SMPL - Simply Good Foods: Near-Term Challenges Are Fading

2023-07-27 15:10:33 ET

Summary

- The company's revenue growth is expected to benefit from volume recovery and better sell-in and sell-out alignment.

- The company's volume is expected to recover sequentially as comparisons ease.

- Margins are expected to recover as inflation moderates and the company sees improved sales leverage and volume growth.

Investment Thesis

The Simply Good Foods Company's ( SMPL ) revenue growth is expected to benefit from volume recovery due to easier comparisons, and better alignment of sell-in and sell-out as inventory destocking has been completed, giving a boost to reorders to meet the good end market demand. On the margins front, the company should benefit from moderating inflation and improving volume leverage. This should help in the sequential recovery of margins over the coming quarters. A more favorable cost environment in the coming years should also help in margin expansion for the company. The company is trading below its historical average forward P/E and given the volume and margin recovery prospects, I continue to have a buy rating on the stock.

Revenue Analysis And Outlook

In my previous article , I discussed Simply Good Food's medium to long-term growth prospects benefiting from good demand in the nutritional snacking category. I also noted that the near-term challenges from retail inventory destocking which has adversely impacted revenue growth in the recent few quarters should begin to ease moving forward.

The company reported its third quarter of fiscal 2023 earnings since then, and management noted that demand for the nutritional snacking category remained at healthy levels. SMPL's total retail takeaway (Point of Sales) in the combined measured and unmeasured channels grew by 13% YoY, led by good demand momentum at the Quest brand which grew retail takeaway in the combined measured and unmeasured channels by 24% YoY. However, the company continued to see volume decline and lower sell-in, as retailers continued their inventory destocking. This resulted in a 2.6% YoY increase in sales to $324.8 million, reflecting a 7.4 percentage point benefit from price increases, which was partially offset by a 4.6 percentage point decline in volume.

SMPL's Historical Revenue (Company Data, GS Analytics Research)

Looking forward, I expect volume to recover sequentially moving forward as comparisons ease.

For a quick recap, in fiscal 2022, SMPL's top-line growth momentum was meaningfully impacted by retail inventory adjustments. The retailers and customers built excess inventory in the first three quarters of fiscal 2022 in order to address supply chain challenges. However, in the fourth quarter of FY2022, the company saw a normalization of demand post-pandemic, and consumers also tightened their pockets in an inflationary environment. This led to retailers drawing down their excess inventory to meet the sell-out, resulting in retail inventory destocking, which continued in the first three quarters of fiscal 2023 as well. So, the inventory built in the initial three quarters of FY2022 and inventory destocking in the first three quarters of the current fiscal year, made the comparison tough for the company's sales growth in the last few quarters as sell-in was lower compared to retail takeaway.

However, as we move to the fourth quarter of fiscal 2023, the company should see more favorable comparisons. This is because SMPL will be lapping the period during which retail inventory destocking occurred, making comparisons less challenging. So, the pain of inventory destocking should gradually become less of a headwind moving forward and sell-in should start aligning with retail takeaway. This should aid volume recovery going forward and contribute to sales growth.

Moreover, over the last few quarters, many of SMPL's snacking categories were also impacted by consumer sensitivity to price increases. In an inflationary environment, companies across the board have increased prices to protect margins and consumers have begun tightening their pockets. This led to volume declines. However, the good news moving forward is that management is seeing inflation moving in the right direction and further price increases are unlikely in the near term. This should give more room for volume recovery. Further, end-market demand continues to stay at a good level as the company saw an 11% YoY growth in retail takeaway for the first three weeks of the fourth quarter. So volume should start recovering from the fourth quarter of fiscal 2023 due to good demand, easing comparisons, and less impact of price increases.

Margin Analysis And Outlook

In the third quarter of 2023, SMPL continued to experience higher commodity and packaging costs, which adversely impacted gross margin. This was partially offset by the carryover impact of price increases. As a result, the gross margin declined by 80 bps YoY to 34.6%. However, the adjusted EBITDA margin increased by 50 bps year-over-year to 17.2% due to benefits realized from SG&A cost control measures.

SMPL's Historical Gross Margin and Adjusted EBITDA Margin (Company Data, GS Analytics Research)

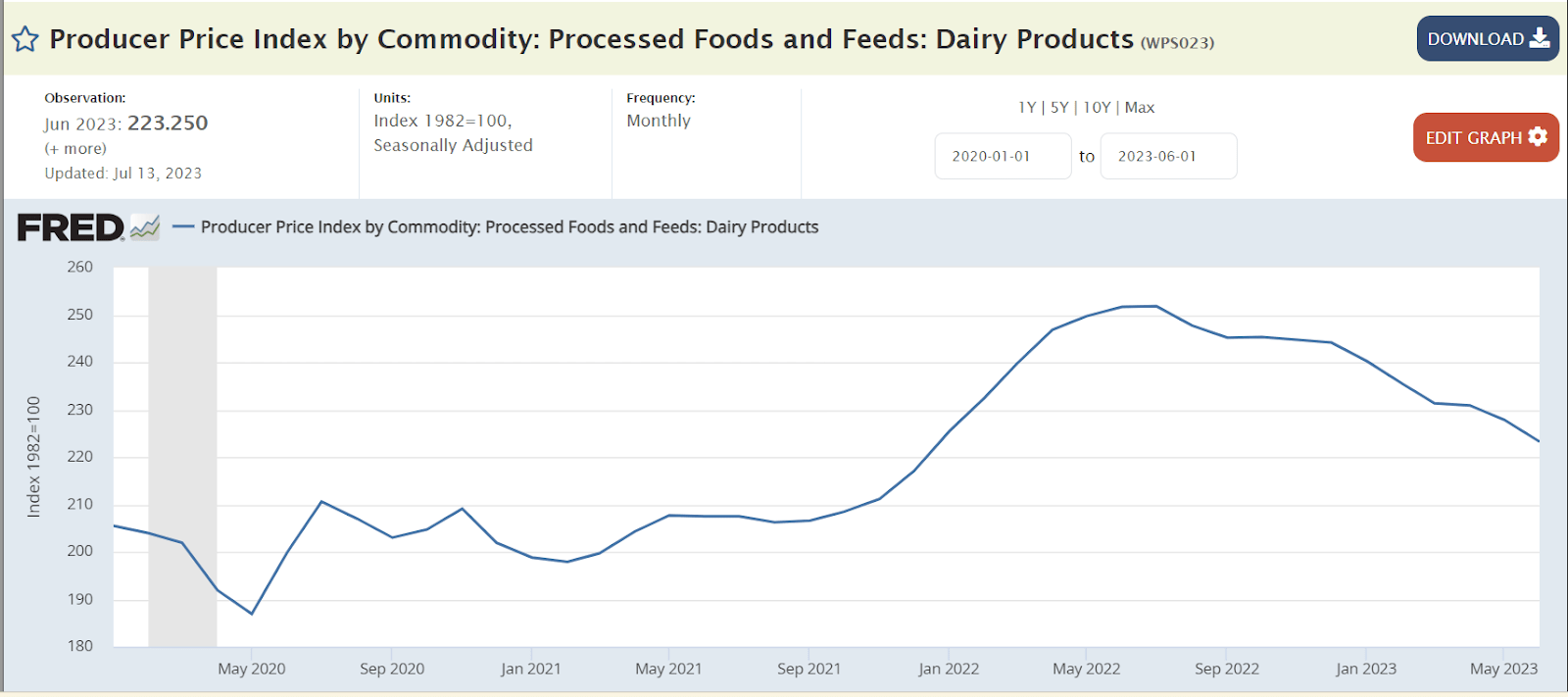

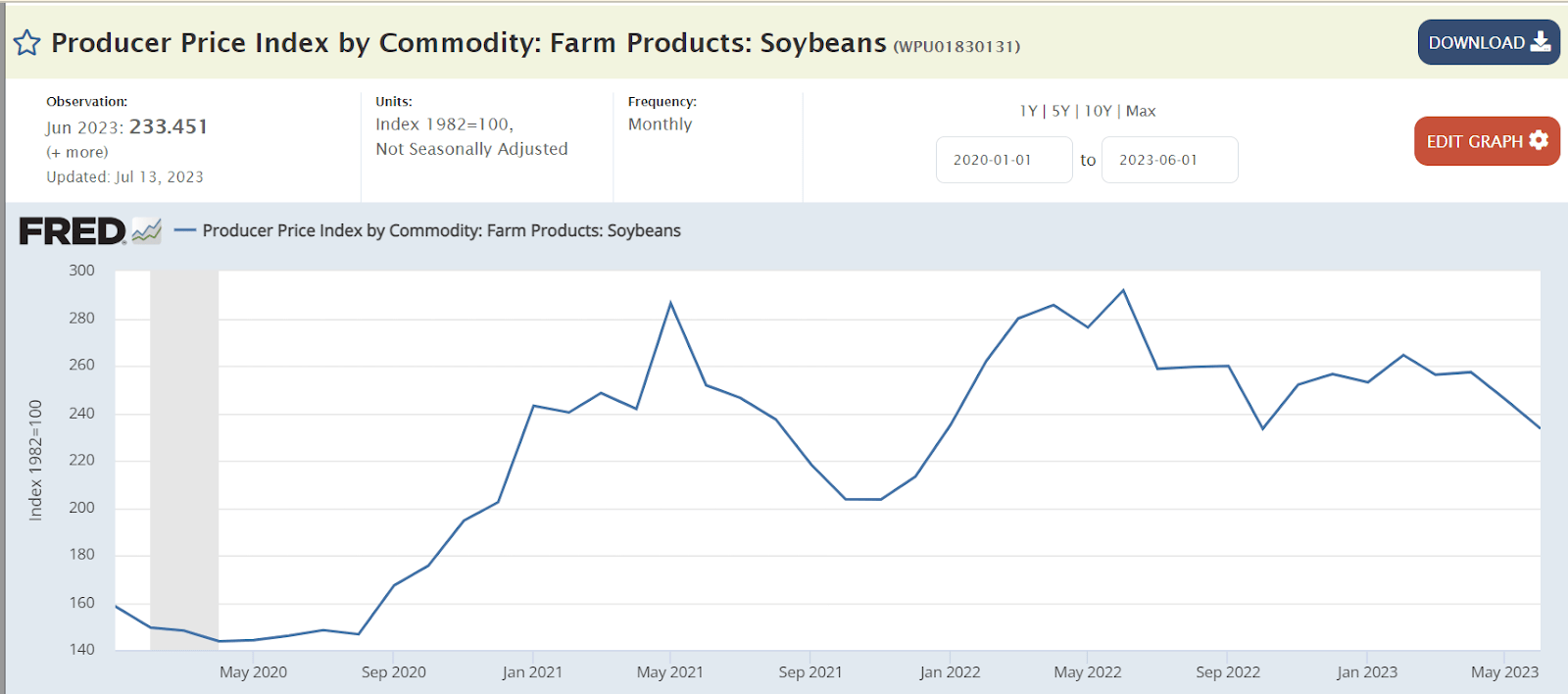

Looking forward, I expect margins to start recovering. While the ingredients and packaging costs are expected to remain elevated year-over-year, management has noted a sequential moderation in commodity costs. The company's major raw material is protein, which it gets from dairy products and soy products. Both of these protein sources are sequentially moderating in price, indicating a favorable cost environment moving forward.

PPI Dairy Products (FRED) PPI Soyabeans (FRED)

{kind=link}

{kind=link}

Moreover, quarter-by-quarter the company is also seeing margin pressure decline as inflationary costs are becoming less of a drag on margins. In the first quarter of fiscal 2023, margins declined by 450 bps YoY while the recent quarter saw only a decline of 80 bps.

SMPL Y/Y Gross Margins (Q3 FY2023 Earnings Call Presentation)

For the fourth quarter, management expects a flat year-over-year margin growth. As the company moves forward in fiscal 2024, further moderation of inflation should help in sequential as well as year-over-year recovery of margins.

Moreover, as the retail inventory level destocking ends, the company should see an increase in reorders, helping volume growth and improving sales leverage in the coming years. This should also help in margin recovery moving forward. Hence, I remain optimistic about the margin growth prospects for SMPL in the coming years.

Valuation and Conclusion

The Simply Good Food Company is currently trading at 23.68x based on the FY23 consensus EPS estimate of $1.62, and 21.08x based on the FY24 consensus EPS estimate of $1.82. The company's valuation is below its historical 5-year average forward P/E ratio of 28.77x. The company has good growth prospects and headwinds from retail inventory adjustments and a tough cost environment also seem to be fading away as we move into the next year. So, the company should see good top line and bottom line recovery in the coming fiscal year. Given good growth prospects and a reasonable valuation, I continue to rate the stock buy.

For further details see:

Simply Good Foods: Near-Term Challenges Are Fading