UNBLF - Simon Property Group: A Fine REIT But Better Alternatives Exist

2023-07-14 12:31:58 ET

Summary

- Simon Property Group, Inc. reported $4.4 billion in FFO for 2022, a 5% increase compared to pre-pandemic levels in 2019, showing its resilience during crisis periods.

- Despite a slight potential undervaluation, I suggest considering alternatives to Simon Property Group, such as Unibail-Rodamco-Westfield SE or W. P. Carey Inc.

- These two alternative ideas may offer higher total returns while suiting different types of investors who are, however, considering maintaining their exposure within the REIT space.

As a long-term Simon Property Group, Inc. (SPG) shareholder, I can't complain much about the company. I find SPG to be a well-managed, shareholder-friendly real estate investment trust, or REIT. CEO David Simon is a competent leader who has forged a solid organization, prioritizing balance sheet strength and quality locations over aggressive growth, choices that, in times of distress like during the COVID pandemic, proved to be correct.

To fully appreciate these words, investors should look no further than to how Simon's funds from operations ("FFO") has evolved vs. its pre-pandemic levels in 2019. For 2022, Simon reported $4.4 billion in FFO, a 5% increase vs. 2019. The results were approximately flat at $12 per share when accounting for a slight share dilution. However, Simon's closest peer, The Macerich Company (MAC), reported an FY22 FFO of $437.5 million, an 18.5% decrease vs. its pre-pandemic levels. Once accounting for shares dilution, results were an even more unmitigated disaster of $1.96 in 2022 vs. $3.54 in 2019, a 44.6% decrease.

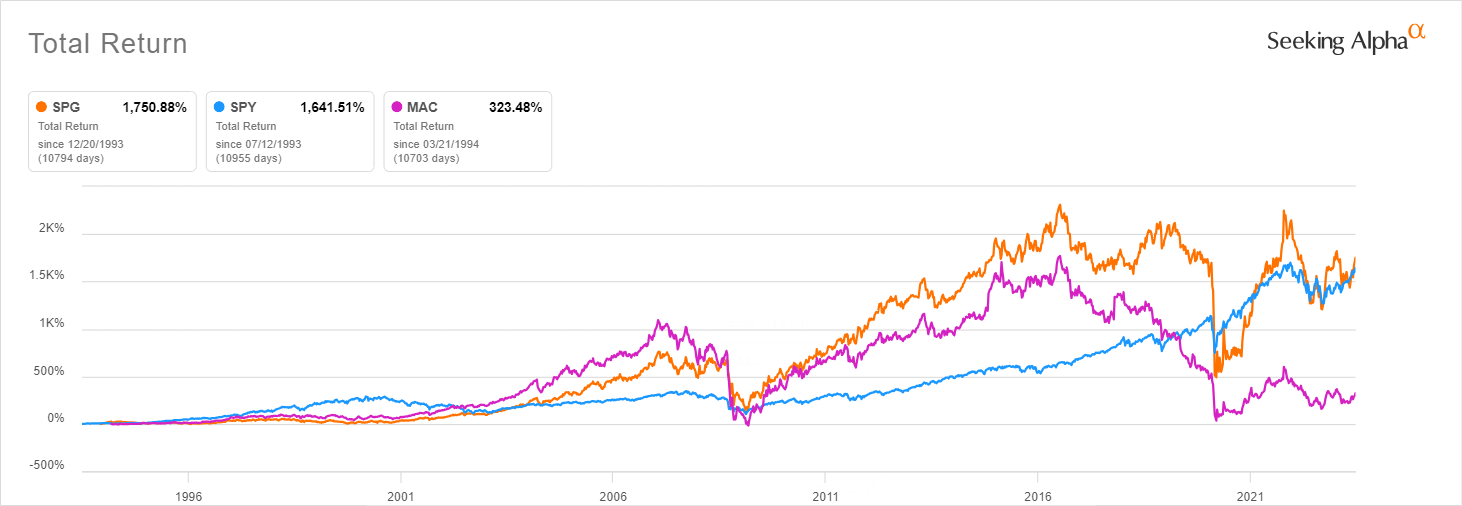

Simon has proven capable of handling crises and has been a fine choice in the mall REIT space. Even if its last ten years of performance lags behind the indexes, its long-term track record remains strong.

{kind=link}

SPG's 2023 forecast

For the current year, SPG guided investors to an FFO result of $11.80 to $11.95, again more or less flat y-on-y, as the company will probably hit the high end. For 1Q23, the FFO was $0.04 higher than the previous year at $2.74, but it missed analysts' consensus. The lack of more vigorous growth was somewhat concerning, especially since consumer spending was strong, and consumption growth accelerated sharply from 1.0% to 3.7%. However, during the Q1 earnings call , David Simon observed that 1Q23 FFO was impacted by "a $0.13 lower contribution from our other platform investments ((OPI)) compared to Q1 2022." However, Simon also said he expects FY OPI contribution in line with 2022, with the retail portfolio turning to a small profit in Q2 and Q3 before making a significant contribution in Q4 due to holiday season shopping.

Regardless, I am not entirely cozy with Simon's ever-increasing venturing on the other side of the retail industry. Despite continuous reassurances about profitability and the idea that the landlord's competencies can be leveraged to improve retailers like JCPenney, I'd be more comfortable with Simon sticking to its core real-estate business. David Simon seems to agree to some extent, figuring a successful exit from the ventures by SPG at some point during the next cycle:

I expect more growth from that category. Same time, 10 years from now or five years from now, we don't own in any of these companies (David Simon, 1Q23 earnings call Q&A).

The valuation

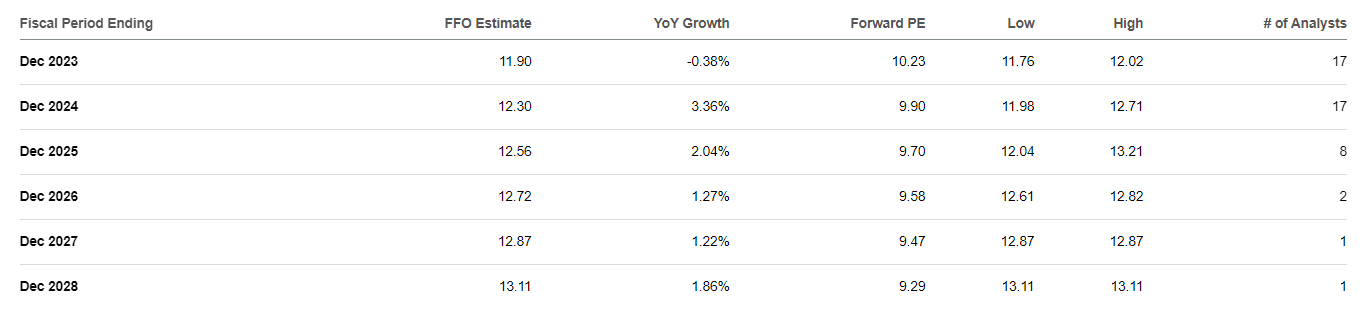

Based on the current FY estimates and share price hovering around the $120 level, SPG trades at about 10x fwd FFO. Is it fair? Several years back, the company used to command much higher multiples, so a fair value in the 14x - 16x region would have been the ongoing assumption. Morningstar still assigns a $150 fair value that indeed considers a fwd FFO multiple of approximately 13x adequate.

While I agree that Simon could be mildly undervalued here, I wouldn't bet on the market accumulating shares based on this potential undervaluation. Still, the market has gone up recently, and so has SPG.

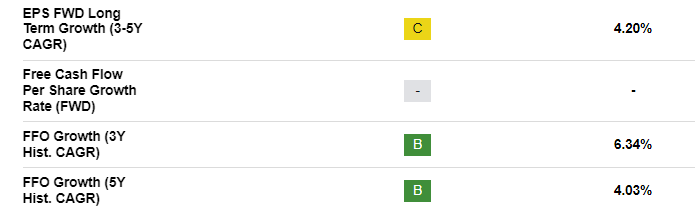

While waiting for SPG to hit the $150 long-term target, investors could bank the current 6.1% dividend yield ($7.4 annual payout) and expect a mild 1%-3% growth. Perhaps the total return potential could lay in the 12% - 13% region if the price target is achieved in 5 years, which is okay but still unremarkable, considering the risks. But if that price appreciation remains unrealized, buy-and-hold investors could be stuck with an 8.1% total return. Indeed, analysts expect SPG to only deliver a 2% FFO CAGR over the next few years.

{kind=link}

For further analysis , I have recently covered SPG's peer Unibail-Rodamco-Westfield SE ( UNBLF , "URW") and assigned the stock a Strong Buy rating. Despite the company not paying dividends at the moment, I consider URW a superior choice to SPG. The company trades at less than 6x FFO (even after a 20%+ run from my original coverage), and even if it is somewhat riskier due to its weaker balance sheet, the higher potential return overcompensates for that. URW could generate a 5-year return between 20% and 25%, even without significant FFO growth.

The risks

For investors willing to bet on the mall REIT space, a potentially better bet could be URW. Regardless of the fact the company seems way cheaper now, another added benefit of such a choice is that, despite the more significant balance sheet risks, the company does not have direct exposure to retailer investments that, in an economic downturn, can cause substantial losses.

If the macro conditions worsen, expect retailers to ditch their weaker physical locations and focus on e-commerce capabilities to produce cost savings. While Simon's locations are typically strong, a headwind could be represented by closures from those online-first brands that have recently added a physical presence in SPG malls, as their primary objective in opening these locations might have been marketing/showrooming, hence more prone to cost-cutting measures.

A potential portfolio swap

Another idea for income investors unwilling to sacrifice yield revolves around potentially swapping SPG with triple net REIT W. P. Carey Inc. ( WPC ). While WPC already commands a higher P/FFO multiple than Simon, it is not unlikely that REITs operating in the triple-net lease space can command multiples in the 16x-18x region. WPC should be no exception.

I assign a target of $89 to WPC based on a 17x P/FFO multiple and fwd FFO of $5.24. While I don't expect WPC to grow much higher than 2% in the short term, I believe the company can return to generate approximately 4% FFO/AFFO and DPS growth over the longer run.

{kind=link}

Based on its current price of about $70 per share, I expect WPC to return about 10% to buy-and-hold investors, which is about 2% higher than SPG, or a potential IRR of about 14%, including the realized capital gain over a 5-years holding period. While the spread doesn't seem huge, a good part of the appeal comes from the fact that I rate WPC a stock much safer to hold through a recession than SPG. Also, this potential overperformance seems due to the fact that SPG has significantly overperformed WPC during the last month:

{kind=link}

But triple-net lease durations are typically longer and harder to break than mall leases. WPC stock has a 5Y Beta value of 0.79 vs. 1.55 for SPG, and the company portfolio is well-diversified by property type, with the safer industrial and warehouse types constituting over 50% of the total. The portfolio is 99.2% occupied, and 99% of it includes rent escalators.

Conclusion

I have been a shareholder of Simon Property Group for years and like the company and its management. The company has done well for me, as the bulk of my position was acquired in 2020 at prices well below $100, but in fairness, the company hasn't performed great in the last decade. With the price recovering to over 10x P/FFO, and considering the alternatives, I wonder whether SPG should remain a foundational holding in my income basket. With e-commerce gaining more and more traction, mall REITs have been a tough sector to invest. While I do not avoid mall REITs, I need to see a large-enough potential upside to remain invested here, and I currently don't see it anymore in Simon Property Group, Inc.

I see two potential replacements here: one is to add to my URW position, which I believe still has a considerable upside. The downside is that URW is a foreign-listed stock currently not paying dividends. Another potential substitute for SPG in my portfolio could be WPC. WPC has a similar yield, slightly better growth prospects, and longer leases (triple-net type) with almost no capex. The tenants pay the leasehold improvements and are typically e-commerce resistant. Hence, I believe the risk of WPC is lower, but the stock could provide a slightly higher total return.

Thanks for reading this analysis. Are you invested in SPG or WPC? Would you recommend a switch (let aside tax implications)? Leave a comment below and share your opinion!

For further details see:

Simon Property Group: A Fine REIT, But Better Alternatives Exist