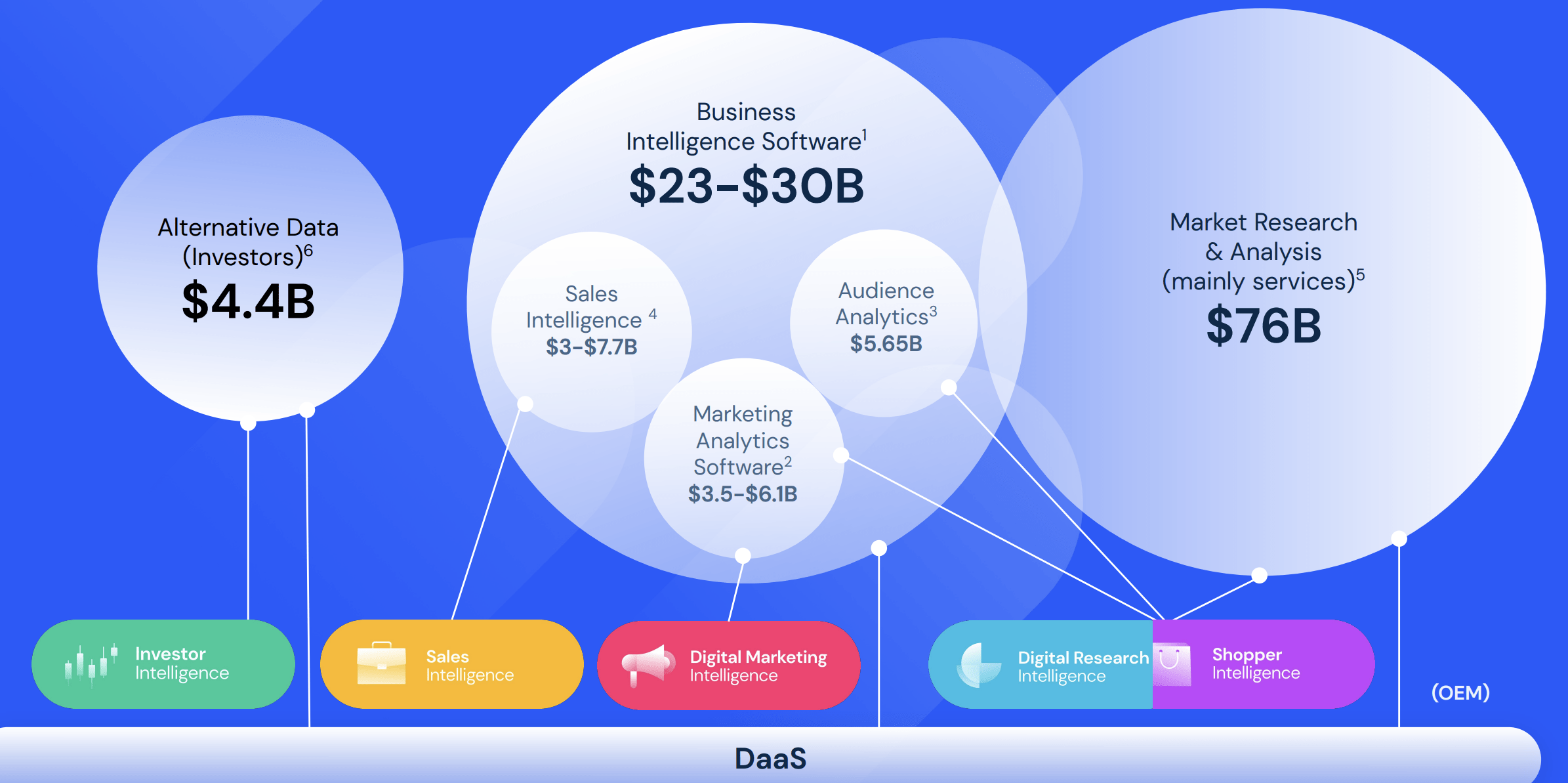

Similarweb estimates a $44 billion TAM, based upon 850,000 companies which could each pay them ~$52,000 per year. Given this is around $4,333 per month, it is not an unbelievable number for companies which are over 100 employees (which Similarweb is targeting).

In addition, Similarweb cites forecasts which indicate a $76 billion TAM for its Market Research & Analysis segment alone. Add to that, up to a ~$6.1 billion TAM in marketing analytics software and $5.65 billion for Audience analytics, both markets which I think Similarweb can "own" or lead. Alternative data for investors could also be an extra bonus with a $4.4 billion TAM, but this is still an unproven market opportunity.

The good news is I have personally used this tool in my own investing research; thus, I believe there is a "value add" from the usage of alternative data pre earnings reports, especially given most standard financial data is already baked into the stock price.

{kind=link}

Fourth Quarter Financials

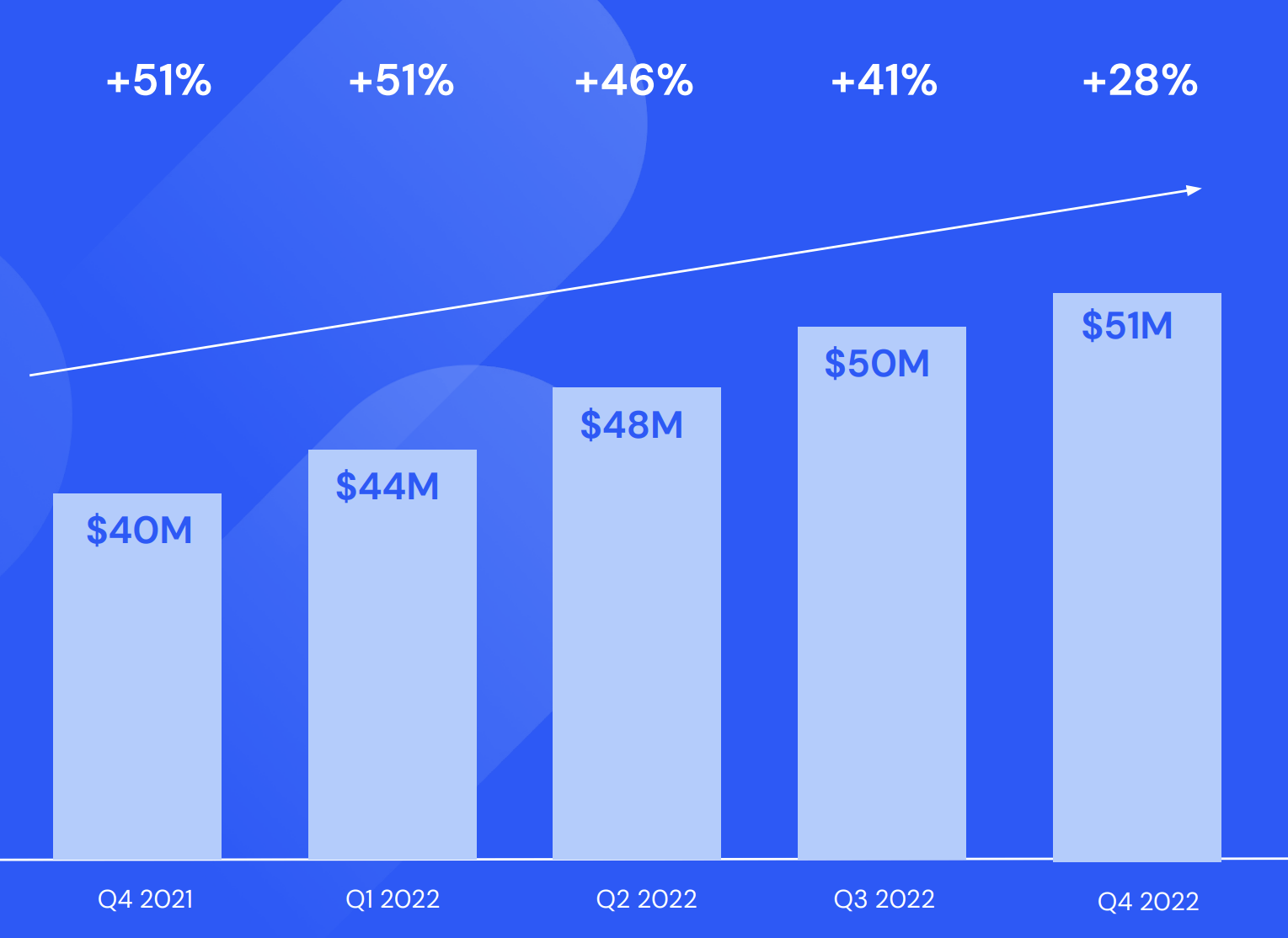

Similarweb reported strong financial results for the fourth quarter of 2022. The company reported revenue of $51.35 million, which surpassed analyst expectations by $696,023 and increased by 28% year over year. It should be noted this growth rate has slowed down significantly from the 41% growth rate reported last quarter, 46% in Q2 22 etc. This is a common trend I have seen across many technology companies (see my other analyses). I believe this has been caused by a slowdown in the global macroeconomic environment, which has called for delayed spending. A positive for Similarweb is the company operates with a "product led" growth strategy. This includes a free trial and free usage of many elements of the platform. Therefore, I believe the company can still continue to acquire customers cheaply, and then upsell the paid product to the most engaged customers, which could get easier as economic conditions improve.

{kind=link}

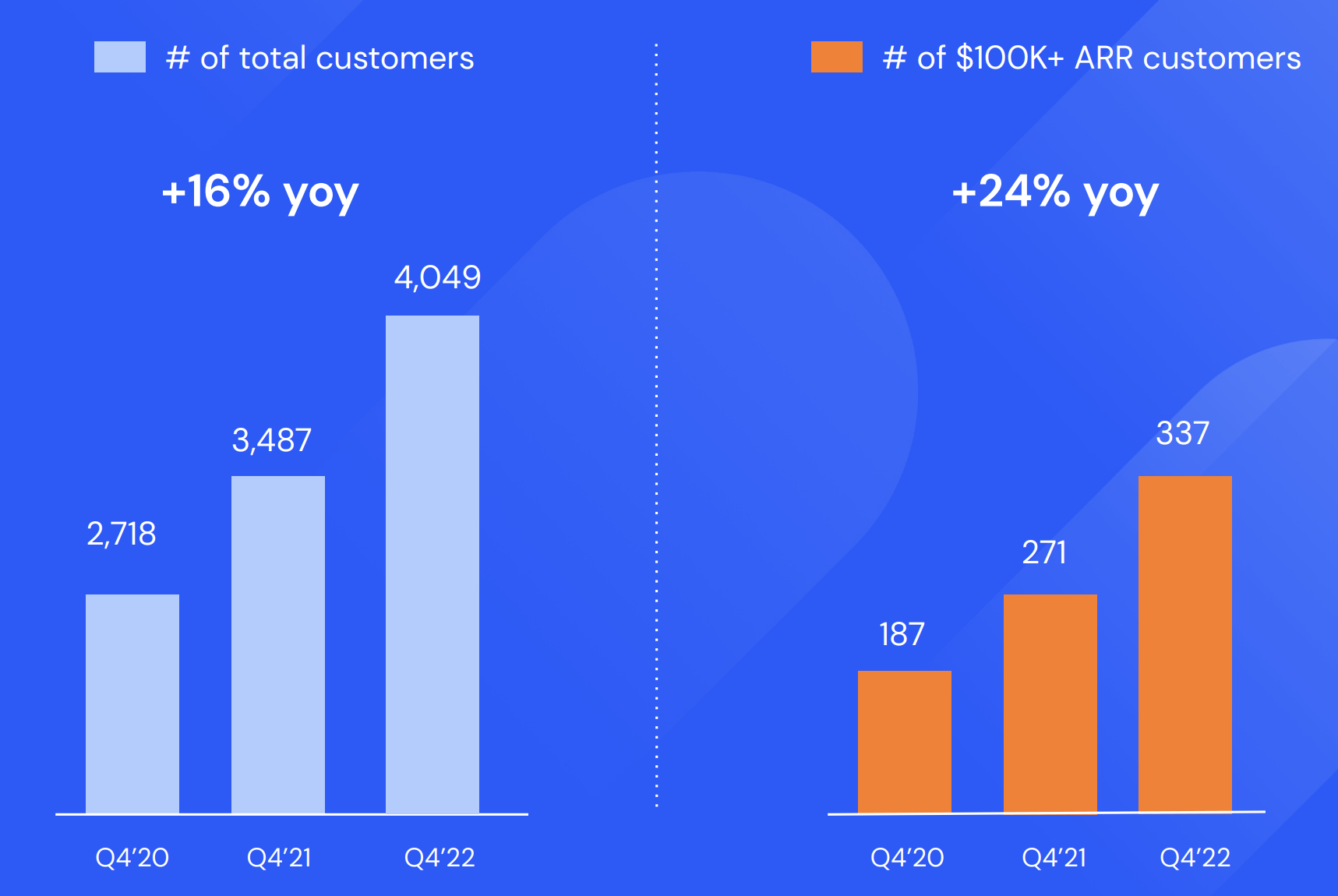

The top line result was driven by solid customer growth of 16% year over year to 4,049 in total. It should be noted Similarweb is "moving upmarket" with its customer acquisition strategy and grew its larger customers with over $100,000 in ARR by 24% year over year to 337. This is a positive sign in my eyes as larger organizations tend to be more "sticky" by nature, with higher retention rates and greater opportunities for contract value expansion.

{kind=link}

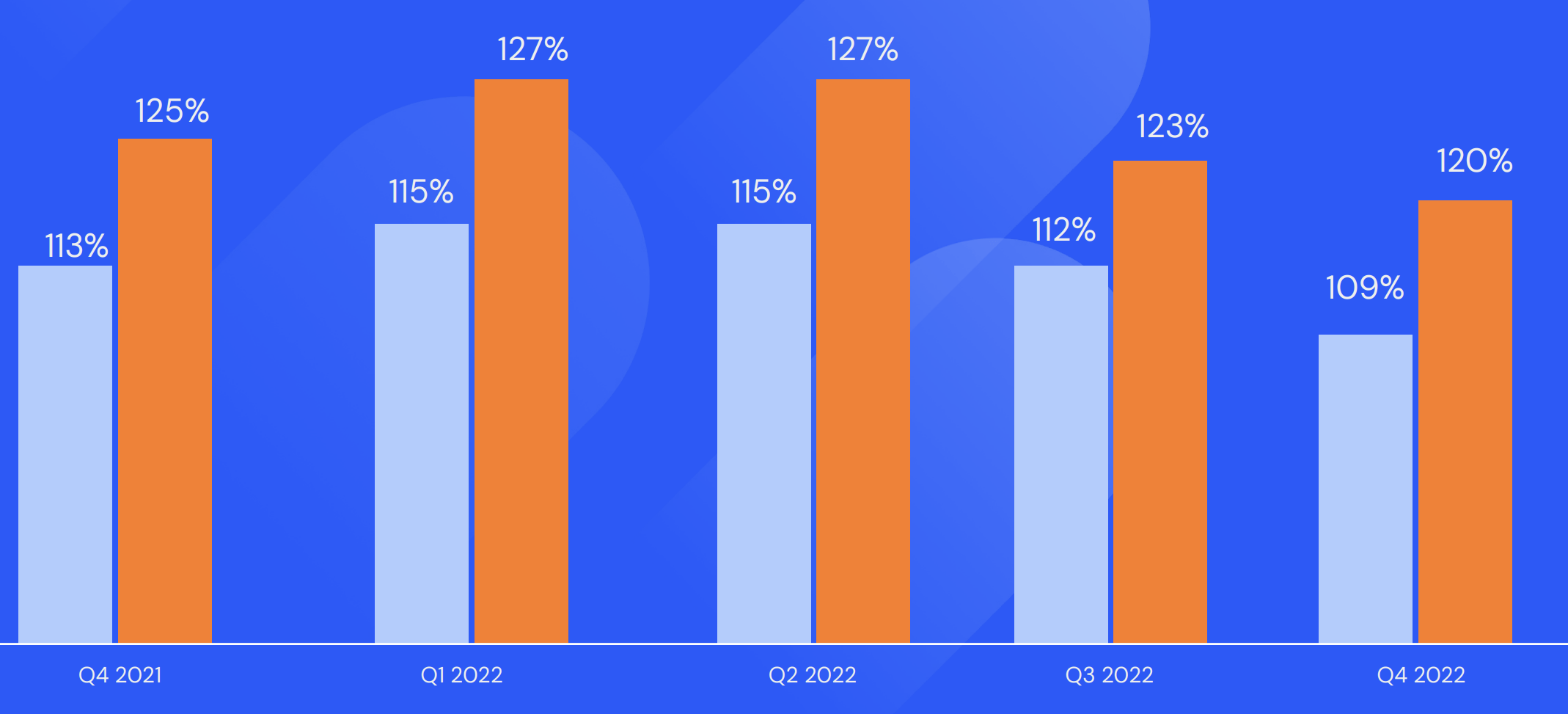

If we dive into the company's retention rate, we see this confirms my hypothesis, with its larger customers having an average net dollar retention rate of 120%, versus the 109% average for all its customers. It should be noted that its retention rate has dropped slightly from 113% in Q4 '21 to 109% by Q4 '22. Overall, I would expect this as I believe customers are delaying extra spending due to the macroeconomic environment.

{kind=link}

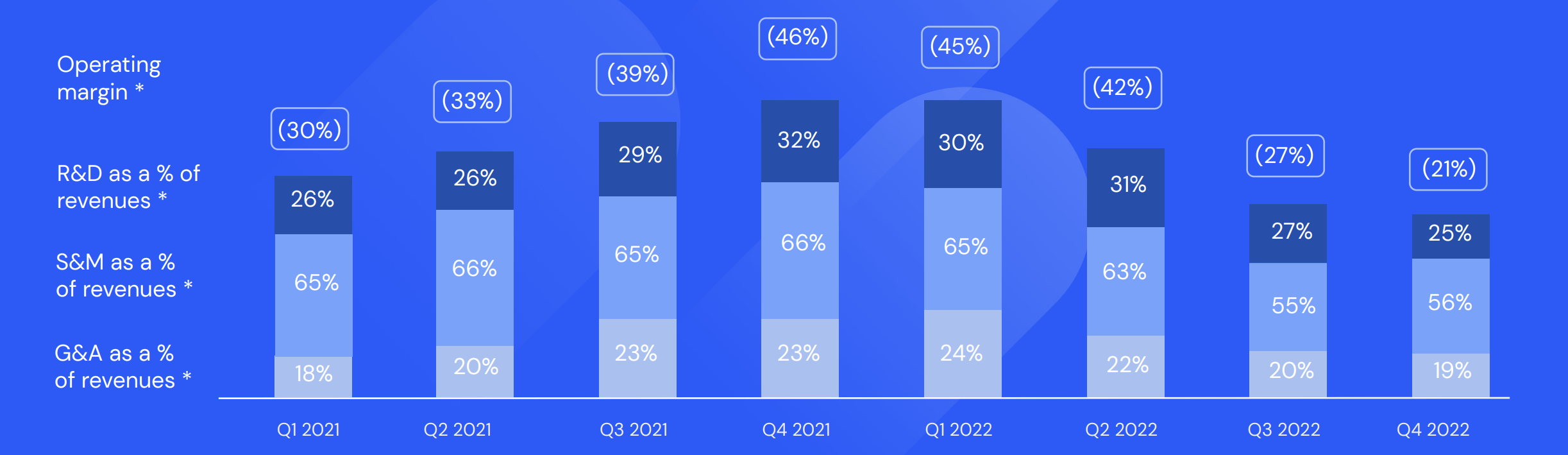

Moving onto earnings, the company reported earnings per share [EPS] of negative $0.20, which beat analyst estimates by $0.04. This is also an improvement over the negative $0.32 per share reported in Q4 '21. This has mainly been driven by lower sales and marketing revenue, as a portion of the total. This metric has been reduced from 66% of revenue in Q4 '21 to just 56% of revenue by Q4 '22. This has been driven by brand growth, improved customer acquisition costs and the company scaling back its marketing spend due to the macroeconomic environment. In management's model, they forecast Sales & Marketing spend to contribute to 35% of total revenue, "long term". Although they do not allude to exactly when "long term" is, I will discuss more on this in the valuation and forecasts section.

{kind=link}

Similarweb has a steady balance sheet with $77.8 million in cash and short-term investments, in addition to $74.2 million in total "debt" which looks to be manageable. As I believe the majority of this "debt" ($40 million) is actually long-term operating lease liabilities, thus not technically debt. In terms of pure "debt" on its balance sheet, the company reports $25 million in current debt related to credit facility borrowings.

Valuation and Forecasts

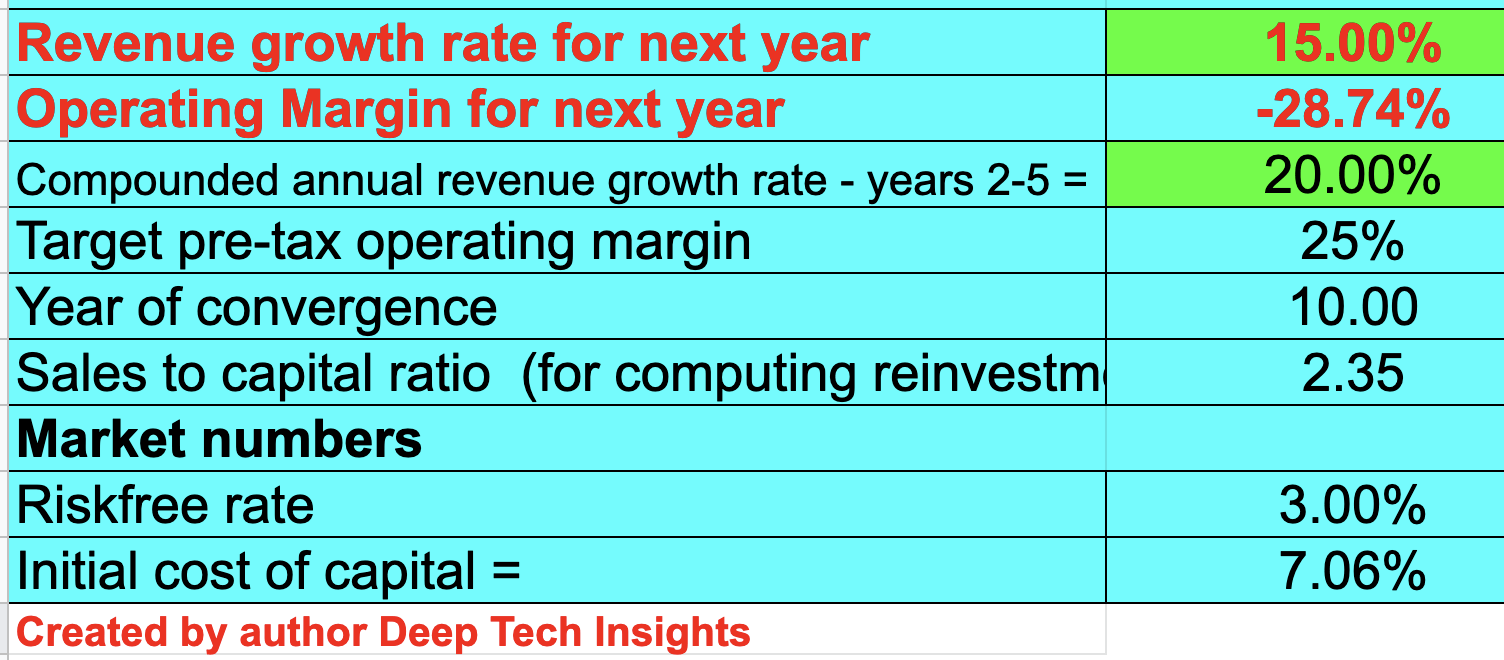

In order to value Similarweb, I have plugged the latest financial data into my discounted cash flow valuation model. I have forecast just 15% revenue growth for "next year", which is aligned with management's guidance for the full year of 2023. This slower growth rate follows the current trend and is expected due to the "recessionary" environment I will discuss more about in the "Risks" section. In addition, management is focusing less on growth (sales/marketing) and more on profitability given the environment.

In years 2 to 5, I have forecast a faster 20% revenue growth per year, as I believe Similarweb will be able to better monetize its existing customer base, as economic conditions improve in the future. The economy and human psychology tends to be cyclical by nature, but as Similarweb uses a product-led growth strategy, it should be able to position this effectively.

Similarweb stock valuation 2 (created by author Deep Tech Insights)

{kind=link}

To increase the accuracy of my model, I have capitalized the company's R&D expenses which has boosted net income. I have forecast a pre-tax operating margin of 25% "long term", which is aligned with management's guidance. In this case, I have categorised "long term" as 10 years, which I believe is a sufficient amount of time to achieve growth.

Similarweb stock valuation 2 (Created by author Deep Tech Insights)

{kind=link}

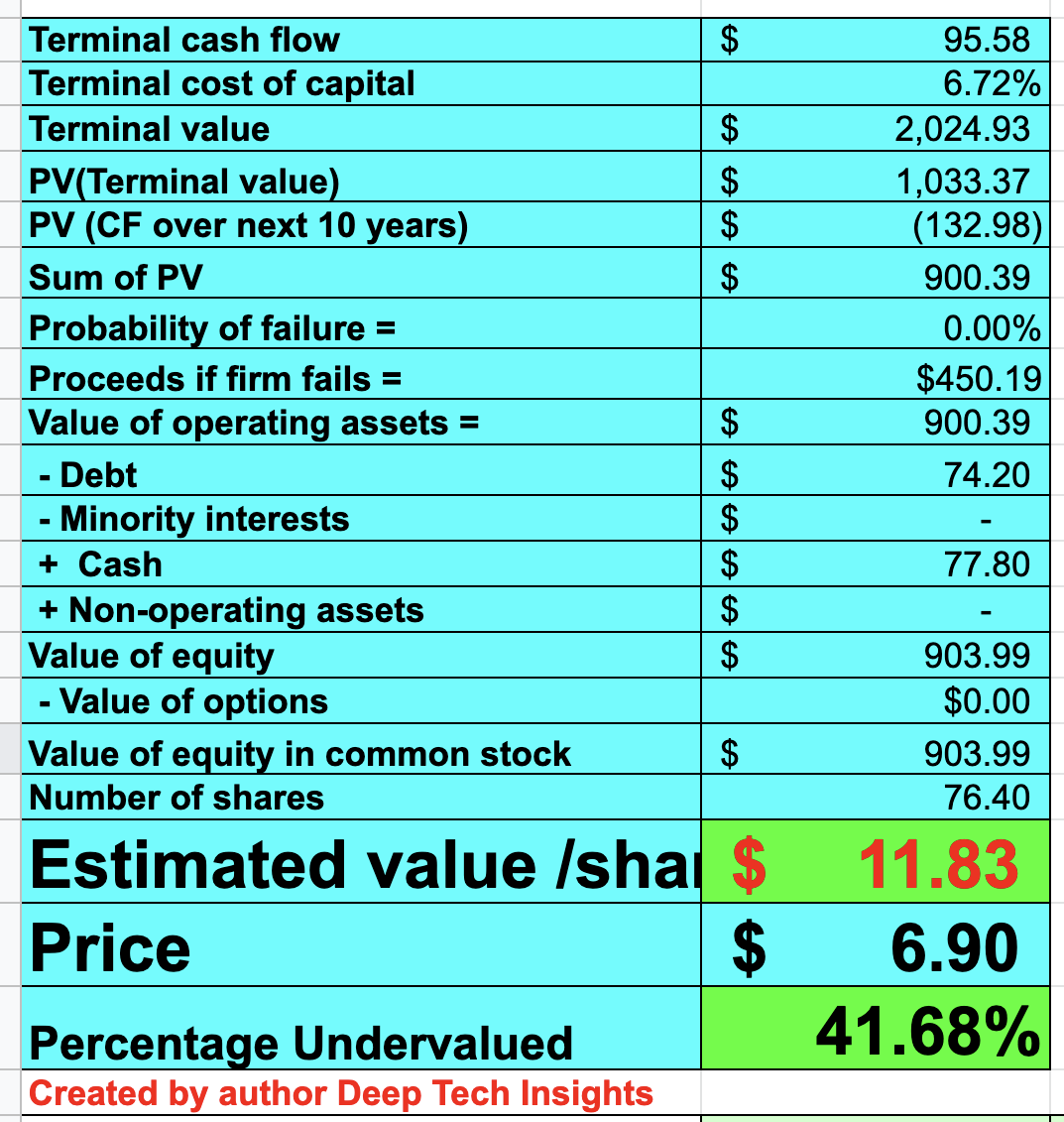

Given these factors, I get a fair value of $11.83 per share, the stock is trading at ~$6.90 at the time of writing, and thus it is ~41.68% undervalued.

Similarweb also trades at a price to sales ratio = 2.7, which is cheaper than its historic high of over 7 in early 2022.

Risks

Cash Burn and Share Dilution

Similarweb reported negative $85.2 million in operating losses for the full year of 2022. Without improvement in this metric, the company would "burn" through its $77.8 million cash and short-term investments position in less than one year, after which the company would need to raise capital which could dilute shareholders. Given the stock price has been hammered, raising capital during this time is not a good idea, due to the high cost of equity. A positive for Similarweb is its operating margin has been improving over the last few quarters. For example, the company reported negative $15.7 million in operating income in Q4 '21. Therefore, if this trend continues (as management is hoping), the company may be able to avoid raising more capital.

Final Thoughts

Similarweb is an intriguing company which offers insightful data with a fantastic user interface to complement this. I personally have found value in the market research part of the product and I can see why many companies have found value too. Its move into "sales intelligence" data will be a tougher battle due to the high competition, but the TAM across all its markets is worth billions of dollars. Given SMWB stock is undervalued intrinsically according to my model and forecasts, I will deem the stock as a "buy".

For further details see:

Similarweb: Undervalued With A $44 Billion Big Data TAM