SMPL - Simply Good Foods: Attractive Company Tight Valuation

2024-01-01 02:39:13 ET

Summary

- Simply Good Foods sells nutritional snacks and meal replacements.

- The company has achieved strong revenue growth organically and through the acquisition of Quest, with a CAGR of 22.0% from FY2015 to FY2023.

- The company's long-term target of a 4% to 6% growth seems low compared to the historical performance, setting my expectations above the targeted level.

- For the time being, the valuation seems quite tight, and doesn't necessarily leave attractive upside for investors.

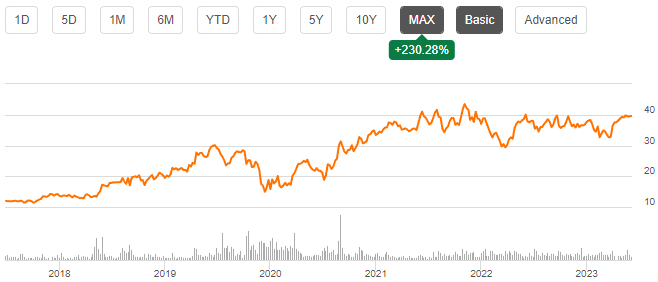

The Simply Good Foods Company ( SMPL ) sells nutritional snacks and meal replacements, such as protein bars, ready-to-drink shakes, and protein chips through partnered retailers and directly to customers. The company operates under Atkins and Quest brand names. After the company went public in 2017, the stock has had a great return. From the first day of trading, the stock has compounded at a CAGR of 20.3%. For the time being, the company doesn’t pay out dividends, as so far cash flows have been spent on select acquisitions.

{kind=link}

Financials

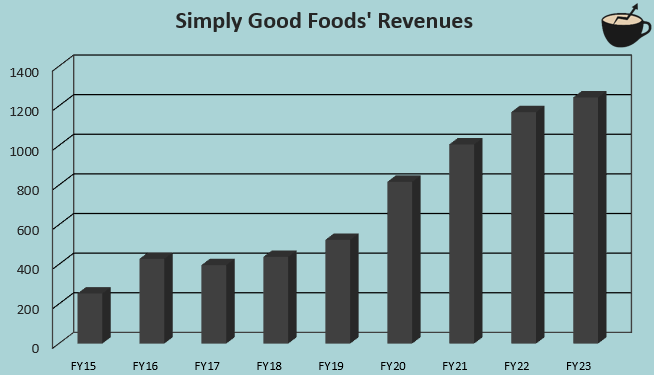

Simply Good Foods has grown its revenues well in the past years; from FY2015 to FY2023, the revenues have had a CAGR of 22.0%. The growth has been achieved organically as well as through the acquisition of Quest Nutrition , one of the company’s two brands, in FY2020 for a consideration of $1.0 billion. Excluding the acquisition, the company’s organic growth seems to have been quite good as well, achieving double-digit growth in multiple years without acquisitions.

Author's Calculation Using Seeking Alpha Data

{kind=link}

The company doesn’t have very ambitious growth targets for the long-term future. In Simply Good Foods’ Q4 earnings presentation , the company relates to a long-term target of a 4% to 6% growth which seems quite low when compared to the achieved performance. In Q4/FY2023, for example, the company achieved a revenue growth of 16.9%, of which 13.4% is attributed to a year-over-year increase in volume. Although the quarter’s growth is boosted by a weak comparison figure in Q4/FY2022 as retailers were decreasing inventories in the prior year’s quarter, the growth seems to support a thesis on higher than a 4% to 6% growth.

With the company’s historical growth, Simply Good Foods has achieved a good amount of efficiencies in SG&A – in FY2015, the company’s SG&A was 33.8% of revenues, whereas currently, the ratio is only 18.3%, providing an incredible amount of operating leverage. Selling products with outsourced production makes the company’s cost structure quite light, as seen in the low SG&A. As a result of the leverage, Simply Good Foods’ EBIT margin has risen from 3.2% in FY2015 and 11.1% in FY2016 to a current level of 16.8% despite slightly lowering gross margins. I believe that some further leverage in margins is still quite likely if revenue growth is achieved.

Upcoming Q1 Results

Simply Good Foods is reporting its Q1/FY2024 results on the 4 th of January. Analysts are expecting revenues of around $308.9 million, corresponding to a year-over-year growth of only 2.7%. The low expectation is in line with the management’s guidance given in the Q4 earnings call; the previous year’s Q1 included sales from a program that is not repeated in FY2024 for Quest, and Atkins’ “New Year, New You” -campaign’s RTD bonus packs are expected to ship largely in Q2 instead of Q1 in the previous year, contributing to a low growth in the quarter. As the management also communicated a low-single digit growth in Q1, the estimate doesn’t seem to have significant chances for a surprise on either side.

Analysts also expect a normalized EPS of $0.42, the same figure as in the previous year. For the entire FY2024, Simply Good Foods is guiding for an increased adjusted EBITDA margin, and in Q4, the company’s EBIT margin increased well with a year-over-year expansion of 2.2 percentage points. In addition, the company communicated that the gross margin is expected to increase in Q1 on a year-over-year basis; I believe that the EPS estimate has some upside.

Prospects Are priced in

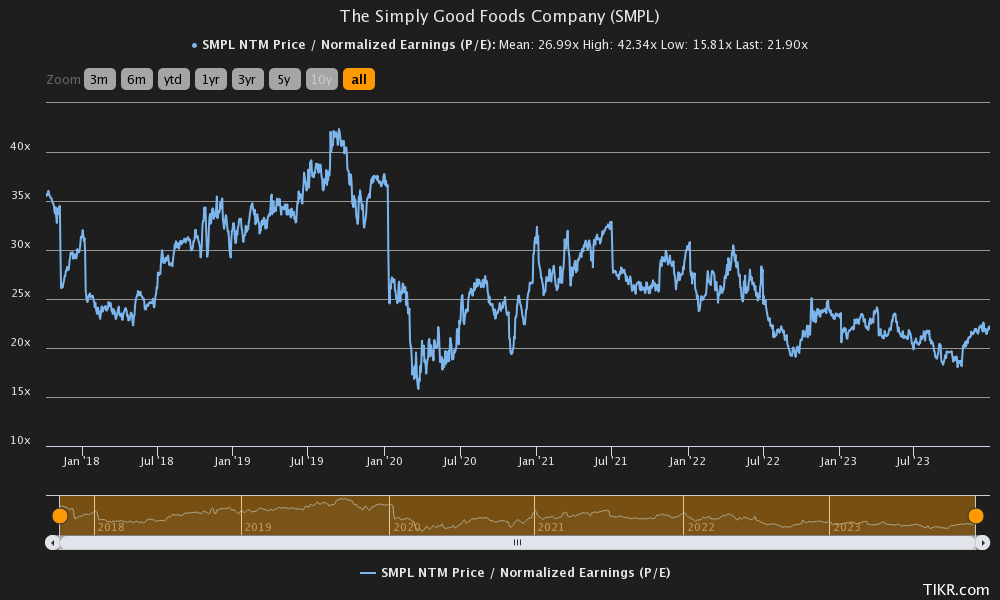

The stock currently trades at a forward P/E multiple of 21.9, somewhat below the historical average of 27.0. The ratio is still quite high, but Simply Good Foods’ stable earnings make the company’s risk profile low, making the required rate of return on the stock lower than average.

{kind=link}

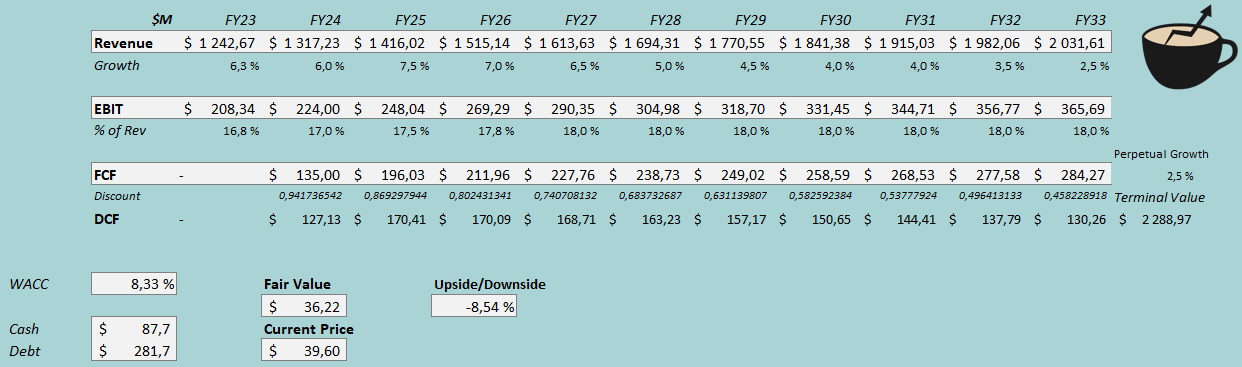

To better contextualize the valuation, I constructed a discounted cash flow model. In the DCF model, I estimate a growth for upcoming years that’s very slightly above the company’s long-term targets – after an FY2024 revenue growth estimate of 6% mostly in line with the company’s guidance, I estimate the growth to accelerate very marginally into 7.5%, slowing down afterward in steps into a perpetual growth of 2.5%. In total, the revenue estimates represent a CAGR of 5.0% from FY2023 to FY2033. For the margins, I estimate very slight leverage from an EBIT margin estimate of 17.0% in FY2024 into a margin of 18.0% from FY2027 forward. The company has quite a low need for capital expenditures due to its light cost structure in the business model; I estimate the cash flow conversion to remain very good even with the estimated growth.

With the mentioned estimates along with a cost of capital of 8.33%, the DCF model estimates Simply Good Foods’ fair value at $36.22, around 9% below the stock price at the time of writing. The stock seems to be valued quite fairly considering Simply Good Foods’ historically proven performance, although the model does estimate a very modest downside - the valuation seems quite tight at the moment. The company could in my opinion improve its capital structure though the cost of capital could potentially come down by improving the estimated fair value.

DCF Model (Author's Calculation)

{kind=link}

The used weighted average cost of capital is derived from a capital asset pricing model:

CAPM (Author's Calculation)

In Q4, Simply Good Foods had $6.9 million in interest expenses. With the company’s current amount of interest-bearing debt, Simply Good Foods’ annualized interest rate comes up to a high figure of 9.76%. I believe that the company could potentially have an opportunity to optimize its use of debt – the high interest and quite a low amount of interest-bearing debt seem non-optimal for a defensive stock such as Simply Good Foods. For the time being, I still use the high interest rate and quite a low debt-to-equity ratio estimate of 10% for the long term.

For the risk-free rate on the cost of equity side, I use the United States 10-year bond yield of 3.87% . The equity risk premium of 5.91% is Professor Aswath Damodaran’s latest estimate for the United States, made in July. Yahoo Finance estimates Simply Good Foods’s beta at a figure of 0.73 . Finally, I add a small liquidity premium of 0.25%, crafting a cost of equity of 8.43% and a WACC of 8.33%.

Takeaway

Simply Good Foods has so far been a great investment. The company has a light cost structure and has proven a great track record of growth with organic efforts and the acquisition of Quest. The given long-term plan of a 4% to 6% growth seems like an unambitious target with proven growth, and I estimate that the company is likely to achieve some more growth than the management seems to anticipate. At the moment, the stock’s financial prospects seem to be priced in, though, as my DCF model estimates a very minor downside. For the time being, I have a hold rating for the stock.

For further details see:

Simply Good Foods: Attractive Company, Tight Valuation