SMPL - Simply Good Foods: Positioned Exceptionally For The Nutritional Revolution

2023-10-16 21:35:41 ET

Summary

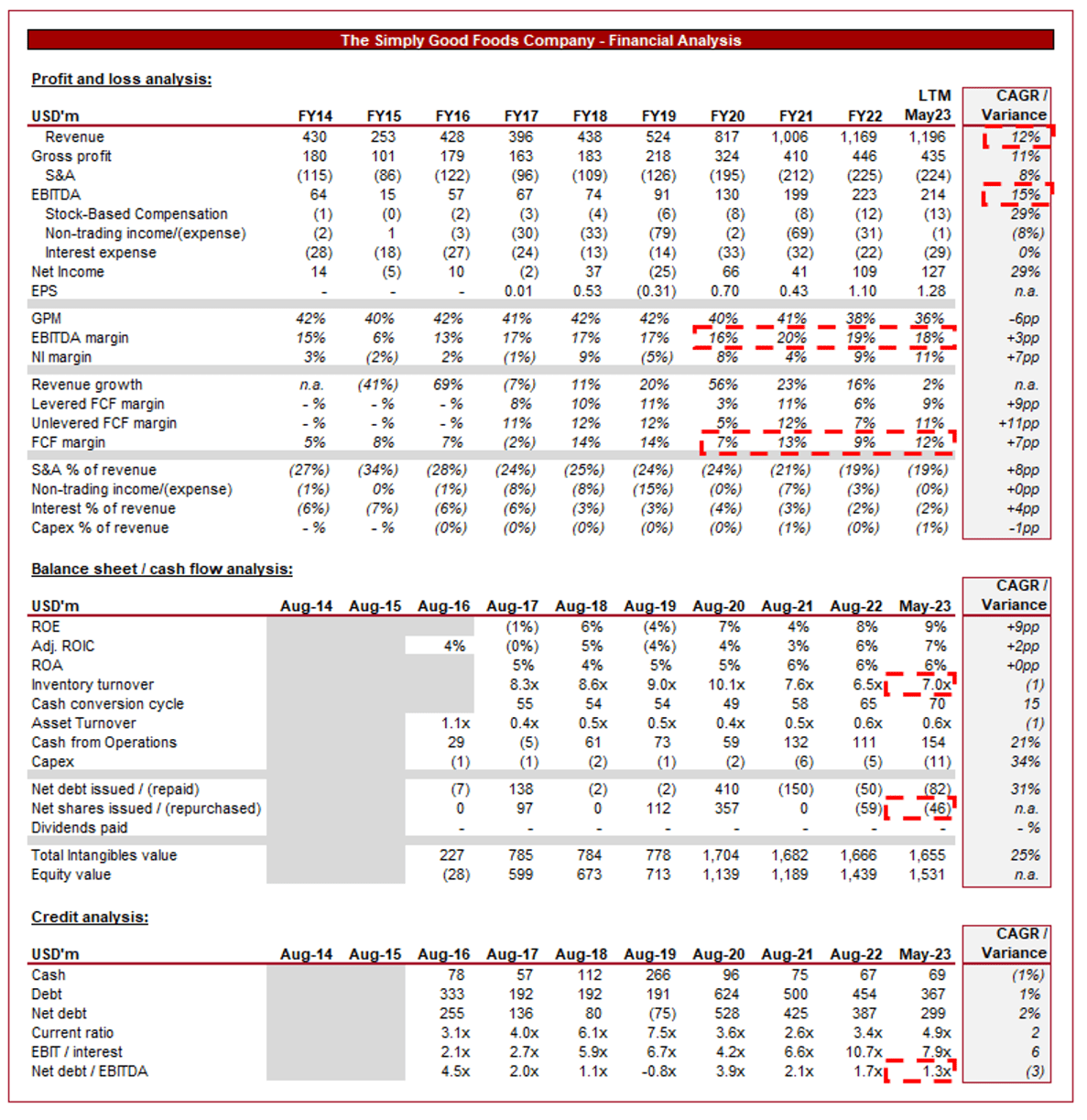

- SMPL’s revenue has grown incredibly well, with a CAGR of +12% during the last decade. EBITDA has exceeded this, with a CAGR of +15%.

- The company has achieved good organic growth through its focus on healthy premium products. Consumers increasingly care about the content of their foods and how it impacts their lifestyle.

- We see this as a long-term growth trend, with products such as those that are high in protein expected to outgrow the wider packaged food industry.

- This has allowed SMPL to exceed its and earn superior margins. There is a good runway to maintain this outperformance, with the expansion of its Quest brand.

- SMPL is trading at an unwarranted discount to its historical average and without a sufficient premium to its peers. At a FCF yield of 7.0%, we consider the stock attractively priced.

Investment thesis

Our current investment thesis is:

- SMPL represents a quality opportunity to gain exposure to the nutritional revolution globally. Consumers are increasingly aware of the ingredients in the foods they eat, the impact on their health, and the long-term implications. The response is greater spending on “clean” products and also those that assist with exercise (protein-based goods). SMPL owns two strong brands in this sector, one that is on an impressive growth trajectory with a long runway.

- From a financial perspective, SMPL has grown at a superior rate to its peers, while operating with consistently better margins. At a FCF-M >10% and defensible margins, we see superior returns with SMPL.

- Despite this, the company is trading at a ~21% discount to its historical average, while only trading at a ~16% premium to its peers. Both factors imply strong upside in our view.

Company description

The Simply Good Foods Company ( SMPL ) is a prominent player in the health and wellness food industry. Known for its commitment to providing nutritious and wholesome products, the company operates with a mission to enhance the well-being of its consumers.

Share price

SMPL’s share price performance since 2017 has been impressive, with over 150% returns compared to ~80% by the S&P. This is a reflection of its current growth trajectory, in conjunction with a reasonable valuation.

Financial analysis

{kind=link}

Presented above are SMPL's financial results.

Revenue & Commercial Factors

SMPL’s revenue has grown at an impressive +12% CAGR during the last decade, with broadly consistent growth since 2018. This was accelerated during the post-pandemic period, before slowing in the LTM. EBITDA has exceeded this, with a CAGR of +15%.

Business Model

The SMPL business focuses on sourcing and offering premium organic products, currently under its two brands Atkins and Quest. Its emphasis on quality attracts health-conscious consumers who are willing to pay a premium for organic and natural food items.

By ensuring the highest quality standards with ingredients, taste, and macros, the company has established trust among customers, leading to repeat business and positive word-of-mouth marketing. This credibility has positioned it as a leading option with retailers.

SMPL offers a diverse range of organic products, including ready-to-drink shakes, bars, confectionary treats, frozen meals, etc. This variety allows for brand development and growth opportunities through reach. Management has placed a strong emphasis on product development, seeking to further expand in the coming years.

The company has invested in a user-friendly online platform, allowing customers to conveniently order organic products from the comfort of their homes. This allows SMPL to tap into its core customer base which is regularly purchasing, allowing SMPL to improve unit economics. From a customer perspective, offering home delivery services and a seamless online shopping experience caters to the modern consumer's need for convenience and accessibility.

Nutritional Snack Industry:

The healthy snacks segment is forecast to grow well in the coming years, with a CAGR of +6.7% into 2030. The following trends are expected to be key growth drivers:

- Growing Health Consciousness - As global awareness of health and nutrition rises, more consumers are seeking healthier food options, especially organic products. We consider this more than just a trend, with scope for a fundamental shift in consumer habits. We believe SMPL is perfectly positioned to maximize its growth from this as a pure-play option.

- Gym Culture and Protein Consumption- In conjunction with this, there has been a growing interest in exercise and specific diets to partner this. This has contributed to increased demand for protein products, such as shakes and snacks.

- Premium Quality and Trust - ****With the focus on health, consumers are more stringent about the ingredients and process of creation. Providing premium-quality organic products will be the most successful segment, regardless of cost, as it will help build trust among customers. Trust is a vital factor in the healthy food industry.

- Convenience in the Digital Age - ****In the age of online shopping, providing a seamless and convenient online buying experience critical to driving growth and reducing reliance on retailers and their strategies.

- Diversification - Expanding product offerings to respond to new trends and changing tastes will be critical to maintaining growth. Key examples we see are vegan, keto, or gluten-free.

- Global Expansion - For strong brands, such as those owned by SMPL, entering untapped international markets represents a key opportunity to improve growth, particularly through utilizing existing retailer relationships, such as with Amazon (AMZN).

We believe SMPL is positioned perfectly to respond to almost every trend identified, in many cases from a leading market position. With the brand diversification it now has, a proactive attitude to product innovation, and heavy exposure to the specific growth segments identified, we are highly bullish. The company faces competition from competitors including General Mills ( GIS ) (Nature Valley), Kellogg's ( K ) (RXBAR), and Clif Bar & Company, but we believe its pure-play nature is a major benefit.

Margin

{kind=link}

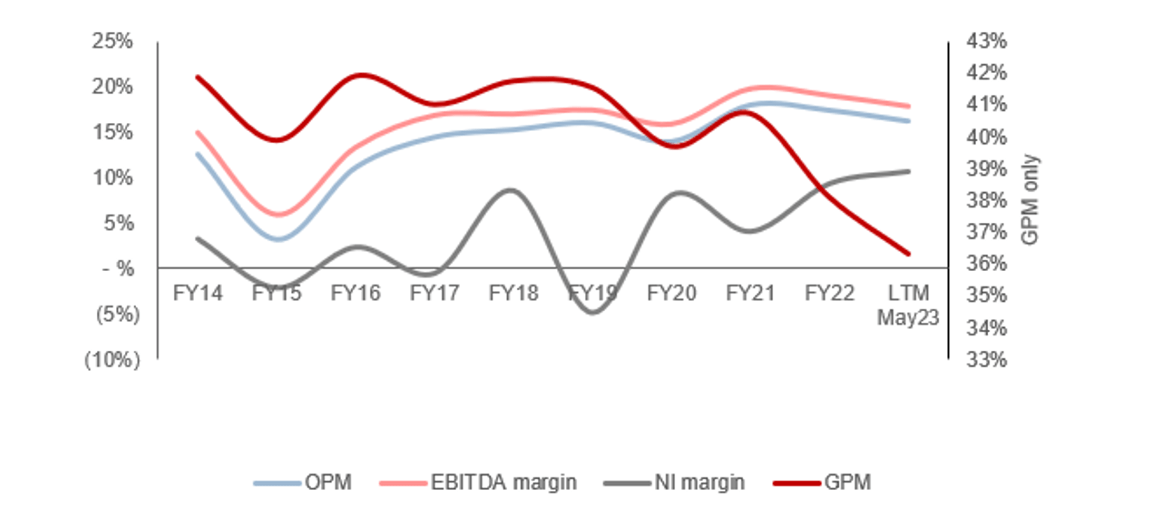

SMPL’s margins have improved over the historical period, with EBITDA-M increasing from 15% in FY14 to 18% in LTM May23. The improvement is a reflection of the company’s growing scale and its development along the business lifecycle. SMPL is investing less in its marketing effects, while benefiting from economies of scale on a GPM level.

Between FY18 and FY21, margin improvement had slowed, suggesting the business has likely reached its normalized level.

Quarterly results

SMPL’s recent performance has slowed relative to its 3Y trajectory, with top-line revenue growth of +5.5%, +7.0%, +0.0%, and +2.6% in the last four quarters. In conjunction with this, margins have slipped, with EBITDA-M falling below 17.0% for the first time in several years.

This is a reflection of the current macroeconomic environment in our view, with elevated interest rates and inflation contributing to softening spending across various segments to protect finances. SMPL’s products are priced at a premium to much of its alternatives, owing to a higher quality and focus on popular segments (high protein, etc.).

We believe demand will continue to be muted in the coming quarters, as the focus remains on keeping inflation under control. This said, due to the popularity of its products and the general upward trajectory through market awareness, we do not believe demand should turn negative.

Key takeaways from its most recent quarter are:

- Retail takeaway growth exceeded net sales change primarily due to customer inventory build in the prior year.

- The Quest brand’s momentum continues to be strong, with a strategic focus on building awareness of this brand. Management believes household penetration remains noticeably below many of its peers, indicating a long runway for growth.

- GPM was better than expected and is potentially normalizing. This is due to input cost moderation and a significant easing of inflationary pressures. The belief is that there is still further room for gains.

- In addition to the growth of the Quest brand, the focus is on bar innovation and regaining the distribution capacity lost for snack bars in the Atkins brand.

- Additionally, there will be continued investment in accelerating the e-commerce segment of the business, as well as strengthening relationships with retail customers.

- SMPL reaffirms its previous FY23 outlook and believes net sales will increase at a rate higher than the 4-6% long-term algorithm.

Balance sheet & Cash Flows

SMPL’s balance sheet is clean. The company currently has a ND/EBITDA ratio of 1.3x, leaving sufficient scope for further debt if required and no immediate concerns.

Inventory turnover remains below its pre-pandemic level but has improved since Aug22. This represents a positive trajectory that can contribute to an improvement in its FCF conversion. We expect this to occur as Atkins’ distributions improve.

Regardless, SMPL’s FCF margin is extremely strong, allowing the business to deleverage its balance sheet and distribute to shareholders. We expect deleveraging to decline in the coming years, contributing to greater distribution potential.

{kind=link}

Outlook

{kind=link}

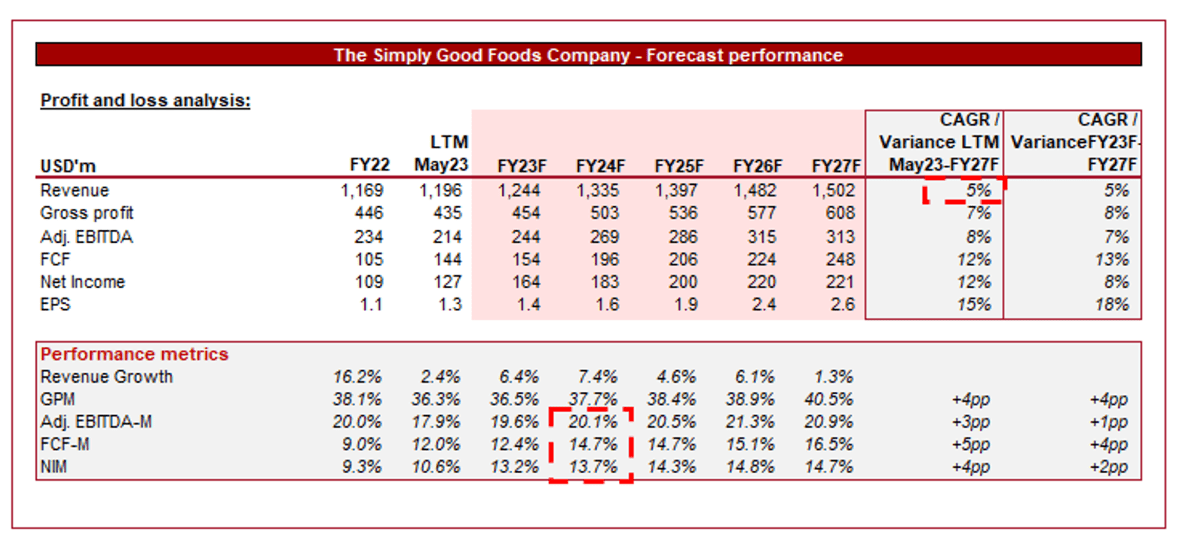

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting a softening of its historical growth rate, aligning with Management’s view of 5-6% as a long-term trajectory. In conjunction with this, margins are expected to normalize at the existing level, with minimal improvement.

We broadly agree with these forecasts. Following a significant growth period, which involves M&A, it is inevitable that the company’s growth trajectory will slow. We consider ~5% to be a strong level if it is sustainable, particularly due to its unit economics.

Industry analysis

Packaged Foods and Meats Stocks (Seeking Alpha)

{kind=link}

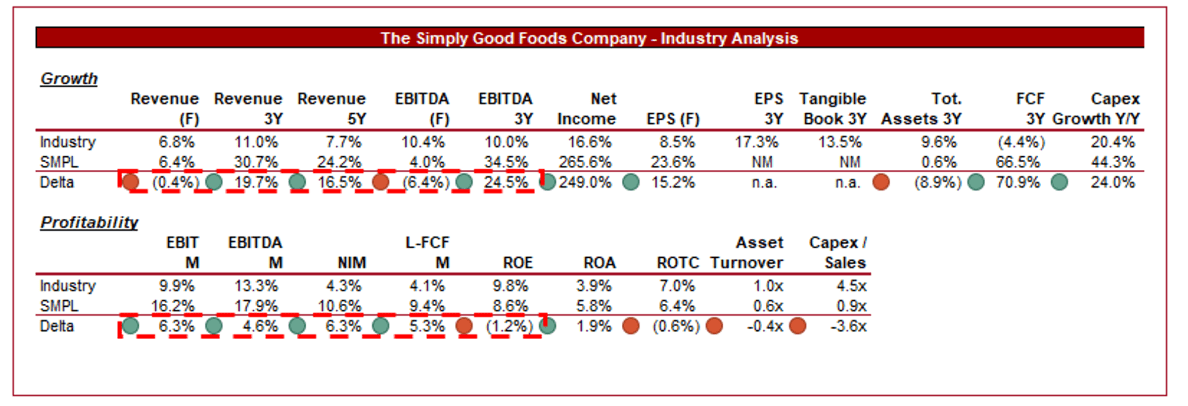

Presented above is a comparison of SMPL's growth and profitability to the average of its industry, as defined by Seeking Alpha (42 companies).

SMPL is performing exceptionally well relative to its peers. The company’s revenue and profitability growth have significantly outperformed its peers, both on a 3Y and 5Y basis. This is a reflection of the segment it targets within the packaged food industry, with an impressive upward trajectory (that we consider sustainable). It should be noted that the slowdown is expected to bring the business below average, although we are not overly concerned due to its margins.

SMPL’s margins are its key strength we feel, given the maturity of the industry (and thus the ability to materially deviate from existing levels). SMPL has a +4.6% EBITDA-M delta and a +5.3% LFCF-M delta. This is attributable again to the niche it operates within, in conjunction with strong brand development and brand awareness. Given Management believes further penetration is possible (which we concur with), we believe these margins are defensible.

Valuation

{kind=link}

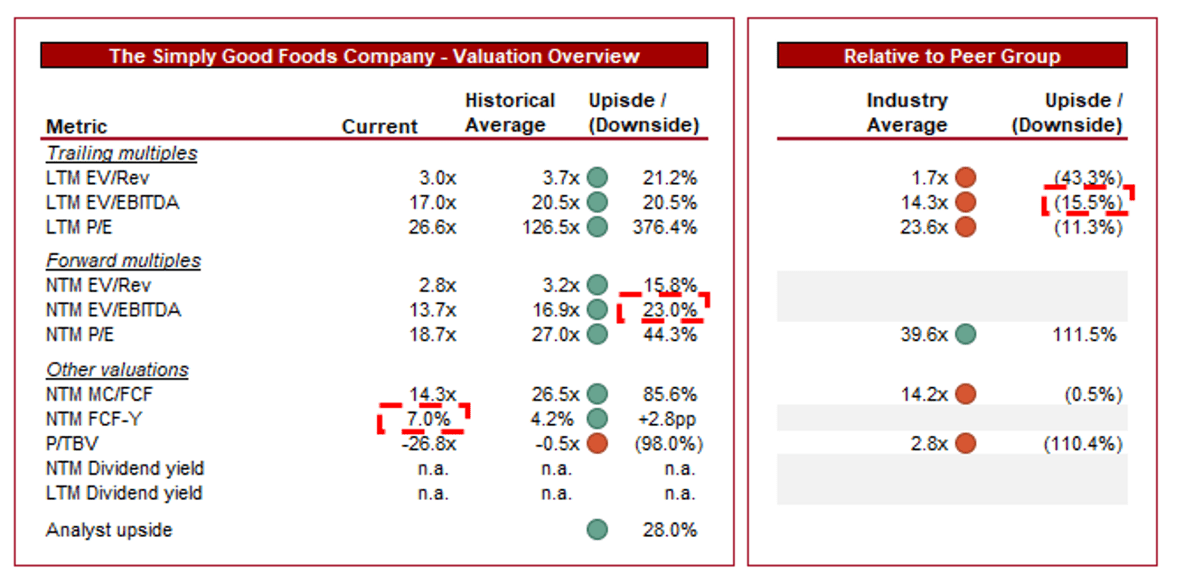

SMPL is currently trading at 17x LTM EBITDA and 14x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is difficult to justify beyond a very small level (~5%) in our view. The key argument is a decline in its growth trajectory, however, we would counter argue that its existing scale is far more impressive. During the decade, the risk of growth derailment through competition was much higher, while now it has two well-established brands, one of which still has substantial room for growth. This, we believe, is illustrated in its NTM FCF yield, which is substantially higher (~7%) than its historical average (~4.2%).

Further, SMPL is trading at a ~16% premium to its peers on a NTM EBITDA basis and ~0.5% on a NTM FCF basis. We believe this premium does not sufficiently reflect the company’s current superiority. Importantly, we consider its margins to be defensible and thus further upside should reflect its future returns.

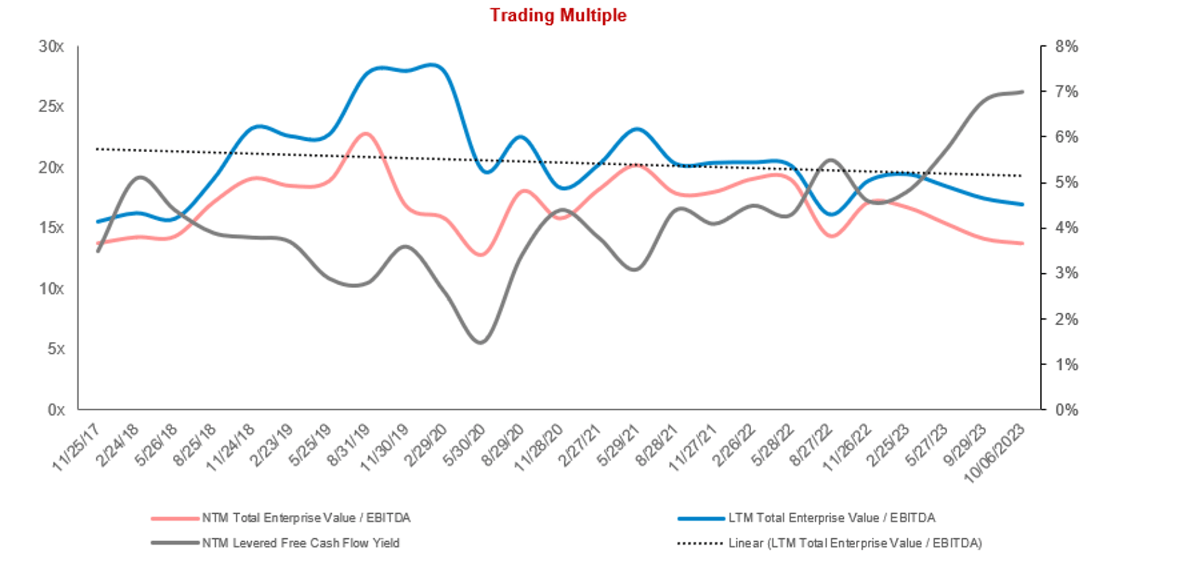

As the following illustrates, SMPL’s valuation has fallen below its historical trajectory.

Trading evolution (Capital IQ)

{kind=link}

Key risks with our thesis

The risks to our current thesis are:

- Failure to adapt to changing consumer preferences - Current trends are toward protein products such as shakes and bars. This may not always be the case and so ensuring continued new product launches is critical.

- Increased competition - SMPL’s current margins will attract new market entrants, which have the potential to cause margin dilution. This is why brand development is critical.

Final thoughts

SMPL is a high-quality business in our view. The company operates a strong business model. that is underpinned by two strong brands that have an assortment of products that are in high demand. Health consciousness is not a fad but a long-term trend, with many turning to exercise, clean products, and generally better eating habits. SMPL is a pure-play option to partake in this growth.

From a financial perspective, the company is extremely attractive in itself, with no material threat to its margins. Despite this and the commercial consideration, SMPL’s valuation does not sufficiently reflect the upside we see.

For further details see:

Simply Good Foods: Positioned Exceptionally For The Nutritional Revolution