KLPEF - Simon Property Group: 7.1% Yield Is Not Enough

2023-10-14 06:08:31 ET

Summary

- Simon Property Group is the largest owner of shopping malls in the US, but there are better alternatives in the REIT retail segment.

- The company's revenues primarily come from rental income and are not well-diversified internationally.

- Despite the impact of COVID-19, SPG has shown resilience with a recovery in occupancy and operating profitability, but its growth prospects are not particularly impressive.

Simon Property Group (SPG) offers a high-dividend yield, but there are other better alternatives in the REIT retail segment.

Business Overview

Simon Property Group is a self-managed Real Estate Investment Trust ((REIT)) that owns shopping malls and other retail assets across the U.S. and internationally. Its current market value is about $35 billion, being the largest owner of shopping malls and retail centers in the U.S., owning a portfolio of about 240 properties spread across 14 countries.

SPG is also the largest shareholder of Klepierre (KLPEF), a French REIT that owns shopping malls that I've covered in the past , giving it indirect exposure to this industry in Europe.

Nevertheless, the vast majority of its revenues come from rental income (about 95%) and more than 90% of its revenues are generated in the U.S., being therefore not much diversified by this measures compared to other REITs that have also expanded to other services and have increased international expansion in recent years.

At the end of last June, its property portfolio had a gross value of about $38.7 billion, plus it also had stakes in Taubman Realty Group (valued at nearly $3 billion), Klepierre ($1.5 billion) and other unconsolidated entities in the value of $3.4 billion.

Historically, the company has a good growth history since it has been a public company 30 years ago, both through acquisitions and new developments, a strategy that is not expected to change in the near future.

As I've covered recently on Prologis (PLD), the penetration of e-commerce sales has steadily increased over the past decade in the U.S., and this trend is likely to continue over the next few years. While this is positive for a company like Prologis, which owns warehouses that are key for online retailers to distribute goods in a rapid pace to customers, this structural trend is a headwind for SPG that relies heavily on physical store sales.

However, this does not mean that shopping malls and retail centers will gradually cease to exist, but they have to adapt to the current market landscape. Indeed, following the pandemic and a big shift of retail sales to online channels, physical sales have recovered much faster than most predicted, showing that shopping malls are still attractive to customers and an important sales channel for retailers.

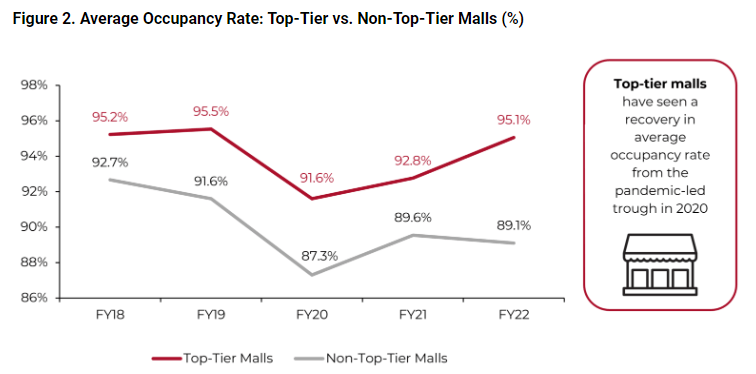

Occupancy has recovered from low points in late 2020 and early 2021 as traffic recovered, and the operating profitability of SPG has also recovered to levels similar to 2019. This also shows that SPG has a quality portfolio in well located areas, being a key factor for long-term resilience of its business model. While some malls are struggling, top-tier malls are maintaining strong levels of occupancy and have seen a rapid recovery to levels close to pre-pandemic, plus physical retail sales also recovered to levels close to 2019.

{kind=link}

This landscape bodes well for SPG, which is mainly focused on top-tier malls, supporting its growth prospects in the near term. Moreover, retailers are increasingly following an omni-channel strategy, combining both online retail and physical stores to boost overall sales, which means that quality and well-located shopping malls should continue to be valued assets for the foreseeable future, despite the expected rise in penetration of e-commerce on overall retail sales.

Financial Overview

Regarding its financial performance, SPG has a mixed performance over the past few years given that its business was naturally negatively impacted by COVID-19, which impacted mainly its financial performance during 2020/21. However, as shown in the next graph, its business recovered quite rapidly compared to pre-COVID, especially regarding its business profitability.

Key metrics (Simon Property Group)

Despite that, SPG's revenues amounted to some $5.29 billion in 2022, an increase of 3.4% YoY, but still some 8% below its 2019 level. This increase in revenue is justified by higher rental income, which amounted to $4.9 billion in 2022 and represented some 93% of total revenue during the last year, which is justified both by higher occupancy rates across its portfolio (94.9% at the end of 2022 vs. 93.4% in 2021) and higher base minimum rent per square meter foot.

Due to good cost control during the last year, despite the inflationary environment, SPG increased its comparable free funds from operations (FFO) to $4.45 billion (+3.5% YoY), or $11.87 per share, which was slightly ahead of its revenue growth.

During the first six months of 2023, SPG maintained a relatively positive operating momentum compared to the same period of last year, given that its occupancy rate and rent base have improved compared to the same period of 2022, which led also led slightly higher revenues and stable earnings.

In H1 2023, SPG's revenues amounted to $2.72 billion, up by 5.6% YoY, supported by lease income growth of 4.2% YoY in this period. Total expenses increased to nearly $1.4 billion, an increase of 5.3% YoY, which means that SPG's operating leverage was quite low over the last six months justifying flat earnings growth in this period.

Indeed, its FFO was $2.1 billion in the first semester, flat compared to H1 2022, or $5.62 per share (vs. $5.61 in H1 2022), while its net income was $938 million (vs. $923 million in H1 2022). Regarding cash flow, SPG has a very good cash generation capacity given that its free cash flow was about $2.1 billion during the first six months of the year.

SPG also upgraded slightly its guidance for the full year, and now expects FFO to be between $11.85-11.95 per share, which is slightly ahead of 2022 level. Going forward, SPG is likely to maintain positive top-line growth, but earnings are likely to remain pressured by higher borrowing costs, while over the medium to long term growth is mainly supported by its investments in new space.

Regarding its balance sheet, due to its large size and good credit profile the company has been able to refinance bonds over the past few months, even though at higher costs, leading to a liquidity position of $8.8 billion. Furthermore, its refinancing needs over the next couple of years are manageable, at some $2.5 billion in 2024 and $1.6 billion in 2025, thus SPG is not expected to have any issues on refinancing in the near term. On the other hand, its leverage position was acceptable at the end of last quarter, given that its net debt-to-EBITDA was 6.2x, a higher ratio than compared to other REITs that have a more conservative position.

Nevertheless, as the company has a good cash flow generation capacity and plenty of quality assets that it may eventually dispose to reduce debt levels, I don't think its leverage position will be an issue in the short to medium term.

Therefore, SPG can use a great part of its cash flow generation to distribute dividends to shareholders, even though its dividend history is not great given that its business was impacted significantly by COVID-19 and the company had to cut its dividend in 2020. At the time, SPG cut its quarterly dividend from $2.10 per share to $1.30, but has been gradually increasing the dividend over the past two years.

Its current quarterly dividend is $1.90 per share, representing an increase of 8.6% YoY, but is still below its 2020 level. This means its annual dividend is now $7.60 per share, which at its current share price leads to a forward dividend yield of about 7.1%. Moreover, this assumes that SPG will not increase even further its quarterly dividend over the next year, which is quite unlikely.

Indeed, SPG's payout ratio based on FFO per share is only 64% based on the bottom of its 2023 FFO guidance, which seems to be a conservative payout ratio and can easily be increased in the near future. However, this doesn't seem to be expected by the street currently given that, according to analysts' estimates , SPG's dividend is expected to be $7.81 per share in 2024 and grow to $8.01 in 2025 and $8.20 in 2026. This seems to be conservative and SPG may increase its dividend above expectations in the coming quarters, which would be supportive for its share price in near future.

Conclusion

Simon Property Group is largely exposed to top-tier shopping malls, which protects its business, to some extent, from structural headwinds for bricks-and-mortars retailers due to the steady rise of e-commerce sales. Nevertheless, after a strong recovery from pandemic lows, its recent growth and prospects aren't particularly impressive over the medium term.

Not surprisingly, the market is not valuing SPG at a high multiple, given that its shares are currently trading at only 8.8x FFO, at a discount to the average of its retail peers, which trade at about 10.9x FFO. Due to a relatively low share price (its shares are trading below 50% its peak in 2016), SPG currently offers a dividend yield of more than 7%, which at first sight seem to be attractive to income investors.

However, from a yield perspective, this is not much higher than Realty Income (O) for instance, which I've covered recently , and is a better long-term investment in my opinion than SPG due to superior fundamentals and growth prospects. Therefore, while SPG currently offers a high-dividend yield, this doesn't seem to be enough to make it an interesting income play presently.

For further details see:

Simon Property Group: 7.1% Yield Is Not Enough