KLPEF - Simon Property Group Q4 Results: Fundamentals Continue To Improve

Summary

- Simon Property Group's fundamentals continue to improve, but at a slower rate.

- Operational improvements are being offset to a certain degree by higher financing and operating costs.

- At current price, we still believe there is value in the shares, but they are no longer a bargain. We are updating our rating to 'Buy', from 'Strong Buy' previously.

What we've seen from all the high-quality shopping mall companies that we follow is a very similar story this earnings season. Fundamentals continue to improve, but the rate of improvement is slowing down, and some of the benefits from things like higher rents and improved occupancy are being partially offset with headwinds like higher interest expense. The end result being relatively modest NOI growth being guided for 2023. Simon Property Group ( SPG ) was no exception, as it provided very soft 2023 guidance. Still, the valuation remains undemanding and we believe shares remain slightly undervalued. Given the slowing rate of operational improvement, and the fact that shares have significantly rallied since our 'Strong Buy' rating , we are now updating our rating to 'Buy', as we believe it better reflects the current situation. We believe Simon continues to be a good investment option for investors that want to invest in the sector, but want to take less risk given Simon's very strong balance sheet. We see more value in the shares of some competitors, such as Macerich ( MAC ) and Unibail-Rodamco-Westfield ( UNBLF ), but these two are significantly more leveraged compared to Simon. Another interesting mall operator is France-based Klépierre ( KLPEF ), whose results we also recently covered , and where Simon Property Group holds a ~22% interest.

Seeking Alpha

Q4 and 2022 Results

Simon generated $11.95 per share in FFO during 2022 and $11.87 on a comparable basis. This is a modest increase of 3.8% y/y, with portfolio NOI growing 6.3% for the quarter and 5.7% for the year. Q4 FFO was $3.40 per share, which included a net gain of $0.25 per share mainly from the sale of the company's interest in the Eddie Bauer licensing JV in exchange for additional equity ownership in Authentic Brands Group.

Q4 saw retailers increase their sales, reaching a record $753 per square foot with the malls and outlets combined. This was an increase of 6% year over year. This is particularly important, since the company needs healthy retailers to be able to continue raising rents, and there is also some benefit from rents that have a sales-based component.

We believe the biggest disappointment in Q4 came from the 'Other Platform Investments', or OPI segment, which contributed only $0.23 per share in FFO compared to $0.38 in the prior year. In 2022 OPI contributed $0.64 in FFO compared to $1.07 in the previous year. As a reminder, this segment houses many of the retail investments that Simon has made, and these retailers can have high variability in their earnings. Another big headwind came from higher interest expenses, from either floating rate debt that's now higher or increased cost when refinancing.

There were some positives shared during the earnings call as well. One thing that caught our attention is that the company believes their domestic property NOI can probably get back to 2019 numbers, on a run rate, by the end of this year. When asked about occupancy the reply was that they believe it will end the year "slightly up". Perhaps the biggest thing to be optimistic about is that a lot of recent leases will start paying rent in the latter half of 2023 and early 2024, which should provide a nice tailwind for next year. This is what CEO David Simon had to say in that respect during the Q&A session of the call:

We still have a lot of openings scheduled for the latter half of '23 and the early part of '24. So we're not going to see the full contribution of those tenants open until essentially really a run rate at '24, I'd say, sometime in '24. Now you ask why?

Well, because we have a high-quality group of retailers opening in these, and it takes a while to build out their quality stores.

Occupancy & Leasing Spreads

Occupancy for malls and outlets at the end of Q4 was 94.9%, an increase of 150 bps compared to the previous year, and an increase of 40 bps sequentially. Simon reported that leasing remains strong, and that they have a significant number of leases in the pipeline that are scheduled to open in late 2023 and during 2024. Compared to some of its competitors, Simon provides less details about leasing spreads, other than to say that renewals were positive.

During the Q&A session an analyst asked a very good question on why despite some potential occupancy upside and contractual rent bumps, why NOI guidance is so weak at only about 2% growth, and whether that meant that leasing economics were not great. David Simon replied that spreads are positive, but that some operating costs are increasing, and that they are projecting flat sales:

I would say we have positive spreads across the portfolio in renewals and in new leases versus existing leases for new fixed. And again, we also had operating spend increase because we're not immune to security cost increases, housekeeping, all of that normal operating expenses. To some extent, our fixed and bumps don't cover that. We're also projecting flat sales.

Balance Sheet

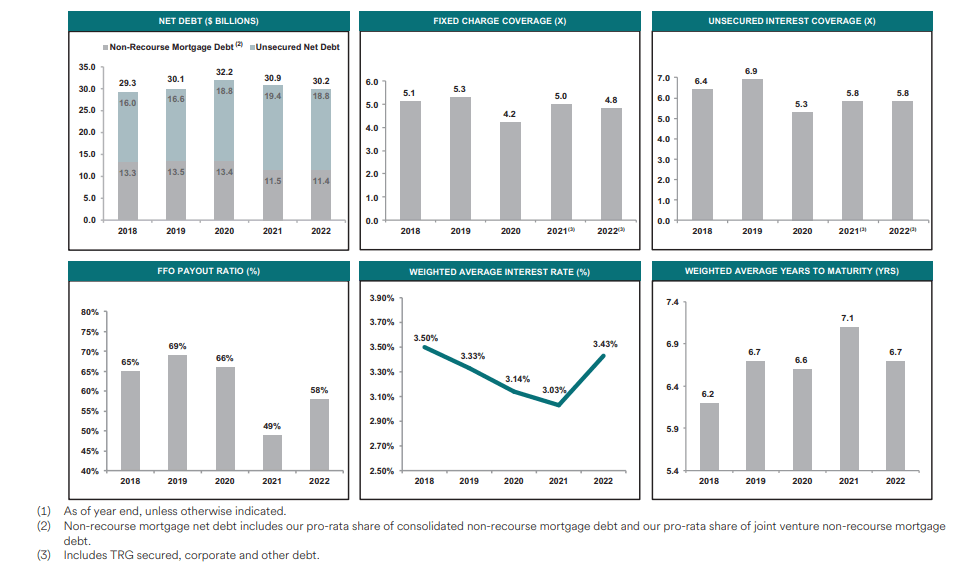

We believe Simon's best competitive advantage is its strong balance sheet, rated by S&P Global ( SPGI ) with an A- grade, and a stable outlook. Simon completed refinancings on 20 property mortgages for a total of $2.3 billion, at an average interest rate of 5.33%. Its fixed coverage ratio is 4.8x, and it ended the year with ~$7.8 billion of liquidity. The company shares in its supplemental a very useful credit slide which can be seen below. Something to note is that the weighted average interest rate is starting to increase in a very meaningful way, and that the weighted average debt maturity is trending down. All of this points to refinancing becoming an increasingly important headwind.

{kind=link}

Guidance

Guidance was disappointing, as the company basically expects to generate a very similar amount of FFO in 2023 when compared to 2022. Comparable FFO guidance is $11.70 to $11.95 per share, and reflects the assumption that domestic property NOI will grow at least 2%. It also assumes increased interest expense compared to 2022 of roughly $0.30 to $0.35 per share, and similar OPI FFO contribution compared to 2022.

Valuation

The good news for investors is that the valuation remains undemanding. Shares are currently trading with a P/FFO ratio of ~10.4x. Analysts expect modest FFO improvements in 2024 and 2025, which we believe to be reasonable based on management comments during the earnings call that a lot of leases will start paying rent in the latter half of 2023 and into 2024. The dividend is well covered and currently yields an attractive ~5.8%. Shares are no longer the bargain they were when we published our previous Simon Property Group article, but we believe they remain a 'Buy'.

Seeking Alpha

Risks

The biggest risks for investors include a weakening economy which could potentially go into recession later in 2023. A rising interest rate environment that is making refinancing significantly more expensive. An inflationary environment that is putting pressure on consumers. A well as the continued competition that e-commerce represents to some of Simon's tenants.

Conclusion

After reviewing Simon's results we conclude that fundamentals continue to improve, but at a slower rate. These improvements are being offset to a certain degree by higher financing and operating costs, resulting in very soft guidance for 2023. Despite the disappointing guidance, we still believe there is value in the shares at current prices. We like some of Simon's competitors even more, but Simon has a stronger balance sheet. There is also a significant number of leases that are scheduled to start paying rent in the second half of 2023 and into 2024. For these reasons we remain optimistic on the company, and we are updating our rating to 'Buy' from 'Strong Buy' previously.

For further details see:

Simon Property Group Q4 Results: Fundamentals Continue To Improve