REG - Simon Property Group Yielding 6% Looks Undervalued Still

2023-07-17 09:00:00 ET

Summary

- Simon Property Group, Inc.'s total return has been 14.13% since last year, with a 7.09% appreciation compared to 5.86% for the S&P 500.

- Despite the growth of e-commerce, physical retail remains dominant, with Simon Property Group's business model not imploding as feared and its mall locations still profitable and integral to society.

- Simon Property Group trades at a lower valuation than its peers, with a 10.11x price-to-FFO ratio compared to the peer.

On 8/19/22, I wrote an article on Simon Property Group, Inc. ( SPG ) discussing how I believed it was significantly undervalued. Since then, SPG has appreciated by 7.09% compared to 5.86% for the S&P 500 (SP500), and when dividends are included, SPG's total return has been 14.13%.

We're headed into Q2 2023 earnings (no announce date yet for SPG), and I feel there is still a long-term opportunity in shares of SPG. Over the past year, management has provided shareholders with 3 dividend increases , taking the quarterly dividend from $1.70 to $1.85 while repurchasing 1.6 million shares . The doom and gloom scenario that was pushed during the pandemic isn't playing out the way some had indicated, and top-tier malls are still a destination for social interactions. While e-Commerce has grown, and Amazon's ( AMZN ) supply chain has created efficiencies where products can be received the next day, physical transactions are still the dominant driver in retail and are expected to grow. SPG has many crown jewels in the mall sector, and I think the panic was overdone, and shares will eventually trade between the $150 - $200 range.

{kind=link}

Looking at SPG from 2019 to the TTM and assessing if their business model is imploding

Everyone has an opinion, and while this article is my opinion, I am going to stick with the facts and then make a determination about SPG's business. When it comes to business, the most important thing is the numbers, so let's dive into what the numbers looked like in 2019 and how they progressed after 2020.

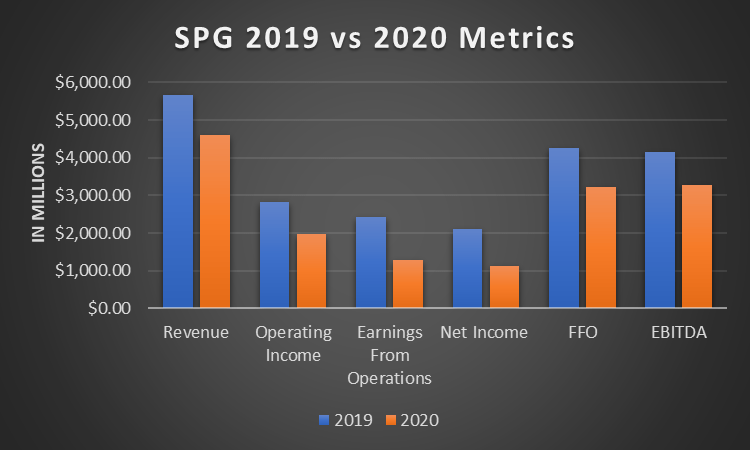

In the 2019 fiscal year , SPG generated $5.67 billion in revenue. SPG produced $2.83 billion in operating income, $2.42 billion in earnings from operations, $2.1 billion in net income, $4.27 billion in Funds From Operations ((FFO)), and $4.17 billion in EBITDA. SPG was operating a cash cow with strong margins. On the bottom line, SPG operated at a 37.06% profit margin, and its FFO ran at a 75.34% margin, while the amount of EBITDA produced was a 73.45% margin.

In 2020, during the height of the pandemic, we saw SPG decline on every income metric. SPG's YoY revenue declined by -18.85% or $1.07 billion. This caused margins to soften and less income to the bottom lines to be produced. SPG's operating income fell -15.2% to $1.97 billion, earnings from operations declined -20.21% to $1.28 billion, net income came in at $1.11 billion as it dropped by -17.44%, FFO declined -18.26% to $3.24 billion, and EBITDA fell -15.79% to $3.27 billion. While SPG was still profitable, its overall revenue declined by over -$1 billion and its profit margin retraced by -12.88%.

{kind=link}

2020 was a rough year for SPG as the narrative around physical retail was negative, and a revolution of displacement through e-Commerce gained traction. While physical retail did struggle, and there was a changing of the guard, physical footprints are still the cornerstone of commerce. Keep in mind the pandemic wasn't officially declared over until 2023, and to this day the ramifications are still being felt.

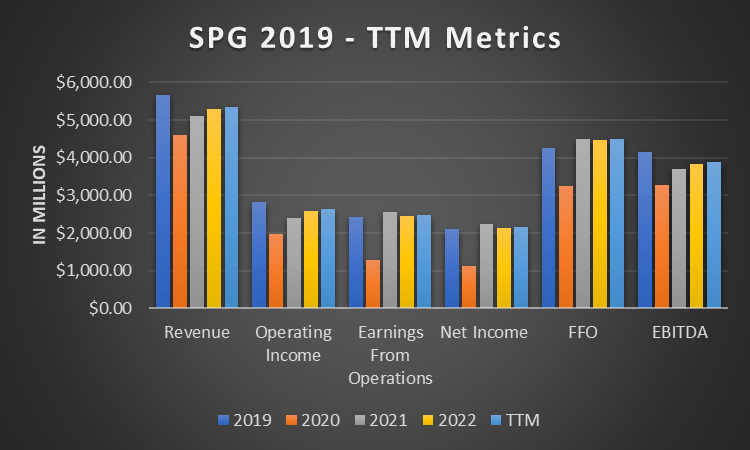

2021 and 2022 were very telling to SPG's operations, as its business would either continue deteriorating from the trends set in 2020 or the business would pick up steam. Over the next 2 fiscal years, SPG saw its annual revenue increase by 14.97%, operating income increase by 31.37%, earnings from operations increase by 92%, net income increase by 92.3%, FFO increase by 38.42%, and EBITDA increase by 17.32%. In the fiscal year of 2022, SPG generated $5.29 billion in revenue, produced $2.14 billion in net income, $4.48 billion in FFO, and $3.84 billion in EBITDA.

After looking at the numbers, which are set in stone, it's not accurate to say the physical retail locations SPG operates in represent a dying business. If the situation from 2020 was going to get worse, the downtrend would have continued for more than one year. Currently, 2020 looks like an outlier looking at 2019 thru the TTM, and if this trend continues, 2020 will look like an anomaly. I am not saying that there aren't problems in the mall sector, but not all malls are created equal, the same way not all real estate is created equal. SPG is still a printing press, and it's locations are engrained throughout the fabric of society. There is a wide moat on the physical side and the threats come from e-Commerce, not other malls, when SPG is concerned. Overall, the model doesn't look like it's imploding, and we will see how the TTM numbers change once Q2 earnings are reported.

{kind=link}

E-Commerce is a threat to physical retail, but it's not the boogie man that some made it out to be

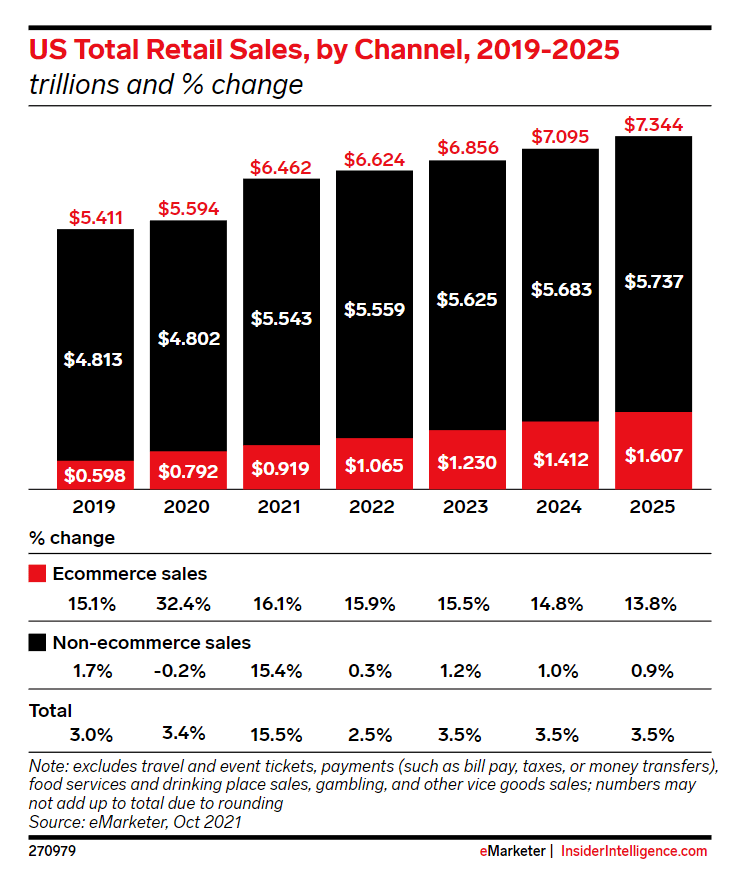

While e-Commerce is growing at a much faster rate than physical retail in the U.S., physical retail is still growing. In 2021, non-e-Commerce sales grew by 15.43% YoY to $5.54 trillion, and by the end of 2025, it's projected that an additional $178 billion of sales will be conducted from physical locations. In 2023, e-Commerce is projected to be 17.94% of total U.S retail sales. In 2025 when total U.S. retail sales are projected to be $7.34 trillion, e-Commerce is only projected to account for 21.88% of the transactions.

These numbers can certainly change, but they are a clear indication that physical retail is currently and will remain the dominant force in the U.S. retail sector. Between these projections and the underlying metrics from SPG's income statement, I feel that SPG will continue to trend upwards on its income statement metrics.

{kind=link}

How SPG is being valued compared to its peers and if there is still an opportunity in its shares

I compared SPG to other REITs that specialize in physical retail to see how SPG's current valuation looks. I used the following REITs as the peer group:

NNN REIT ( NNN ), Federal Realty Investment Trust ( FRT ), Realty Income ( O ), Regency Centers ( REG ), Kimco Realty ( KIM ).

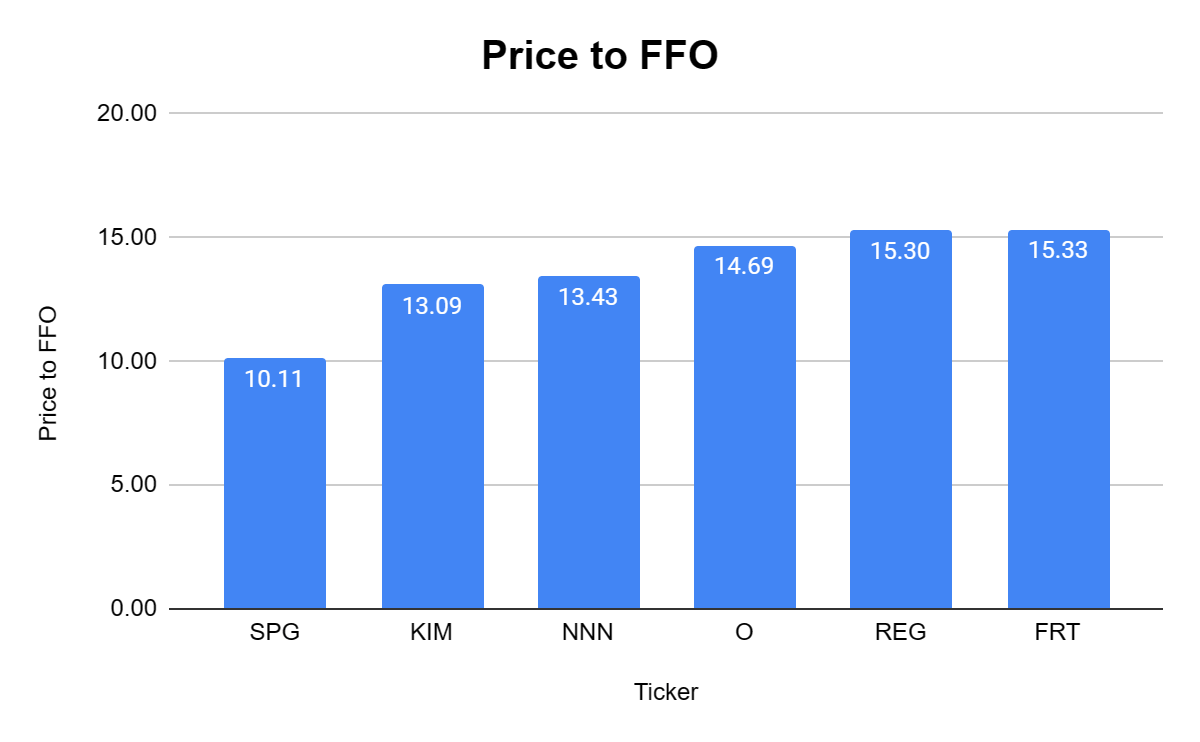

SPG currently trades at a 10.11x price-to-FFO ratio compared to the peer group average of 13.65x. I like paying a low price for a REIT's FFO, so this is very interesting to me.

{kind=link}

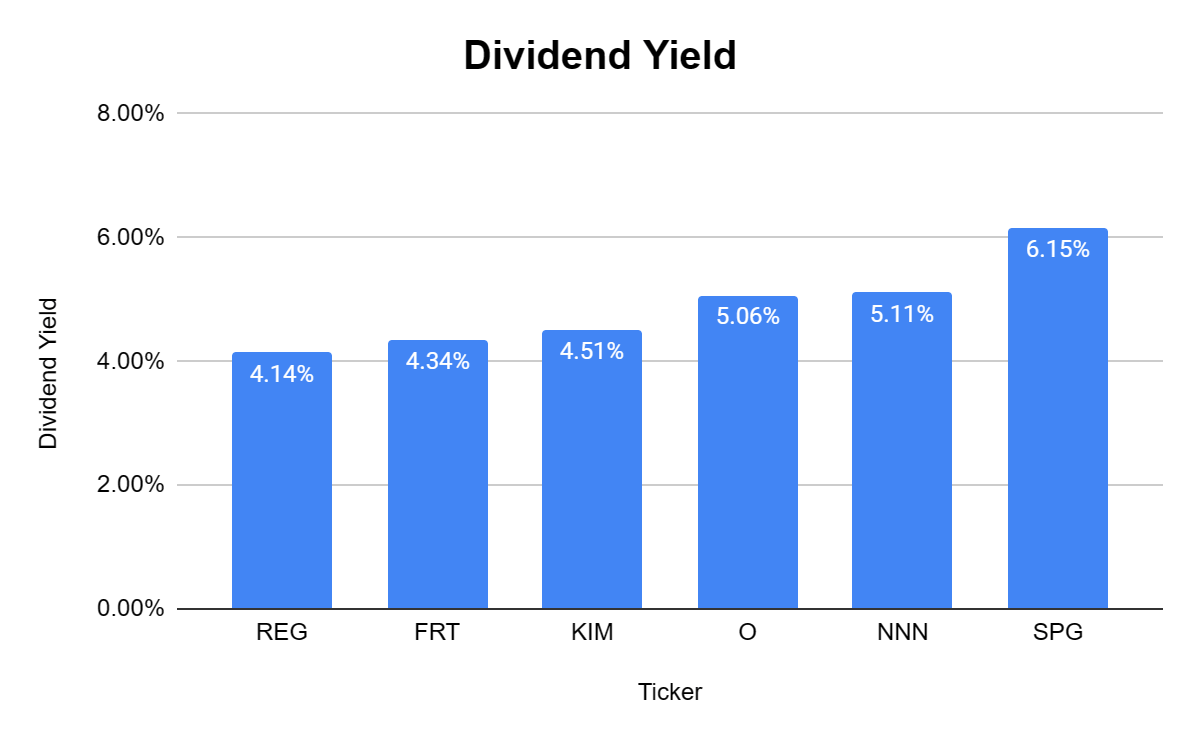

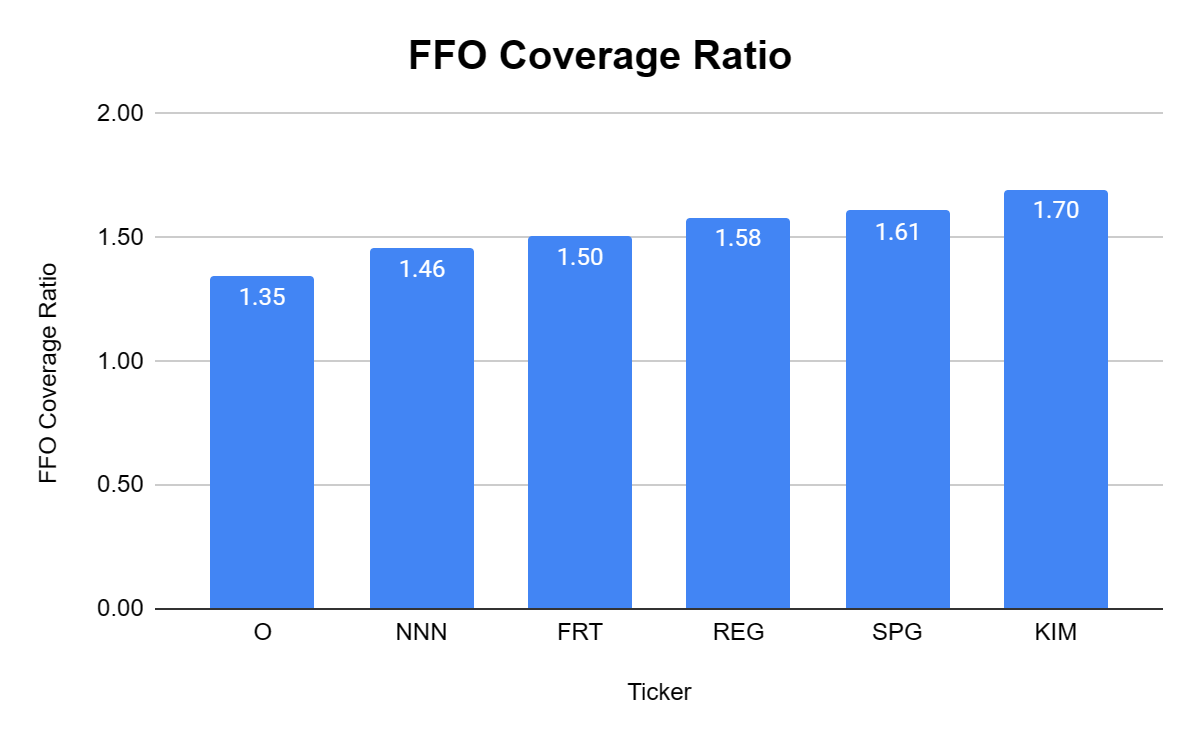

Investing in REITs allows me to invest in real estate and collect income without being a landlord, so the dividend yield and coverage ratio is critical. SPG has a current yield of 6.15%, the largest in the group and above the 4.88% peer group average. SPG also has the 2 nd largest FFO coverage ratio for the dividend at 1.61x. The dividend is fully supported and has a larger yield than I can get in risk-free assets.

{kind=link}

{kind=link}

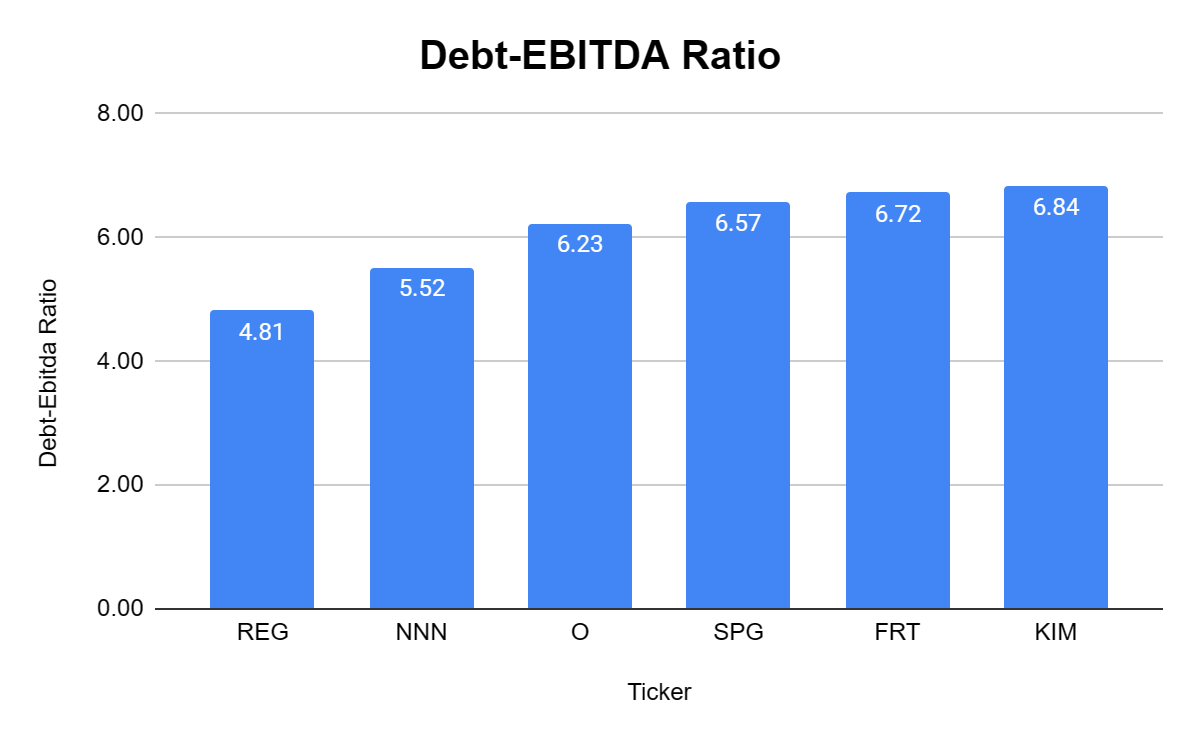

I am not opposed to tapping the debt markets to fund growth, but I don't want to see an outsized amount of debt compared to the EBITDA that is generated. SPG trades at a 6.57x Debt to EBITDA ratio, which is well within my comfort level.

{kind=link}

Conclusion

I like top-tier mall assets because they are an institution for social interaction. Malls aren't just shopping, they are gathering outlets for social engagement which includes shopping, dining, and experiences. While the pandemic propelled e-Commerce to the spotlight, physical retail is still here, and SPG is still a printing press for profits. I am still shocked that SPG trades at a lower valuation than its peers on a price-to-FFO methodology while it generates the largest levels of EBITDA and FFO per share. To trade at the peer group average of 13.66x its FFO, SPG would need to trade at $162.60, and I feel there is a case for them to trade at a premium.

The numbers indicate that Simon Property Group's business continues to improve from the pandemic lows, and management continues to provide shareholders with dividend increases. I think Simon Property Group, Inc. stock is a buy and believe it has the potential to trade between $150-$200 in the future.

For further details see:

Simon Property Group, Yielding 6%, Looks Undervalued Still