SMPL - Simply Good Foods: Poised For Growth Initiate At Buy

2023-10-08 23:07:24 ET

Summary

- Simply Good Foods faced margin pressures and slowing revenue growth due to inflationary headwinds and higher input costs.

- We believe Q4 is likely to be better as a result of positive data from Nielsen, and the gross margin is likely to improve due to moderating input cost inflation.

- The stock is undervalued compared to peers, and the company's long-term prospects in the active nutrition category support a Buy rating.

Investment Thesis

The Simply Good Foods (SMPL) faced a rocky year as a result of consistent margin pressures due to higher input costs. In addition, its revenue growth slowed from sustainable double digits during the previous years to a flattish growth during the year due to significant pressure in international markets as a result of inflationary headwinds along with an adverse impact from licensing its Quest frozen pizza business to Bellisio, which also owns the license for Atkin's frozen meal business.

The stock experienced P/E derating as a result of decelerating sales growth and bottom line pressures. However, we believe the long-term trajectory for SMPL remains well poised for sustainable high-single digit growth underpinned by the strength in its Quest brand along with the recovery seen in its Atkins brand. We believe the worst is likely behind and ascribe a Buy rating on the basis of 1) attractive positioning in the growing active nutrition market 2) brand reinvestments in Atkin to drive recovery 3) moderating input cost inflation and 4) comfortable valuation.

Company Background

The Simply Good Foods was formed in 2017 when a SPAC, Conyers Park Acquisition Corp., merged with NCP-ATK Holdings, whose primary asset was the Atkins brand. It is primarily a consumer packaged foods company engaged in selling a wide range of wellness and nutrition products such as protein bars, snack bars, RTD shakes, low-carb diets, and weight loss management plans. Prior to its merger with Conyers Park, the Atkins business acquired Wellness Foods, a Canadian company selling protein-rich and low-sugar protein under the brand 'SimplyProtein'. Post its listing in 2017, it acquired the 'Quest' brand in 2019 focused on convenient nutrition products.

Strong Q3 and Q4 Earnings Preview

SMPL reported strong Q3 earnings with in line revenues with gross margins of 36.7%, declining 80 bps YoY, still ahead of the management guidance and beating consensus estimates. US retail takeaway jumped about 11% YoY which outperformed the sales growth as a result of inventory build last year. Adj. EBITDA margins improved 50 bps as a result of strict cost control partially offset by a decrease in gross margins. In addition, the firm reaffirmed its full-year outlook and maintained the sales growth to be higher than its 4-6% long-term target. Management expects Q4 gross margins to improve sequentially as a result of moderating cost inflation with the bulk of its impact expected to be realised in Q4. While the company is down a few items in shelf space, the company maintained that they are working to fill that void during Spring and Fall which may take time but alluded to the fact that Atkins distribution was still up 7% YTD.

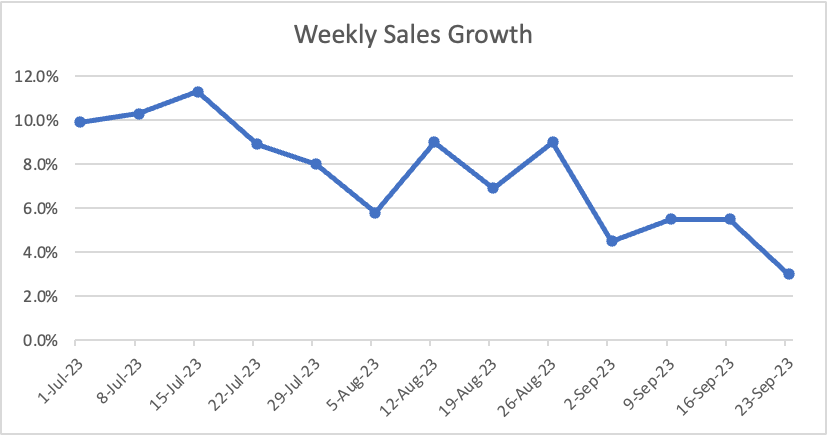

According to Nielsen data, Packaged foods players reported a decelerating sales growth as the benefit of the pricing action wanes with flattish volumes. However, SMPL reported a strong start to the quarter, despite the growth decelerating through the quarter, still implying a weekly average growth of 7.5% driven by continued outperformance of its Quest brand along with recovery of its Atkins brand as a result of improvement in its distribution points.

{kind=link}

We expect the company to end the year with organic sales growth of 6.5% - 7.0% ahead of the company's long-term goals driven by strong weekly sales growth. In addition, we expect FY24 sales growth to be near the higher end of the guidance driven by the outperformance of its Quest brand along with recovery in Atkins and further expect gross margins to improve by 150 - 200 bps as a result of input cost moderation and lapping peak pressure in gross margins it observed during the current year. In addition, SG&A expenses are likely to slightly increase by 50 - 100 bps as a result of wage hike inflation and higher selling and advertising spends, which we believe would have an Adj. EBITDA margin expansion by ~100 bps.

Valuation

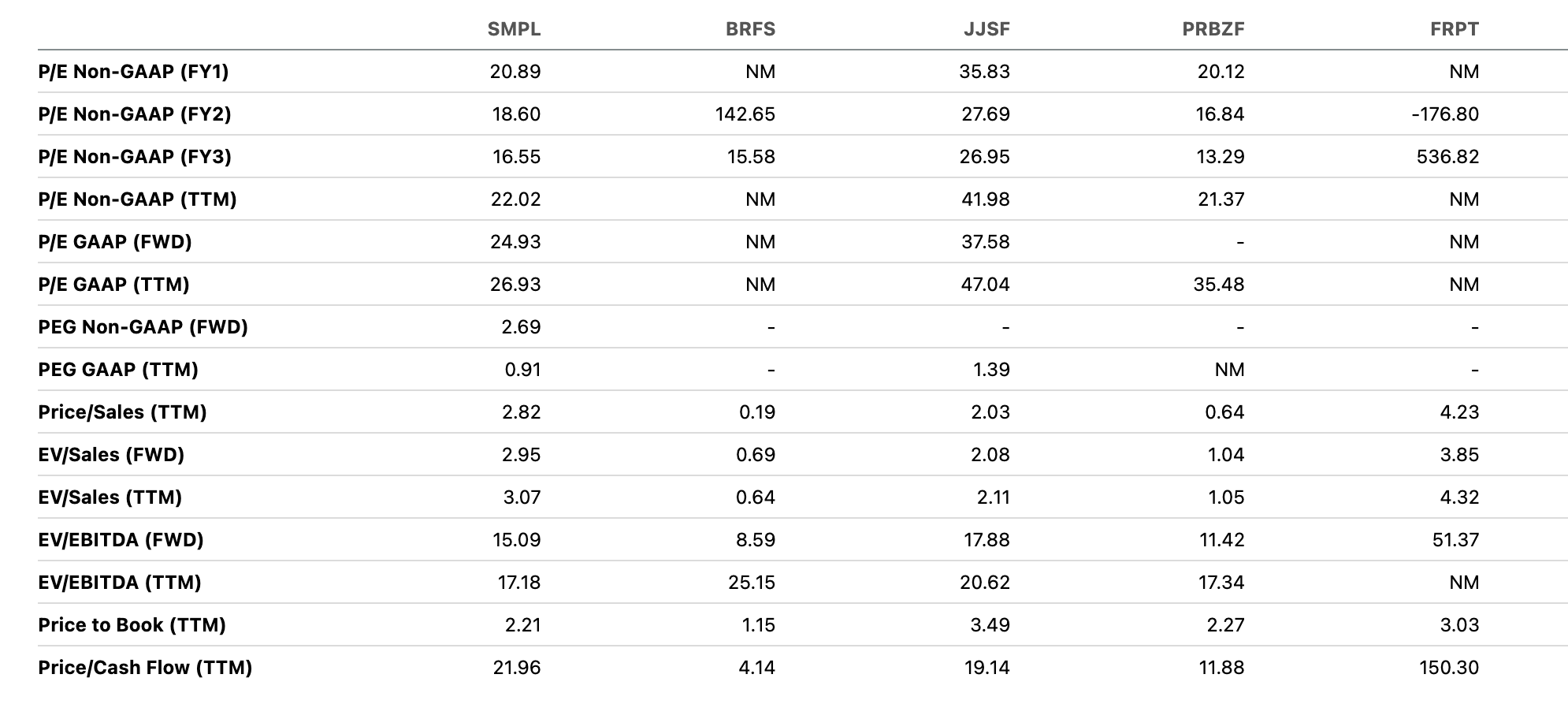

SMPL trades at 18.6x P/ FY24E, which still ranks at the bottom of the quartile underlying the relative cheapness, as well as it trades below its long-term historical average of 25x.

{kind=link}

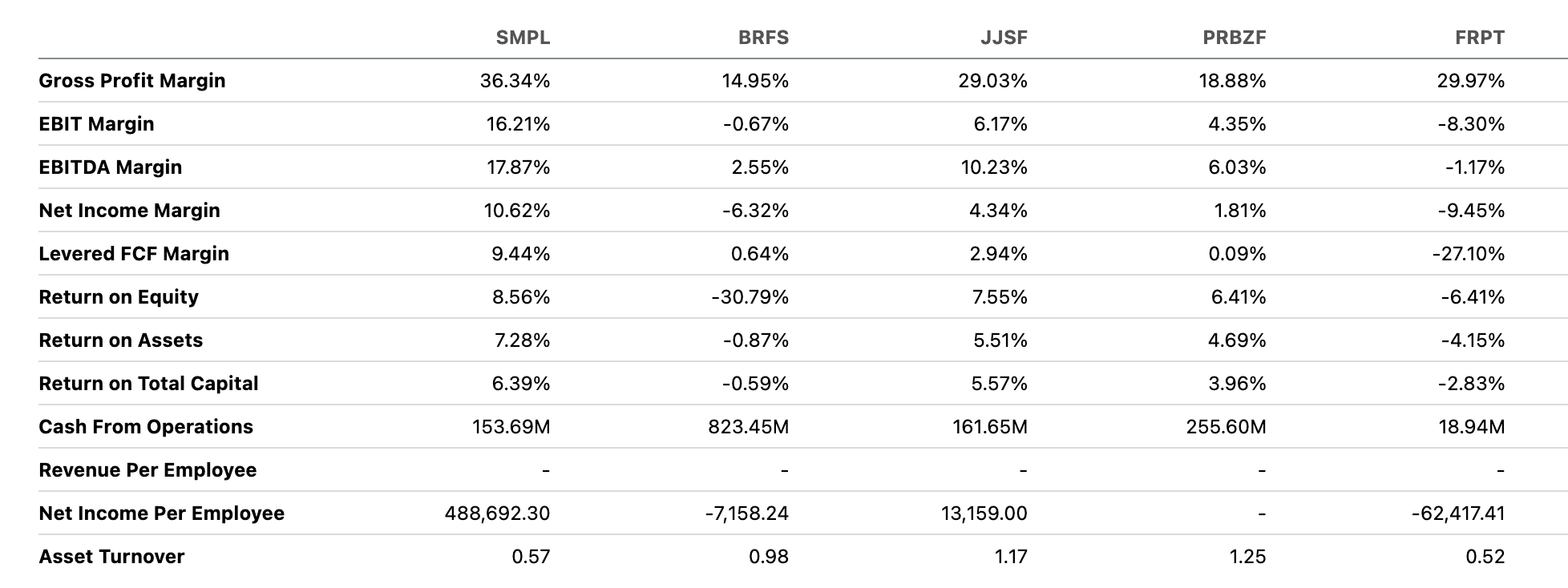

Despite the relative undervaluation, it has robust operating metrics with strong growth, top-of-the-class margins, and strong return ratios compared to its peers.

{kind=link}

We remain positive on the long-term trajectory of the packaged foods market particularly within the snacking category and the increasing focus of the consumers on a healthy diet with the recovery in its Atkins brand. We also remain positive on its offering of weight loss meal plans as a result of growing obesity in the US, with over 40% of the population becoming overweight .

We initiate with a Buy underpinned by HSD organic growth on the back of strength in Quest brand with Atkins likely to play catch-up and potential margin expansion. We ascribe a target price of $42 at a P/ FY24E of 22x (in line with its peer average) and below its long-term average considering the current tough macro backdrop.

Risks to Rating

Risks to rating include

1) Category growth for healthy snack bars could decline and consumers would look to trade down as a result of a tough macro backdrop and decline in consumer spends

2) Competitive pressures may intensify which can lead to higher-than-expected promotion spends and can impact top line and bottom line growth

3) Inflation is expected to moderate going forward, however, sticky inflation and lesser than expected decline in input costs can lead to pressure in gross margins

Final Thoughts

SMPL had a volatile year with share prices remaining flat as a result of higher cost inflation which has led to a squeeze in gross margins with a decelerating top line growth. However, the company reported positive results in Q3 and we believe the newly appointed CEO, Geoff Tanner, has taken steps in the right direction heading into FY24. We remain positive on the long-term prospects of the packaged foods category within the healthy snacks/protein bars category. In addition, its relative undervaluation compared to its peers despite strong operating metrics warrants a Buy. We ascribe a target price of $42 at a P/ FY24E of 22x.

For further details see:

Simply Good Foods: Poised For Growth, Initiate At Buy