KRE - Simmons First National: Resilient Amid Regional Bank Fallout

2023-06-17 02:27:14 ET

Summary

- Simmons First National Corporation is a small regional bank with a 120-year track record of avoiding unnecessary risks and focusing on creating shareholder value.

- The bank has experienced a downturn in stock price but has continued to meet its objectives, with insiders buying shares during the recent decline.

- The bank's resilience, growth, and efficiency initiatives could lead to a return to pre-Silicon Valley Bank blow-up levels, representing a gain of over 30% from its current price.

Simmons First National Corporation (SFNC) is a small regional bank located in Pine Bluff, Arkansas. The bank offers typical services to its customers in the way checking, savings, and certificates of deposit as well as loans on real estate, agricultural finance, equipment lending, and SBA lending. It also offers consumer products and services including credit cards and investment services.

While those things listed above are table stakes for any small regional bank, there are several factors that set Simmons apart from many of its peers.

Tried-And-True

The bank has been in business since 1903. During that time, it has been able to operate continuously through World War I, the influenza pandemic of 1918, the roaring 20s (without overextending itself), the Great Depression, World War II, Korean War, the Kennedy assassination, Vietnam, Nixon resignation, and many other history-making events. Through all of that, and much more, Simmons muddled through, serving clients and generating profit for shareholders. What is impressive is not only that the company was able to operate, but that it paid dividends to its shareholders the entire time and continues to this day. Simmons has paid cash dividends to shareholders for 114 consecutive years. That feat puts it in the same league as other better-known dividend aristocrats like Coca-Cola ( KO ), Procter & Gamble ( PG ), Exxon Mobil ( XOM ), and Eli Lilly ( LLY ). I view this as proof of conservative and diligent management with a long-term focus while making shareholder value a priority.

A World Apart From Silicon Valley

The bank's footprint spans much of the south-central U.S. Specifically, the bank owns and operates 231 branches in Arkansas, Kansas, Missouri, Oklahoma, Tennessee, and Texas. Again, on the surface this might not seem that interesting, but its area of operations has likely insulated the bank from much of the nonsense that has taken down several regional banks and has caused the entire regional banking industry to decline. Operating in consistent businesses lines with the same type of customers the bank has had for 120 years has allowed it to avoid being caught up in high-flying ventures, or unnecessarily risky behavior.

In other words, the bank has continued to perform well, growing its balance sheet, shareholder equity, and dividends despite the turbulence elsewhere in the regional banking industry. However, its stock price has not been immune to the downturn despite the fact the company continues to meet its objectives.

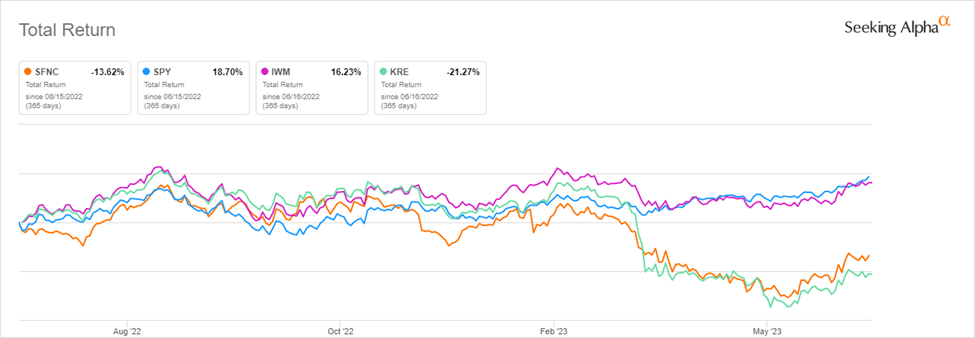

Over the last year, Simmons has declined more than 13% on a total return basis. While it is outperforming the broader regional banking space, it is underperforming both small cap and large caps as measured by the iShares Russell 2000 ETF ( IWM ) and the SPDR S&P 500 ETF Trust ( SPY ).

{kind=link}

Beyond the exceptional 120-year track record, avoidance of unnecessary risks, and focus on creating shareholder value, there are several other positive factors that could drive share prices higher.

Insider Buying

Insiders have been buyers of the stock during this most recent turndown, mostly during April and May. There are many reasons for insiders to sell shares, but generally only one to buy them: they believe the stock is undervalued by the market.

For example, on May 1 the CEO Robert Fehlman purchased 12,000 shares while senior executive vice president Stephen Massanelli purchased 10,000 shares on the same day. Director Edward Drilling picked up 6,000 shares while on May 3 board chairman George Makris bought 10,000 shares. During that period, there were numerous officers and directors that exercised options to purchase shares. It is reasonable to view this as a vote of confidence in the bank and its continuing operations in the face of a challenging environment.

Tailwind From A Resurgence in Small Caps

Given that Simmons is a small cap regional bank, it is held within numerous ETFs and other funds including the SPDR S&P Regional Banking ETF ( KRE ) and the iShares Russell 2000 ETF ( IWM ). These are two widely followed and traded funds. The KRE has suffered due to the failures at Silicon Valley Bank, Signature Bank ( SBNY ), and First Republic Bank ( FRCB ), as well as concerns that there might be other landmines yet to be found.

However, Simmons is one of about 140 other holdings in KRE, the vast majority of which will likely avoid any major issues. Most of these banks, like Simmons, are well run, and are now trading at depressed values. During a recovery in the space, it is reasonable to expect the rising tide to lift all boats, including Simmons. It is a good bank temporarily caught in an out of favor area, and that creates an opportunity for investors.

Similarly, small cap stocks have underperformed their large cap counterparts. This underperformance creates an opportunity for investors to play catch-up with the broader market. In other words, many investors have been overly pessimistic on the market and are holding relatively high levels of cash. As the market continues to climb, these investors are not fully participating. To catch up, they will need to put that cash to work. I suspect that much of that cash will be deployed in areas that have underperformed rather than mega cap tech stocks. In that scenario, small caps benefit. And like what I expect for regional banks, I think it is reasonable that a closing of the performance gap between large and small will push most small cap names higher.

Managing Risk

Simmons has done a good job diversifying its interest rate exposure as well as hedging it as necessary to continue generating stable returns. The real estate loan portfolio has about 6% exposure to office space, a factor that protects it from catastrophic losses as companies reassess their office space needs. Furthermore, that exposure, as well as all real estate exposure, is spread across several states, and those states are generally less exposed to the work from home trend relative to New York, San Francisco, and other major coastal metropolitan areas. The Dallas and Houston metros are the largest geographical exposures within the real estate loan portfolio.

Valuation

Relative to its own history Simmons is trading below multi-year valuation measures. Specifically, it is trading a steep discount to book value at only 0.68x.

| Valuation Metric |

| SFNC |

| SFNC 5-Year Average |

| % Difference to 5-Year Average |

| P/E GAAP ((FWD)) |

| 11.25 |

| 11.33 |

| -0.71% |

| P/Book ((FWD)) |

| 0.68 |

| 0.91 |

| -25.38% |

| Book/Share Q1 2023 |

| $26.24 |

| Tangible Book/Share Q1 2023 |

| $14.88 |

Relative to a sample of peer regional banks, it is difficult to determine if Simmons is cheaper. While it is trading at a lower valuation when looking at the multiple to book value, its P/E is on the higher end. While peer comparisons can be useful, it is important to keep in mind that the entire industry has experienced a sell-off, resulting in depressed values across many companies and also creating dislocations within the space.

| Valuation Metric |

| SFNC |

| First BanCorp ( FBP ) |

| WSFS Financial Corp ( WSFS ) |

| Ameris Bancorp ( ABCB ) |

| P/E GAAP ((FWD)) |

| 11.25 |

| 8.75 |

| 9.11 |

| 8.11 |

| P/Book ((TTM)) |

| 0.70 |

| 1.63 |

| 1.04 |

| 0.75 |

| Dividend Yield ((FWD)) |

| 4.33% |

| 4.37% |

| 1.53% |

| 1.69% |

Dividend

The dividend has sufficient coverage and continues to be safe. This is unsurprising given the company's 114-year track record of paying cash dividends. Simmons continues to focus on creating shareholder value, and while the recent dividend growth rate has dipped below historical averages, continued growth initiatives combined with recent cost savings provide reasons to believe that this will revert to long run levels.

| Dividend Growth or Coverage Metric |

| SFNC |

| SFNC 5-Year Average |

| % Difference to 5-Year Average |

| Cash Dividend Payout Ratio ((TTM)) |

| 30.51% |

| 51.81% |

| -41.12% |

| Dividend Coverage Ratio |

| 2.03 |

| 3.16 |

| -35.93% |

| Dividend Growth Rate 5Y ((CAGR)) |

| 7.24% |

| 7.66% |

| -5.54% |

| 1 Year Dividend Growth Rate ((TTM)) |

| 5.48% |

| 8.88% |

| -38.32% |

Profitability

Similar to the dividend metrics, some profitability metrics have dipped below long run averages. Again, I do not view this as a cause for concern. The environment has been challenging for most banks, particularly small regional banks, and a slight decline in these ratios is to be expected. With monetary policy moderating while the broader economy remains healthy, it is reasonable to expect margins to improve in the coming quarters.

| Profitability Metric |

| SFNC |

| V 5-Year Average |

| % Difference to 5-Year Average |

| Net Income Margin ((TTM)) |

| 27.64% |

| 30.79% |

| -10.24% |

| Return on Common Equity ((TTM)) |

| 7.52% |

| 9.02% |

| -16.63% |

| Return on Total Assets ((TTM)) |

| 0.86% |

| 1.11% |

| -22.72% |

Risks

Like any stock and any bank, there are numerous risks. The broader market could encounter headwinds, dragging down small caps and regional banks further. Uncertainty around monetary policy might have the dual impact of making existing loans less profitable while slowing the growth in new loans. Losses on loans could exceed what is expected, reducing the profitability of the bank. Furthermore, as the largest exposure in the loan portfolio is to Texas, a slowdown in the state could have a material impact on Simmons' earnings.

The expansion of the bank through acquisitions could slow or create new unforeseen issues. Bank management is targeting about $15 million in annual noninterest expense cost savings for 2023. While management has achieved about 50% of that goal to date, there is a risk that they fall short, resulting in lower-than-expected earnings for this year, and likely next year.

Deposits could shrink, contributing to a possible slowdown in lending. A bank run is unlikely as the risks experienced by Silicon Valley Bank and others have largely been mitigated by Simmons management. Simmons has a broadly diversified depositor base with the largest 20 depositors representing only 8% of the total. Furthermore, of the total deposits, only about 23% are uninsured, and in the case of a problem, those deposits are covered two times over by other sources of liquidity.

Outlook

Given the resilience of the bank combined with currently underway growth and efficiency initiatives, it is reasonable to expect the stock to return to its pre-Silicon Valley Bank blow-up levels. This would mean a price target of $24/share, representing a gain of over 30% from its current price.

Final Thoughts

I typically don't cover under the radar small cap banks, but I think this is a special case. I am always interested in companies that have been in business for extremely long periods, and even more so when they have a history of paying dividends consistently for over 100 years. Given what has happened in the regional bank industry, it is reasonable to believe that Simmons was sold-off with others in its industry due to fear. While I generally believe that the market is mostly efficient most of the time, the combination of an under covered stock in an out of favor industry creates an opportunity for investors. I am not a banking expert but see the value and potential in this stock. That said, given that it is a small company with idiosyncratic risks, I suggest that any position in the stock be sized appropriately. Any position in this stock needs to be considered carefully to understand its impact on long-term total returns and long-term investment objectives. Thank you for reading. I look forward to seeing your feedback and comments below.

For further details see:

Simmons First National: Resilient Amid Regional Bank Fallout